Since the 2015 election, the Liberal government has made two major adjustments to federal programs targeted at children and youth. First, the uniform payment to every family with children was replaced by the new Canada Child Benefit, a benefit worth more to lower income families and withheld from the wealthy. In a similar vein, the government announced it would phase out some of the existing tax credits for post-secondary education (PSE), which were available to all families with taxable income, so it could use the savings to increase the value of grants for students from low-income families.

Still, the work to improve support to children from low-income families is not done – 1 million low-income children each year are still missing out on the Canada Learning Bond.

The Canada Education Savings Program

The federal government runs two main programs to promote access to PSE (not including tax credits). The most widely recognized is the Canada Student Loans Program, which provides loans and grants to students with financial needs.

In addition, since 1972, the federal government has encouraged families to prepare for the cost of PSE by providing a tax incentive to parents who put aside education savings for their children in a Registered Education Savings Plan (RESP). Since 1998, this tax incentive has been enhanced through the provision of savings grants. In 2013-14, the total cost of these tax incentives and grants – which together form the Canada Education Savings Program (CESP) – was $1.1 billion.

There are now three different education savings grants on offer.

The Canada Education Savings Grant (CESG) is a matching contribution to an RESP paid by the government, and equal to 20 percent of the first $2,500 contributed annually. The CESG is available to any RESP holder, regardless of family income.

In 2004, in order to encourage more lowand middle-income families to save for PSE, the federal government introduced two additional grants. The first is the Additional Canada Education Savings Grant (A-CESG), which provides an additional contribution of 20 percent of the first $500 contributed annually to an RESP by low-income families, or an additional contribution of 10 percent of the first $500 contributed annually to an RESP by middle-income families.

The second incentive introduced in 2004 was the Canada Learning Bond, which is available to lower-income families. While the Canada Learning Bond is also paid into an RESP, its distinctive feature is that it does not require the family to make its own RESP contribution. The government makes a payment of $500 in the child’s first year of eligibility, and then pays $100 for every subsequent year during which the child is eligible, up until the child reaches the age of 15 (to a maximum amount of $2,000). The Canada Learning Bond is not, therefore, a matching grant, but rather a seed grant, which ensures that there are some savings for PSE available to children from lower-income families, regardless of how much their parents are able to set aside themselves.

Education savings grants and the increased use of RESPs

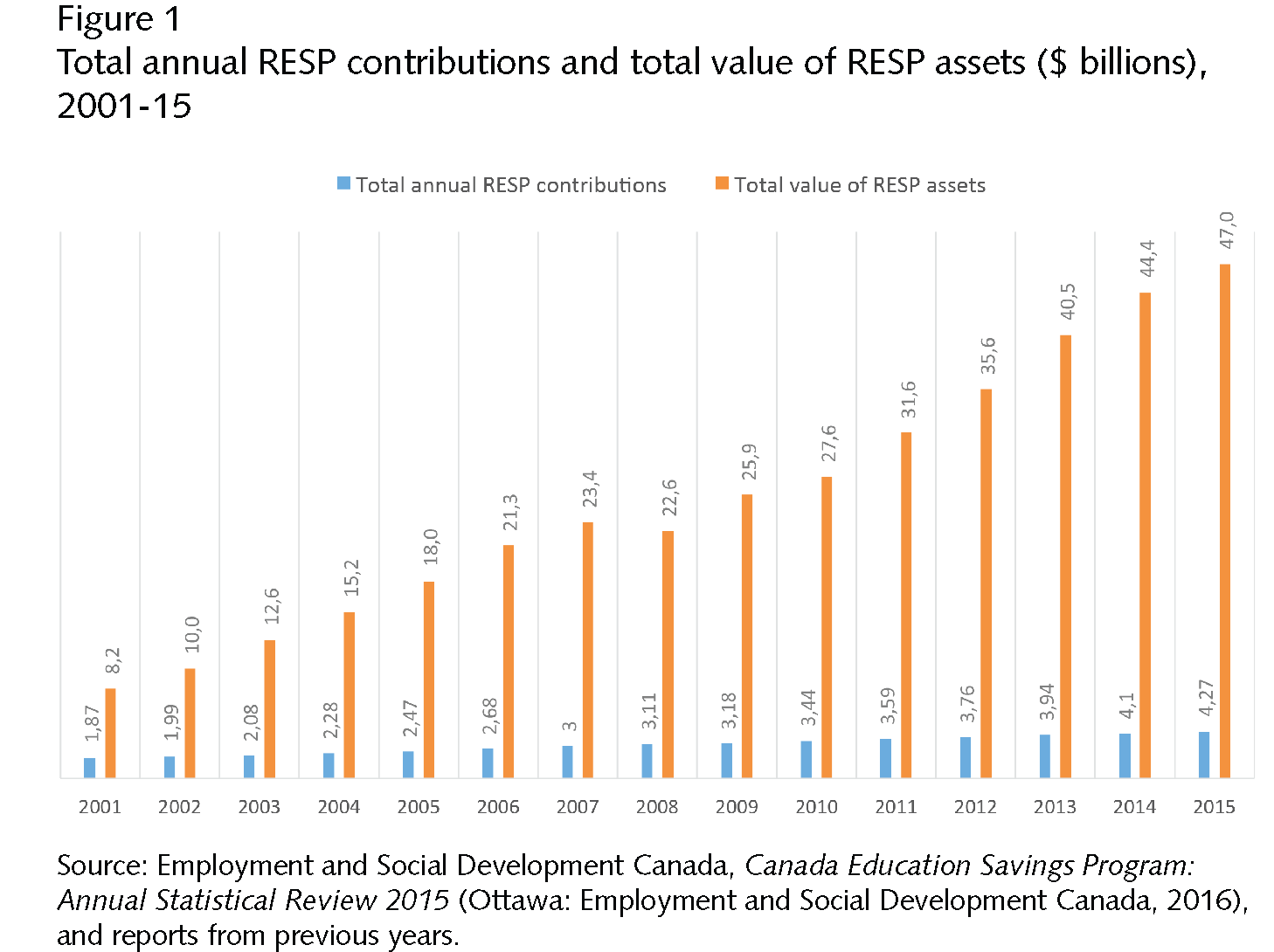

The introduction of the education savings grants was followed by a dramatic increase in the use of RESPs. The portion of Canadian families with children under the age of 18 who are saving for their child’s post-secondary studies through an RESP rose from fewer than one in five at the start of the 2000s to over half today. As more families open RESPs, the total amount of savings contributed annually and the total accumulated savings have both grown dramatically. In 2015, Canadians contributed over $4 billion to their RESPs, and the total value of all RESPs reached over $47 billion (figure 1). The total amount accumulated in RESPs has doubled since 2008 and quadrupled since 2002.

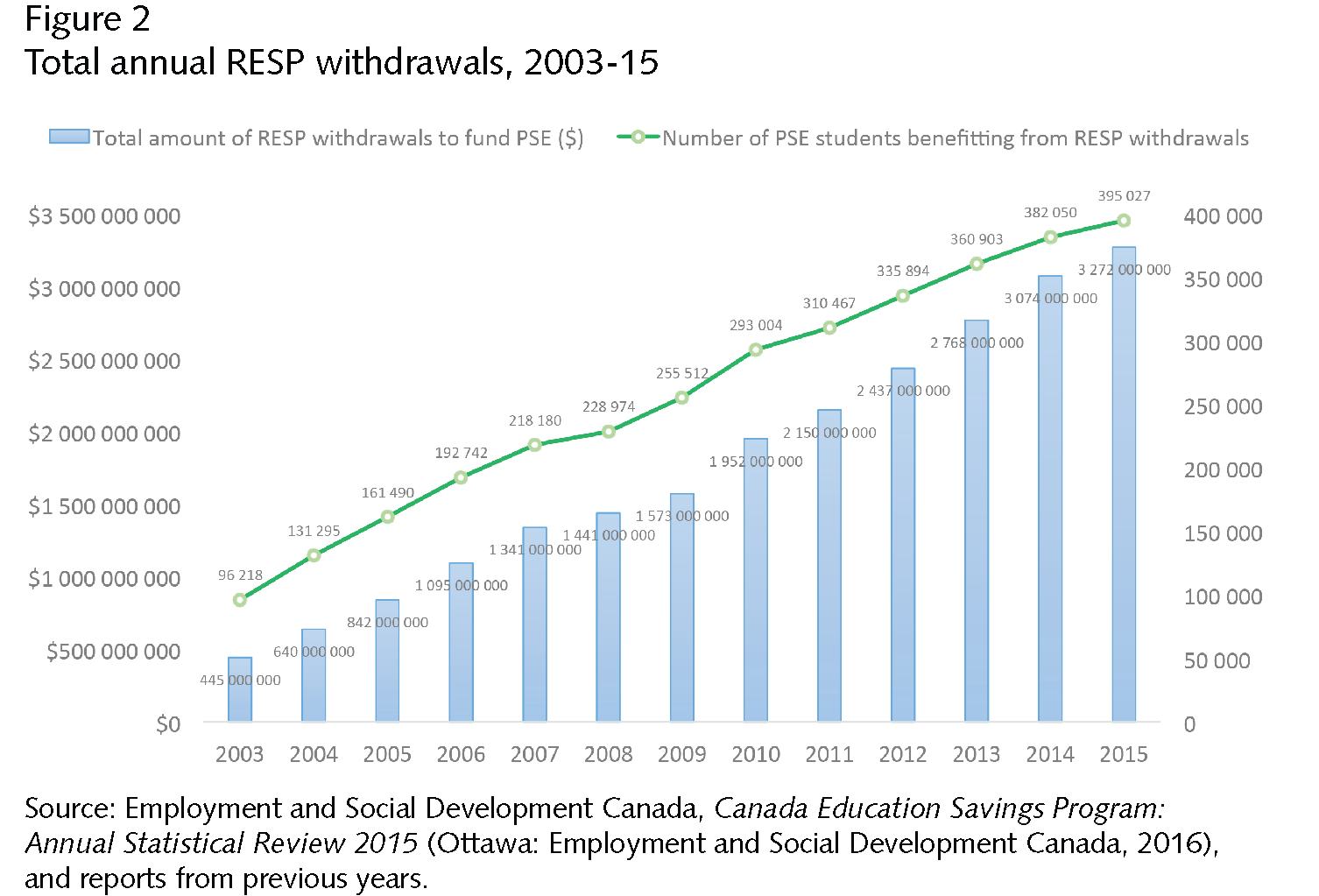

Perhaps more importantly, withdrawals from RESPs have become an increasingly important source of funding for post-secondary students. The proportion of students making use of RESP withdrawals to fund their current year of study has grown from only a handful (fewer than 1 percent) in 1998 to close to one in five today. In 2015, withdrawals surpassed $3.2 billion – 395,027 post-secondary students made use of funds that had been set aside for them in their RESPs, with an average amount of $8,283 per student (enough at least to cover the average undergraduate university tuition for one year) (figure 2). Students as a whole are now receiving as much financial support from RESP withdrawals as they are from Canada student loans. In short, whereas RESPs were once a peripheral source of funding accessed by only a very small proportion of students, they have now become an integral component of the student financing system.

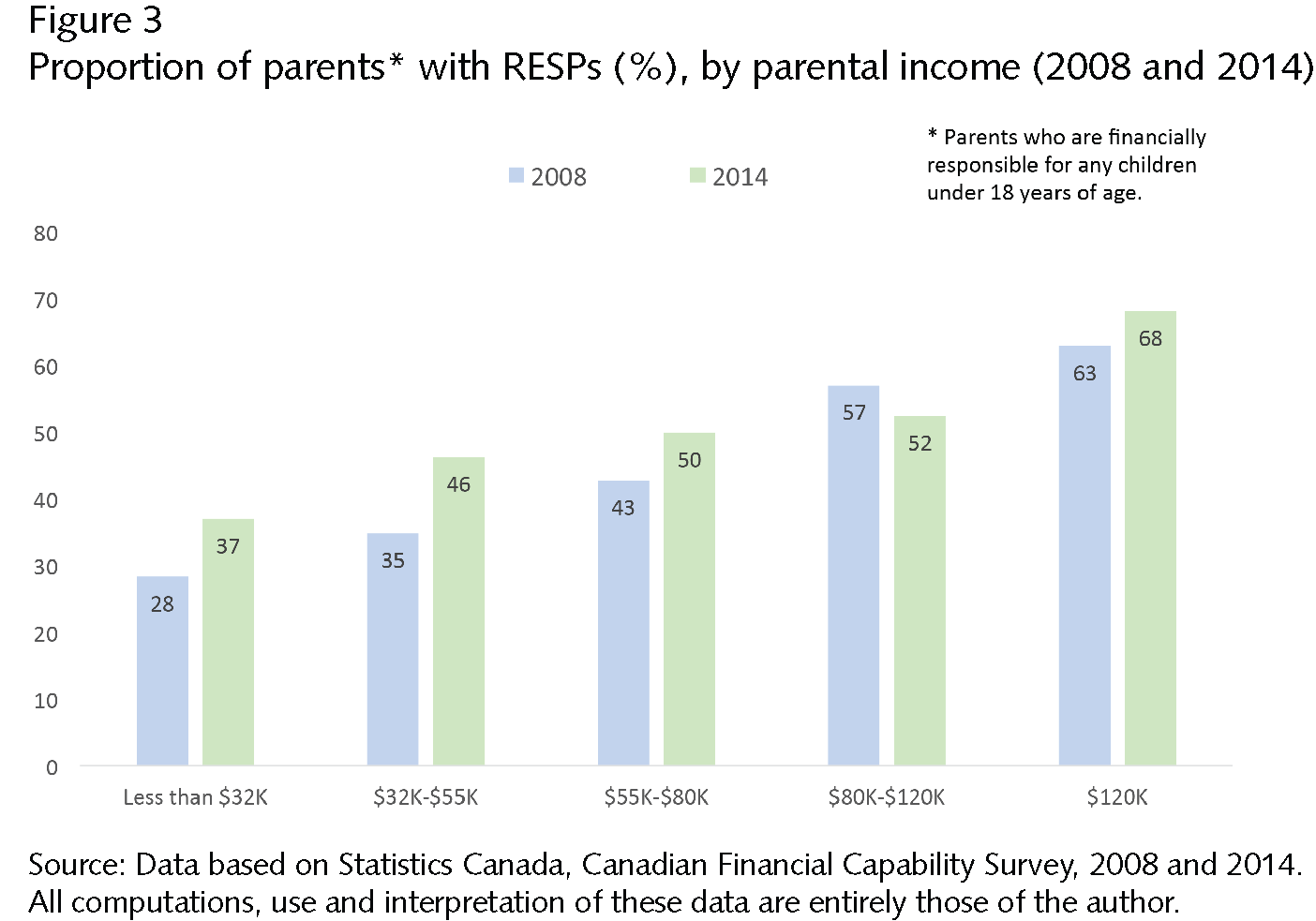

The primary complaint about RESPs and the associated savings grants as a means of financing PSE is that their benefits accrue disproportionately to wealthier families. In 2014, according to Statistics Canada, 68 percent of parents with children under the age of 18 and with annual incomes over $120,000 had an RESP; this compares with 46 percent of those with incomes between $32,000 and $55,000, and only 37 percent of those with incomes of less than $32,000 (figure 3).

This means that far fewer than half of families with incomes in the lower range, which entitles them to receive the A-CESG and Canada Learning Bond savings incentive grants, can in fact receive them; the remainder cannot because they do not have the prerequisite RESP. In addition, the fact that higher-income families are more likely than lower-income families to have RESPs also means that they are more likely to receive a Canada Education Savings Grant, since these are available to any RESP holder, regardless of family income.

The Canada Learning Bond

The proportion of lower-income families who have opened an RESP and who are therefore able to receive the three savings grants (the CESG, the A-CESG and the Canada Learning Bond) has been steadily increasing. Between 2008 and 2014, for instance, the proportion of families in the lowest-income group that had an RESP increased by a rate of 31 percent, compared with a rate of 8 percent for those in the highestincome group.

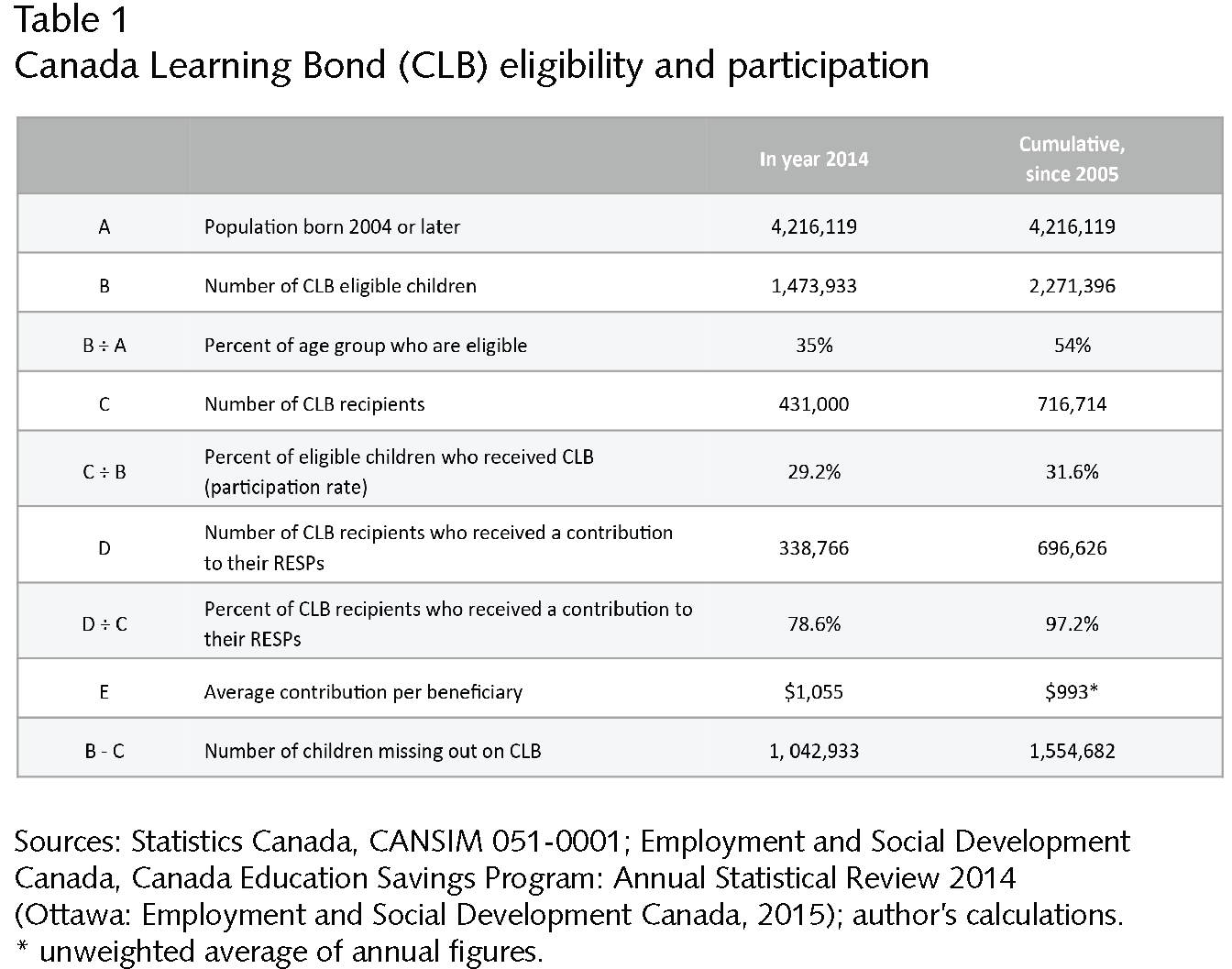

The take-up rate for the Canada Learning Bond has also been rising steadily since its inception in 2005. By 2014, just under 32 percent of the children of eligible age whose family’s income fell below the threshold (approximately $45,000) in at least one year since they were born – and who thus had been eligible for the Canada Learning Bond at least once – had in fact received it at least once. This is about double the proportion in 2008. Of the children who were eligible in 2014, 29 percent received the Canada Learning Bond in that year.

There are two major obstacles to receiving the Canada Learning Bond. The first is the requirement that eligible children have an RESP already opened in their name; as we have seen, the majority of low-income families do not have one. Second, even those that have an RESP need to take a further step and apply specifically for the Canada Learning Bond through the financial institution that holds the RESP. In fact, almost one in four low-income RESP holders who are eligible for the Canada Learning Bond do not receive it because the appropriate application has not been completed.

The end result is that of the 2,271,396 children who have been eligible for the Canada Learning Bond over the lifetime of the program only 716,714 have benefited, meaning over 1.5 million children have missed out. In 2014, 1,473,933 children were eligible, but only 431,000 received it, meaning over 1 million children missed out in that year alone. While the Canada Learning Bond has had the potential to benefit over half of all children born since January 1, 2004, only 17 percent have in fact benefited so far (table 1).

The case for education savings grants

With all the difficulties that the Canada Education Savings Program has had in reaching the families who stand to benefit the most from it, it would be tempting to think that it is ripe for scrapping. However, reforming the program is a better option.

To see why, we need to recall what we have learned since 2000 – in large part through the research commissioned by the Canada Millennium Scholarship Foundation – about the factors that affect access to PSE. Much of this research has focused on the barriers facing students from low-income families, and it’s not just about the availability of funds at high school graduation. Lower family income at an earlier age also has an impact. These students might receive less academic encouragement and support, have access to fewer resources and opportunities to help with learning inside and outside school, and have different expectations placed on them, and have different aspirations of their own in terms of careers and PSE. For this reason, they face multiple inter-related barriers to accessing PSE, some financial, but others relating to academic preparation and achievement, or motivation and encouragement.

Information is also an issue. Most students make decisions about whether or not to pursue PSE – and particularly university education – well before the end of high school; in many cases, these decisions are made in middle school or junior high school. In making those early decisions, students are more likely to look for information and advice to their parents than to other sources, including teachers and guidance counsellors. Unfortunately, neither students nor their families are necessarily well informed about issues related to the cost of PSE and the different means of financing it. And so, decisions about PSE tend to be made within families, before the end of high school, and often in the absence of good information.

The implication of these findings is that policies designed to encourage more students, and particularly more students from disadvantaged backgrounds, to continue their studies past high school and into post-secondary education need to focus long before the student turns 18. Access to education policies need to include so-called “early interventions” – strategies to help reframe the way in which students and their families approach education, from an early age. It is in this context that the importance of PSE savings incentives programs becomes clearer.

There is, of course, a straightforward practical and mathematical advantage for any family to start to save early. Small amounts saved each year are enough to trigger the matching savings grants and generate returns through compounding interest. As a result, an amount such as $240 (or $20 per month) invested each year over a child’s first 18 years generates almost $2,000 more in total savings than the same total amount saved just in the child’s high school years.

Increasingly, however, researchers and advocates have begun to argue that the importance of programs to encourage families to start saving early for their child’s post-secondary education goes far beyond the help they provide lower-income families in building up the financial resources that children will eventually rely on to pay for their studies.

The very existence of an education savings fund can help to reframe the conversation about educational opportunities within the household. Because parents are saving for their children’s post-secondary education, they will begin to convey to their children the expectation that they will make it to college or university as well as the sense that a post-secondary education is not financially out of reach; this, in turn, will affect how children approach school and their futures.

Some also argue that the presence of an account can help improve financial literacy, trigger greater awareness of the costs and means of financing PSE, and establish greater familiarity and comfort with financial institutions. In other words, these programs can have a positive impact, not only — or even not mainly — because they can increase the amount of money available to pay for a child’s PSE, but also because they can change children’s and parents’ attitudes and behaviour long before children are old enough to enroll in (and pay for) college or university.

Do education savings incentives programs work?

An emerging body of evidence is lending support to these arguments and the theory that lies behind the introduction and expansion of PSE savings incentives programs. There are three main types of evidence to consider.

First, the data show that low-income families can and do save for PSE, and that savings incentive programs can play a role in encouraging such savings. In the case of low-income families who had opened an RESP and received the Canada Learning Bond in 2015, just under 80 percent made their own contribution to their RESP that year, even though no contribution was required. In the case of families who have ever received the Canada Learning Bond, almost all (98 percent) made a contribution to their RESP at least once. A more in-depth analysis of the government’s database of RESP holders confirms that the introduction of the A-CESG and Canada Learning Bond helped to kick start savings among lowand middle-income families, by reducing the average child’s age at which parents opened an RESP, and by increasing the amounts contributed to RESPs and the total amounts saved.

Second, we have known for some time that there is a correlation between savings and education outcomes. Students who have had education savings set aside for them are more likely to access PSE, and particularly university; they also transition more quickly from high school to post-secondary education to graduation and are less likely to drop out. The problem is we do not know whether this correlation extends to causation; that is, whether the existence of education savings contributes to better education outcomes, or whether these students are bound to succeed, regardless of how early their families start savings for their education or how much savings they manage to accumulate.

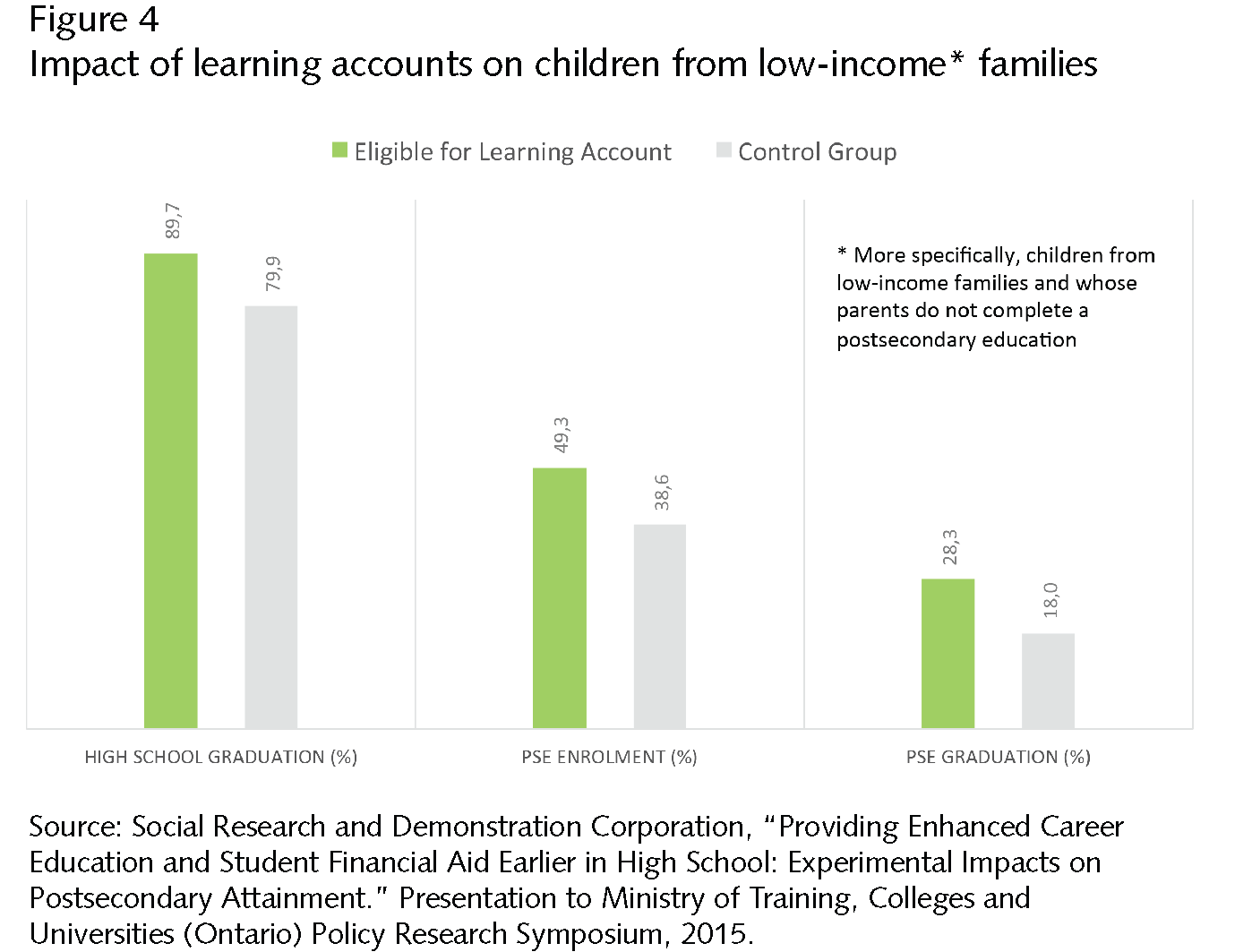

This is why the third and most recent type of evidence – from the Future to Discover experiment in New Brunswick – is so compelling. Future to Discover tested the effectiveness of two different approaches designed to encourage more students, particularly those from less advantaged families, to pursue PSE. One of these approaches was a financial incentive called a learning account, which was a promise to students at the end of grade 9 that they could access up to $8,000 should they graduate from high school and undertake post-secondary studies. Students received a deposit of $2,000 in a virtual account at the end of grades 10 and 11 and another $4,000 upon graduation from high school, funds they could access once they were enrolled in a post-secondary program. The impact of the learning accounts was measured using a random-assignment design, which means that the education outcomes of students who had funds for PSE set aside for them in their learning accounts were compared with those of students in a control group who did not have access to these funds.

The most recent follow-up study of the Future to Discover students has demonstrated that the learning accounts had an impact. Looking particularly at students from low-income families and whose parents did not complete PSE, the study shows that those offered access to the learning accounts were significantly more likely to graduate from high school, enrol in PSE, and graduate from PSE (figure 4). In fact, the graduation rate of the groups offered the learning accounts was one-and-a-half times higher than that of the control group.

It’s important to note that the learning accounts were not family savings; they were funds provided by a third party (the Canada Millennium Scholarship Foundation) that were set aside for high school students in a virtual account for the sole purpose of funding PSE. The Future to Discover experiment nonetheless provides the evidence that those who have access to funds set aside for PSE will, because of the existence of the funds, be more likely to access and complete PSE. This evidence as to the effect of funds set aside for a child’s PSE is among the strongest available to date, not only in Canada, but internationally.

Improve take-up of the Canada Learning Bond

The understanding that policies designed to improve access to PSE must focus on students long before the end of high school, coupled with the growing evidence about the relationship between education savings and access, suggests that best option is to seek to improve the Canada Education Savings Program by raising the take-up rates among lowand middle-income families, and, in particular, addressing the problem of the 1 million children in low-income families who currently miss out on the Canada Learning Bond each year.

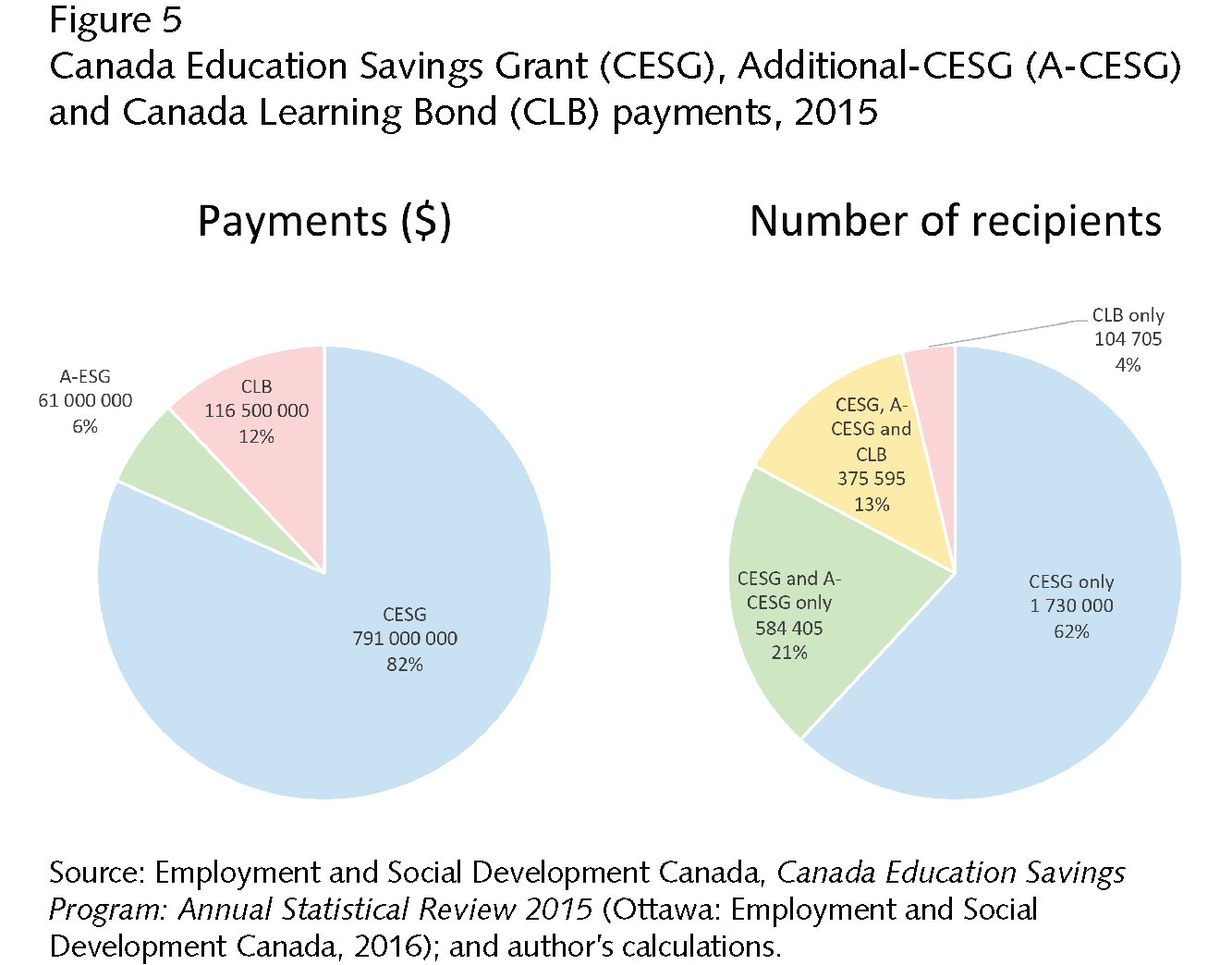

One way of doing this is to adjust the value of the different savings grants in order to make the Canada Learning Bond more attractive. Currently, over 80 percent of the approximately $900 million the federal government spends each year of education savings grants is in the form of the CESG, which is available to all families regardless of income (figure 5).

Less than $1 in $5 is set aside for lowand middle-income families. This ratio could be adjusted by raising the value of the Canada Learning Bond and reducing the matching rate or the maximum annual amount of the CESG. A doubling of the initial Canada Learning Bond payment from $500 to $1,000, for instance, would have cost $55 million in 2015, which is less than 7 percent of what was spent in that year on CESGs. A doubling of the total amount of Canada Learning Bond benefits could be offset by a 15 percent cut in the value of CESGs, and still leave the federal government spending three times as much on CESGs than on Canada Learning Bonds.

It would even be possible to roll the three existing grants into one single grant whose matching rate declined as family income rose, from as much as 50 percent for low-income families to as little as 10 percent for high-income ones. The point here is that the Canada Learning Bond program could be made significantly more generous in a revenue neutral way that would only slightly effect the non-means-tested part of the savings grant program. This would channel more money to those most in need of an incentive to kick-start savings — thereby making the incentive more effective — and less money to those most likely to be accumulating savings regardless of what types of incentive are on offer.

Another option is to make the Canada Learning Bond an automatic rather than an opt-in benefit dependent on recipients taking steps to open an RESP. The federal government could create either virtual savings accounts, savings set aside for children from low-income families (identified through their parents’ income tax returns) and available to them once they enrol in PSE, or actual registered savings accounts in the child’s name, seeded by the Canada Learning Bond. The automatic approach has been tried on an experimental basis in the United States, was used for a time in the United Kingdom, and has been adopted in Maine, where the Harold Alfond College Challenge recently moved from an opt-in to an automatic enrolment format (every new baby in Maine now automatically receives a $500 deposit into a virtual college savings account). Advocates of this approach argue that it is the only way to address the traditional inequity in education savings incentive programs, which sees the greatest share of benefits flow to those who need them the least.

The success of this approach, however, rests on the assumption that the effects of education savings incentive accounts — in terms of savings behaviour and attitudes towards education and the child’s future — will stem from the very presence of the account, regardless of whether the families themselves have taken any steps to sign up for it. It is also possible, however, that a family that is automatically enrolled in a savings incentive program as opposed to opting in will be insufficiently engaged with it to experience any effect. In the case of non-automatic programs, the decision to opt in represents a first step of engagement with savings that can be expected to have a cascading effect; in the absence of this initial point of engagement, the existence of the account may have much less impact.

While there is some debate about the merits of automatic enrolment, there is more of a consensus as to the importance of direct, in-person contact from service agencies familiar to and trusted by low-income families. This means that changes to program rules and mechanism can only ever be one part of the policy solution.

At the end of the day, the participation of low-incomes families in education savings programs will always depend in large part on effective communications and outreach initiatives, including direct contact by community partners trusted by eligible families. In a country as diverse as Canada, this means mobilizing a diverse network of community organizations and partners in an effort to ensure that more families with children can access the benefits for which there are eligible, kick-starting savings for PSE. Here, the best role that the federal government can play is one of facilitation and support.

The federal government provides almost $1 billion a year in education savings incentive grants. There needs to be a much greater effort to ensure that children from low-income families benefit fully from this expenditure. While evidence of the link between family savings for PSE and post-secondary access and completion grows, 1 million eligible Canadian children continue to miss out on the Canada Learning Bond each year. Raising the Canada Learning Bond participation rate should be a priority, so that more low-income families can accumulate savings for their child’s educational future.

This article draws on a more extensive research paper commissioned by the Omega Foundation.

Photo: Karen Roach / Shutterstock.com

This article is part of the Public Policy and Young Canadians special feature.

Do you have something to say about the article you just read? Be part of the Policy Options discussion, and send in your own submission. Here is a link on how to do it. | Souhaitez-vous réagir à cet article ? Joignez-vous aux débats d’Options politiques et soumettez-nous votre texte en suivant ces directives.