We have a child care problem in Canada (duh).

One of the main barriers to doing better in the provision of child care is our wide-eyed all-or-nothing one-size-fits-all approach. We daydream about universality and shout-out Quebec’s $9/day system, and then sort of just wait for federal elections in the hopes the program will be a platform priority. Because the provision of child care spans all orders of government depending on federal fiscal transfers to the provinces and territories, with policy regulated by the province and the municipality as the service system manager it is almost impossible for one order (or elected member) to revolutionize the system solo. Sorry, kids (*see what I did there?).

That said, in the true spirit of policy options, our major cities could offer an interesting interim solution to large-scale policy change in the form of loans to middle class families. I’m looking at YOU New York City, where true to form, they are piloting something -wait for it -NEW.

During their last mayoral election (2013), the lone female candidate (go figure!) Speaker Christine Quinn proposed municipal loans for childcare via a local credit union. The rationale is that we allow families to borrow capital for post-secondary education (also, cars! Like, you can get a loan for a vehicle but not childcare?), but childcare is a) more expensive than [Canadian] university and b) young families have more up-front costs to carry (student debt, housing via rent/mortgage, transit) –especially in big cities. The NYC pilot has started with funds for 40 families and pointed out that daycare spaces are subsidized for families below the poverty level, but there haven’t been specific policies for middle class families. Here’s how it works: Parents with children aged two to four are able to receive loans of $11,000 (about one year of childcare), at a 6% interest rate. Applicants must have an annual income of between $80,000 to $200,000, and a credit score of at least 620. In Ontario, with full-day kindergarten available for 4 and 5 year olds, parents would access the loans for a period of either two or three critical years, assuming a one-year parental leave.

Is a loan for two to four years of high-quality early childhood education, one of the best public investments we can make, worth the debt? Or should one parent stay home, delay her career, and income split with the hubs?

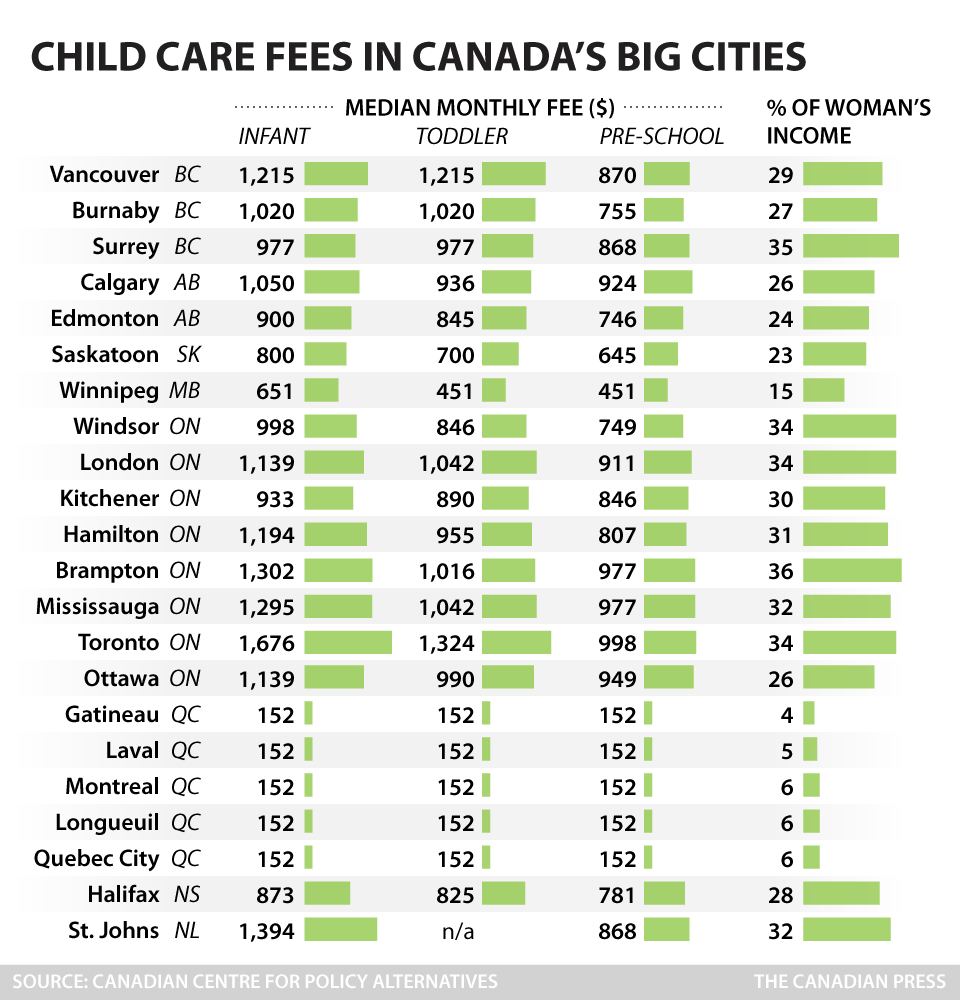

Think about the impact of an early learning program on a young family’s monthly budget: a 2014 report from the Canadian Centre for Policy Alternatives surveyed Child Care Fees in Canada’s Big Cities. Median fees for toddlers in Vancouver ($1,215), Burnaby ($1,020), Calgary ($936), London ($1042), Hamilton ($955), Brampton ($1,016), Mississauga ($1042), Toronto (1,324), and Ottawa ($990) are one third of the average woman’s income. With housing prices rising, it’s not hard to imagine that a small loan might make accessing childcare fiscally possible for stretched urban families.

There are fair reasons to oppose entertaining such an option. Municipal governments aren’t banks and don’t have the same skills and experience to loan funds; Canadian household debt is at an all-time high, and frankly, having people borrow money is an odd way to sorta subsidize a service. Slate called it a new debt trap, but what if the program helps ease the squeeze on Millennial fams in the short term and builds support for slightly higher taxes and a badass child care system in the long term?

Perhaps helping middle class families -officially the most politically palatable group of all time -access the capital required for child care could help improve access overall and even drive more licensed spaces. We know Toronto is having a “baby boom” as well. Mimicking NYC and similarly testing such a pilot program would be a huge policy innovation and a model for major Canadian municipalities.

Last thing -I was a little bit of a melodramatic Debbie downer when I was all, “no one institution or person can fix child care!” But municipal governments despite being the service system managers for child care in Canada are often (if not always) overlooked for their potential to innovate in terms of service delivery. I’d love to see Canada’s Councils prioritize exploring a range of innovations in the location and provision of child care service in an urban setting: more non-profit care offered in Bay Street buildings (the private sector), a public dialogue on municipal loans for child care and more short-term drop-in child minding options (e.g. Goodlife Fitness Centres). Our baby-booming cities could be a model in the federation and source of policy inspiration instead of exasperation and envy.

I get it: giving some qualifying families modest loans so that they can carry the costs of childcare and keep both parents in the labour force would make childcare more affordable for them -but it wouldn’t make for the ultimate goal: affordable child care for everyone. Perhaps it will be a step on our path to social policy greatness. Otherwise, I suggest you move to Quebec.

*Full disclosure: I used to advise the Minister of Education (Ontario) on child care policy. Now I wonk at a think tank at the University of Toronto. You with me?

**More about me: just finished reading How to be Danish and the Almost Nearly Perfect People in an effort to cope with the physiological responses that the policy *solution* of, “Why can’t we be more like Denmark/Finland/Iceland/Norway/Sweden?” elicit. Why? Taxes, honey. That’s why. When you pay more, you (tend to?) get more. And when you enjoy relatively low marginal tax rates, you get a fractured, piecemeal and pretty confusing child care system that is expensive and challenging to access. We’re Canadians. We can do better.

***Last thing! Here’s the official website of the NYC pilots. Yeah, I wish there was more info there, too.