In the budget introduced on June 6, Finance Minister Jim Flaherty made good on an election promise and did what the Conservative government had been trying to do since late 2008: begin the process of eliminating the quarterly allowance given to national political parties. As the newest component of the financial support package for political parties, the quarterly allowance is a tempting target. We argue, however, that the debate over the public financing of political parties should be broader and encompass the whole package of state support for parties.

Canada’s political parties have enjoyed various forms of state financial support since Parliament passed the Election Expenses Act in 1974. The 1974 legislation provided for two forms of financial support for parties. First, it established a generous political contributions tax credit (PCTC) that provided tax credits as large as 75 percent for small donations. Individuals could claim credits for donations to parties, candidates and local party associations. Second, the Act provided for a system of reimbursements for election spending. Political parties that spent at least 10 percent of their maximum spending limit could get 22.5 percent of their election spending reimbursed. Similarly, candidates who earned at least 15 percent of the vote in the district in which they ran could get half of their election spending reimbursed from the public purse.

The basic framework of public support for political parties remained relatively intact until 2004, with only minor changes, most notably to the criteria needed to qualify for the party expenses reimbursement. After the Natural Law Party, a party with little electoral support among Canadians, began to advertise its religious views using subsidized election campaign spending, Parliament amended the criteria to require parties to earn at least 2 percent of the vote nationally or 5 percent of the vote in the districts in which they ran.

The 2004 reforms to Canada’s election and party finance regime enriched the existing public financing. At the national level, the legislation increased the election expenses reimbursement considerably, taking it from 22.5 percent of eligible spending to 50 percent. Furthermore, a wider range of expenses were considered eligible for reimbursement, most notably public opinion polling. The legislation also raised the party spending limit, increasing the maximum reimbursement.

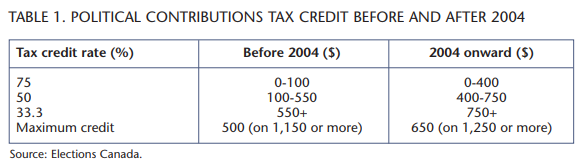

The PCTC was also enriched. The range of donations eligible for the maximum 75 percent credit was raised from $0$100 to $0-$400. Table 1 reports the changes in the tax credit levels before and after the 2004 reforms. Contributions above $100 received more generous tax credits after 2004 than was the case previously. For example, before 2004 a $500 donation would have been eligible for a $275 tax credit; a $1,000 donation would have been eligible for just under $450 in tax credits. After the changes to the law, these donations would be worth tax credits of $350 and $558.25, respectively.

Although these changes significantly increased the amount of public money going to political parties, they stuck closely to the existing framework of the Election Expenses Act. The 2004 reforms also added a quarterly allowance to the array of financial supports provided to national parties. While banning donations from corporations and unions (at least at the national level), the new financing regime provided an allowance to political parties based on $1.75 per vote earned in the preceding election. This allowance is indexed for inflation and paid quarterly to any political party that earned at least 2 percent of the vote or 5 percent of the vote in the districts in which they ran in the preceding election.

Canada has been providing state funding for its national political parties since 1974. The 2004 reforms strengthened the two existing components of state support — the political contributions tax credit and the election expenses reimbursement — while simultaneously establishing a quarterly allowance.

Canada has been providing state funding for its national political parties since 1974. The 2004 reforms strengthened the two existing components of state support — the political contributions tax credit and the election expenses reimbursement — while simultaneously establishing a quarterly allowance. The latter has received the bulk of the attention and controversy, while the other two components of state support for Canada’s parties escape almost unnoticed. A complete understanding of the extent to which Canada’s parties are financed by the support requires us to assess all three components.

Canada’s political parties are now required to provide extensive reports to Elections Canada, reporting quarterly on revenue and expenses, as well as transfers to other entities in the party, such as electoral district associations, candidates and contestants for party nominations or the leadership. This reporting allows us to analyze the extent to which parties are reliant on state support.

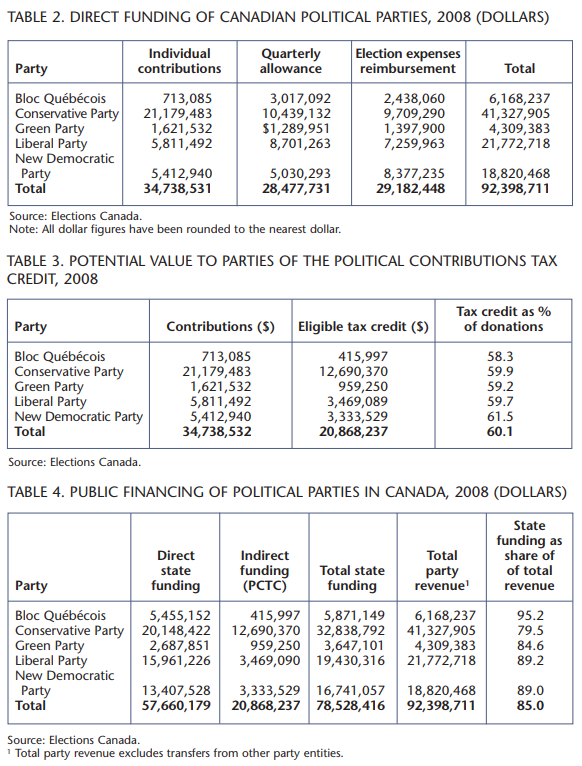

Elections Canada provides easily accessible data on the election expenses reimbursement and the quarterly allowance, allowing us to easily determine how large these components are for each of the parties relative to their overall income. Estimating the value of the PCTC as a component of party income is much more difficult. The only estimate of how much this tax expenditure costs the federal treasury comes from Finance Canada estimates of its cost to the treasury. For the year 2008, Finance Canada estimated that the PCTC would result in $25 million in forgone revenue. These estimates are of limited usefulness, since they do not help us to understand how this indirect financial support is distributed among the parties. Since the relative value of the tax credit declines as the magnitude of the tax credit increases, parties that raise fewer large contributions receive comparably less public support than parties that raise more small donations. For example, a party that raised 1,000 donations of $100 would enjoy indirect public financial support of $75,000 for those donations, while a party that raised $100,000 through 100 donations of $1,000 would receive public support of $55,825. The difficulty of estimating the value of the PCTC to parties compared with the other sources of public financing explains why most estimates of the level of public support to political parties look only at the extent to which they are supported by the election expenses reimbursement and the quarterly allowance.

This tendency in the research into public financing and the debate over public financing to neglect the role of the PCTC is regrettable, since tax credits for donations are a form of public financial support for political parties. Revenue that the federal government chooses to forgo is still a form of expenditure, an idea captured by the term “tax expenditure.” This form of public support is less transparent than the other two. Leaving it out of estimates of public support for parties leads to an underestimation of the total package of public financial support for parties and also of the extent to which each of the parties is relatively dependent on state support.

Because this public support is paid as a tax refund to the donor rather than directly to the party, we must estimate the value of the tax credit by using donor information provided by Elections Canada. For each donor to a national party, we calculated the value of the tax credit they would have been eligible to claim using the formula on the tax reform. We then added up those values for all of the donors to a party to assess the value of the tax credit to that party. These totals provide an estimate of the extent to which the state indirectly subsidizes parties through the tax credit.

There are certain limitations to the analysis that must be remembered when interpreting the results below. First, these estimates only include donations to the national party. The PCTC is claimed by individuals and includes all of the donations to the various entities of the parties. Identifying the donations made by individuals to various party entities to be able to add them together is impossible. Although this obstacle limits the extent to which we can develop a complete picture of the level of public support, it is unavoidable. Moreover, the bulk of individual donations is raised by the parties at the national level and this tendency has only been enhanced by the 2004 reforms. The PCTC is most relevant at the national level. Similarly, if someone donated to more than one national party, we are unable to account for that in our analysis.

Second, these estimates represent the potential tax credit claimed by individuals, not necessarily the actual amount of the tax credit claimed by donors. Not everyone claims all of their tax credits. It is impossible to know the extent to which this occurs and whether donors to one party are more or less likely to claim the available tax credit than donors to another party.

In what follows, we report the extent of public support to parties in 2008. We chose 2008 because it is the last available full year when all three forms of public financing were provided to the parties. Table 2 reports the value of the quarterly allowance and the election expenses reimbursement for each of the five major parties, as well as the total value of individual contributions. The Conservatives’ advantage in fundraising from private sources is readily apparent. In 2008, the Conservatives raised more from individual donors than all of the other major parties put together. The Conservatives receive more in these two direct sources of public financing than the other parties, but their advantage in public financing is not as pronounced as in private fundraising. Altogether, the Conservatives enjoyed a significant financial advantage over their opponents.

Table 3 reports the results of our analysis of the potential value of the PCTC for each of the five major parties in 2008. Although the value of the tax credit varies significantly by party in absolute terms, in relative terms, the share of individual donations indirectly subsidized by the PCTC displays relatively little variation by party. The variations reflect the relative importance of smaller donations to each of the parties, with the New Democratic Party most reliant on small individual donations and the Bloc Québécois most reliant on larger individual donations.

Adding the results of the analysis of the value of the PCTC to the direct sources of state funding allow us to get a more complete analysis of the extent of state financial support for political parties in Canada, as reported in table 4. All Canadian parties are heavily dependent on state sources of income to finance their revenue. Even the Conservative Party, the party most successful at raising donations from private individuals, is heavily dependent on state funding when measured in this way.

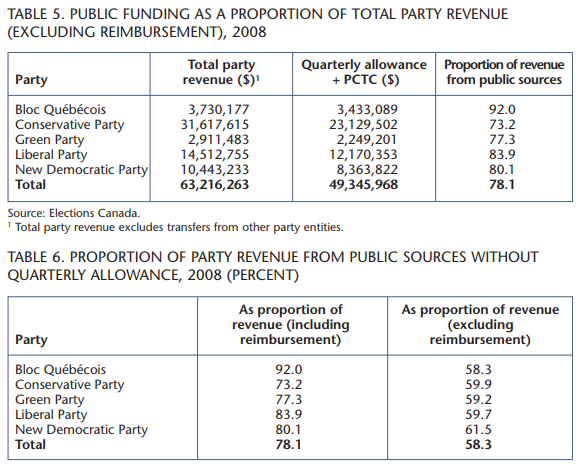

Including the election expenses reimbursement in a particular year tends to produce a misleading picture of both the total revenue and the extent of state support for parties for that year. Other analyses of party revenue (such as our chapter in our recent book and Flanagan and Jansen’s of 2009) have shown that excluding the reimbursement provides a picture of revenue and state support that is more comparable to non-election years. Table 5 reports the total funding and level of state support with the reimbursement removed. These results also paint a picture of heavily state dependent parties, much more so than is the case when the PCTC is not included in the calculations. For example, calculations of the level of state dependence for the Conservatives that do not include the PCTC estimate their state dependence at around one-third of their total revenue.

Our analysis shows that all of Canada’s political parties are heavily dependent on state financial support, delivered either directly or indirectly. In this sense all of Canada’s political parties are “wards of the state.” That said, the different forms of state support provided to Canadian political parties have different implications.

The quarterly allowance has been singled out in the past few years as an undesirable form of public support for political parties (for example, by Tom Flanagan in 2009), because it does not require political parties to actively “earn” them in the sense of maintaining connections with voters between elections. Furthermore, the quarterly allowance is seen to allow parties to survive without raising much money from individuals, as was the case with the Bloc Québécois. It does, however, have at least some connection with voter preferences. Although it requires voters to consider that their vote also entails a donation to the party, the quarterly allowance requires political parties to earn that level of support. Furthermore, it is completely transparent to taxpayers and voters in that it is easily calculated and reported. Finally, by being tied to voter support, it provides financial support to parties that more truly reflects their support in the electorate, helping to equalize inequities created by reliance on private fundraising.

The debate over the public financing of parties should begin with the recognition of the full extent and methods of state support for political parties, rather than selectively choosing one or the other for debate. A more holistic accounting of state support for parties allows us to identify the trade-offs involved in the mechanisms by which we deliver the state support.

In contrast, the PCTC is oblique and complex. Unlike the quarterly allowance, its cost is reported only in the aggregate and tucked away in obscure reports from Finance Canada. Conversely, it does have the virtue of still requiring political parties to convince voters to make that initial donation to the party. Delivering public money in

this way encourages parties to maintain constant connections with donors, which helps to minimize tendencies toward cartelization that may come with public money (Young, 1998). As fundraising becomes more professionalized, however, with increased reliance on telemarketing and direct mail appeals, the virtues of this type of fundraising as a way of maintaining contacts between parties and civil society are increasingly questionable.

The election expenses reimbursement is relatively transparent, following clear rules, and it is reported on the Elections Canada website. Furthermore, it partially subsidizes political parties for their activities in connecting with voters. By tying the value of the subsidy to the value of spending, however, it treats all party activity the same. Attack advertising and voter suppression efforts are subsidized at the same rates as efforts to inform voters of a party’s platform during the election. This form of public support assumes that parties are using the money to connect with voters; it does not require them to do so in the same way as the PCTC or the quarterly allowance.

This has implications for the kinds of reform Canada might consider to its party finance system. The Conservative plan is to abolish the quarterly allowance; at this point there are no plans to replace the lost revenue with other sources of income. Setting aside the question of whether this would provide political parties enough money to carry out their activities, the result would still leave political parties largely funded by the public purse. Table 6 reports the proportion of revenue coming from public sources, both including and excluding the reimbursement from the analysis. When factoring in the PCTC, abolishing the quarterly allowance would still leave the majority of party revenue as coming from state sources, but perhaps to the detriment of equitable competition and informed political debate.

Tom Flanagan has suggested in 2009 that the quarterly allowance be replaced with measures that encourage voters to donate to parties and parties to appeal to voters. He suggests that an enriched PCTC or a check-off system on tax forms might be a way to accomplish these goals. Flanagan and David Coletto suggest in a 2010 article for the University of Calgary Public Policy Briefing Papers that such a move would likely leave parties in a worse financial position and these measures would recoup only a fraction of the lost revenue, at best. The point we would add to this conclusion is that replacing the quarterly allowance with further action through the tax system is replacing one form of public support for parties with another.

In this article, we have tried to assess the full extent of public financial support for Canada’s national political parties. We have found that all of Canada’s parties are heavily dependent on state support, whether on the direct support of the election expenses reimbursement and the quarterly allowance or on the indirect support of the PCTC. The debate over the public financing of parties should begin with the recognition of the full extent and methods of state support for political parties, rather than selectively choosing one or the other for debate. A more holistic accounting of state support for parties allows us to identify the tradeoffs involved in the mechanisms by which we deliver the state support.

Photo: Shutterstock