Canadians are living longer and working later in life, so why do many of our politicians keep talking about retirement as a fixture of age 65?

Over the last several months both Thomas Mulcair and Justin Trudeau have sketched out details of the platforms their respective parties will run on in next year’s federal election. On retirement and pension issues, both the NDP and the Liberals have committed to roll-back the planned increase in the eligibility age for Old Age Security and the Guaranteed Income Supplement, and to work with the provinces on enhancing the Canada and Quebec Pension Plans. Both of these promises continue to assume age 65 as the normal age at which someone would become eligible to draw retirement benefits. The same is true of Ontario’s own proposal for a provincial supplemental pension plan.

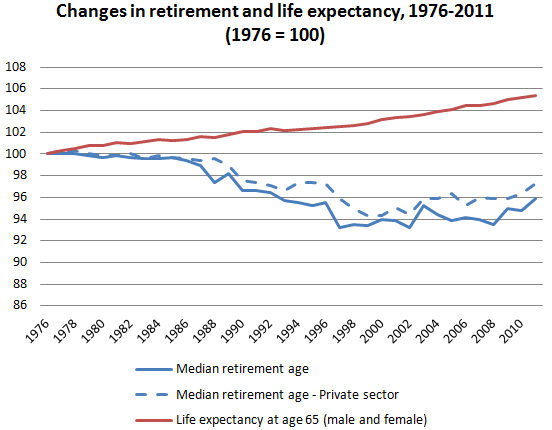

For most people sixty-five is probably a pretty popular psychological milestone, so it is understandable that politicians, themselves, may be stuck on this number. But for the purposes of policy-making, consider how life expectancy and retirement patterns have diverged over the last several decades (Chart 1). In 1976, not long after our retirement income system was implemented in its modern form, the typical Canadian retired at the age of 65 and was expected to live another 16.1 years until their death. By 2011, the median retirement age had dropped to 62.3 years, while the life expectancy of a 65 year-old had increased to 20.5 years. In other words, in those thirty-five years the expected number of years in retirement increased from about 16 to 23 years.

Chart 1

While it is true that retirement ages fell quite noticeably through the 1980s and 1990s, more recent cohorts have reversed this trend. Between 2002 and 2011 median retirement ages rose from an all-time low of 60.6 years to 62.3 years as all classes of workers””especially those in the private-sector””chose to retire later. By 2013 (not shown in the chart) this stood at 63.3 years.

Many analysts believe that these trends toward later retirement and longer life expectancy will continue, though potentially at a slower pace. A critical consideration, as former senior public servant Peter Hicks has argued, is whether we also see a greater interest in staged retirement planning in which people choose to work later in life at a reduced work schedule, or end up taking multiple retirements as they move into and out of the labour market. There is already some evidence of this phenomenon of previously retired individuals returning to the workforce.

What then, are the implications, of ignoring these changing realities in health and work?

It is true that at current trends the Canada Pension Plan is sustainable, the Chief Actuary projects, for at least the next 75 years. This means that the current contribution structure is sufficient to cover future payouts even as life expectancy rises, though much depends on future economic and demographic performance. If life expectancy rises faster than the projected mid-point, CPP contribution rates would have to rise in coming decades. And that only deals with the sustainability of benefits already covered by the current system.

For new benefits that governments may add (e.g. Ontario’s pension proposal or an enhanced CPP), keeping the eligibility age at 65 is a rather odd policy choice. For one, the earlier the retirement date is set, the higher the contribution rate will have to be for the same level of benefits. Whether or not you see pension contributions as a “tax”, this means that both businesses and workers pay more than may be necessary if the retirement age were set even slightly higher.

A more attractive proposal, financially as well as politically, would exchange a later eligibility age for additional retirement benefits. This “grand bargain” of sorts, might just be a win-win for everyone. Indeed, it is stunning that amid all the talk about CPP, political parties have failed to think about these kinds of options.

For OAS, GIS and other pay-as-you-go benefits the sustainability challenge is much more daunting since benefits are paid out of current revenues. This is why in 2012 the federal government announced a plan to gradually increase the age of eligibility for OAS and GIS, from 65 to 67. The savings from this change are modest since most of the baby-boom generation will retire before it begins to take effect in 2023, but it raises an important question about how we set eligibility rules.

It is important to remember that OAS and GIS are designed to provide basic income floors for older Canadians; for OAS in particular the clawback is so gradual that a large majority of retirees receive some benefit from the program. Therefore, if eligibility is kept at age 65, and Canadians continue to work longer, we will be faced with a situation where a growing number of Canadians will be receiving old age benefits while still working. Society may view that as a desirable outcome in order to promote broader labour force attachment, but it also goes to a question of equity which deserves significant debate.

This is not to say, however, that the government’s own changes to OAS and GIS were well thought out. Not only do they start rather late in the demographic transition, they were also done in a fairly arbitrary way. Because life expectancy varies quite significantly in relation to one’s income, education, occupation and health circumstances it fails to recognize that a shift in eligibility age will disproportionately affect those less fortunate. As I have argued before, we ought to keep the eligibility age for OAS and GIS at 67 but provide a revenue-neutral, actuarial adjustment for those who need or want to claim it at age 65. If opposition parties want to fix the government’s proposal, this would be a much better set of reforms than simply reverting to age 65.

As we head into the next federal election we need to demand more of our political leaders. Why do we assume that Canadians aren’t up for a more substantive debate? By their own retirement behaviour, Canadians understand that the future will be different from the past, both potentially more uncertain financially, but also one in which we are healthier. Our public policy and our politicians should keep pace, too.