The Government of Canada has called for a “progressive trade agenda.” A common view holds that the liberalization of international trade in recent decades has harmed the economic prospects of middle-class workers in Western countries like Canada. This view was expressed by then trade minister Chrystia Freeland (now Minister of Foreign Affairs), at a speech to the Conference of Montreal last year. She said, “the middle class in western industrial societies…has begun to fear very profoundly that the two great economic transformations of our time — globalization and the technology revolution — may have been good for a narrow elite…but that they haven’t been good for most people.” The government’s progressive trade agenda is meant to respond to these concerns — to ensure that trade contributes to broad-based prosperity and that public sentiment does not turn against free and open trade. But the implications of these principles for trade policy have yet to be specified.

The development of a progressive trade agenda requires an empirical, quantitative assessment of the impact international trade has had on Canadian labour market outcomes in recent decades. We summarize here the main findings of a recent Centre for the Study of Living Standards report by Alexander Murray, for Global Affairs Canada, that measures the impact on Canadian labour markets of China’s rapid rise as a manufacturing export superpower. The main finding was that there was a net loss of manufacturing jobs. (The report does not take into account the larger impact of international trade on welfare in Canada.)

The “China shock”

There is a large body of empirical literature on the effects of international trade on labour market outcomes such as employment and wage distribution. In general, research in the 1980s and 1990s found little evidence that international trade openness in advanced economies was a significant driver of either employment outcomes or the wage distribution. More recent research has focused on the effects of increased trade with developing countries, especially China. This research suggests that trade has become a more important determinant of labour market outcomes than was suggested in the past, and that labour markets are slower to adjust to the dislocations associated with trade shocks than was previously thought.

Our work fits into a recent line of research pioneered by David Autor and his colleagues on the labour market impact of the China shock — the rapid increase in China’s exports in the 2000s. Autor and his co-authors maintain that the United States could be divided into many local labour markets (small regions where workers commute extensively inside the region but not much between regions), and that the extent to which these localities are exposed to Chinese imports could be used to assess the impact of the China shock on employment, wages, and other outcomes. The more a locality’s employment is concentrated in industries that are highly exposed to Chinese imports, the greater is that locality’s exposure to Chinese competition. (To establish causality, Autor et al. developed an “instrumental variable” strategy in which they use the rise of Chinese imports in other advanced economies to make inferences about the rising supply of Chinese imports in the United States.)

The main findings from this literature are that the rise in competition from Chinese imports led to large declines in employment in certain regions of the US that have a high concentration of manufacturing industries, and that employment gains in other industries in these regions have not materialized. On the contrary, the loss of manufacturing jobs caused by competition from Chinese imports have been associated with increases in unemployment and decreases in labour force participation in those local labour markets. The local labour markets that are more exposed to competition from Chinese imports also exhibit larger reductions in average wages, concentrated mainly among workers in the bottom 40 percent of the initial wage distribution.

This literature has shed new light on the US labour market’s ability to adjust to large trade shocks. On the basis of the older empirical evidence, most economists believed that the labour markets of advanced economies were sufficiently flexible that workers displaced in import-competing industries could easily reallocate to other industries or regions. The recent research suggests that — in the US at least — the labour market’s adjustment to China’s rise has not been so easy.

The Canadian experience

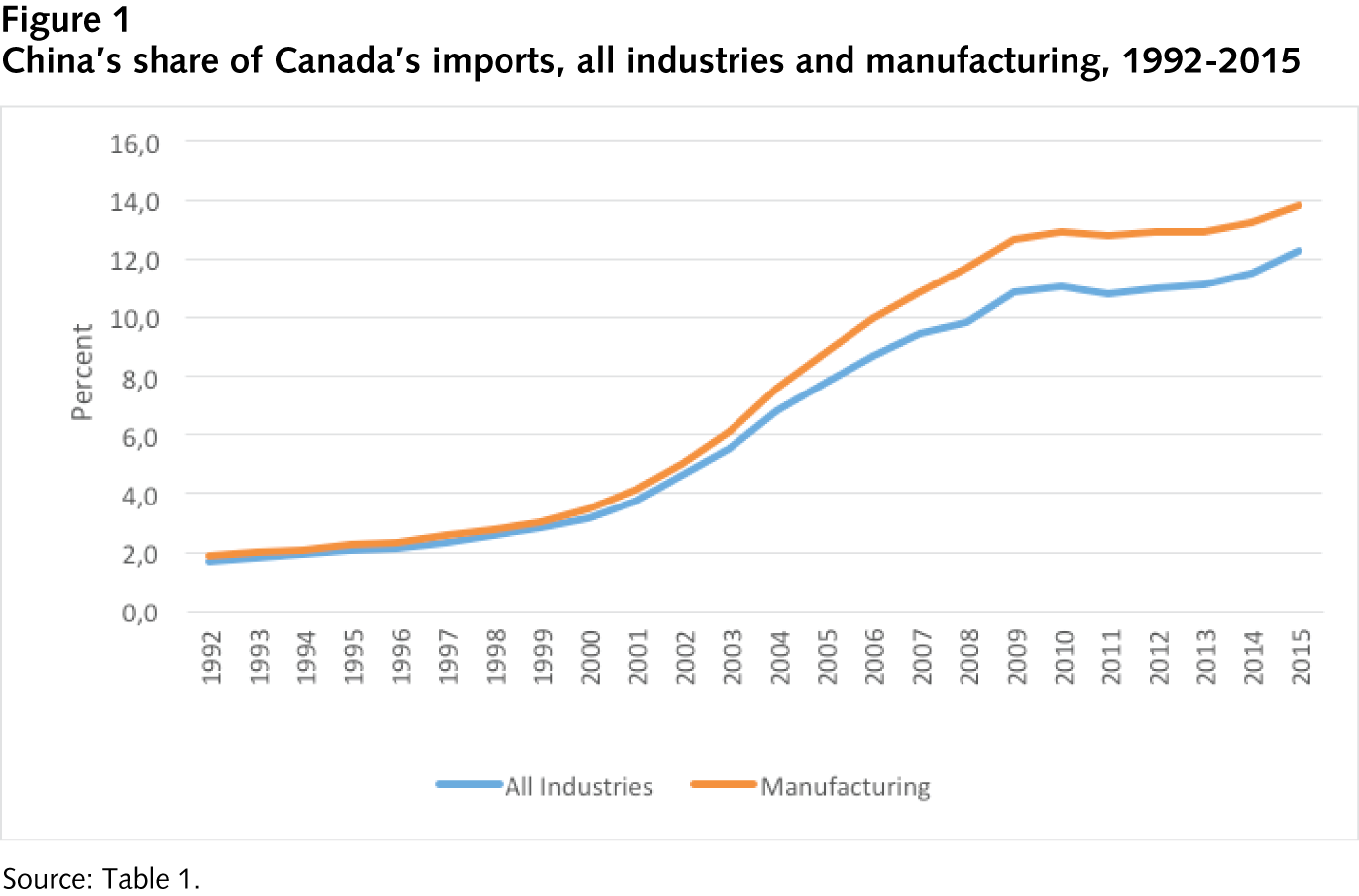

After 2001, China’s exporting capacity surged. By 2015, China had become Canada’s second-largest trading partner, after the United States, accounting for 12.3 percent of Canada’s total imports, up from 3.2 percent in 2000 (figure 1).

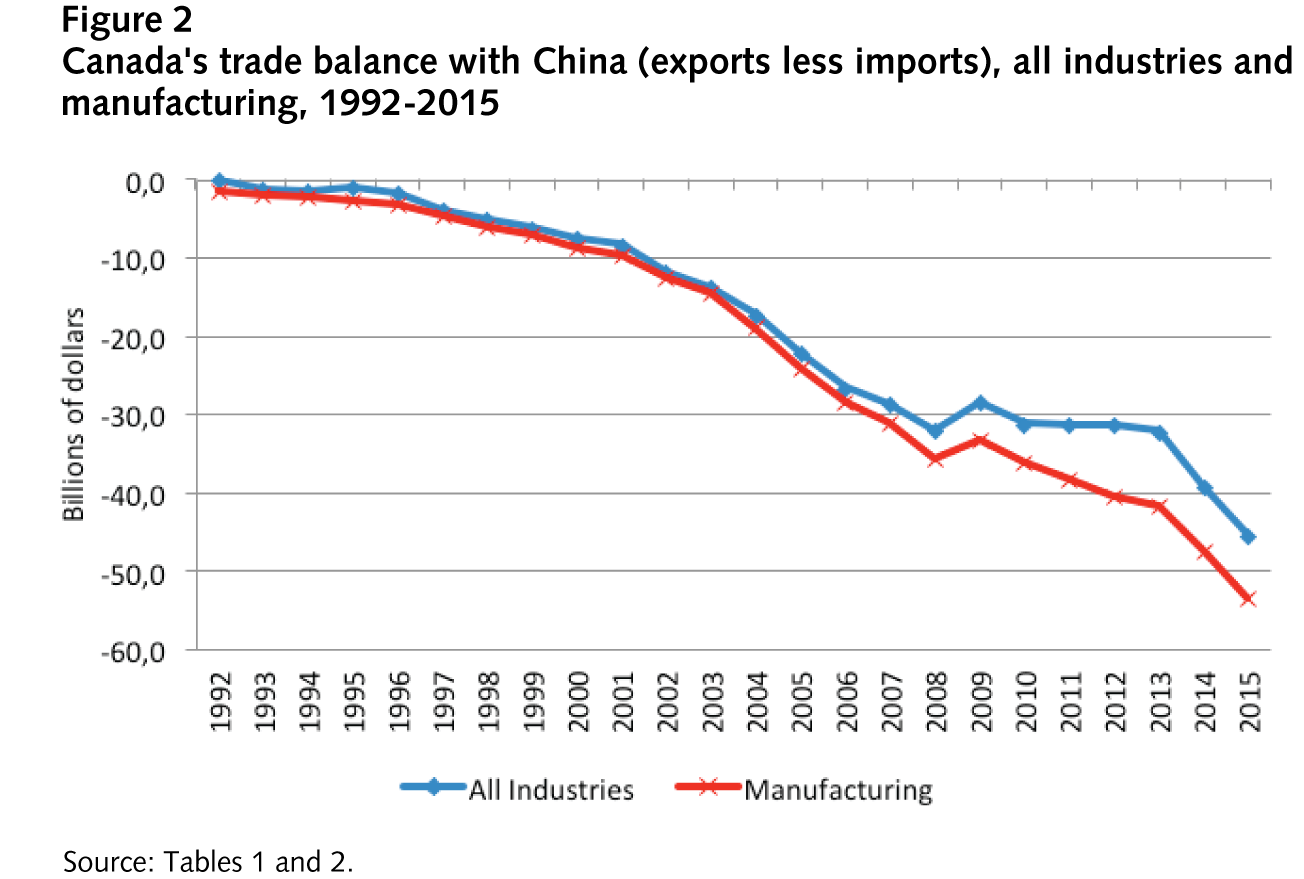

Canada’s imports from China grew much faster than its exports to China, before and after 2000. Canada’s bilateral trade deficit with China (i.e., imports less exports) increased from $188 million (or 0.03 percent of GDP) in 1992 to $45.5 billion (or 2.3 percent of GDP) in 2015 (figure 2).

One common measure of an industry’s exposure to competition from imports is the import penetration ratio — the share of imports in the total supply of that industry’s goods available in a country. Exposure of Canadian manufacturing to import competition increased over the 1992-2015 period. The import penetration ratio rose by 18.8 percentage points, from 45.7 percent in 1992 to 64.5 percent in 2015. Of this 18.8 percentage-point increase in import penetration, 8.1 percentage points (or 43 percent of the total increase) were attributable to rising imports from China.

Total employment in Canada increased by 1.5 percent per year over the 1992-2015 period. This was slightly faster than the 1.3 percent annual growth of the working-age population, so that the employment rate increased by 2.9 percentage points over the period. Growth in employment has been markedly slower since 2008, however, and by 2015 the employment rate had decreased by 2.1 percentage points.

Within the manufacturing sector, employment grew at a robust 2.7 percent per year over the 1992-2000 period, but then it fell at annual rates of 1.9 and 1.7 percent over the periods 2000-08 and 2008-15, respectively. As shown earlier, the 2000-08 period was a time of rapid growth in Chinese import penetration in Canadian manufacturing.

Correlation does not imply causation, so more careful analysis is required to assess the impact of Chinese import competition on Canadian employment. (We used an “instrumental variables approach” to estimate the causal impact of the rise in China’s exports on Canadian employment, following the model of Daron Acemoglu et al).

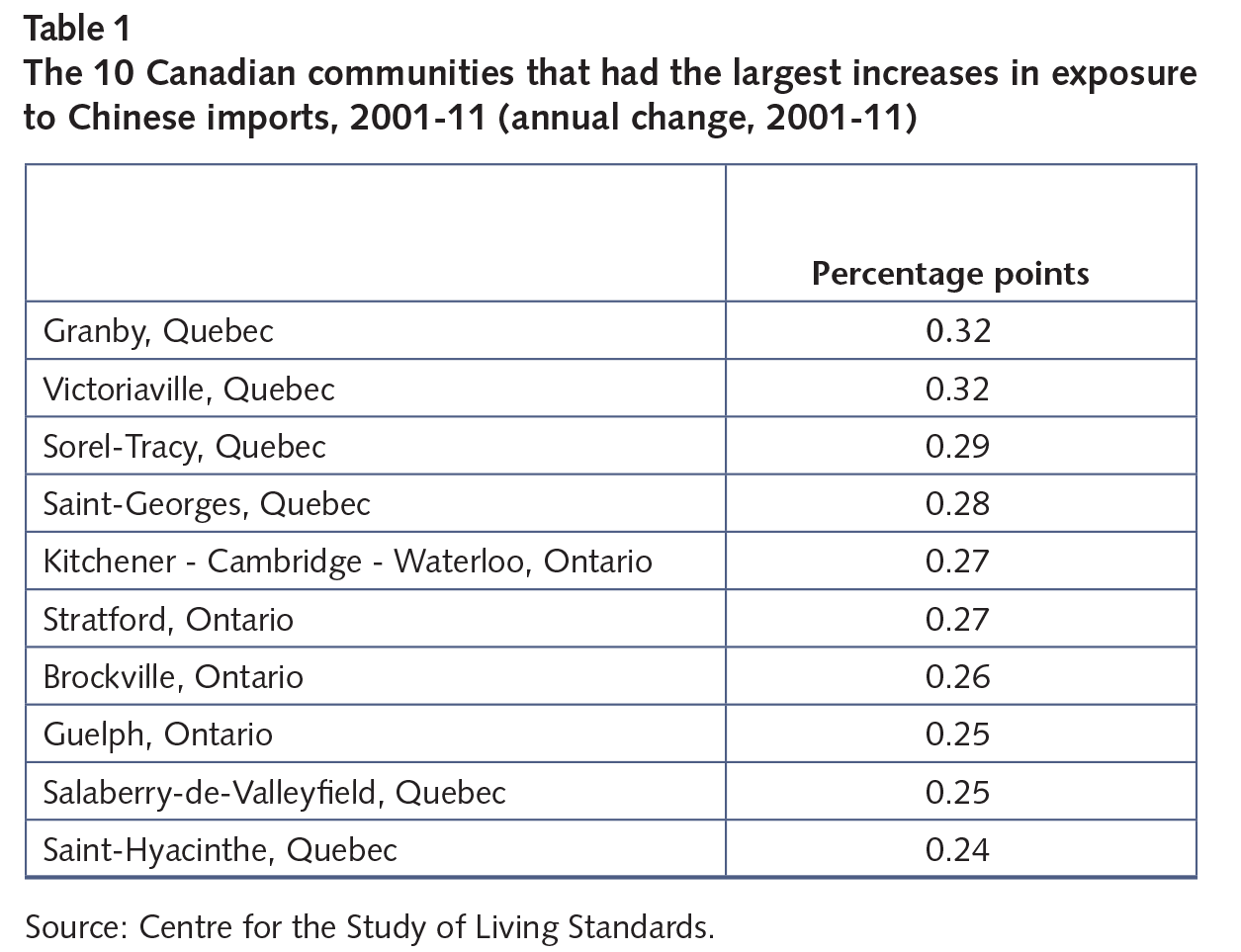

Our research report provides estimates of the changes in import exposure for 85 manufacturing industries and 125 localities (census metropolitan areas and agglomerations). The localities that show the largest increases in Chinese import exposure over the period are all located in Quebec or Ontario (table 1). This pattern reflects the relative concentration of economic activity in Quebec and Ontario in manufacturing industries, while other regions specialize in commodities industries, which are less exposed to Chinese import competition.

We found that the variation in employment rates over the 2011-11 period mirrors the regional variation in Chinese import exposure.

Among the 10 localities with the largest declines in the employment rate, 7 are in Quebec or Ontario (table 2).

We estimated the direct effect of increased import competition on employment in manufacturing industries, but this direct effect does not fully capture some of the indirect effects. For example, job losses in one industry may raise employment in other industries by expanding the supply of available workers (the “labour reallocation effect”), or they may reduce employment in other industries because unemployed workers have less income to spend on goods and services (the “aggregate demand effect”). To account for these effects, we use the data on local labour markets to estimate the combined impact of the direct and indirect effects.

Our main finding is that the direct effect of Chinese import competition in Canadian manufacturing was a net loss of 105,000 manufacturing jobs over the 2001-11 period. This amounts to 20.7 percent of the actual observed decline in manufacturing employment over that period (508,000 jobs). Our estimates imply an additional loss of 64,000 jobs over the 1991-2001 period, for a total loss of 170,000 manufacturing jobs over the 1991-2011 period.

We stress that our analysis is not a comprehensive assessment of the impact of international trade, or trade with China in particular, on welfare in Canada. The employment impact of import competition is one of many implications for Canada of rising trade with China. Other effects include lower prices for Canadian consumers and higher prices for oil and other primary commodities exported by Canada, hence the improvement in Canada’s terms of trade since 2001. The opening of the Chinese market also provides new opportunities for Canadian exporters. More broadly, international competition is known to enhance productivity by reallocating market share from less productive firms to more productive ones, as well as by leading exporters to innovate. We do not address any of these dimensions of the impact of trade with China.

Nevertheless, the narrow scope of our analysis does not diminish the importance of our results from the perspective of economic inclusiveness. Economic inclusiveness requires that all people be able to participate in and benefit from a society’s economic activity. Further analysis can be extended to include an examination of the effects of the China shock on outcomes other than employment, such as wages, the usage rates of social assistance and employment insurance benefits, health, and interprovincial migration. The analysis could also break down the employment effects of the China shock by occupation, gender and level of education.

Employment is the most important way most people participate in the economy and partake in the gains from economic growth, so labour market outcomes are a fundamental determinant of the inclusiveness of growth. Even if rising trade with China has, on balance, been beneficial for Canada, the loss of employment opportunities in certain sectors may represent a net loss for a segment of workers tied to those sectors. A progressive trade agenda should take those losses into account and find ways to improve them.

This article is part of the Trade Policy for Uncertain Times special feature.

Photo: Jiujiang dock, China. Shutterstock, by humphery.

Do you have something to say about the article you just read? Be part of the Policy Options discussion, and send in your own submission. Here is a link on how to do it. | Souhaitez-vous réagir à cet article ? Joignez-vous aux débats d’Options politiques et soumettez-nous votre texte en suivant ces directives.