The Canada Pension Plan/Quebec Pension Plan (CPP/QPP), together with the Old Age Security (OAS) and other seniors’ benefits such as the Guaranteed Income Supplement (GIS), are doing much to lift many of Canada’s 9.5 million low-income workers out of poverty in the postwork years of their lives. Through the cooperative efforts of Ottawa and the provinces, these programs were updated in the 1990s and placed on a more fiscally sound footing. As a result, experts agree that the universal OAS/GIS and CPP/QPP components of Canada’s retirement income system are in better shape today than are their counterparts in many other developed economies.

The news is not so good in the supplemental (i.e., supplemental to OAS/CPP/QPP payments) sector of Canada’s retirement income system. This sector ideally provides Canada’s 8.3 million middle- and higher-income workers the additional postwork income to necessary to maintain desired postwork living standards. The option to defer income tax on retirement savings has indeed spawned millions of individual registered retirement savings plans (RRSPs) and thousands of collective registered pension plans (RPPs). However, Statistics Canada data and studies commissioned by the Alberta/British Columbia, Nova Scotia and Ontario governments, and by the C.D. Howe Institute, among others, show that 3.8 million of these 8.3 million workers (mainly middle-income, in the private sector) have been left to their own devices to navigate the complex, dangerous waters of saving and investing for their retirement. There is evidence that many of these 3.8 million workers will not be able to maintain their desired standard of living when they stop working 10, 20 or 30 years from now.

Meanwhile, the 4.5 million private and public sector workers in the middleand higher-income brackets who are covered by employment-based defined benefit plans (DB) and capital accumulation plans (CAPs) have a different problem. Many of these plans have serious design flaws. The recent global financial crisis has laid these flaws bare for all to see, with DB plan coverage declining, the DB plans of some financially weak corporations failing, many public sector DB plans becoming seriously underfunded, and many individual pension accounts in CAPs losing 20 percent of their value or even more.

Why is the sector that should be supplementing postwork incomes beyond what the public components of Canada’s retirement income system provide in such a sorry state today? A common theme of the expert studies is that while we have been innovative in the OAS/GIS and CPP/QPP sectors, this has not been the case in the supplemental pensions sector. The designs of our collective and individual supplemental pension plans are out of date, as are the ways in which we legislate and regulate these arrangements and the ways in which we manage them. Fortunately, the recent plethora of pension reform studies show an increasing awareness of these problems and provide important ideas on how they could be solved.

The studies broadly agree that needed pension reforms should be based on four fundamental principles:

- Pension plan designs should target a postwork standard of living that is adequate, achievable and affordable.

- All workers should have a simple, accessible, portable opportunity to participate in such target benefit pension plans that have explicit postwork income-replacement targets.

- All forms of retirement saving should receive equal tax, regulatory and disclosure treatment across all sectors of the Canadian workforce.

- Pension management and delivery structures should be expert, transparent and cost-effective.

While pension arrangements consistent with these four principles can be structured in a number of ways, all will have the following four overarching elements in common:

- A stated target postwork income-replacement rate for all pension plans (e.g., 60 percent of final work income, indexed for inflation, including the OAS/CPP pensions)

- One national, or a number of regional, provincial or other large group-based supplementary pension plans for workers without an employment-based pension plan

- Guarantees in pension plans that are subject to the same solvency standards as those governing insurance companies and other financial institutions

- A requirement for pension delivery structures or organizations to demonstrate good governance and cost-effectiveness on a regular basis. The implementation of the four pension reform principles in a manner that includes these four elements would constitute a comprehensive pension care policy for Canada, earning it the top global ranking in retirement income system design and management. This in turn would create a material competitive advantage for Canada through enhanced postwork income levels and stability and by spurring capital formation and wealth creation.

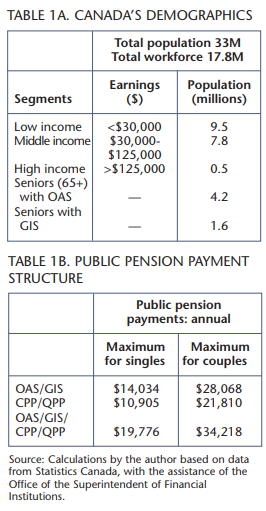

Table 1 itemizes key facts and figures about Canada’s demographics and public pension system. Out of a population of 33 million people, almost 18 million participate in the workforce. With no other income sources, a 65year-old Canadian with maximum government pension benefits currently receives $19,776 in inflation-indexed income ($34,218 for couples). However, today the typical recipient receives only half of the maximum CPP/QPP total, reducing the annual amount to $16,760 for singles and $28,202 for couples. Out of Canada’s 4.2 million seniors, 38 percent currently receive GIS payments.

Government pensions at these levels represent significant income-replacement rates for Canadians with low incomes from full-time employment. So they are not the natural target group in the consideration of how to reform the supplemental sector of Canada’s pension system today. We also assume that high-income Canadians (those earning over $125,000) are generally in a better position to look after their own retirement income needs, although this group faces formidable (and inequitable) barriers to accumulating adequate postwork incomes. This segmentation leaves middle-income workers earning between $30,000 and $125,000 as the group for whom it is critical to assess the need for and shape of pension reform. This is the group most likely to need help securing additional retirement income to supplement basic OAS/CPP/QPP pension entitlements if they are to maintain an adequate postwork standard of living. Statistics Canada data suggest there are 7.8 million workers in this category, out of a total workforce of 17.8 million.

Where are the supplemental pension payments for our target group of 7.8 million middle-income workers to come from? The prevailing public policy answer has been that they would come through voluntary arrangements where income taxes on retirement savings can be deferred until they become pension income in the hands of individuals. These arrangements take one of two primary forms: employment-based RPPs, or personal pension accounts, mainly in the form of individual or group RRSPs and registered retirement income funds (RRIFs).

The maximum deduction ceiling for RRSPs is currently set at 18 percent of pay, up to a maximum of $21,000. While in theory contributions made into RPPs are subject to the same ceilings, this is often not the case in practice. A report by the Canadian Federation of Independent Business, Canada’s Pension Predicament, documents the growing inequity and unfairness between retirement and pension income practices in Canada’s public and private sectors. The study notes, for example, that while the average age of retirement in the public sector has fallen from 64 in the 1970s to 59 in this decade, it has fallen from 65 to only 62 in the private sector. The average retirement age of the self-employed has not changed at all. It was 66 in the 1970s, and is 66 now. On the pension income side, while the private sector is limited to a maximum 18-percent-of-pay contribution rate, the full cost of a final earnings-based, inflation-indexed pension in Canada’s public sector exceeds 30 percent of pay today.

Where are the supplemental pension payments for our target group of 7.8 million middle-income workers to come from? The prevailing public policy answer has been that they would come through voluntary arrangements where income taxes on retirement savings can be deferred until they become pension income in the hands of individuals.

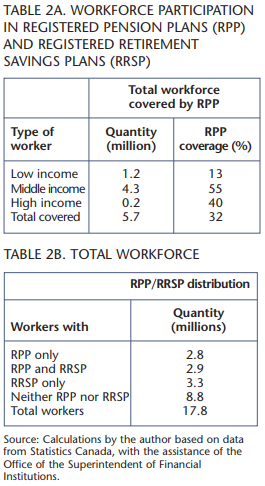

Out of Canada’s workforce of 17.8 million members, 5.7 million have an RPP, of which 4.6 million are in DB plans (table 2). Note this includes about half of the 7.8 million middle-income workers. Of all 5.7 million workers with an RPP, 2.9 million also have an RRSP. At the same time, 3.3 million workers have accumulated retirement savings in RRSPs only. The remaining 8.8 million workers (almost half the total workforce) have neither an RPP nor an RRSP. On the payout side, 3.3 million retirees are currently receiving payments from an RPP, and 0.4 million are drawing down personal RRIFs. Against the current senior (aged 65 or more) population base of 4.2 million, these numbers imply that a significant proportion of today’s seniors are receiving supplemental pension income from sources other than GIS. On the other hand, we also noted that 38 percent of today’s Canadian seniors receive GIS payments.

None of these figures speak directly to the question of the adequacy of future postwork income. We can, however, draw some inferences from the data. For example, we can reasonably assume that most workers with both RPPs and RRSPs or even just RPPs alone will receive adequate levels of postwork income (including OAS/CPP payments and assuming the RPP remains solvent). Thus we are narrowing in on the workforce segment likely to be most in need of help: the subset of the 7.8 million workers with incomes in the $30,000125,000 range without RPP membership. There are 3.5 million Canadian workers in this category. They are probably self-employed, or working for small or midsized private sector employers. But are these people not capable of looking after their own postwork income needs?

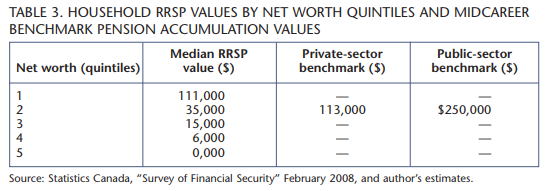

The distribution of RRSP savings plotted against the total net-worth (i.e., a measure of wealth) rankings of Canadian households offers a clue as to how this question might be answered. As table 3 indicates, this distribution is asymmetrical, and the top 20 percent of Canadian households ranked by their net worth have a median RRSP value of $111,000. The median values by quintile for the other 80 percent of Canadians ranked by net worth are considerably lower at $35,000, $15,000, $6,000 and $0. Arguably, the $35,000 median RRSP value of the group with the second-highest net worth (i.e., in the second quintile) offers a not unreasonable basis of comparison against two possible adequacy benchmarks: the mid-career RRSP value of a private sector worker who has contributed a modest 7 percent of a constant $60,000 salary each year; and the midcareer fair value of the accrued pension of a public sector employee earning a constant $60,000 per year.

As table 3 indicates, both benchmark values exceed the median $35,000 RRSP value of Canadian households with second-quintile net worth by considerable amounts. The calculated benchmark of a $113,000 RRSP value for a midcareer, middle-income, private sector worker is over three times the $35,000 value, and exceeds even the $111,000 median RRSP value accumulated by the 20 percent of the Canadians with the highest net worth. The estimated benchmark $250,000 fair value of the accrued pension of a midcareer, middle-income public servant is seven times the $35,000 median RRSP value of Canadians in the second net-worth quintile.

Why do many of the 3.5 million middle-income Canadians without RPPs appear to not be saving enough to maintain postwork living standards? This in a demographic environment that will, according to Canada’s Chief Actuary, see the number of Canadians over the age of 65 rise to 25 percent of the population by 2040, compared to 14 percent today. That is the question we turn to next.

The life-cycle theory of why people should save for retirement (and how much) is both elegant and conceptually simple. Financially speaking, people progress through three life phases: prework, work and postwork. The theory requires people to save during their working years so as to maintain their desired standard of living during the postwork years. How much to save? Simple. Just project how much you will earn during your working years, how long you will work, what return your savings will earn, and how long you will live. Plug these assumptions into the right computer formula, and after some number crunching, voilà, the required savings rate appears on the computer screen. This theory is not only elegant, but potentially useful!

However, behavioural finance experts point out that its widespread application requires three things to be true: (1) that ordinary people can solve complex mathematical problems; (2) that they can adequately model the future uncertainties in their lives; and (3) that they have the willpower to faultlessly implement the resulting savings plan. Unfortunately, none of these requirements square well with reality. Most people are not capable of solving complex mathematical problems. They have difficulty dealing with future uncertainties such as their work-income trajectory over future decades. Finally, even if they could, we know from observation that most people do not possess the willpower to see the resulting savings plan through its 30to 40-year implementation period. Indeed, there is a fourth problem: even if people could conquer the complex math problem, could deal with future uncertainties, and had the willpower to do the savings part of the plan, they could still be easily stumped by the technically and emotionally challenging investment part. In short, human failings prevent the elegant theory of life cycle personal finance from waving its magic wand.

But what about collective DB pension plans? Do they not solve the computational, skill and behavioural problems of individual retirement finance? Yes, they do. DB plans operate with an automatic pension formula based on a participant’s salary and years of service, and require a series of annual contributions sufficient to fully prefund the plan. Typically, pension payments continue as long as the plan member (or spouse) is alive. Further, participants have no direct role in determining how the accumulated collective retirement savings of the plan are invested. Unfortunately, what seems to be too good to be true actually is too good to be true. For example, many people who change jobs during their careers do not do well in DB plans because vesting provisions usually delay plan participation. Lack of portability is another problem. DB plans are also complicated and expensive for employers to administer.

These are not the only DB plan problems. Most fundamentally, DB plans usually operate as incomplete contracts that do not fully spell out the respective rights and responsibilities of the parties to the DB contract (e.g., pensioners, active workers, shareholders, current and future taxpayers, unions, management and pension plan trustees). Thus in times when the DB balance sheet is in surplus (i.e., assets exceed liabilities), it is often unclear who owns that surplus. The result is that all balance sheet stakeholder groups will lay claim to it. Similarly, when the balance sheet is in deficit, it is often unclear how that deficit should be remedied.

Now all stakeholder groups attempt to pass the parcel to somebody else.

The inner workings of government

Who’s doing what to get federal policy made. In The Functionary.

The inner workings of government

Who’s doing what to get federal policy made. In The Functionary.

This would be irrelevant if DB plans were immediately vested and fully funded at all times, with the projected pension payments matched by an asset portfolio of high-quality bonds. But that is not how DB balance sheets are managed. Usually they are subjected to material asset-liability mismatch risk, based on a convention that took shape during the 1980s and 1990s. The convention was to assume that this mismatch risk would eventually lead to additional asset returns, which in turn could be used to make expensive DB pensions affordable. The two serious equity market setbacks during this decade (in 2001-2003 and 2008) are now forcing DB plan stakeholders to reexamine this convenient but faulty risk-equals-return convention. The global adoption of fair-value accounting rules is accelerating this reality check process in the corporate sector.

Similarly, better disclosure forces are at work in the public sector. As a result, sponsors of DB plans in the public sector are being increasingly persuaded to disclose the true cost of employee pension promises accruing at the federal, provincial and municipal levels of government. Using discount rates that reflect the high quality of these promises (often based on final earnings and inflation-indexed), as we have already noted, their true cost today can exceed 30 percent of current pay. Despite recent increases, actual pension contribution rates are still well below these true costs. As noted by Alexandre Laurin and William Robson in 2009, the result is a steady shifting of wealth from future generations of Canadians to current public sector employees. Meanwhile, in the corporate sector, the reexamination of the risk-equals-return convention has already led many employers to close their DB plans, or is causing them to consider doing so. New employees are typically offered a DC-based capital accumulation plan, with the employer making contributions to it. Now we are back in the behavioural finance world of human failings defeating elegant theory.

A central implication of behavioural finance is that choice architecture matters. You can nudge people toward making better decisions without restricting their freedom of choice. Here is how this powerful idea can be applied to designing more effective pension structures:

Target savings rate: This is a tough one. We showed above how to derive an elegant, personalized answer. All you have to do is decide what kind of postwork standard of living you want, estimate how long you will work, what your salary path will be, what your retirement savings will earn, how long you will live after you retire and what your government pension benefits will be. Because most real people will suffer a brain-freeze when faced with such a daunting list of questions, choice architecture requires a series of thoughtful default answers. The postwork standard-of-living target is the most fundamental and difficult issue to tackle. The best a conscientious choice architect can do is to set a transparent, reasonable default target, which then, along with all the other assumptions (including the government pension programs), produces the default retirement savings rate required to hit that pension target (e.g., 7 percent of pay). For participants desiring higher income replacement rates or shorter working lives, it is now easy to provide them with the higher target savings rate implications.

A central implication of behavioural finance is that choice architecture matters. You can nudge people toward making better decisions without restricting their freedom of choice. Here is how this powerful idea can be applied to designing more effective pension structures.

Plan enrolment: Research confirms human inertia stops us from doing many things we ought to do, especially if the rewards from doing so are a long way off. Voluntarily joining a well-designed pension plan is one of those things. What is the choice architect solution here? Easy: change the default choice from non-enrolment to autoenrolment with an opt-out option. Research shows this to be a very effective nudge toward better decisions. For example, a new study by the United States Government Accountability Office (2009) projects auto-enrolment will move DC plan participation rates from the 60 percent range to over 90 percent.

Investing: Research confirms our intuition that the average person is not good at investing, and that better investor education is not the answer. People operate with attention spans that are far too short and emotional ranges that are far too wide. They also vastly underestimate the negative impact of high fees on their retirement income prospects. Thus here is another opportunity for choice architecture to provide the right nudge. Both theory and common sense tell us that investment programs should be cost effective, and that older workers should invest more conservatively than younger workers. These considerations should be reflected in constructing both default investment policies and the means of implementing them.

Annuitization: Annuitization is a simple, effective strategy for ensuring that individuals do not outlive their retirement savings by pooling longevity risk. Yet again, inertia stops many people from availing themselves of this logical insurance option. Even worse, irrational loss aversion leads many people to have a negative view of annuities. Loss aversion leads people to worry more about buying an annuity and dying early than they do about not buying one, and then living too long and running out of money. Once again, choice architecture can come to the rescue. For example, in the default choice, workers could start purchasing deferred annuities at the age of 45, with a target of annuitizing a significant portion (but not all) of their retirement savings by the age of 65.

How do we get these choice architecture ideas into the supplementary sector of Canada’s retirement income system? It requires doing two things. First, we must address the problem of Canada’s outdated pension rules and regulations that have accumulated through years of neglect. Second, we must solve the pension coverage gap problem documented above. A possible solution is to create the Canada Supplementary Pension Plan (CSPP), which was first proposed in a 2008 C.D. Howe paper titled “The Canada Supplementary Pension Plan: Towards an Adequate, Affordable Pension for All Canadians.” The basic thrust of the CSPP is to auto-enrol all Canadians who do not have a workplace pension plan into a simple, lowcost pension arrangement with full portability. The CSPP design has the four choice architecture features set out above. DB plans could also be part of the solution, but only if Canada radically rethinks its approach to DB plan regulation.

As it is in Canada, the pension coverage question is now on the political radar screens in the United States and the United Kingdom. Any serious resolution of the question in the United States will likely have to wait until after that country deals with its even more fundamental Medicare coverage problem (although the Obama administration did introduce some modest pension reform measures in September 2009). The United Kingdom has decided to proceed with a bold national plan to cover the 7 million private sector workers who have no workplace pension plans and are judged to be undersaving for retirement. The Personal Accounts Delivery Authority (PADA) will be reaching out to over 1 million employers and is slated to become operational in the fall of 2012. Much like our CSPP proposal, the UK plan’s key features include the following:

- Targeted workers will be auto=enrolled in the plan with an option to opt out.

- Those not in the targeted group can opt in.

- Total default contribution rate is 7 percent of pay, with 3 percent coming from the employer.

- Personal accounts to be managed by a well-governed, not-for-profit trustee corporation funded by member charges.

PADA is charged with launching the United Kingdom plan on time and on budget, and notes that significant challenges still lie ahead in moving this project into operational reality.

We noted above that 5.7 million workers continue to be members of RPPs, of which 4.5 million are in DB plans (2.5 million in public sector plans, and 1.0 million each in corporate and multi-employer plans). We also noted that while DB plans solve human foible problems related to retirement saving and investing, many of the DB plan versions in use today have other problems related to surplus, deficit, funding, costing and disclosure. If employment-based DB plans are to continue to play an important role in Canada’s retirement income system, it is essential that these nagging problems now be addressed.

In our view, the attempts by the provincial expert studies to fix DB plans did not address the fundamental sources of these problems, which are the following:

- DB pension contracts are seldom fully spelled out: examples include fuzziness about surplus (and deficit) ownership, about funding policy, about ranking of accrued pension debt in corporate reorganizations, about maximum allowable DB balance sheet mismatch risk and about inflation indexation rules. Stated differently, DB plans are full of embedded options issued and held by various parties to the pension contract that are not fully specified, and hence difficult to value and enforce.

- Pension funds have historically been used as profit centres: if a pension fund’s only purpose was to secure pension promises, it would always be a flow-through vehicle, fully funded and fully immunized with assets matching liabilities. This is clearly not the case. Instead, employers and plan trustees expose DB balance sheets to considerable mismatch risk in the hope of earning a risk premium on pension assets. If the risk premium is indeed earned, the employer does not have to pay the full economic cost of the pension promise. In short, the plan becomes a profit centre.

Both of these realities create problems. The incomplete contract reality sets up situations of potential conflict between various stakeholder groups, each trying to interpret fuzzy pension deal options in their own favour. Current pension legislation implicitly accepts this fuzzy-deal reality by attempting to establish financial boundaries (e.g., through solvency funding rules) within which DB pension contracts must be written. In this context, it is interesting to observe that governments everywhere are now loosening these contract boundaries in response to urgent corporate requests to stretch the standard five-year solvency deficit amortization period to ten years.

Similarly, if the profit centre mindset continues, DB balance sheets will continue to be subjected to material mismatch risk, which in turn guarantees there will be periods of material DB balance sheet surpluses and of material asset shortfalls. The current Nortel situation offers a stark example of what happens when the incomplete contract and asset shortfall features coincide with a corporate reorganization or bankruptcy. A material reduction in current and future pension benefits results. The profit centre problem plays out differently in public sector plans. Now the problem is that the investment risk premium assumption allows the stakeholders in these plans to contribute 20 percent of pay for what is today really a 30 percent of pay risk-free benefit. If the assumed risk premium is in fact earned, the 20 percent contribution rate will be sufficient. With realized risk premiums in fact negative in this decade, the 20 percent rate has not been enough. Just as the surpluses of the 1990s were spent on bigger benefits and lower contributions to current workers, the bulk of the unfunded liabilities in public sector plans will now be loaded on the shoulders of future workers and taxpayers.

Once the real problems with today’s DB plans are properly diagnosed and acknowledged, the fix logically follows. We need legislation that requires regular true and full disclosure about the economic (i.e., fair value) cost of the pension promises being earned, and regular true and full disclosure about the economic (i.e., fair value) status of DB balance sheets. As importantly, the solvency requirements of DB balance sheets should be treated no differently than the balance sheets of insurance companies and other financial institutions. In other words, the pensions sector should not be exempted from the fundamental principle that promises made should be promises kept. This implies that accruing pension promises must be fully costed and fully funded at all times. In a balance sheet management context, this has one of two implications: assets match liabilities in terms of duration and inflation sensitivity; or, if there is risk-taking on the DB balance sheet, it must be buffered by a risk capital cushion proportional to the estimated degree of balance sheet mismatch risk. A third possibility is to make pension payments explicitly variable, contingent on ability to pay.

We are well aware that these rules would fundamentally change the funding and management of many DB plans in Canada today. That is exactly the point. Fundamental change is required to deal with the cited havoc the current ad hoc funding, management and disclosure rules are causing in many plans. With the new prudential rules we propose here, DB plan stakeholders would no longer be able to flip mismatch risk coins with the current heads-we-win, tails-you-lose rules. Pensioners at Nortel and other financially weak corporations would not have to worry about whether they are going to get 50 cents on the dollar out of their pension plans. Future taxpayers and public servants would not be left to pay for the pensions-related legacy costs being created by today’s public servants and their employers.

The time has come to clearly articulate a comprehensive pensioncare vision of where Canada could and should now take its retirement income system. Achieving it requires doing five things:

- Agree on the principles that will guide the design and implementation of the concrete pension reform steps that should now be taken.

- Agree on the list of dysfunctional pension rules and regulations that must be either eliminated or modified so that they become functional. Develop a feasible work plan to achieve this.

- Agree on the validity of the assessment that Canada indeed has a pension coverage problem, and choose and implement a concrete course of action to deal with it (e.g., the CSPP).

- Solve the DB plan dysfunction problem by addressing its underlying root causes rather than its symptoms.

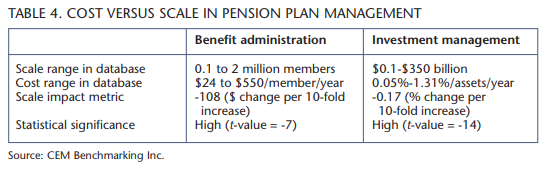

- Agree on the importance of getting the institutional structure of pension management and delivery right and take the necessary steps to achieve scale and measurable cost effectiveness (see table 4).

Is Canada ready to go from saying to doing?

Awareness of our building pension problems and debate on how to deal with them has accelerated steadily over the last five years. Missing thus far has been a clear framework and a compelling narrative that transform that now-large body of research and debate into an integrative pension-care vision from which a concrete reform plan can be constructed. The financial well-being of Canadians in the 21st century depends on its success.

This article is adapted from the C.D. Howe Institute’s 2009 Benefactors Lecture delivered in November 2009.

Photo: Shutterstock