On June 20 in Vancouver, Canada’s Minister of Finance, Bill Morneau, signed an agreement with eight provinces (nine now with Manitoba) that will increase the replacement rate of the Canada Pension Plan (CPP) from 25 percent to 33.3 percent and the yearly maximum pensionable earnings (YPME) from $54,900 to $62,600 (in constant 2016 dollars). In order to finance this improvement, the government will increase contributions on earnings below the present YMPE by 2 percent and on earnings above that level by 8 percent. The increased contributions will be shared equally between employers and employees.

However, only those people whose incomes fall between $54,900 (the average industrial wage, or AIW) and $62,600 will get any significant benefit from this increase, and this means mostly men will benefit. For people earning less than the YMPE, the main effect of the pension increase will be to reduce the amount they receive from the Guaranteed Income Supplement (GIS).

Quebec did not sign the agreement. Quebec Finance Minister Carlos Leitão announced that the Quebec Pension Plan (QPP) would take a different approach, so that low-income families do not have to pay higher contributions. People earning less than $27,450 (and their employers) would be exempted from the increase in contributions, but it is not clear whether they will benefit from an increased pension (in our opinion, it’s unlikely they will). As well, the contribution rate and the YMPE in the Quebec proposal are unknown.

Over the last few years, several proposals for reform have been circulated. The most generous is that of the Canadian Labour Congress (CLC), which launched a campaign in 2009 to increase the replacement rate of the CPP/QPP to 50 percent (see the report, in French, by Ruth Rose for a more complete analysis of the various proposals). The Quebec Federation of Labour (QFL) asked that, in addition, the YMPE be increased to $71,500 and that the basic exemption for contributions be doubled, to $7,000. This proposal would require increases in contributions of 6 percent for earnings below the present YMPE and 11.5 percent for higher earnings.

In the face of Stephen Harper government’s refusal to go ahead with an improvement in the CPP/QPP, in spite of a quasi-consensus among the provinces in 2013, Ontario began to create its own plan, the Ontario Retirement Pension Plan (ORPP). This plan would provide a replacement rate of 15 percent for incomes below or equal to $90,000, bringing the total income replacement rate (combined with the CPP) to 40 percent for incomes below the current YMPE. The ORPP would mean a significant improvement in retirement income for the middle class, with a contribution rate increase of only 3.8 percent. In signing the new agreement with Ottawa, Ontario has, to our surprise, agreed to a compromise position much lower than its initial objectives. It has announced that it will discontinue the ORPP if the Vancouver agreement holds.

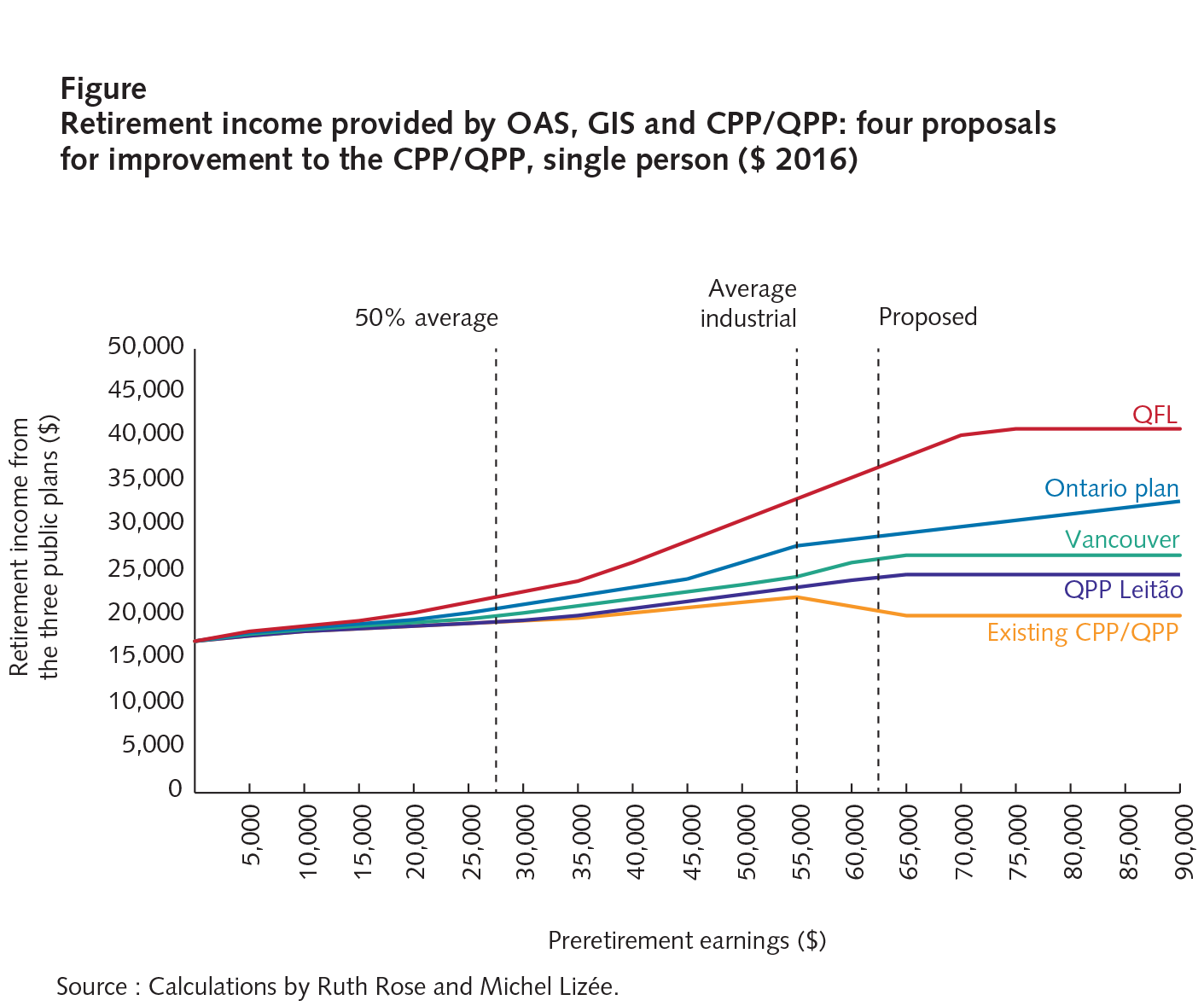

The figure below compares retirement income currently received from public pension plans and the income that would be received according to four other options. In 2016, Old Age Security (OAS), which pays $6,846, and the Guaranteed Income Supplement (GIS), provide a minimum income of $17,076 per year for single people aged 65 and older, with the exception of a few recent immigrants. However, any additional income, for example the CPP/QPP pension or withdrawals from an RRSP, reduces GIS at a rate of 50 percent, or even 75 percent in some intervals.

Thus, the maximum a single person can get from public pension plans is $22,046, and that is only if he or she earned at least the AIW of $54,900 for 40 years (orange line in the figure). The three public pension plans replace less than 40 percent of pre-retirement incomes, which is among the lowest rates in the industrialized countries.

The Vancouver agreement (green line in the figure) will do little to improve the situation, especially since the reform will not be fully implemented until between 2066 and 2073. For example, a woman whose salary was $41,241 — the average for Canadian women — will get a pension increase of $3,270, but will be able to keep only half of this, because her GIS will be clawed back by that amount. People earning $27,450 will lose three-quarters of the increased pension as a result of the GIS claw back; the effective increase in their retirement income will be only $634.

With an additional contribution of $549 per year for 40 years (plus $549 from his or her employer), those earning the AIW will see their retirement income increased by about $2,000 a year. In contrast, those earning $62,600 or more will potentially see an increase in their retirement incomes of $6,802.

Finance Minister Leitão says he is in favour of a “modest, targeted and gradual” solution that would encourage voluntary savings. If Quebec goes ahead with the same parameters as the Vancouver agreement, but adding an exemption for incomes below $27,450, the increase in incomes will be even more modest (purple line in the figure).

A replacement rate increase of only 8.3 percent is far too modest, as the figure shows. In order to allow most of the middle class to be released from the GIS, an increase of at least 15 percent is required, as proposed by the ORPP (blue line in the figure).

The Vancouver agreement and Leitão’s proposal target those earning between $54,900 and $62,600, those who are in fact disadvantaged by the current situation. An increase in the YMPE is desirable in itself, in order to ensure that the pension reflects average career earnings more closely. But the target should have been much broader in order to cover incomes that range from half of the AIW ($27,450) to 150 percent of the AIW ($82,350), in other words, most of the middle class, which is having difficulty maintaining its standard of living after retirement.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

Finally, the implementation of the reform will be too gradual. Employees will begin paying higher contributions in 2019, but the first enhanced benefits will be paid starting only in 2026. In other words, a person who is 59 in 2019 and who applies for his/her pension at age 65 in 2025 will have paid increased contributions for six years without getting any increase in benefits.

The modest proposal that seemed to have rallied a majority of the provincial finance ministers in 2013 would have come into force over a period of 10 years. Under this proposal, if initial contributions began in 2019, a person who retired at age 65 in 2025 would have received 60 percent of a full pension. The full pension would have been payable in 2029. This “pay-as-you-go” approach is viable and equitable if the contribution rate is set in such a way as to distribute the costs of both the existing and the new CPP/QPP fairly between generations.

Limiting the increase in contributions for companies, but not necessarily for participants, seems to have been the primary objective of the Vancouver agreement, in response to an organized campaign by business groups and the financial sector to block any change.

In order to decrease the burden of an increase in contributions for low-income earners, the federal government will provide $250 million to increase the Working Income Tax Credit. However, people who earn as little as $27,450, who will lose three-quarters of the increase in pension to the GIS claw-back, are probably too “rich” to benefit from this measure.

The agreement also provides that the increased contributions will be a tax deduction rather than a tax credit. However, only people earning above $46,000 will benefit. The higher the income, the more the deduction will reduce taxes. In other words, the people who will benefit the least from the reform will get no relief from this measure either.

Leitão’s expressed desire to avoid higher contributions for low-income earners seems rather hypocritical, since Quebec has just made it obligatory for companies with at least five workers to register their employees in a “voluntary” retirement savings plan (VRSP), with a normal contribution rate of 4 percent. If, instead, Quebec adopted a model similar to the ORPP, with an increase in contributions of 3.8 percent — of which half was contributed by the employer — it could finance a fully indexed, guaranteed for life pension, with a replacement rate of 15 percent above the current CPP/QPP. With an RRSP or a VRSP, we know how much we save but we don’t know how much our pensions will increase, because high management fees eat up a significant part of our savings and rates of return are low and unpredictable. And it is women in particular who bear the risk of longevity, not knowing how long the money will have to last.

The meeting in Vancouver could have been the occasion to improve incomes for future generations of retirees significantly. Instead, the main beneficiaries will be the federal government, which will save on GIS payments, and financial institutions, which will continue to benefit from high fees for managing RRSPs and TFSAs. A real enhancement of the CPP/QPP is even more urgent because employers, especially in the private sector, are phasing out their defined-benefit pension plans and, in many cases, imposing less generous defined-contribution plans on new hires.

Manitoba, which hesitated before signing the agreement, asked that the other benefits provided by the CPP/QPP — survivor and disability benefits in particular — also be examined. We find it untenable that our governments will go ahead with a reform of this importance without spelling out all the implications and without wide public consultations.

Photo: The Canadian Press/Darryl Dyck

Do you have something to say about the article you just read? Be part of the Policy Options discussion, and send in your own submission. Here is a link on how to do it. | Souhaitez-vous réagir à cet article ? Joignez-vous aux débats d’Options politiques et soumettez-nous votre texte en suivant ces directives.