Yesterday, the Ontario government released new details on its forthcoming provincial pension plan. There is a lot to dig into, and other parameters still to be worked out (like the specific administrative cost). Looking at what Ontario has announced, and where this sits in the long and still unfolding debate over Canada’s retirement income system, I have 3 reactions:

For a more in depth analysis of the challenges facing the retirement income system, readers are encouraged to consult my recent paper on this topic, published in collaboration with the Mowat Centre.

1. The financial services industry should be happy (this is a good thing)

The biggest change announced by Ontario concerns the definition of a ‘comparable pension plan’ that will be grandfathered during implementation. Since the goal of the ORPP is to increase pension coverage among workers who do not currently participate in a pension plan, or are not saving enough, this detail is key.

In the white paper issued by the government earlier this spring during public consultations, the clear signal was that only defined-benefit (DB) pension plans would qualify to be grandfathered. This made some conceptual sense since the ORPP will use a DB structure, although the implications for transitioning the investment community would be massive. With the announcement yesterday, Ontario has indicated that defined-contribution (DC) pension plans will also qualify, provided they meet a number of conditions, including:

- joint employer and employee contributions, representing a combined 8 percent or more a year of eligible salary;

- locked-in benefits; and

- mandatory employee participation.

Although these conditions are stricter than is the norm among DC and group RRSPs in Canada, generally the financial services industry, which administers and invests these private retirement assets on behalf of workers, will be quite happy.

On Twitter, I have received a number of questions from people wondering what this will mean for plans which currently fail the comparability standard set out by the ORPP. In a way, this is good news for all investors.

By allowing DC plans into the definition, there is now a strong incentive on the part of insurance companies, benefits administrators and investment professionals to work with employers who already offer retirement savings plans to improve the quality and standard of benefit plans. No one in the investment industry wants to lose potential business to the forthcoming public pension plan, and this creates a strong bias in favour of competition. I suspect that as we get closer to implementation, we will see the ORPP have an important nudging effect on the standard of group RRSP and DC pensions across the province.

Though it may reduce the number of people ultimately sent into the ORPP, this change sets out a path for those currently in DC plans to maintain their existing arrangements while also potentially increasing the level and quality of savings that are set aside. What it does to the underlying cost of mutual funds and group investment products will also be important to watch. Combined with potential changes the Ontario Securities Commission may be making in the coming years to enforce greater transparency and competition in investment fees, we are in the midst of a major transformation in the Ontario (and by extension, Canadian) investment landscape. This is all for the better.

2. The plan continues to assume a retirement age of 65 (that’s a problem)

My overall impression of the ORPP is generally positive, since I think it does a good job of putting the issue of a targeted increased in mandatory savings on to the public policy agenda. In addition to the cost and complexity of the implementation that others have raised, I am a bit concerned about the basic assumptions it takes toward longevity and demographics.

The ORPP assumes that contributors will become eligible to draw benefits starting at age 65, or as late as age 70. While this may be politically smart if the eventual goal is to harmonize the ORPP with an enhancement to CPP/QPP, assuming that you can get an unreduced pension at age 65 still gives me pause. Considering that a CPP enhancement may never come to pass, I am concerned that the rigidity of age 65 reinforces a bad tendency among our politics to avoid changing patterns in life expectancy.

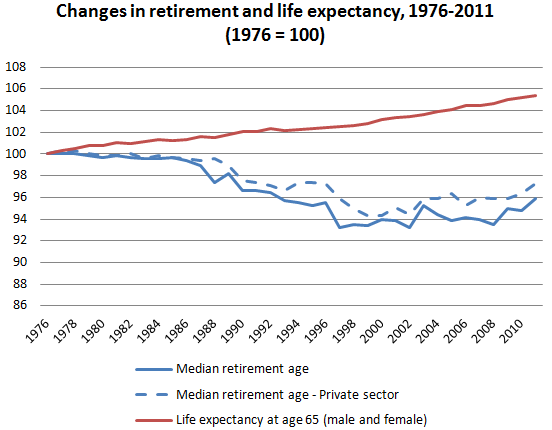

There is no question we are living longer, and this contributes to the need for a more secure retirement. But if we are to respond to that challenge effectively, then we need to ensure that our pension system reflects these changing realities. As I blogged last fall, retirement patterns, although improving since the late 1990s, have not kept pace with life expectancy. The trends in the figure below speak for themselves. We are living longer and still retiring earlier than in the past. That is not a viable combination.

Since the ORPP is the first major addition to the retirement income system in nearly five decades, we need to get this right. As I outlined in my recent paper with the Mowat Centre, we need to get to a place where eligibility for retirement benefits – of all kinds – changes in line with life expectancy. While we do clearly need to make sure this is done in a way this fair to those who cannot work longer, I think we can agree age 65 is not what it used to be. This is important if the ORPP is to provide benefits that are sustainable, and a contribution structure that is affordable, over the long-run.

One thing that should be considered with any enhancement in public pension coverage – either via the ORPP, or CPP – is to make this additional tranche of benefits conditional on a later eligibility. Indeed, as Wolfson has shown, this could even be used to phase-in the enhancement of benefits faster than the normally assumed period of 40 years, thus providing a bigger lift, sooner.

3. There remains much more to do (and Ottawa has an important role to play)

The ORPP details announced yesterday reinforce the need for greater co-operation between Ottawa and the provinces in this area. Without consequential amendments to the Income Tax Act and other steps the federal government ought to take, the ORPP risks not being able to help self-employed individuals and facing challenges with tax treatment and benefit administration that were never contemplated when this process began. For very legitimate reasons Ottawa may oppose what Ontario is doing, but it should not stand in the way of a well-functioning federation.

If the retirement income system is to function effectively – working in the interest of the single taxpayer each government shares – then collaboration is what is needed.

But to what end?

If there is one message I can send to policy-makers debating the ORPP it is that, whatever you do on this file, you need to appreciate that it is not the magical solution to all of the challenges facing the retirement income system. Indeed, there is a lot more work still to do if we are to have a system that effectively responds to the challenges of an aging population that is living longer, and facing greater investments risks than in decades past.

In the paper with the Mowat Centre I argue that policymakers need to focus on four sets of reforms:

- reducing the rate of poverty among seniors who are single;

- ensuring that eligibility for pension and retirement benefits better reflects long-run changes in longevity;

- closing gaps in pension coverage through a targeted increase in mandatory saving (using either CPP/QPP or Quebec’s VRSP as a national platform); and

- enhancing the resources and mandate of the Chief Actuary to provide objective and consistent information to provincial and federal Ministers of Finance about the state of the RIS.

The ORPP, good as it may be, addresses only the third point on this list. When the election is over, let’s get back to governing and, hopefully, with a renewed sense of collaboration.