Over the past decade, China has demonstrated that it has emerged from its long sleep. Modernization, urbanization and marketization are occurring at a dizzying pace.With a population of more than 1.3 billion and a rapidly growing economy, China deserves full credit for its unprecedented turnaround. No other country has ever sustained double-digit growth for three decades, as did China from 1979 to 2009. If it succeeds in maintaining even half that pace, it will surpass the United States at some point in the next few decades to become the world’s largest national economy.

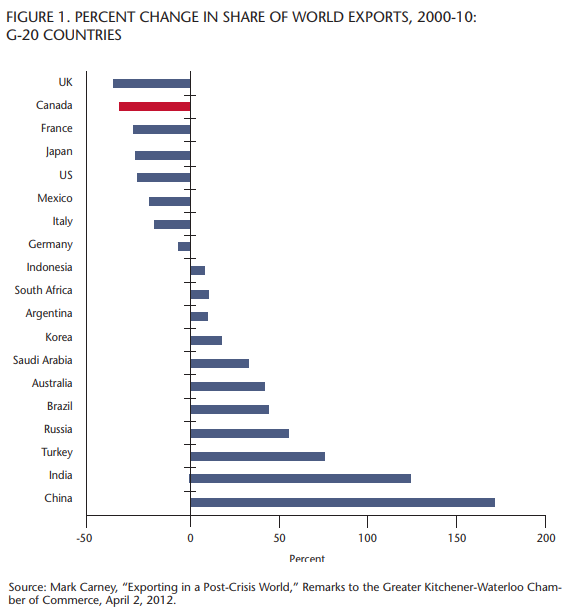

China’s trade and foreign investment have grown even faster. In 2010 it became the world’s second-largest trader, its exports ranking first and its imports second after the United States. China has scoured the world for the raw materials it needs to feed its modernization, becoming an important foreign investor in its own right. Meanwhile, global corporations have increased the flow of components for the growing range of products assembled in Chinese factories. On the export side, China’s role as the world’s leading low-cost economy has attracted overseas investment in facilities that finish a dizzying array of consumer and producer goods, resulting in a huge increase in its share of world exports (figure 1).

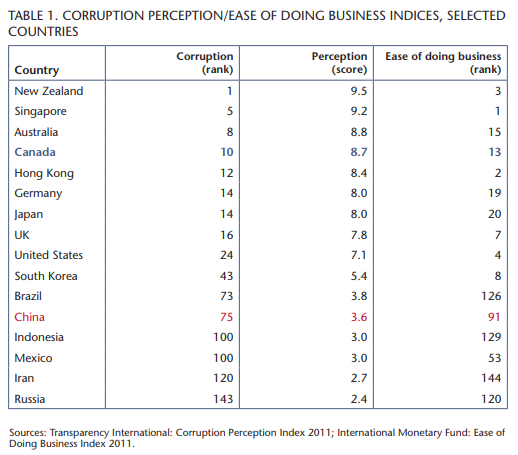

China’s rapid growth is remarkable not only for its depth and duration, but also because it took place in the absence of many of the rules and institutions that have underpinned economic growth and development in most Western economies. China does not score well on any of these. The cost of all this progress, however, has been high. Corruption permeates much of the state; inequality has reached alarming proportions; wealth is concentrated in the coastal regions, while large parts of the interior remain much poorer and more backward; and environmental degradation has reached dangerous levels (see table 1). As in other East Asian economies, maintaining development at its recent pace will pose a major challenge to China, as will the need to address environmental, social and other problems that are the inevitable result of rapid development.

Nevertheless, China’s 30-year economic reform program has lifted more people out of abject poverty than all of Western aid combined, and it has improved the well-being of millions more. Yet China remains a poor country. It can now claim more than a hundred billionaires and a larger middle class than any other country, but its poor remain as numerous as the total population of North America. Such contrasts remind us not to think of China in monolithic terms. A country this large and diverse cannot be encapsulated in a few pages. China is a tremendously complex country, rife with contradictions that would take a lifetime to appreciate fully.

The central government’s capacity to exercise control over this vast economy, for example, can easily be exaggerated, while the interests of local authorities may conflict with the interests of Beijing, adding to the difficulties that foreigners encounter when trying to do business in China. Its leaders can point to national laws and institutions that superficially appear similar to those in Canada and other market economies; in reality, such provisions are largely immaterial to the way China’s economy functions.

Instead, provincial and municipal officials exercise a high degree of discretion in attracting investment, providing permissions and applying many other regulatory requirements, subject only to broad supervision by national authorities and Communist Party officials. The nature of this supervision remains ambiguous, resulting in creative tensions between local and national officials.

With a population of more than 1.3 billion and a rapidly growing economy, China deserves full credit for its unprecedented turnaround. No other country has ever sustained double-digit growth for three decades, as did China from 1979 to 2009. If it succeeds in maintaining even half that pace, it will surpass the United States at some point in the next few decades to become the world’s largest national economy.

The fine line between nimble decision-making and corruption is not always clear. In these circumstances personal relationships, rather than rules and regulations, are paramount. Laws may be on the books, but their interpretation and implementation often hinge on whether one has carefully cultivated the right officials. This institutionalized ambiguity poses major challenges to Canadian policy-makers and business leaders who seek closer relations with China.

China’s remarkable trade performance is of particular interest to Canadians. Canada-US trade, the bread and butter of the Canadian economy through most of the postwar era, has stagnated since it reached a peak in 2000. Slow growth in the US economy, the post-9/11 thickening of the bilateral border, the reluctance of the US government to address post-North American Free Trade Agreement (NAFTA) bilateral trade issues and the emergence of Asia as a major economic force have combined to reduce the role of the US market in the Canadian economy.

China’s share of all merchandise imported into the United States reached 19.1 percent in 2010, while Canada’s share shrank to 14.5 percent.

In terms of total imports into Canada, China’s share was 11 percent, while the US share has declined to 50.4 percent. Some see China as an important contributor to the Canada-US trade malaise, taking an increasing share of Canadian exports as well as imports into both countries. On the basis of conventional trade statistics, China has overtaken Canada as the leading supplier to the US market and is now the second-largest supplier to the Canadian market.

But, like the formal governing structure, China’s trade numbers are deceptive. Much of what China exports it first imports. Thousands of foreign and Chinese firms have positioned themselves to exploit China’s comparative advantage as the final stage in sophisticated global value chains producing computers, sports equipment, clothing, household fixtures and a wide range of other products. Understanding China’s role in these global production networks is critical to understanding China’s emergence as an economic power.

China’s remarkable growth is in part the result of deliberate decisions, but it has also benefited from the reorganization of global production. At the same time that China was opening its market and inviting in foreign firms and investors, global industry was retooling to take advantage of a number of interrelated phenomena: the steady decrease in the cost of international communications and transportation, the first realization of the logistical possibilities opened up by increasingly sophisticated but low-cost computing power, and a significant reduction in government-imposed barriers to international exchange. The globalization that followed was partly a matter of growing international trade and investment, but even more the result of a reorganization of production along global lines and a concomitant increase in trade in parts and services and in international investment.

No other country has embraced the benefits of these new trade and production patterns more enthusiastically than China. The process of increasing value through disaggregation and rebundling is critical to understanding the rapid growth in China’s trade. It provided the means by which the political and economic reforms initiated in the late 1970s could be harnessed to bring development to large parts of China and its huge population of underemployed workers. China has emerged as the prime site for locating labour-intensive assembly and related activities and has replaced other Asian suppliers that have moved up the value chain to supply components used by assembly facilities in China. More than three-quarters of the value of Chinese exports represents imported components, and more than two-thirds of Chinese imports are for use in exports.

China’s trade numbers are deceptive. Much of what China exports it first imports. Thousands of foreign and Chinese firms have positioned themselves to exploit China’s comparative

advantage as the final stage in sophisticated global value chains producing computers, sports equipment, clothing, household fixtures and a wide range of other products.

The popular image of China as the manufacturing centre of the world is thus misleading. Instead, China has become an integral part of a much more complicated reality that involves leading firms in North America, Europe and Japan; resource firms all over the world; manufacturers of components in the more advanced economies of East Asia such as Korea, Taiwan and Malaysia; and final assembly in China, Vietnam and other countries in East Asia.

Chinese leaders have concluded that their success in positioning China as the point of final assembly in an integrated East and Southeast Asian manufacturing system is no longer the key to future development. They are now trying to reposition the country so that it can create a capacity for indigenous innovation, pursue scientific development, build up its own technologies and industries, and bring further inland the benefits of industrialization. If the past 30 years are anything to go by, they are likely to reach these goals sooner rather than later. Canadian firms interested in pursuing opportunities in China will do well to take these goals into account.

Three principal economic actors have played roles in China’s economic development. At the outset, China relied on its thousands of state-owned enterprises (SOEs) that were in competition with one another for foreign markets, capital and partners. As the reforms took hold, however, their role steadily declined, except in the resource sector, heavy industry, traditional low-end manufacturing (such as toys and clothing), banking and the provision of infrastructure. Many of the SOEs in these sectors are larger than the largest Canadian firms and have become significant players in the global economy.

The Fortune Global 500 list for 2011 includes 61 Chinese firms — double the number of British, German and French firms — many of which are SOEs. The success of these companies suggests that Chinese firms — private and public — understand very well how capitalism works.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

The relative decline in SOEs in other sectors has provided more and more room for foreign-invested enterprises (FIEs), initially those from Taiwan, Hong Kong, Japan and Korea and, increasingly, those from Australia, North America and Europe, either directly or through Hong Kong or Taiwanese intermediaries. Most of these FIEs are focused on consumer products for export, integrating Chinese assembly into internationally organized value chains, but some are also beginning to focus on the Chinese market.

Finally, Chinese entrepreneurs are emerging as suppliers of goods and services to SOEs and FIEs and, more recently, as providers in their own right of nontraditional, technology-intensive products for both export and domestic markets.

China’s rapid emergence as a major exporter, particularly of consumer products, has given rise to concerns about China as a fair trader, particularly in the United States, and often focused on its exchange rate and large current account surpluses. Over time, however, as has happened in other countries in similar circumstances, domestic demand will increase, particularly as the population ages and savers become spenders, albeit probably not quickly enough to satisfy US and other critics. Given Japan’s negative experience with US pressure to adjust its exchange rate in the 1980s, Chinese authorities are understandably reluctant to accede prematurely to US demands.

The oft-repeated charge that global corporations are moving capital and jobs to low-wage countries such as China at the expense of jobs and investment in North America and Europe is also simplistic and misleading. China is not replacing gross OECD output but is allowing manufacturers to continue to reap productivity gains by moving labour-intensive, less productive areas of activity offshore to China and to its suppliers of intermediate goods in the rest of Asia, and then importing finished consumer and producer goods from China, a net economic benefit to both sides.

China’s relatively weak regulatory system has given rise to serious problems resulting from the production of shoddy and even dangerous goods. For those who have short memories, however, similar concerns were expressed about shoddy Japanese, Korean and other products. China is experiencing the same phenomenon but appears to be moving up the quality ladder more quickly than Japan, Korea and others did during their transformations.

China’s determination to carry through with its decision to join the world trade regime is proving an important corrective to some of the excesses of rapid development. No other country has been scrutinized at such an exacting level of detail nor has any other acceding country been required to accept as many concessions and conditions. The accession process took 15 years (1986-2001) and involved stipulating numerous Chinese commitments to make its trade and economic laws and practice much more transparent, uniform, predictable and market-oriented. Reviews of these commitments by the WTO’s trade policy review body every other year since 2006 indicate that China is making steady progress in meeting them.

China’s record on human rights is another area of Western concern, and rightly so. China remains a totalitarian state, and dissenting voices that threaten the control of the Communist Party and the central authorities are ruthlessly stamped out. That being said, the quality of life of most Chinese citizens has improved substantially over the past 30 years. The standard of living has improved, and the range of available consumer products has greatly increased. Private property rights are gradually being recognized. Newpapers and journals have proliferated. Access to the Internet, while subject to censorship, has become widespread. Dissent and fierce internal discussion is not uncommon, although subject to the overall caveat of staying away from dissent and comment that the central authorities consider threatening. Foreign travel is now allowed for most Chinese, and internal passports are enforced more flexibly, which has resulted in both corruption and more freedom. Most urban residents have become responsible for finding their own jobs, accommodation and transportation on a competitive basis.

But there remain limits that would be intolerable in a Western democracy. How long this can continue is one of the great questions facing China and the world. Direct criticism by foreign governments of this fault line has proven counterproductive, as Prime Minister Stephen Harper appears to have concluded. Chinese authorities like to point to the many developments outlined above and to contrast their pragmatic approach to that of the failed communist regimes in Europe and to that of many other developing countries. The direction of change is clear, indicating that with greater prosperity will come more pressure to loosen the bonds further.

On balance, a prosperous China is in Canada’s — and the world’s — political and economic interests, and while it may have short-term negative effects on individual firms and workers, the long-term impact on the prosperity of Canadians should be positive. While human rights concerns and the absence of democratic rights remain serious challenges, a weakened China could well let loose nationalist and militaristic forces that would be much more destabilizing to global peace and prosperity.

Canadians have contributed materially to the emergence of China. As consumers, they have contributed to the demand for low-cost finished goods, whether clothing and footwear or electronics and machinery. As traders and investors, they have begun to turn to China as the location of choice for labour-intensive operations in increasingly sophisticated global value chains, as well as a potential market for Canadian goods. Canadian manufacturers have been relatively minor participants in this process, often as junior partners in US-anchored value chains. In contrast, Canadian resource firms increasingly are suppliers of raw materials for the Chinese economy and major beneficiaries of the Chinese-fuelled global commodity boom. Canadian firms, for example, are major suppliers of organic chemicals such as ethylene glycol, a key ingredient in man-made fibres for the clothing industry, as well as coal, wheat, canola oil, wood pulp for paper-making, and other commodities.

Even in areas for which Canada is not a major supplier, Chinese demand has driven up world prices, strengthening the position of Canada’s resource sector. Finally, Canadian service firms are beginning to penetrate the Chinese economy. Manulife Financial, for example, is active in 50 Chinese provinces and municipalities and is now China’s largest foreign supplier of insurance and other financial instruments.

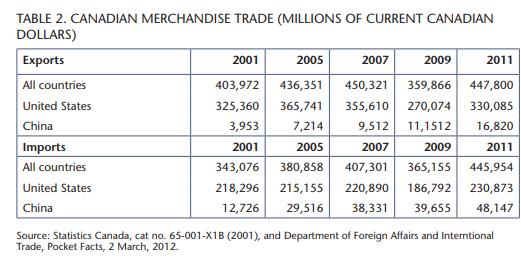

As a result, China has been Canada’s fastest-growing trading partner over the past decade, albeit from a relatively small base, growing at a rate 10 times faster than trade with the rest of the world (see table 2). Not only has the emergence of China as a major player in global trade improved Canada’s terms of trade, it has also contributed to a marked diversification in Canadian trade patterns. Similar to Australian firms, Canadian resource companies have benefited enormously from the global surge in resource prices stimulated by rising demand in Asia. Canada is well positioned to increase trade across the Pacific. Both South and East Asia are hungry for energy and raw materials, and Canada is potentially a much more reliable and stable supplier than African, Latin American and Middle Eastern suppliers. More will need to be done, however, to improve transportation infrastructure on the West Coast and remove regulatory bottlenecks.

Even if growth slows to half the pace of the past 30 years, there will be substantial trade and investment opportunities for many years to come. Canada has been relatively late in forging relationships in Asia, both private and public. Nevertheless, the base is sufficient to suggest that a concerted strategy of greater engagement will pay major dividends.

Such a strategy requires active engagement on the part of both the government and the private sector. The success of government initiatives will depend on critical feedback and support from the private sector and clear evidence that Canadian firms are prepared to become more actively involved in transpacific markets. Government activity should build on the initiatives already underway, but there needs to be more resolve and a willingness to take on entrenched domestic protectionist forces.

At the same time, efforts in Canada to strengthen the required infrastructure, to reduce regulatory bottlenecks and to raise awareness of Canadian interests in Asia will help to ensure that efforts to enhance transpacific engagement will lead to sustained market growth. Canadians’ awareness of the importance of trade and investment and of the emergence of China and the rest of Asia is episodic and easily derailed by protectionist and other interests. Both government and business leaders need to be prepared to speak out and exercise leadership in making a robust Canadian transpacific presence a reality.

Photo: Shutterstock