Post-secondary education (PSE) student financial aid systems in Canada use parental income information to calculate how much money students are expected to receive from their parents and adjust the assistance provided accordingly. But new evidence using a unique data set suggests that estimates of what parents contribute are in many cases inaccurate, leaving some students at a disadvantage.

The data also show that the education of the parents appears to be a more significant determinant of parental financial contributions than family income, contributing to a growing body of evidence that parental education is significant when it comes to youths’ PSE opportunities.

Our findings thus challenge assumptions about the way youths’ PSE experiences are funded and about the system that is meant to broaden opportunities for students. We suggest that students facing parental contribution shortfalls may need alternative avenues for financial support, and that perhaps formulas for determining parental contributions should be revisited.

Here’s how the current system works. Applicants for student financial aid are classified as either ”dependent” or ”independent,” according to preset criteria that judge whether a student should rely financially on their parents. For example, all married students are deemed to be independent of their parents.

Most student financial aid applicants are classified as dependent, and for these individuals, parental income factors into their eligibility for financial aid. Dependent students from families with incomes higher than what is deemed sufficient to maintain a basic standard of living (which varies by province) are considered to have discretionary income. A portion of this discretionary income is considered to be available to the student and determines the system’s calculation of the ”expected parental contribution.”

Financial aid eligibility is determined by calculating the financial resources available to the student and their schooling costs (principally tuition and other student fees plus -living costs). If a student’s resources from all sources — including the expected parental contribution and the student’s own earnings — are deemed sufficient to cover all schooling costs, the student will not qualify for assistance.

But if the student’s resources are deemed to be insufficient to meet their financial needs, they will qualify for financial aid; the amount will depend on their assessed need. So a student’s expected parental contribution affects whether they qualify for aid and, if so, the amount of aid awarded.

Whether a student actually receives the expected -parental contribution does not, however, factor into their eligibility. In other words, it is only the assumed contribution that affects eligibility, not the actual amount. But in reality, some students do not receive the expected parental contribution assumed by the government formulas, while others receive more than expected. This potentially results in financial hardship for those students who face contribution shortfalls and, conversely, a more comfortable situation for those who receive overcontributions.

Perhaps formulas for determining parental contributions should be revisited.

To explore the differences between expected and actual contributions, we use a unique data set that links student financial aid administrative data, which include information on expected parental contribution amounts, with survey data, which include information about the actual amounts students received from parents.

Our sample consists of students who received the Millennium Access Bursary (MAB), targeted toward lower-income students, in 2005, as well as some students who narrowly missed receiving the bursary. The sample comprises around 7,470 students, all from Nova Scotia, Ontario and British Columbia. The unique nature of our sample precludes us from generalizing our results to the general population, and the relationships may have changed since these data were collected. That said, the results are interesting, and they suggest that further research is needed, including into the policy implications.

The average expected parental contribution of the students in our sample was $820, but they actually received an average of $1,520 from their parents, an average parental overcontribution of $700. From another perspective, 74.7 percent of students received a parental contribution equal to or above their expected amount.

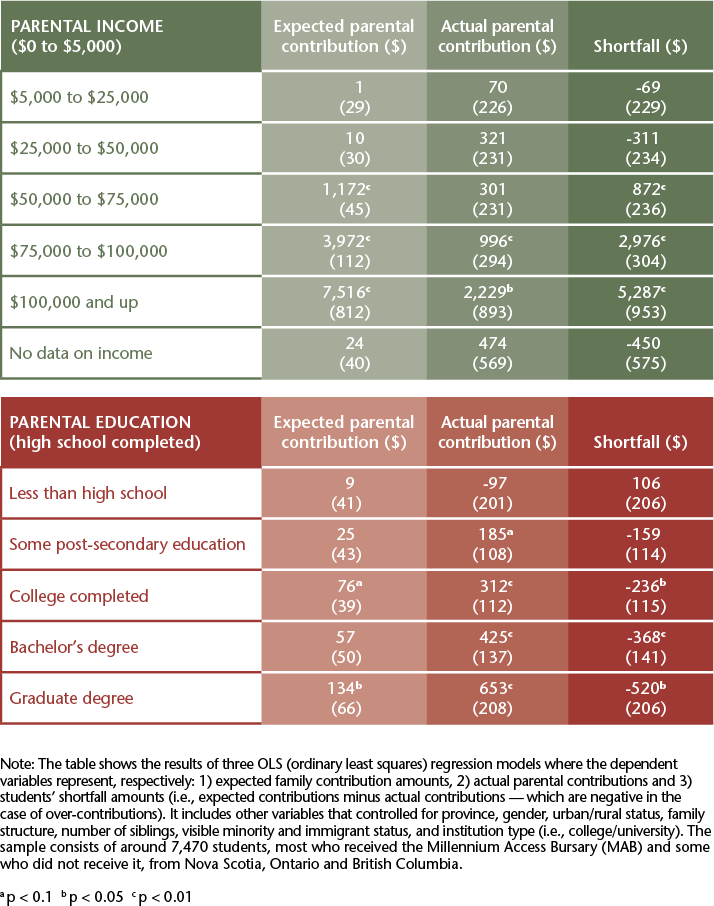

Using a regression analysis (see the table), we see that parental income is indeed the principal characteristic that determines the expected parental contribution. Controlling for income and other factors included in our analysis, parental education does not appear to be related to expected contributions. This is as expected, since expected contributions are based on parental income, and parental education is not taken into account.

The inner workings of government

Who’s doing what to get federal policy made. In The Functionary.

The inner workings of government

Who’s doing what to get federal policy made. In The Functionary.

Parental income is much less sharply related to actual parental contributions, and here parental education is found to play a significant role. The net effect is that higher parental incomes are strongly associated with shortfalls in parental contributions, while higher parental education is associated with students receiving more financial support from their parents than is expected by student financial aid systems.

These results are consistent with the emerging evidence that suggests that parental education is a stronger determinant of PSE participation than family income. At all income levels, youth with highly educated parents are more likely than others to pursue PSE, and this may be at least in part because of the financial aid they receive from their parents. Parental education likely affects PSE access in other ways, however, such as the importance parents attach to their children’s academic achievements and how they help their children prepare for PSE. Hence, we cannot say whether parents’ financial contributions have a direct effect on their children’s education choices or whether these factors are only spuriously correlated.

This cautionary statement is especially important in a context where emerging evidence suggests that financial barriers are only rarely the principal factor in a young person’s decision not to attend PSE. Nevertheless, parental contribution shortfalls and overcontributions of the type identified here may be part of the broad set of family-based factors that determine not only who attends PSE, but which level of PSE they attend, as well as how students get by in PSE and beyond once those schooling choices have been made.

We also used our data to determine whether parental contribution shortfalls are related to student -experiences and outcomes among those who attend PSE. We find that students facing parental contribution shortfalls are more likely to work for money and to study less; yet, interestingly, their grades are not lower and they are no more likely to drop out of school. Disentangling the causality of these relationships is beyond the scope of our analysis. However, examples of such causality are that students may work more because they face a parental contribution shortfall, or parents may give their children less money if they think it is not needed because the student has their own earnings. Similarly, performance is related to a broad range of factors, many of them mutually dependent. These relationships are relevant to student financial aid systems and merit further study.

Our findings challenge assumptions about the system that is meant to broaden students’ opportunities.

Our results could lead some policy-makers to conclude that student financial aid formulas should be revised to consider the contributions that students actually receive from their parents rather than what they are expected to receive. Such a change could pose problems, such as those relating to verifying actual parental contributions, and potential incentive effects, as parents may be inclined to give less if they believe the financial aid system will fill any gap that is left.

Furthermore, actual parental contributions flow to students over the course of a school year and could therefore be measured only at that time, while students need to know how much money they are going to receive from government sources before the school year begins. Hence, such a system would have critical timing problems.

Some systems in Northern European and Scandinavian countries circumvent these issues by assuming all students are independent of their parents, and hence provide student financial aid independently of parental income levels. This may be attractive, and it would get around the problem of parental undercontributions documented here, but it would also result in many students from wealthy families receiving financial aid, the same amount as those from lower-income families. This would result in an inefficient targeting of student aid money and would exacerbate the overcontribution side of the problem.

Another approach would be to find a way for students facing parental contribution shortfalls to receive additional funds; unsubsidized loans might be a compromise measure in this respect. This could provide students with the money they need, while minimizing the disincentive effects noted above. In this context, it would be useful to better understand the degree to which the substantial amount of institution-based student financial assistance (much of this coming from tuition fee increases since the mid-1990s) currently fills these gaps.

The problem of parents not giving as much to their children as student financial aid systems assume has always existed in theory, but there has never been much empirical evidence for it. We hope our work will push those considerations further along and spark new research, given the potential implications of our findings both for the financial aid system and for students’ schooling opportunities. There are no perfect solutions here, but perhaps we can do better by, for example, tweaking expected-parental-contribution formulas and providing alternative sources of aid for students who need it.

Photo: Shutterstock by ultramansk

Do you have something to say about the article you just read? Be part of the Policy Options discussion, and send in your own submission. Here is a link on how to do it. | Souhaitez-vous réagir à cet article ? Joignez-vous aux débats d’Options politiques et soumettez-nous votre texte en suivant ces directives.