Investors who wish to address climate change in the construction of portfolios often seek to reduce their dependence on investments connected to the fossil fuel industry. One growing response and framework for decision-making is to quantify an investment portfolio’s “carbon footprint.”

A number of proponents, including the United Nations through the Montreal Carbon Pledge and the largest public pension fund in the United States, argue that measuring and disclosing the carbon footprint of portfolios will encourage firms to reduce carbon emissions and help quantify and manage climate-change-related risks. The University of Ottawa and Simon Fraser University (SFU) have gone a step farther and made ambitious-sounding commitments to reduce the carbon footprints of their endowments by 30 percent by 2030. They argue this target is in line with Canada’s own commitment to reduce greenhouse gas emissions by 30 percent by 2030, and have presented carbon footprint reductions as an alternative to the full divestment from the fossil fuel industry that is being called for by campus groups.

Are investment carbon footprints useful in reducing greenhouse gas emissions or reducing climate risks to portfolios? The answer hinges on the meaning of “carbon footprint” as used by the finance industry. Investors and institutions using the investment industry’s definitions of “carbon footprint” should be aware that by relying on this methodology, they may fail to lower climate risks to portfolios. They may even exacerbate the problem of climate change. A few real-world examples help illustrate how investment carbon footprints work, where they are useful and where they are not.

While reducing a carbon footprint sounds beneficial for reducing both greenhouse gas emissions and investment risks, a closer look reveals some surprising consequences of the underlying methodology. For example, investments in coal mining are credited with lower carbon footprints than investments in natural gas extraction. Moving an investment from aircraft manufacturing into solar panel production can increase your carbon footprint by 70 percent. And at least one existing low-carbon fund recently claimed an 84 percent lower carbon footprint, despite reducing its investments in clean energy by 30 percent and maintaining investments in large fossil fuel companies like ExxonMobil, Shell and Kinder Morgan.

In understanding the carbon footprint of investments, it helps to understand the carbon footprints of physical products.

In understanding the carbon footprint of investments, it helps to first understand the carbon footprints of physical products. The carbon footprint of a product is simply the total greenhouse gas emissions released to produce it. This includes the direct carbon emissions, such as from burning natural gas in the factory and gasoline used to transport the product to market, as well as indirect emissions from earlier stages of production and those released to generate electricity used by the factory. By comparing the carbon footprint of similar products, a consumer can choose the one with lower embodied emissions.

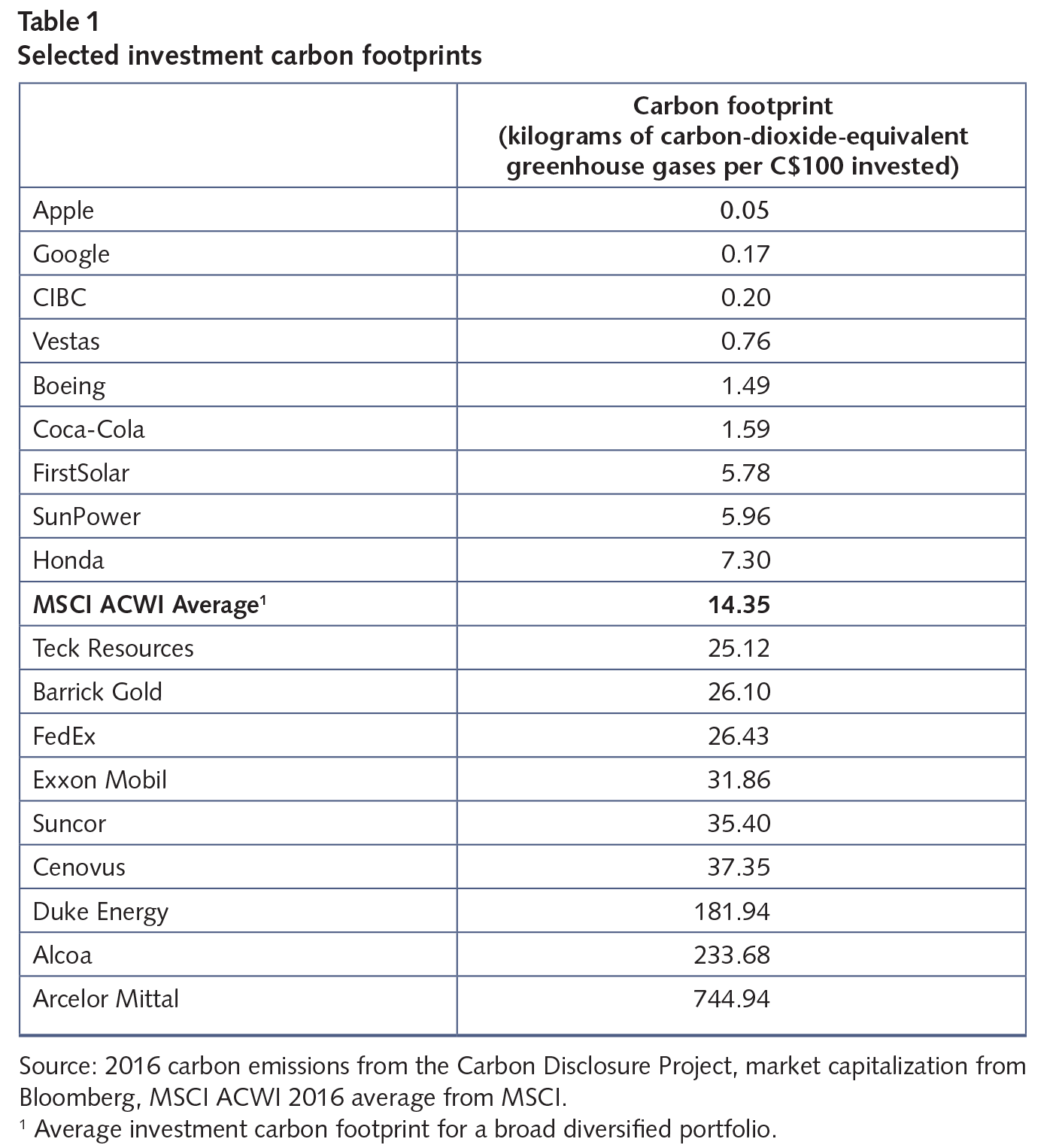

The carbon footprint of an investment is similar to that of a product, but with important differences. It is the total carbon emissions emitted by a company from its operations, including both directly emitted greenhouse gases and indirect emissions required to produce electricity used by the firm. The footprint is distributed pro rata across the company’s shareholders. If you purchase 1 percent of a company’s value, you take responsibility for 1 percent of its annual carbon emissions. Sell that investment and purchase shares in a different company with lower carbon emissions (per dollar of value), and you’ll lower your investment’s carbon footprint. (See table 1 for examples of some companies’ carbon footprints.)

Taking a weighted average of carbon footprints of individual companies, you can calculate and compare the carbon footprint of different portfolios. However, reducing a portfolio’s carbon footprint bears little relation to changes in real-world carbon emissions and can lead to counterintuitive investment decisions when comparing footprints across different industries, stages of production and products.

The problem is that footprints for stages of production are not necessarily a good guide for a technology’s total climate impact. For example, approximately 99 percent of the life-cycle emissions from coal-fired electricity occur downstream from coal mining and therefore are excluded from a mining company’s investment carbon footprint (even after accounting for electricity used in coal mining). As a result, Canada’s largest coal mining company, Teck, has a 30 percent lower investment carbon footprint than several large Canadian natural gas producers, even though coal-fired electricity generates 60 percent more carbon emissions per unit of electricity than natural gas. So Teck largely escapes responsibility for the carbon emissions of burning the coal it mines. In contrast, extracting natural gas can be a relatively emissions-intensive process and thus has a high investment carbon footprint.

Another striking example is manufacturing solar panels. Large US solar panel producers typically have substantially higher investment carbon footprints than, for example, the financial sector or many manufacturing firms. This occurs in part because approximately 95 percent of the carbon footprint for large US solar panel producers comes from the electricity they use in their manufacturing processes — electricity typically generated from fossil fuels. Yet they receive no credit to their carbon footprint for clean energy generated by the panels once they are sold.

There’s nothing intrinsically wrong with this attribution of emissions to firms’ investment carbon footprints. However, following investment carbon footprints would lead one to conclude that investing in coal mining is preferable — from a climate perspective — to investing in natural gas, and building airplanes is preferable to investing in solar panel manufacturing. This makes investment carbon footprints a poor — and potentially counterproductive — guide to where investments should be made to lower future carbon emissions and reduce risks associated with efforts to address climate change.

Encouraging the disclosure of carbon emissions does help investors understand the risks firms face and the steps firms are taking to mitigate them. However, actively reducing portfolio carbon footprints is unlikely to materially impact the decisions firms make or to reduce carbon emissions. This is in part because of the counterintuitive investment incentives discussed previously, and in part because buying and selling stocks is an accounting transaction, not a change that alters physical consumption.

Selling stocks in coal mining and investing in natural gas means other investors have sold their natural gas stocks and bought coal shares. There has been no change to the real-world products, and any impacts on the stock price are minuscule for most investors. Lowering the investment carbon footprint of a portfolio may change the attribution of emissions across investors but doesn’t directly reduce any greenhouse gas emissions. In other words, the reductions that SFU and the University of Ottawa have made in their endowments’ footprints represent an accounting change, while measures to reach Canada’s goal to reduce emissions by 30 percent by 2030 would represent a physical change.

A further limitation to using investment carbon footprints as a proxy for climate-related investment risks is the manner in which low-carbon investments are chosen. To reduce the volatility of returns, the selection of investments to be held by low-carbon funds is subject to several constraints. These typically include minimum and maximum investment amounts that a fund must maintain in different industries and limits to how much the returns of a low-carbon fund can diverge from those of a fully diversified fund. Constraints on the minimum industry investments a fund must maintain can result in lower carbon footprints, without lowering that fund’s reliance on fossil fuels: for example, by forcing a shift in investments within the energy sector from oil extraction to oilfield service or pipeline companies. A consequence of these constraints is that low-carbon funds may remain as exposed to the risk of a “carbon bubble” — when companies dependent on fossil fuels are dangerously overvalued — as the fully diversified fund would be.

Furthermore, investment carbon footprints do not reflect how firms can pass on costs from regulations on greenhouse gas emissions through higher prices for consumers, or how readily they can substitute alternative energy sources or change production processes. FedEx, with a higher carbon footprint than Teck, may find it relatively easy to adapt to high carbon prices by switching to electric or natural gas vehicles. Similarly, Alcoa, despite its currently high carbon footprint, may relocate smelters to areas offering abundant low-carbon electricity or pass on the higher cost of energy to firms that buy its aluminum. A company based on extracting fossil fuels, despite a lower carbon footprint, may not find it so easy to adapt to a carbon-constrained world.

With such significant limitations, what’s an institution or investor to do? There’s no silver bullet. One option is to continue to use investment carbon footprints while being aware of their downsides. In the longer term, lowering carbon footprints through investment changes within narrow industry classes could allow like-versus-like comparisons of firms that reflect true emissions intensity — not comparisons across different products or stages of production. An alternative being pursued by the University of British Columbia — also under pressure to pursue fossil fuel divestment — is a combination of preferring firms with lower investment carbon footprints and screening out firms that are heavily reliant on extracting fossil fuels. Perhaps most important, adequate carbon pricing and regulations to reduce emissions would remove some of the need for the calculation of investment carbon footprints.

In the meantime, using investment carbon footprints does send a market signal that many investors want more rigorous methods for quantifying exposure to fossil fuels and climate risks. It also sends a political and moral signal on the need for stronger climate action. But if institutions and investors decide to continue relying on investment carbon footprints, they should do so with care.

Photo: Shutterstock, by geniusksy

Do you have something to say about the article you just read? Be part of the Policy Options discussion, and send in your own submission. Here is a link on how to do it. | Souhaitez-vous réagir à cet article ? Joignez-vous aux débats d’Options politiques et soumettez-nous votre texte en suivant ces directives.