The 2008-09 economic downturn in Canada was global in scope. This worldwide financial meltdown affected our economy through trade and financial linkages. As we know, Canada’s real GDP experienced contraction in the final quarter of 2008 and fell further in 2009. In response to Canada’s gloomy economic prospect, the Bank of Canada followed a very easy monetary policy with low interest rates and increased liquidity. Fiscal policy, at the same time, followed a very stimulative path. Indeed, Canada’s Economic Action Plan provided $40 billion of stimulative package over a two-year period.

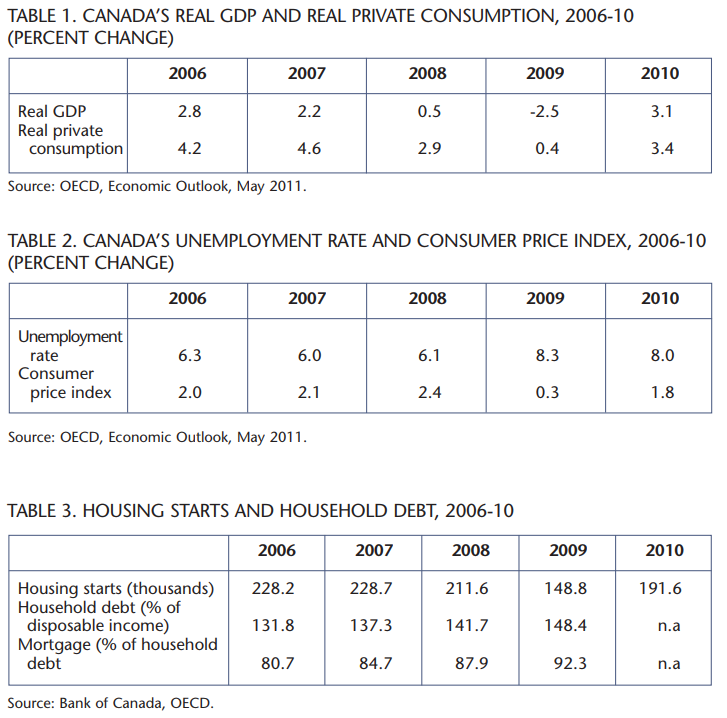

The fiscal package included financial incentives on construction and home building activities; federal infrastructure projects such as roads, highways, public transport and bridges; and lowering of corporate and individual tax burdens in order to help the Canadian economy create the firm traction needed for a growth path. Indeed, Canada’s real GDP grew by 3.1 percent in 2010 after a decline of 2.5 percent in 2009 (see table 1).

Since then, the Canadian economic recovery has slowed down considerably. This relates to the international financial landscape, which has deteriorated due to the European debt crisis, combined with the poor economic performance in Europe and the United States. Canada’s unemployment rate, which improved nicely during 2010 and early last year, unfortunately weakened in recent months. After a small gain of 2,300 jobs in January this year, Canada lost 2,800 in February, according to Statistics Canada. The unemployment rate is estimated to reach 7.5 percent this year from 7.4 percent in 2011, as projected by the federal budget 2012. It is worth noting that our retail prices, as measured by CPI, remain subdued (see table 2).

The Organisation for Economic Co-operation and Development (OECD) as well as most economists and policy makers including Bank of Canada, have revised downward the economic prospects of Canada for this year and next. It is now expected that Canada’s real GDP will grow by 2.1 percent this year and under 2.5 percent in 2013. This downward revision of Canada’s economic fortune is largely due to the European debt crisis, which has created financial and economic uncertainties globally. Lack of a timely and orderly solution of sovereign debt problems in the European nations, combined with higher oil prices, has created recessions in many European countries and has slowed down economic recovery in the US. As well, very soft and fragile economic conditions in Europe have weakened growth prospects in emerging economies, notably in China and India. This in turn will limit our exports and employment in this sector and ultimately will cut our GDP growth through its multiplier effect.

In this bleak economic scenario many observers and policy-makers will urge the Canadian government to provide fiscal stimulus, as they did during the 2008-09 recession. However, I argue in this article that Canada does not require fiscal stimulus now.

Moreover, fiscal stimulus, if used, will certainly fail to yield desired results due to some technical limitations, as discussed below. The government, however, in order to maintain confidence in our government policy, must allow the extension of deadlines for completion of infrastructure projects that are yet incomplete. No doubt, the Canadian economy is getting support from the Bank of Canada’s easy monetary policy with historical low interest rates and from comfortable liquidity in the system. No further support from the fiscal side is warranted at this time. Fiscal stimulus should be used for short-term macroeconomic stabilization purposes only. It should not be used for structural economic problems. One needs to balance the costs and benefits of any fiscal package before implementing it. Otherwise, excessive deficit spending by the government to finance a stimulus package will burden the structural deficit problem and, indeed, will limit economic growth in future years.

No further support from the fiscal side is warranted at this time. Fiscal stimulus should be used for short-term macroeconomic stabilization purposes only. It should not be used for structural economic problems. One needs to balance the costs and benefits of any fiscal package before implementing it.

The most frequently used fiscal tools to stimulate the economy are these:

- Tax incentives to stimulate home construction and home ownership;

- Accelerated capital cost allowance to encourage the business sector to make new investments;

- Lower corporate tax rates to encourage new employment;

- Expansion of federal infrastructure projects.

Canada’s housing sector did not experience the same degree of imbalance as in the USA during the 200809 recession. Canada’s housing starts have fully recovered from a small dip recorded during the recession and currently hover around the 200,000 mark (see table 3). This level of starts, in my judgment, provides a good balance between supply and demand. Any policy-induced housing activity will create an imbalance in this sector, with the risk of a housing bubble. Moreover, household debt for mortgages in relation to disposable income has reached a lofty high level. Any policy-induced home ownership will further burden ordinary

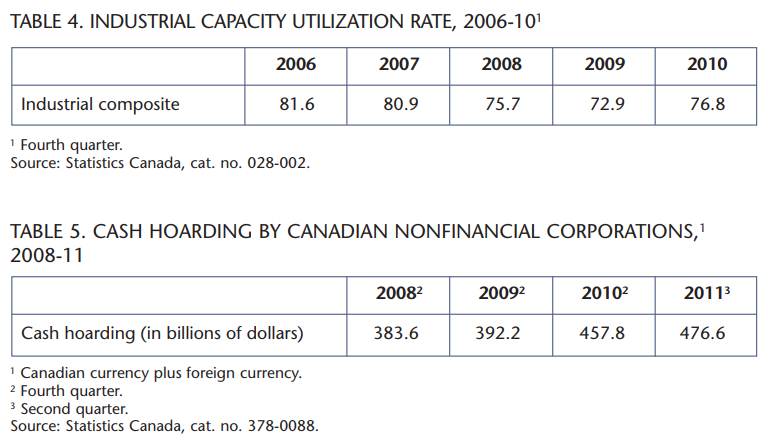

Canadians financially. Another fiscal tool commonly used to stimulate the economy is an accelerated depreciation program. From a corporate perspective, this kind of incentive increases after-tax profits and their cash flows. However, I will argue this tool will not be effective in the current economic situation as the capacity utilization rates are already very low, suggesting that any further increase in capacity will remain idle and wasteful (see table 4).

More importantly, Canadian corporate balance sheets are in good order and flush with cash (see table 5). It is no secret that corporate houses are reluctant to invest in plant and equipment or in technology, largely due to uncertainty about the future demand of their products and of the financial risks felt globally by the European sovereign debt crisis. Indeed, the balance sheet of nonfinancial corporations in Canada reveals that they are sitting on a firepower of cash. Unfortunately, they are not hungry to invest at the moment. Already there is sufficient unused capacity in the system, as referenced earlier, that would allow businesses to increase production should our economy bounce back more quickly and vigorously than currently anticipated. There is no animal spirit” to invest in new projects. As the saying goes, you can take a horse to water but he will not drink if he is not thirsty. Therefore, in the current environment any stimulus in the form of accelerated capital cost allowance will not be effective.

Another popular fiscal tool that is often used in the stimulus package is reduction of corporate tax rates. It is argued that by cutting the corporate income tax rate, businesses will create loads of jobs as the aftertax profits rise and cash flows increase. Indeed, the corporate income tax rate has been falling since 2006 from 21 percent to a proposed 15 percent in 2012. However, it is debatable whether corporate tax cuts pay off by increased job creation. A recent rigorous study by David Macdonald of the Canadian Centre for Policy Alternatives (CCPA) has concluded that corporate income tax cuts failed as efficient means of creating jobs in Canada. Moreover, a recent study by Jack Mintz of the University of Calgary has shown that it would take a long seven years to see the full benefits of corporate tax cuts. Thus, corporate income tax cuts to encourage job creation in the current economic situation are not worth considering.

In sum, Canada’s economy has slowed down considerably since the euro zone sovereign debt crisis. Most forecasters have revised downwards their economic prognostication for Canada for this year and next. However, Canada’s economic fundamentals are in a reasonably good shape considering the early stage of economic growth path. Canada’s housing market is still robust. Its corporations are sitting on a lot of cash. Canada’s public debt to GDP ratio is very low and well below most OECD nations’. Thus the massive fiscal stimulus unleashed during the 2008-09 recession will not be required under the current economic scenario. I have argued in this paper that there is no need for fiscal dosage to uplift our economy as such a policy would prove to be ineffective. Indeed, the federal budget of 2012, as delivered by the Finance Minister Jim Flaherty on March 29, did not provide any fiscal stimulus. Rather, the budget tried to reshape Canada by balancing the long-term and shortterm fiscal objectives of the Harper Government. It did so by announcing spending cutbacks of $5.2 billion, the elimination of 19,200 federal jobs over the next three years and no increase in taxes. These measures are the Finance Minister’s attempt at fiscal prudence in balancing Ottawa’s books by 2015.

Photo: Shutterstock