Canadians thinking about changing their monetary regime—abandoning a floating exchange rate and inflation targets for a pegged exchange rate, or perhaps giving the Canadian dollar up altogether—need to beware of the well-known illusion that the grass is greener on the other side of the fence. Canadians know the fields on their side of North America’s monetary fence well. And on the other side of this fence, they see a US economy that by most measures has outpaced theirs, despite the growing trade and investment links between the two countries. Partly because we usually measure economic performance on a monetary scale, the Canadian dollar’s long-term decline against the US dollar—from rough parity in the mid-1970s to less than 65 US cents at this writing—seems closely linked to Canada’s relative decline, and some people even see it as a contributor.

In some respects, US grass is indeed greener. Careful inspection, however, suggests that the monetary field— central bank accountability to elected representatives, exchange-rate regimes, and financial industry regulation—is not where Canada’s problems lie. As the discussion between Milton Friedman and Robert Mundell in these pages shows, it is hard to make a strong case that domestic inflation targets and a floating exchange rate are worse than importing another country’s monetary order through a fixed exchange rate. And while advocates tend to argue that a different monetary regime would promote better economic policies in Canada, there are good reasons for thinking it might promote worse ones.

At the least, Canadians risk deciding to plough under their own fields only to learn that the grass on the other side is less green than they thought. Adopting the US dollar not only takes control over inflation away from Canadian policymakers. It also confronts them with an unpalatable choice: either lose the central banking services that support Canada’s financial system, or allow regulators accountable to US voters to supervise Canadian banks. The outcome could be an awkward attempt to perch atop the fence—abandoning inflation targets and pegging the Canadian dollar to the US dollar—only to have the peg give way in a crisis, leaving Canada monetarily adrift.

Canadians would do better to think less about the fence and what it would be like to live on the other side of it and more about measures such as tax reform and growth-oriented programs that would make the grass greener on our side of the fence.

For a useful perspective on greenness, it helps to spend a moment on hands and knees— metaphorically speaking—taking a close look at the grass on Canada’s side of the fence.

Canada’s monetary field is home to a currency issued by a central bank that is accountable to the Minister of Finance and, through the Minister, to Parliament. The Bank of Canada’s unique power to create Canadian dollars lets it do two related things.

On a macro level, the Bank largely controls the pace of money and credit growth and the level of short-term interest rates in Canada. This control allows the Bank to influence Canada’s economic cycle and control its rate of inflation. On a micro level, its power to create money makes the Bank a key player in the clearing systems at the core of most of Canadians’ daily financial transactions. This role, and the supervisory and regulatory powers that go with it, allows the Bank to support financial institutions that run temporarily short of funds, and to prevent failures from causing panics and more general collapses.

Americans who take an up-close look at their own grass find that things look much the same. The US Federal Reserve answers to elected representatives; it controls money growth and inflation; and it greases the wheels of the US banking system in normal times, and steps in with support when things go wrong.

The fact that the two lawns are very much alike does not mean that merging them would be a good idea, however. If Canadians and Americans did share the same monetary turf, things would be different.

First, Canadians would be playing on American grass. Some Canadian commentators have advocated new supranational currencies that Canada might adopt or fix to. But US public debate gives scant support to predictions that the US would back such a move. The US has shown no interest in a new world currency or even a western hemisphere currency alongside the US dollar—and since there are advocates for adopting the US dollar in both its northern and southern neighbours, there is no reason to expect any such interest to develop. Moreover, neither Americans nor Canadians, who would be massively outvoted in any supranational arrangement, want the sort of European-style political engagement that would support a currency union.

If Canadians did want a currency union, then, the only one on offer is formal adoption of the US dollar. A vestigial paper currency (like Scotland’s), identical in function to the US dollar but with a Canadian landscape or political icon on one side, would be an optical concession to Canadian pride with no substantive implications for anything that follows. Whatever the design, Canada would use the US dollar, and the central bank issuing it still would be the Fed, with a Chairman appointed by the US president and formal accountability to the US Congress.

Using the US dollar would grate on Canadian sensibilities. In strict macroeconomic terms, however, it would raise problems but no overwhelming objections. As Professor Mundell points out, the essential choices on offer are among different monetary policy rules. Inflation targets with a floating exchange rate constitute a monetary order that, to adopt the terminology of the University of Western Ontario’s David Laidler’s, is “coherent”: a central bank mandated by elected representatives to fulfil a task that is within the technical competence of monetary policy. Adopting the US dollar and committing to adjust as the Fed’s objectives required would also be coherent. Since US public debate supports no expectation that conditions in countries using the US dollar would enter into the formulation of the Fed’s monetary policy, Canadians would get the short-term fluctuations and long-term inflation that US political and economic conditions dictated for it.

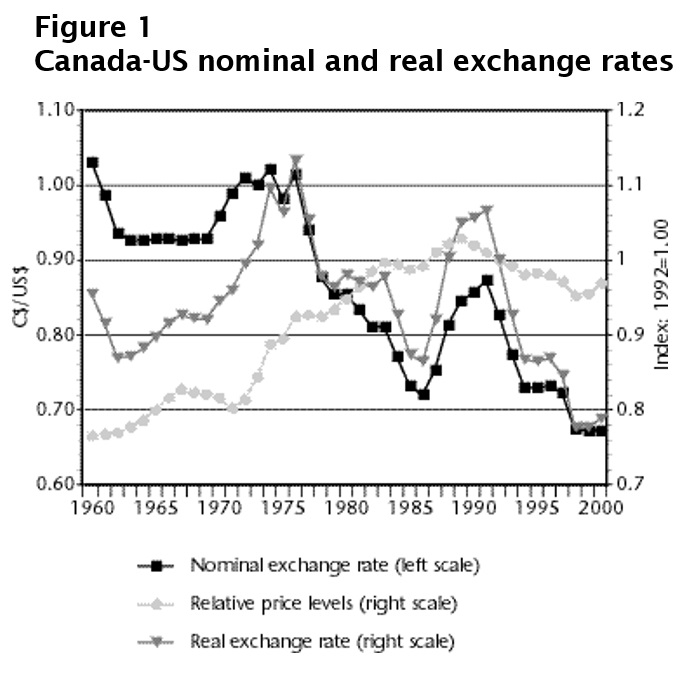

Some hints about possible Canadian experience under a monetary union are available from history. Canada ended its last experiment with a fixed exchange rate when it abandoned its peg at 92.5 US cents in 1970. Figure 1 shows the Canadian/US dollar nominal exchange rate, the ratio of the Canadian and US price levels (as measured by implicit price indexes for GDP), and the Canadian/US dollar real exchange rate since 1960. (The real exchange rate measures the exchange rate net of movements in the two countries’ price levels.) Despite what some commentators on the fundamental capriciousness of financial markets imply, the real exchange rate is clearly influenced by real forces such as changes in Canada’s terms of trade and attractiveness for capital investment. If the nominal exchange rate had not been permitted to vary after 1970, the impact of these forces would have resulted in different relative movements in the Canadian and US price levels.

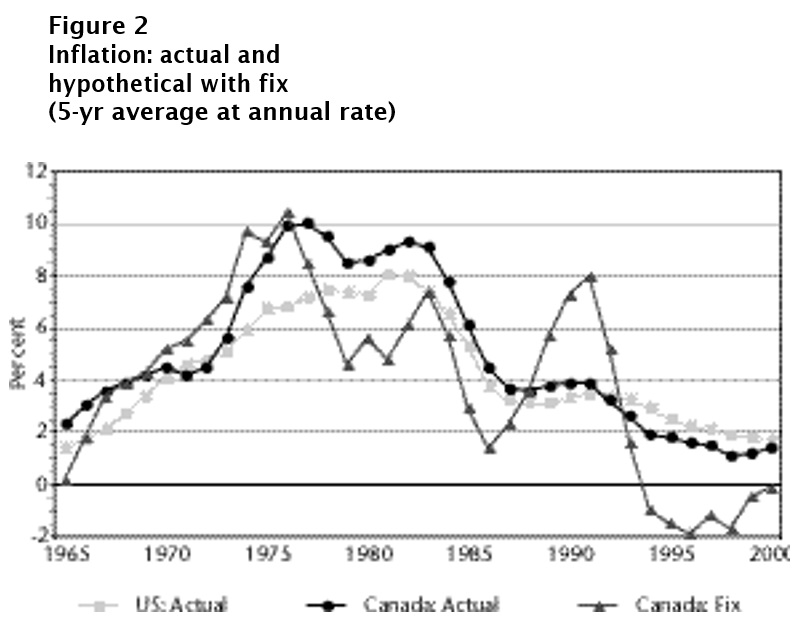

The flavour of the result Canadians could have expected is given by Figure 2, which shows five-year average inflation rates since 1970: actual experience in the US, actual experience in Canada, and the movements that would have been required in Canada to produce the same real exchange rate profile as actually occurred. (Absent perfectly flexible prices and costs, the short-run impact of the peg would have been felt more in output. The figure uses five-year averages to abstract from these shorter-run impacts.) Maintaining the peg would have given Canada higher inflation in the mid-1970s: The upward pressure on Canada’s real exchange rate from the commodity boom would have shown up less in the nominal exchange-rate appreciation that actually occurred, and more in domestic prices. Subsequently, downward pressure on the real exchange rate would have reversed the situation. Without a depreciating nominal exchange rate, domestic prices could not have risen as fast as they did. The disinflation of the 1980s would have been more pronounced, and the disinflation of the 1990s would have been an actual deflation, with several years of declining prices.

On average over the entire period, maintaining a fixed exchange rate would have resulted in Canadian inflation being lower than it actually was, and lower than US inflation as well, since the downward pressure from adverse commodity prices and a less dynamic economic performance on Canada’s real exchange rate would not have found outlet in a declining nominal exchange rate, but instead would have put persistent additional downward pressure on Canadian prices and costs. Output would almost certainly have been more variable, although this period illustrates the Bank of Canada’s tendency to allow exchange-rate fluctuations to compromise its domestic objectives, somewhat mitigating the contrast. (For several reasons, the Bank of Canada has often responded to movements in the exchange rate with opposite-direction moves in short-term interest rates, resulting in changes in monetary conditions that were unhelpful to inflation control.)

If—and as Figure 2 suggests, it is a huge if— Canada had maintained the peg despite these forces, we would have traded stability in output and inflation for lower inflation overall. On balance, in macroeconomic terms, floating looks to have been a better option, although with sufficient determination Canadians would have survived a fixed rate.

Other things, of course, also might have been different if the peg had been maintained. Part of the case for stabilizing the Canada-US exchange rate presumes that more downward pressure on domestic prices and costs would have been a good thing. Producers of tradable goods might have relied less on a declining dollar to offset for poor management or underinvestment. And governments’ fiscal and microeconomic policies might have been more friendly to growth.

But these counterfactual propositions are highly speculative. Relative price changes are the same regardless of the level of the currency in which they are measured. Shifts in Canada’s terms of trade will prompt shifts of domestic resources regardless of the exchange-rate regime. Moreover, if Canadian producers have pricing power, as is likely in some commodity markets, a lower nominal exchange rate will exacerbate a relative decline in commodity prices. And if productivity increases when a fixed exchange rate intensifies a price-cost squeeze, why would other policy-induced squeezes—higher taxes on business inputs, for example—not be equally effective?

The presumption that fiscal or micro policies would have been better is equally speculative. Robert Mundell calls budget deficits “anathema” in fixed exchange rate systems, but they do still happen. North American provinces, states and cities have irrevocably fixed exchange rates against other domestic jurisdictions, yet they not only run deficits, they sometimes run up debts so large that they default. If disinflationary pressure had been stronger in the 1980s and 1990s, Canadian governments might have responded with laxer fiscal policy. As for structural policies, greater contractionary pressure might have spawned larger regional and industrial subsidies. A weaker economy and no exchange-rate cushion might even have stopped Canada entering a freetrade agreement with the United States. Argentina, one of the most aggressive recent dollarizers, in late March violated its trade obligations in the Mercosur by raising import tariffs on consumer goods—a cautionary tale of dubious micro policies arising from the macroeconomic constraints of a fixed exchange rate.

There is, in short, no good macroeconomic reason for asserting that adopting the US dollar would boost Canadian living standards over the long term. The biggest gain on offer for less developed countries—gaining credibility for a central bank that has very little—does not apply to Canada. The Bank of Canada is currently charged with maintaining low and stable inflation, and has done so with considerable success. As long as the US continues to do the same, the macro gains and losses from monetary union appear finely balanced. No benefits large enough to warrant giving up democratic control over an outcome as significant as inflation are obviously on offer.

On the microeconomic side, benefits and costs are also finely balanced. Advocates of currency union typically argue that eliminating conversion costs and the risk of sudden, speculatively-driven currency moves will ease crossborder business, creating new opportunities for gains from trade. While that is true, it is not a decisive consideration.

Canada-US trade has expanded vigorously for decades, despite the obstacle of a floating exchange rate. There is no threshold past which foreign-exchange hedging becomes intolerably expensive—indeed as foreign-exchange and related financial markets get broader and deeper, these costs are falling. And there is no basis for Mundell’s statement: “If Canada had the same currency as the United States and a genuine free trade area, Canadians would have as high or higher a standard of living as the average American.” Again, provinces, states and cities share currencies and free trade areas, but the experience of Canada’s have-not provinces and US inner cities demonstrates the limits of the benefit that fixity confers.

At this point, one might ask why provinces do not have flexible exchange rates as well. The reason is that there is more to a currency than the exchange rate regime. Central banks play a key role in national financial systems, and an examination of this role reveals that giving up their currency would impose microeconomic losses on Canadians. If the Bank of Canada disappeared, what would take its place at the core of the Canadian payments system, providing small amounts of liquidity day-to-day to support interbank clearing, and larger amounts when accidents threaten a systemic breakdown?

Although it is possible to imagine the Fed stepping into such a role, this is another area where actual US debate gives little reason to expect that it would. In a presentation to the US Senate in 1999, ex-treasury secretary Summers stated clearly that the United States is not about to start providing central-banking services to other countries’ banks. So Canadians would face a choice.

On the one hand, Canada could adopt the US dollar without any formal arrangements in place. Canadian banks would clear and settle through private channels that use no central bank money, and access US systems through US intermediaries. This could take place without any domestic lender-of-last resort safety net through the clearing system or deposit insurance. (In support of doing away with such safety nets, one could argue that the moral hazard they create may lead to more bank failures. In practice, however, the public-good aspects of a well functioning financial system have led many regulators to take a deliberately ambiguous stance: bailouts if necessary, but not necessarily bailouts.)

Or Canada could set up an independent backstopping war-chest.

Either way, doing without backstopping services from the Fed—which would be the only agency able to create Canadian legal tender at will—presents risk/cost tradeoffs. At best, the cost of domestic banking services would increase, putting Canadian banks at a disadvantage relative to US counterparts who have central bank support. At worst, Canada would be exposed to a serious financial collapse.

On the other, hand, Canada could approach the United States for a special deal. We could ask the United States to give Canadian banks access to the Fed’s discount window and other sources of backstopping support. In return, Canada could grant US agencies the supervisory and regulatory powers they need to provide such support—in short, the machinery that allows them to lend with confidence that they will be repaid.

But this option is problematic. Why would the United States want such a role? In normal times, it would be an administrative burden, and in the event of a crisis that threatened the viability of a major Canadian bank, it would be a serious political headache. For that matter, why would Canadians want it? US financial regulation has been inferior to Canada’s in many respects in the past. Though it has become less restrictive since late 1999, it is, if nothing else, confusing enough that even non-nationalist Canadians might sensibly incline toward the devil they know. (There is, for example, considerably confusion about which activities of US banks fall under the regulatory authority of the Fed, and which fall under the authority of the Comptroller of the Currency.)

Another important consideration is that banking is in a state of flux. Technological changes are blurring lines of business and revolutionizing payments systems. Institutions are going to merge, and institutions are going to fail. In managing these changes, most Canadians would probably prefer their deliberatively ambiguous regulators to be accountable to politicians that Canadians can vote for.

Close inspection of grass completed, it is time to straighten up and look again at the fields and the fence between them. Canadian dissatisfaction with current arrangements presents a risk. Canadians may decide to jettison the inflationtarget/floating-currency regime without sufficient advance information about what the coherent alternative—the adoption of the US dollar—really requires. If the brown, prickly patches on the US side of the fence only become widely known once Canadians are on their way over, disillusionment may lead them to try to perch on the fence.

One possible outcome would be an attempt by the Bank of Canada to stabilize the exchange rate—limiting its movement over specified periods, or keeping it in a trading range. This outcome would combine the worst attributes of floating and fixing. It would eliminate neither conversion costs nor—especially since arbitrary trading limits lack credibility—the risk of large currency moves. Yet it would compromise the Bank’s commitment to inflation control. As noted already, part of Canadians’ disappointment over their economic performance during the 1990s resulted from the Bank’s having paid too much attention to the exchange rate, not too little. It would be an absurd irony if their reaction led to more of the same.

Another possible outcome would be an attempt to peg the exchange rate—a course that Mundell and Friedman agree sets the stage for inevitable crisis when the peg gives way. Insisting on a distinction between “fixed” and “pegged” exchange rates is an unhelpful fudge. The differing degrees of political commitment involved are evident only in retrospect: At any point in time, an observer will describe an arrangement that has endured until then as “fixed” and one that has not as “pegged.” If pegging is, as Milton Friedman comments, a bad model for the world, it is hardly a better one for a single country— especially one with a more coherent and welltested alternative.

Even a currency board can be an uncomfortable perch atop the fence. Unlike a full union, a currency board still confronts households, businesses and financial institutions with some conversion costs. The usual description of a currency board assumes that domestic currency issue is backed, one-for-one, by the board’s holdings of the foreign currency. In fact, currency boards may resort to less-than-full backing, which makes them more like autonomous central banks, and necessarily provokes skepticism about the durability of the fixed exchange rate they support. Fears of dissolution would never disappear—especially if Canada chose a currency board over dollarization because it wanted to keep some capacity for independent support of its financial system, support that might require a deviation from one-for-one backing—and capital flows speculating on such an outcome would therefore be a constant threat.

If sitting on the fence is uncomfortable and ultimately unsustainable—and it is both—Canadians need to learn more about the grass on both sides of the monetary fence before they decide to cross over. Canadian enthusiasm for the beauty of US verdure may diminish if they realize that giving up the Canadian dollar means adopting the US dollar, that adopting the US dollar means depending on a central bank accountable only to US voters, and that depending on a central bank accountable to US voters means not only losing control over Canadian inflation, but making an unpalatable regulatory choice: do without key central banking services, or give the United States supervisory and regulatory powers over Canadian financial institutions.

Becoming disillusioned part way over and pegging the exchange rate would simply set Canadians up for crisis when the peg gave way. In the meantime, they risk neglecting the task of making the grass on their side of the fence greener. If Canadian businesses are underperforming, designing new currency arrangements should not take energy away from measures that might improve their management. If Canadian policymaking is muddled, a focus on the dollar is unlikely to bring about the tax and regulatory changes that would straighten it out.

Inflation targets and a floating exchange rate represent one of Canada’s most coherent and successful approaches to economic policy. If Canadians dedicated themselves to raising other areas of economic policymaking to the same standard their monetary policy has achieved, they could look forward to a deep, green, luxurious lawn on their own side of the fence.

Photo: Shutterstock