With its Universal Income Security Program (UISP) the Macdonald Royal Commission has proposed a fundamental reform of the income security system. It has also raised the question of a guaranteed income for Canada, but the UISP proposal does not fully address the interaction between government transfer payments to households and the personal income tax system.

The principal objectives of this article are twofold. The first is a general assessment of Macdonald’s UISP proposal. The second is to examine a modification of UISP, a fully integrated reform option that combines a guaranteed income and simplified tax (GI/ST). The GI/ST option is compared with the UISP proposal in order to see whether the Macdonald Commission’s intentions with respect to the UISP proposal – for example, simplification and consolidation of programs, improved incentives, no net costs, more help o the working poor – can be achieved also addressing the problem of harmonizing the personal income tax and transfer systems.

The article illustrates the use of prototype microsimulation model for the analysis of income security policies in Canada. This model is part of a project at Statistics Canada on behalf of a number of clients to develop a more comprehensive database and modelling capacity to support analysis of social programs. For my analysis, the 1985 projection of the SIMTAB database of Department of Health and Welfare has been used. We are very grateful to Health and Welfare for making this database available. Needless to say, neither that department nor Statistics Canada, nor of course the government of Canada generally, bears any responsibilities whatsoever for the way the model and the database are used in this analysis, or for the personal conclusions that are reached.

My analysis concludes that the proposed UISP may have some paradoxical impacts. For example, incentives could be worsened in the middle income range even though one of the Commission’s objectives was to improve incentives. This result’s omission of the relationship of he UISP to the income tax system. The analysis of the GI/ST option presented here shows, further, that the Commission’s objectives might be better met by a more fully integrated proposal.

Canada’s income security system consists of a complex mix federal and provincial direct spending programs in combination with the personal income tax system. The federal and provincial income tax systems have two facets: a basic tax structure with a progressive schedule of tax rates, plus a series of significant tax expenditure programs such as the child tax credit, marital exemption, and RRSPs.

For purposes of this analysis, we shall focus only on the major elements of the income security system. These are family allowances (FA), the guaranteed income supplement (GIS), the federal portion of welfare financed under the Canada Assistance Plan (CAP), unemployment insurance (UI) premiums and benefits, and the personal income tax including the child tax credit, exemption for dependent children and the marital exemption.

In 1985, the Family Allowance (FA) program paid $375 in respect of each child under 18, while the refundable child tax credit paid $367 per child to about two-thirds of all families receiving FA. The elderly received income-tested benefits via the Guaranteed Income Supplement (GIS) of up to $5,170 for couples and $3,970 for single individuals. The unemployed are entitled to Unemployment Insurance (UI) benefits which are (roughly speaking) 60 percent of average weekly earnings just prior to becoming unemployed. The maximum duration of these benefits ranges from 6 to 12 months, depending in a complex way on previous work history and the local unemployment rate. UI benefits are about two-thirds financial by a payroll tax.

Welfare or social assistance benefits are delivered by the provinces but are financed roughly 50 percent by the federal government under the Canada Assistance Plan (CAP), Welfare benefits vary widely by province, family type (single mother, couple), employability, and something age. Benefits re not only income tested, they are also conditioned by means (e.g. assets) and needs (e.g. shelter costs).

A number of other transfer programs will not be considered in this analysis. The Canada and Quebec Pension Plans and the Old Age Security pension have not been included in the discussion mainly because they are viewed as intergenerational transfers or reallocations of income over life cycle. They are taken as given in the quantitative analysis following.

The personal income tax and the other transfer programs are viewed, in contrast, as essentially point-in-time redistributional vehicles, and thus as candidates for change when we are considering a restructuring of the income security system so as to provide a guaranteed income. Programs such as workers compensation, provincial top-ups to the federal GIS, subsidized rent or shelter allowances, and financial aid due to data limitations. A more detailed analysis should consider these programs, but their omission in this analysis is not critical.

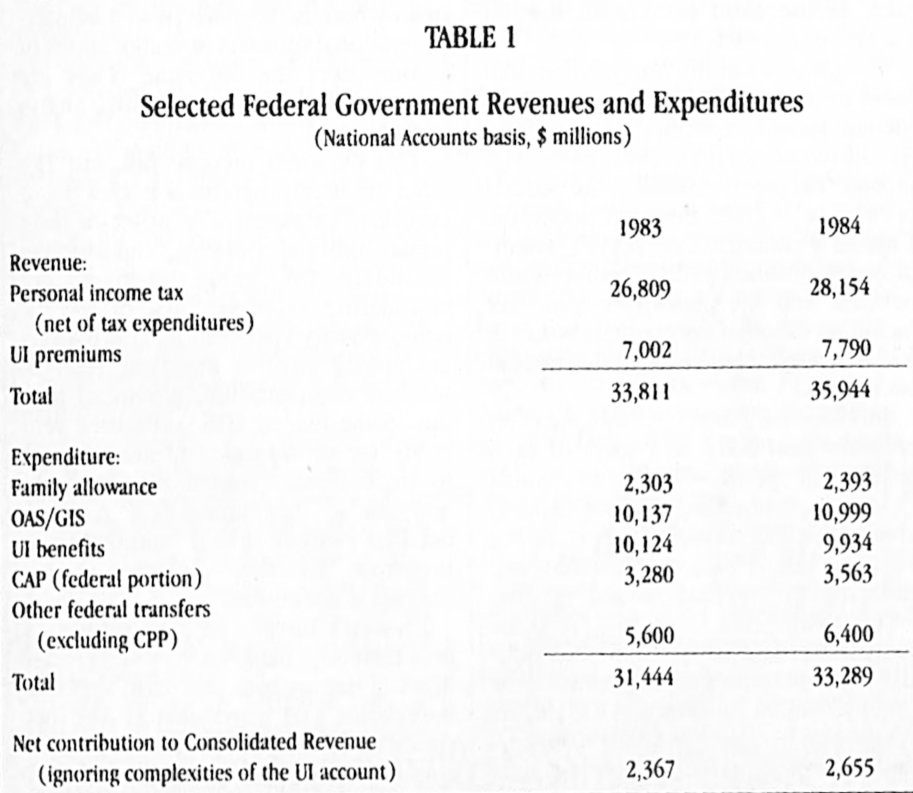

Canada’s income security system as here define is mainly a very large set of flows of money back and forth between households and governments. The net contribution of personal taxes to financing the activities of government, once transfers have been deducted, is perhaps surprisingly small. This is shown in Table 1. As will be discussed later, the large volume of gross money flows relative to net revenues is in part a reflection of the delivery mechanisms for social transfer benefits. Nevertheless, there would appear to be some scope for consolidation and rationalization.

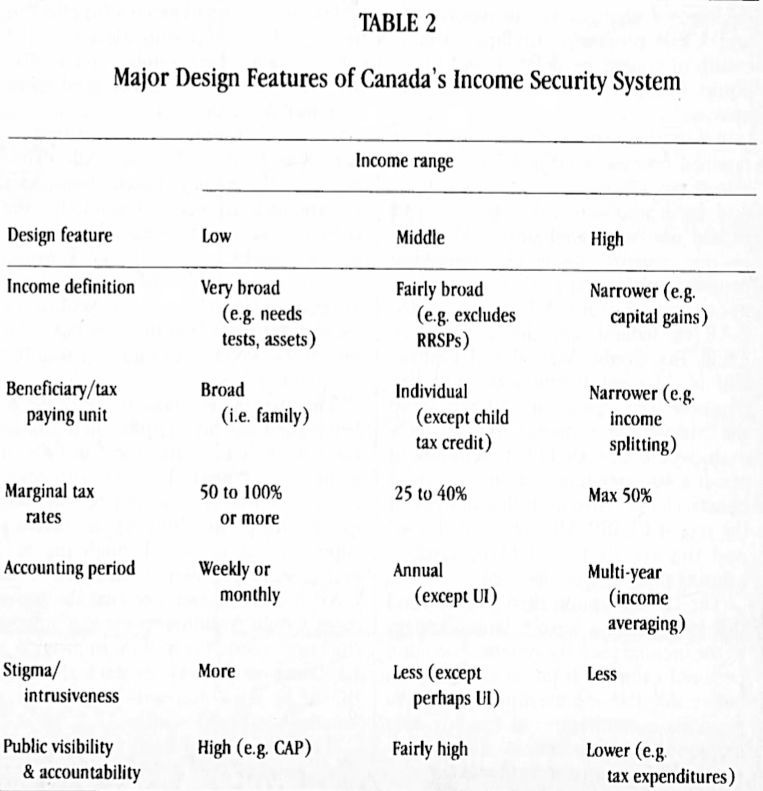

With these large and sometimes complex federal as well as provincial programs, in concert with the many and varied provisions of the personal income tax, the combined impact of the income security system is certainly very complex. The resulting lack of understandability has evolved over many years and is itself a problem. Furthermore, along a spectrum from low to middle, to high incomes, the income security system exhibits a systematic variation with respect to several major design features. These variations, which are illustrated in Table 2, rise basic questions of fairness. The income security system presents one face to the well-to-do, and another to the poor.

For those in the lowest income ranges, CAP and GIS plus provincial top-ups to GIS are the dominant parts of the income security system. Social assistance delivered under CAP, in particular, employs a very broad definition of income. The family is the beneficiary unit for both CAP and GIS; and marginal effective tax rates on income range from 50 percent to 100 percent or more. Receiving social assistance benefits generally requires an application process that many consider demeaning. GIS is fairly straightforward, though many people refer to GIS as a form of welfare.

The expenditures of both programs are highly visible. With provincial top-ups to GIS and the joint funding of social assistance under CAP, both senior levels of government are closely involved on a regular basis.

These particular design features, compared to those further up in the income spectrum, tend to restrict the total amount of benefits available. The weekly or monthly rather than annual accounting period under CAP, however, is relatively more beneficial.

As one moves up to the middle ranges of the income spectrum, UI and the “middle class” facets of the income tax system dominate. The individual rather than the family is now the tax or beneficiary until, no longer aggregated with his or her spouse and children if they also have income; marginal effective tax rates drop to the 25 to 40 percent range; and the income contempt is not so broad. Some tax expenditures like RRSP, charity, child care expense, and tuition fee deductions begin to be enjoyed.

Moving to the upper end of the income spectrum, the income concept becomes narrower still as increasingly income takes the preferentially treated forms of dividends, capital gains, and retentions in incorporated “small” businesses, and greater deductions from tax shelters and carrying charges are claimed.

The maximum marginal tax rate is nominally about 50 percent, but it is effectively reduced by the preferential tax treatment just noted. The tax unit may be effectively smaller than the individual to the extent more sophisticated tax planning is able to achieve income splitting. As well, forward averaging and loss carryforward provisions in effect provide a multi-year accounting period. There is no stigma associated with completing an annual income tax return. Public accounting is limited, particularly because there is no regular process of parliamentary scrutiny for tax expenditures.

Thus, with the partial exception of the accounting period, the general picture that emerges for Canada’s income security programs including the personal income tax, when viewed as a system, is one that is more stringent for the poor than for the rich.

The “give away” part of the income security system when it provides benefits to the poor does so only with many strings attached (the non-elderly poor more so than the elderly poor), while the “take away” part of the system taxes the well-to-do with fewer strings attached, at lower marginal rates, and with more generous definitions of income, family, and the accounting period. When the “give away” part of the system is providing benefits to the middle class (e.g. child tax credit) or well-to-do (e.g. tax shelters), there is less stigma and less formal parliamentary accountability.

The Macdonald report examines Canada’s income security system in considerable depth, and concludes that major reforms are needed. IN essence, the proposals involve the abolition of several programs, scaling back UI benefits, introducing a new Transitional Adjustment Assistance Program (TAAP), and a new guaranteed income called the Universal Income Security Program (UISP).

More specifically, the direct spending and tax expenditure programs, that would be abolished are GIS, FA, federal participation in the Canada Assistance Plan (CAP), the social housing programs of CMHC, the marital exemption, the exemption for dependent children, and the child tax credit. UI benefits would be scaled back by about 40 percent in aggregate as a result of a variety of changes to the benefit structure.

The resulting monies would be redirected to finance the TAAP and UISP proposals. The report’s preferred version of the UISP (Alternative B) would provide basic income guarantees (in 1984 dollars) of $2,750 per adult and $750 per child under 18. There would be an extra $2,000 for single parents (treating the first child like a second adult, analogous to the equivalent to married exemption in the personal income tax) and an extra $1,075 for the single elderly resulting in guarantees of $3,825 and $5,500 for the single elderly and elderly couples respectively.

The report’s Alternative A would in addition abolish the basic personal exemption and provide higher basic income guarantees than Alternative B. The guarantees would then be reduced or taxed back at the rate of 20 percent on total family income. In conjunction with the federal initiative to institute the UISP, the Macdonald Commission expects the provinces to redirect their monies now spent on CAP to top-ups for the most needy.

The income guarantee levels and the relatively low tax back rate of the report’s UISP are similar to the supplementation tier discussed in the previous government’s Social Security Review (SSR) in the mid 1970s. In the SSR discussions, the supplementation tier was to have addressed the major gap in the current income security system, the working poor. This supplementation tier was intended to provide benefits that, when combined with modest levels of earnings, could lift families out of poverty. It would have employed a low enough tax-back rate that there would still be incentives for such families to stay in the labour force.

The provincial top-ups envisaged to the UISP are in turn similar to the support tier discussed during the SSR. This tier was intended to assure adequate incomes for the most needy, particularly those unable or not expected to work.

The main difference between the UISP and the SSR proposals of a decade ago is in the cost-sharing. Unlike the earlier SSR proposals, the UISP embodies a clear form of federal-provincial disentanglement. The federal government via the UISP would be 100 percent responsible for the supplementation tier, principally benefitting the working poor, but also providing a base of support for the non-working poor. The provinces would then be 100 percent responsible for the support tier which would top-up the UISP to assure adequate incomes to the non-working poor.

Our simulations suggest that the report’s UISP Alternative B would not be fiscally neutral; it might involve net costs of $3 to 5 billion, though the report’s objective fiscal neutrality could be achieved by increasing the tax-back rate from 20 to 25 percent.

In this analysis, the UISP will be compared to an option that confronts explicitly the question of integrating personal income taxes and transfers. To put the two on a comparable footing, a fiscally neutral variant of Macdonald’s UI and UISP package of proposals will be used. Specifically, TAAP will be ignored because the details were not precisely specified nor was it intended to be a broadly based program; the abolition of Social Housing will be ignored, because most of the monies in this program are locked in pursuant to long term contractual arrangements; a 22.9 percent tax-back rate will be assumed; the report’s preferred Alternative B will be the focus of the analysis; and the $2,750 and other basic income guarantees will be assumed to be in 1985 dollars. (The report’s guarantee levels are expressed in 1984 dollars. Retaining the same nominal dollar amounts in 1985 dollars means they are roughly 4 percent lower in real terms. To prevent the single elderly from being worse off under the UISP, however, their basic guarantee is increased to $3,970, the 1985 GIS level, from $3,825. As a result, a 22.9 percent rather than 25 percent tax back rate is required to leave the UISP fiscally neutral.)

A major concern about the UISP proposal is that it does not fully deal with the interaction and overlap between the direct transfer and personal income tax parts of Canada’s income security system. The reason for articulating a specific Guaranteed Income/Simplified Tax (GI/ST) option, as a substantially modified version of Macdonald’s UISP, is to show concretely how such harmonization could be achieved.

The GI/ST starts from the simple idea of combining a guaranteed income with a flat tax. The essence of the flat tax idea is a constant marginal tax rate. While some recent discussions of flat tax options, particularly in the USA, have characterized them as regressive, flat rate tax structures can be progressive. For example, if a flat tax rate is tied in with an initial income guarantee (or equivalently a refundable tax credit) the result is a progressive structure: average rates of tax (which are initially negative) increase with income, even though marginal tax rates are constant.

A guaranteed income already exists in Canada, though in a piecemeal form. For the elderly it is OAS plus GIS; for families with children under age 18 it is FA plus the child tax credit; and for everyone else there is CAP. It is precisely these pieces (except OAS) that are recombined to produce Macdonald’s UISP proposal, and the same recombination serves as the basis of the guaranteed income portion of the GI/ST.

Still, the amount of progressivity in such a flat rate tax may be less than that of the present income tax. To address this possibility, as well as to serve other objectives, the GI/ST option in fact incorporates a two-step tax rate structure.

To focus discussion, the GI/ST option is based on an almost identical package of changes as the report’s UI and UISP proposals. Endless variants could, of course, be defined, and many could merit further elaboration and analysis.

As in the report, OAS would be retained because it plays a fundamental role as an income replacement vehicle and intergenerational transfer, and should not be viewed simply as point-in-time redistribution. The following programs or tax expenditures thereon), Child Tax Credit, Marital and Equivalent to Married Exemptions, and Exemptions for Dependent Children. As in the Macdonald proposal, the UI program would be scaled back, resulting in about a 40 percent reduction in total UI benefit claims. Also as in the analysis of the report’s UISP Alternative B, TAAP and the abolition of CMHC’s social housing programs are ignored.

The GI/ST option then goes beyond this by assuming further large changes to the income security system. The basic personal exemption (as in UISP Alternative A), the age exemption, and the pension, investment, and employment income deductions would all be abolished. Furthermore, all income tax rate brackets would be abolished to be replaced by a single basic federal rate of tax at 30 percent. This tax rate would apply to the current concept of net income for tax purposes, with some modifications. Deductions for RRSP contributions, charitable donations, and child care expenses, for example, could still be allowed. With no personal exemptions, tax would start on the first dollar of net income (excluding OAS benefits), just as it does now for GIS.

Employer and employee UI premiums would be abolished along with all the complex accounting currently related to the financing of UI. UI benefits would simply be fully financed out of federal consolidated revenues. With the GI/ST’s basic flat rate of tax, the abolition of UI premiums would be roughly equivalent to broadening the base of the UI payroll tax to include non-employment income, and removing the earnings ceiling.

In place of the abolished programs and tax provisions, there would be a set of basic federal income guarantees almost identical to those proposed for UISP Alternative B: $750 per year for adults age 18 to 64, $2,600 for adults age 65 and over, $2,000 per year additional for single parents (in effect to treat the first child equivalently to the spouse in a married couple), and $1,400 per year additional for those aged 65 or over and living alone.

These guarantees are structured so that, apart from the Spouse’s Allowance program, the elderly and children under 18 are just as well off as under the current system. The guarantees would not be taxable. As well, OAS would become non-taxable. (Making the guarantees and OAS taxable would be redundant, given that the new basic flat rate of tax would start on the first dollar of income.)

The guarantees make no pretense of being adequate, in comparison to Statistics Canada’s Low Income Cut-Offs or some other poverty line. As with Macdonald’s UISP, they would be intended more along the lines of an income supplementation tier. Though the federal government would withdraw from CAP, it must be assumed that the provinces would continue to use the monies they now spend on welfare to provide a basic income support tier stacked on top of the federal guarantees, just as is assumed by Macdonald.

The federal-provincial tax collection agreements would be retained, but provincial tax rates would be altered. At present, provincial income taxes (except Quebec) are levied at about 50 percent of federal “basic tax.” The federal tax base under the GI/ST’s flat tax without exemptions (and before the federal guarantees) would be much broader. Thus, provincial income tax rates of about 20 ⅔ percent on new federal basic tax (including the surtax described below) would leave provincial revenues essentially unchanged.

Finally, a 15 percent surtax would be imposed on total income over $36,000. This provision would serve a dual purpose. First, it would retain a measure of progressivity for the top 30 percent of all families while ensuring that the top marginal tax rate, federal plus provincial, did not exceed 55 percent. Second, the surtax would be levied on total rather than net income for tax purposes; i.e. before various exclusions and deductions. Thus, the surtax would also function as a 15 percent minimum tax on income with essentially a $36,000 basic exemption. Like the Bradley-Gephardt proposal in the USA, this surtax cum minimum tax would have the effect of implicitly converting tax deductions into tax credits at the basic rate of tax.

As a further aspect, the surtax base could include the aggregated investment incomes of the nuclear family. This would eliminate most of the advantages to income splitting (the main exception being grandchildren). Income splitting would in any case be far less advantageous due to the basic flat rate tax. If income is always taxed at least at the 30 percent basic tax rate, there would not be nearly as much incentive to try to arrange a family’s affairs to have income taxed in the wife’s or children’s hands rather than the father’s, for example.

I shall now offer a comparative analysis of the UISP and GI/ST schemes.

Net fiscal impact. The two options have both had their parameters set so that they would be fiscally neutral, at both federal and provincial levels. In the case of the UISP, by ignoring the report’s proposals regarding the TAAP and social housing programs, increasing the tax-back rate to 22.9 percent, and adopting the report’s assumption that provincial revenue windfalls (from abolition of some personal exemptions) would be returned to the federal government via the return of personal income tax points, there would be no net change in the federal deficit or total provincial revenues. The GI/ST has been similarly designed.

It follows that households on average would be no better or worse off in terms of their disposable incomes.

Behavioural response. It should be emphasized that all the estimates of costs in the report, as well as quantitative results presented here, assume no changes in the individual or family behaviour. This is an important area of uncertainty about the likely impact of implementing either the UISP and UI proposals or some form of GI/ST. In terms of the effect on total costs, there are likely to be tendencies in both directions. For example, the UISP’s relatively high marginal rates, when stacked on top of the personal income tax rates for the middle income ranges (see below), could depress work incentives and hence income tax revenues, while the removal of the “poverty trap” for the working poor could have the opposite impact.

The point to be noted is that the failure to consider behavioural responses means that total costs, both here and in the report’s analysis, could be either under or over stated.

Delivery and gross flows. The variant of the UISP proposal considered here would involve a net volume of income guarantees paid out, after applying the tax-back, of about $12.3 billion. Similarly, the GI/ST proposal would involve total payments of $12.8 billion to those who are net recipients of benefits.

Both these figures, however, represent the lower limit of the total volume of cheques that would have to be written by the government each year. One reason, as noted in the report, is that it may be more administratively efficient to pay the full amounts of the basic annual income guarantees (presumably in monthly instalments) during the year. The report also notes that paying out the full amounts during the year would make the benefits more accessible, result in higher take-up rates, and greater responsiveness to income fluctuations. Any tax-back would then be applied after year end, at income tax filing time.

This gross flow approach is the one followed by the current universal programs OAS and FA. A total of about $11.5 billion has been paid out in 1985 under these two programs, and then about $1 billion will be recovered via income taxes this spring.

A net flow approach, on the other hand, is followed for GIS and the child tax credit, examples of selective programs. Under these programs, the amounts actually paid out have already been reduced to the extent any tax-back is applicable.

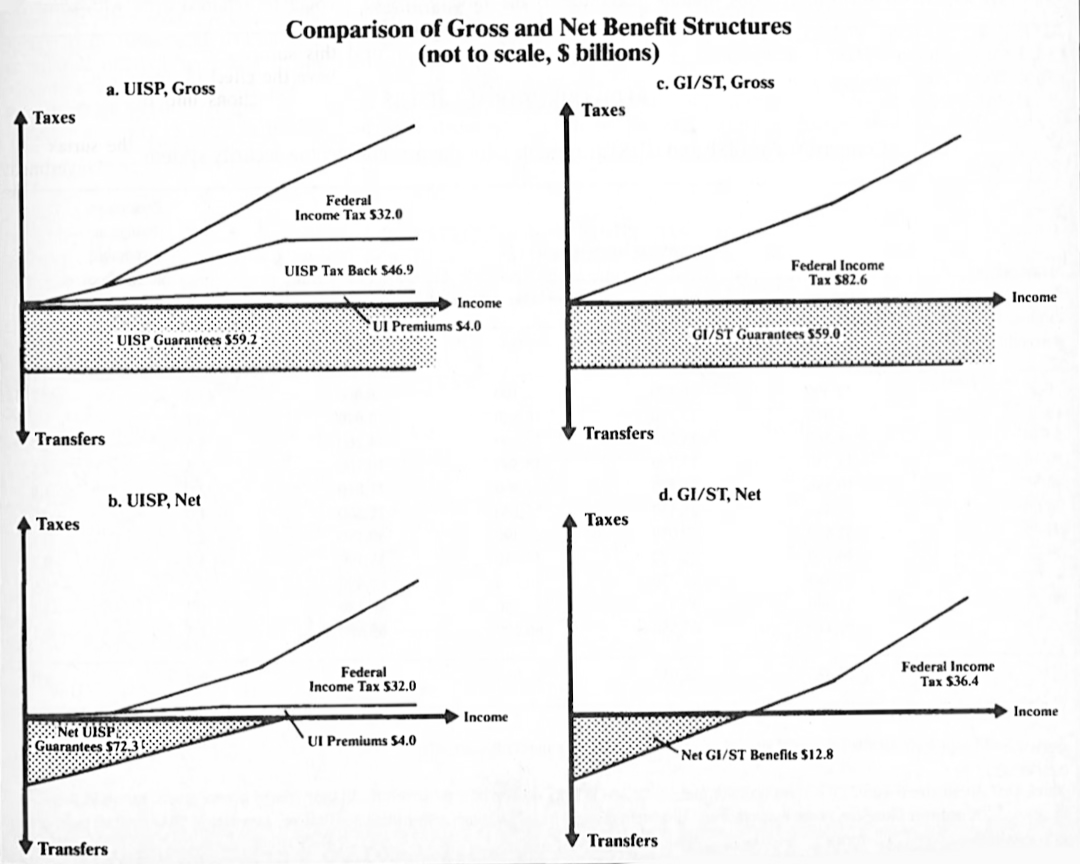

The form of delivery for the income security system can have a major impact on the total dollar flows back and forth between households and governments. This is illustrated in the diagram. Parts a and c illustrate the UISP and GI/ST benefit structures respectively if the gross flow approach were followed, i.e. guarantees were paid out in full during the year and then taxed back after year end. Parts b and d, in contrast, show the net benefit structures—total benefits net of income taxes and tax-backs.

The report suggests that the gross flow or universal approach to delivery is preferable. As shown in diagram a, this implies total payouts of about $59.2 billion. Though the report suggests that it would be “workable,” there does not appear to be any simple mechanism by which these gross dollar flows could be reduced, short of establishing a comprehensive geographic network of UISP offices to accept applications and apply the UISP income test before disbursing benefits. Because the UISP is not integrated with the personal income tax system and because it is based on total family income for the tax-back, it would be difficult to incorporate into the present system of withholding income tax at source.

The GI/ST, as shown in diagram c, involves a similar amount of potential gross flows, $59.0 billion. It does, however, lent itself more readily to the use of the existing withholding system for income tax. This results from the simple integrated basic flat rate of tax applying over the entire income spectrum (leaving aside the surtax) and the use of the individual as the basic tax paying/beneficiary unit. Income fluctuations do not matter nearly so much when all income is subject to a single rate of tax, so year end reconciliations at tax time might not be that large. A range of mechanism could be developed, but it should be possible to cut total payouts to less that half the maximum potential gross flows.

A key issue here is whether a woman staying at home to care for children should receive her own and the children’s guarantees in full, or whether these guarantees could be nettled against her husband’s income tax liabilities. Assuming the current policy with respect to FA and the child tax credit were retained under the GI/ST, paying the corresponding child guarantees as well as one adult guarantee to the mother would impose a lower limit on the amount of payouts on the order of $25 billion. On the other hand, it should be noted that the benefits of the marital and child exemptions currently accrue to the father, typically on a weekly or bi-weekly basis via the source withholding system. As a result, there is precedent for some further netting of the dollar flows, reducing total payouts considerably below the $25 billion figure.

Responsiveness. To the extent that gross amounts are paid out during the year, the system does not need to be responsive to income fluctuations during the year. Total annual income could be determined after year end at income tax time. Under the UISP, as already noted, it would require additional administration to deliver only net benefits. The administrative load would be larger to the extent the system had to be able to respond to fluctuations in income during the year.

With the GI/ST, on the other hand, a considerable degree of responsiveness could be retained even with some degree of netting income guarantees against income tax liabilities, since the source withholding system is responsive to changes in income during a year.

It is not as difficult to assure that the delivery system is responsive to changes in demographic situations, for example, the birth of a child or reaching age 65. The current administration for OAS, GIS, and FA already handles these kinds of events, so it should not be difficult for the UISP or GI/ST to incorporate the same kind of responsiveness.

Accounting and the apparent size of the government. The netting of benefits against taxes owing can have a large impact on total dollar flows and also a corresponding effect on the apparent “size” of the federal government. This depends on whether the income guarantees are treated in the government’s accounts as spending programs like FA, or like refundable tax credits such as the child tax credit was introduced, about $800 million was taken from FA to fund the new tax credit. Households overall were just as well off; but according to the government’s books, the total size of government fell by $800 million.

Similar arbitrary changes in the apparent size of the federal government could be engendered by either UISP or GI/ST. However, as shown in the diagrams, the changes could be much larger—of the order of $15 to $60 billion depending on whether gross or net amounts are shown and whether the basic income guarantees are labelled refundable tax credits or direct spending programs.

The key point is that a better method of accounting for taxes, tax credits, and transfers to households in the Public Accounts is probably required. In particular, it would be most informative if all gross dollar amounts were regularly presented, if transfers were clearly distinguished from other government financial transactions, and if tax credits and other similar benefits delivered through the tax system were treated in the same way as transfers for accounting purposes.

Universality and selectivity. TO the extent that the terms universality and selectivity have a significant meaning, it is with respect to delivery. More precisely, and as stated cogently in the Macdonald report, the terms are relevant to the question of when income testing or taxing back happens—before or after delivery of benefits. For the UISP, the mode of delivery could have a major impact on the way the public would view the program. In the case of the GI/ST, however, the universality-selectivity questions would be of considerably lesser consequence because income testing could be substantially integrated with the source withholding system. A more relevant issue, as noted above, is whether mothers or fathers should receive income guarantees in respect of children, and husbands in respect of non-working wives.

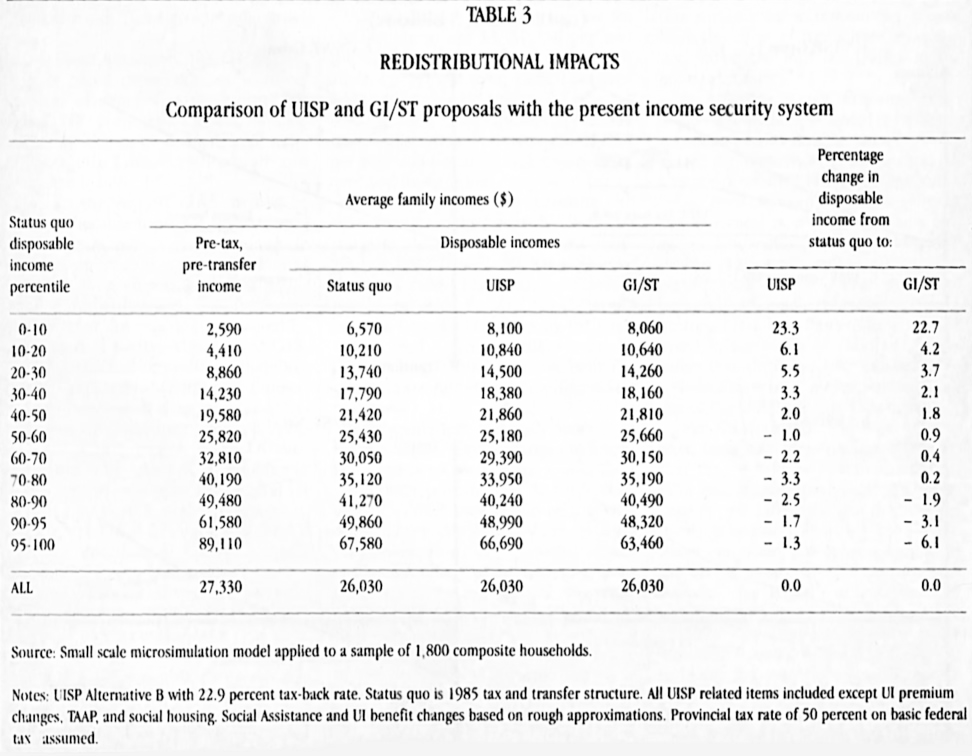

Distributional impact by income class. Table 3 compares the impact of the fiscally neutral UISP and the GI/ST with the current income security system.

About half of all family units in Canada are net beneficiaries from the income security system. This can be seen by examining the first three columns of the table. Up to and including the 40th and 50th percentile group (the first five rows), status quo disposable income (post-tax, post-transfer) is greater than pre-tax, pre-transfer income (mainly market income).

The second key point is that, even though the UISP proposal and the GI/ST option articulated here would constitute very wide-ranging reforms, the average changes in disposable income they would engender are still relatively small compared to the income redistribution that already occurs via the existing income security system. This is evident from the fact that amounts in the three disposable income columns are more similar to each other than to the previous column showing average pre-tax, pre-transfer incomes by percentile income groups.

Overall average disposable incomes (the bottom row in the table) are identical precisely because the options have been designed to be fiscally neutral.

The two far right columns highlight the redistributive effects of the UISP and GI/ST relative to the current income security system. Both options redistribute from higher to lower incomes. The GI/ST’s redistribution is just about the same as the UI/SP’s for the bottom 10 percent, but is less redistributive for the next 30 percent of families. The GI/ST imposes the bulk of its net declines in disposable income on the top 20 percent while the net declines income under the UISP would be relatively greatest in the upper-middle income ranges (the 60th to 90th percentiles). Thus, the GI/ST is more targeted to the upper and lower ends of the income spectrum in its redistributive impacts.

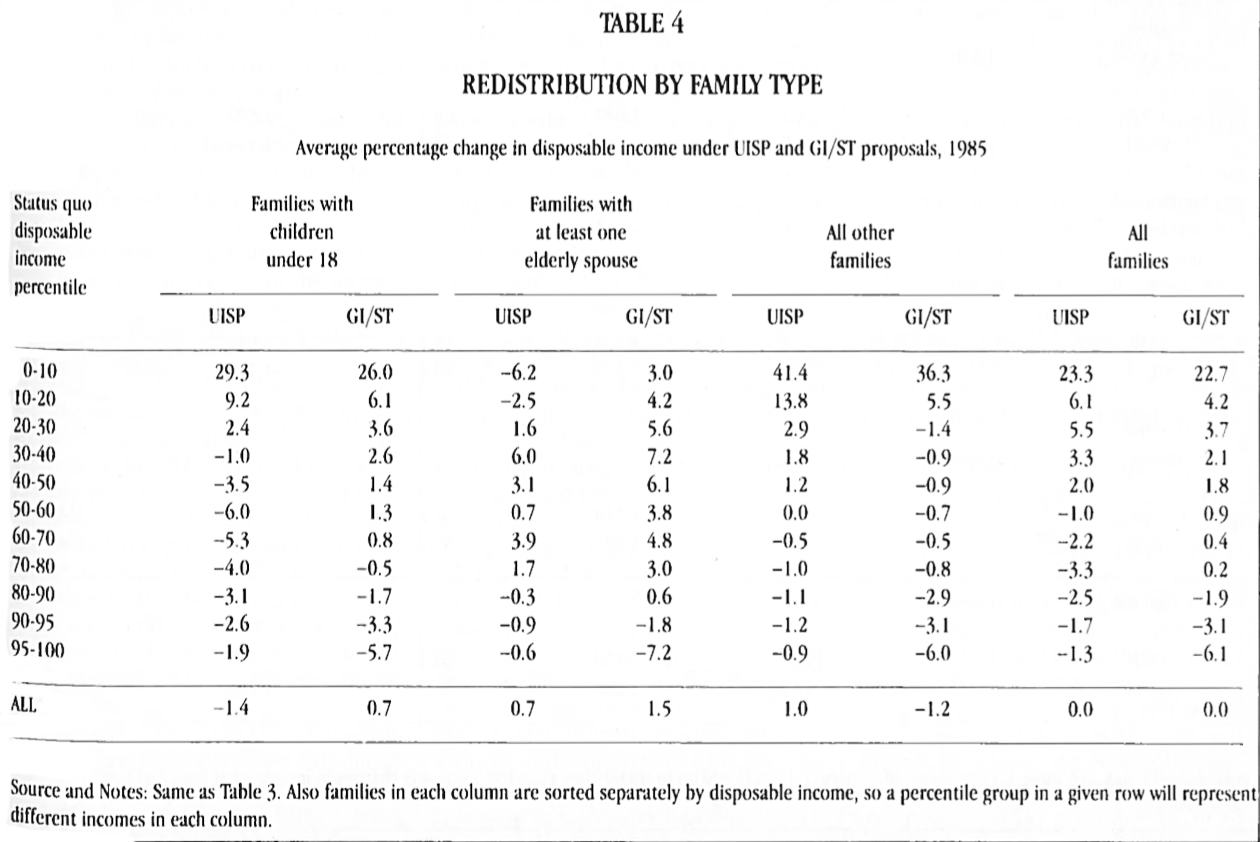

Distributional impact within and among family groups. Table 4 provides greater detail on the comparative redistributive impact of the UISP and GI/ST options within broad demographic groups. The same picture as in Table 3—the GI/ST is relatively more targeted than the UISP in its redistribution from the top end of the income spectrum to the bottom—applies generally within the demographic groups.

The most unusual pattern is among the elderly. Under the UISP, because Macdonald (probably inadvertently) assumed OAS would be subject to tax-back, the poorest 10 percent of the elderly actually could expect an average ne decline in disposable income of 6.2 percent, and the next poorest 10 percent an average net decline of 2.5 percent. The largest gains for the elderly occur in the 30th to 50th percentiles because the effective 50 percent tax rate in GIS has been replaced with a 22.9 percent tax-back rate.

Under the GI/ST, there are no net declines in disposable incomes among the poorest of the elderly because OAS has been made non-taxable. Still, the effective lowering of the GIS tax-back rate from 50 to 36 percent (federal plus provincial) under the GI/ST means that the largest relative gains amongst the elderly occur in the 20th to 50th percentiles.

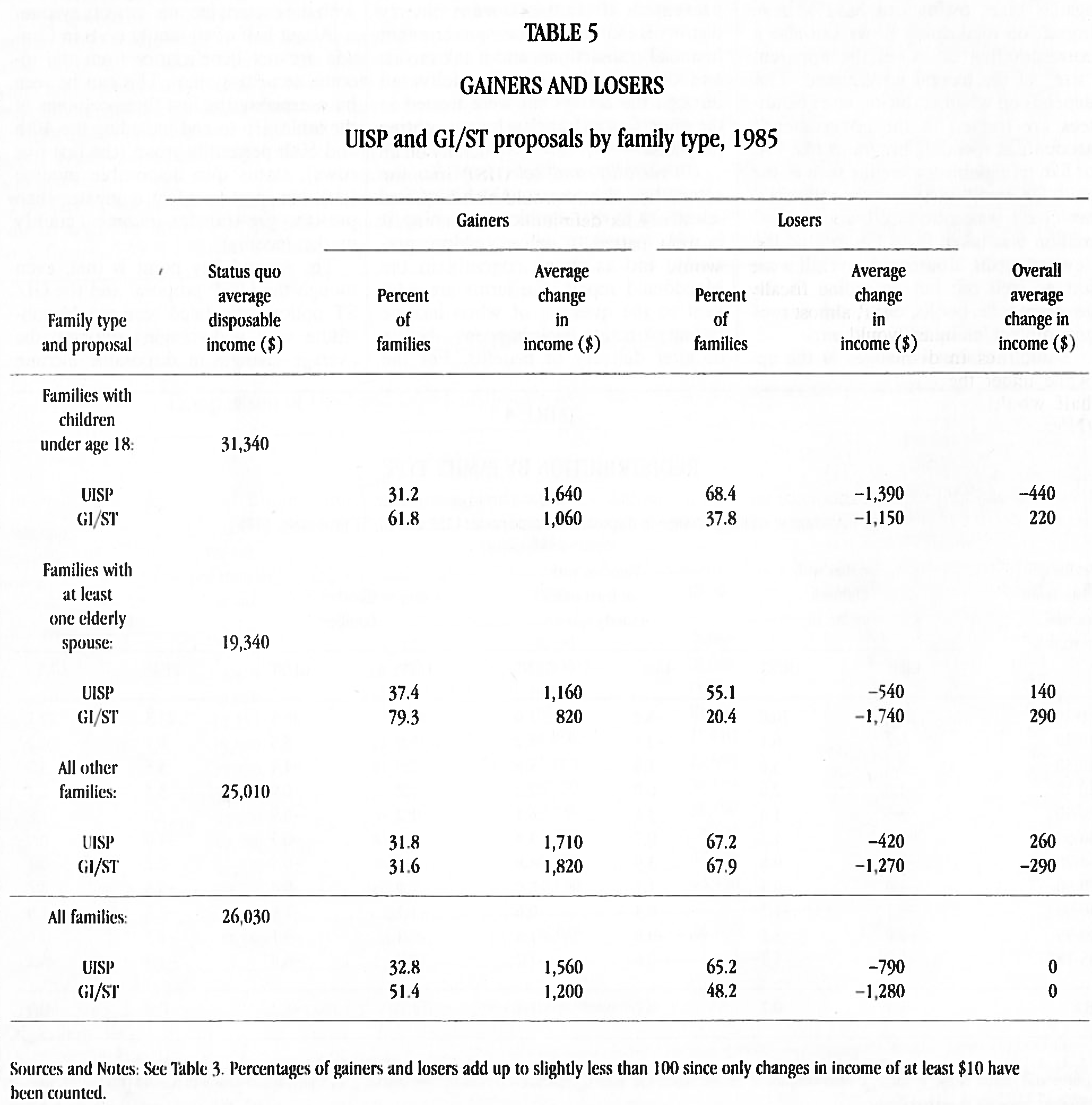

Other differences between the UISP and GI/ST options are in the redistribution between non-elderly families with and without children and in the proportion of gainers and losers. These are shown in Table 5. Under the fiscally neutral variant of the UISP, almost two-thirds of all families would experience net declines in disposable incomes, while under the GI/ST, just less than half would experience net declines. (Note that these figures are consistent with Table 4, which shows only average changes within an income group.) Families with children would experience an average decline in disposable income of $440 under the UISP compared to an average increase of $220 under the GiIST. This difference is mainly attributable to the different tax structures in the middle and upper ranges of the income spectrum, because the basic income guarantees under the two options are virtually identical.

Simplicity. The UISP simplifies the income security system by collapsing six programs and tax expenditures into one new program. However, the overall system is still not easy to understand because of the overlap between the UISP and the personal income tax, as show in diagrams a and b: The GI/ST is simpler still, both because of the explicit integration of income taxes and transfers and because of the single flat rate tax structure facing the majority of households.

This simplicity of the GI/ST suggests that it would involve lower combined administrative costs for Revenue Canada, Health and Welfare, Employment and Immigration, and Supply and Services. With the single flat rate of tax, tax avoidance and tax evasion could be reduced, in particular by extending the scope of the source withholding system. It would probably be much easier under the GI/ST to institute a much shortened (half page?) version of the personal income tax return for the majority of families.

Fairness. Both the UISP and GI/ST would improve fairness if this is taken to mean that more redistribution from those with higher to those with lower incomes would occur.

The UISP would not, however, resolve the issues of fairness indicated in Table 2. Indeed, it would exacerbate the tax unit issue by imposing a family income tax-back for the UISP over a broader range of incomes and families while these same households would be filing income tax returns generally on an individual basis. The UISP income-testing apparently would also be based on a broader definition of income. The current pattern of marginal tax rates would be altered, but new concerns would be created by the stacking of the UISP tax-back rate on personal income taxes. This is indicated in Table 6, discussed below.

The GI/ST, on the other hand, would address many of the concerns indicated in Table 2. The income security system would be moved to largely an individual basis; a common definition of income would be used throughout the income spectrum, except at the top, where the minimum tax would apply; marginal tax rates would be much more uniform; and the accounting period would be of lesser consequence given a basic flat rate of tax.

Some improvement in fairness might also be ascribed to simplification. A simpler system is more understandable and hence more likely to be perceived as fair by the general public. It would also reduce the need for sophisticated tax planning advice, a service which is expensive and hence mostly used by the well-to-do.

Federal-provincial relations. Both the UISP and GI/ST proposals embody a measure of federal-provincial disentanglement, particularly in the case of the Canada Assistance Plan (CAP). As noted at the outset, the UISP and the GI/ST income guarantees are similar to the income supplementation tier put forward in the mid-1970s as part of the Social Security Review. The federal government is thus taking full responsibility for the working poor, and providing a nationally uniform (but not necessarily adequate) base for all Canadians.

The provinces would then have full responsibility for providing top-up income support to the poorest. The provinces could tailor this income support to region-specific factors in a way perhaps inappropriate to federal programming. They would no longer factor into their program design, for better or worse, the 50 cent dollars currently available as part of the cost-sharing under CAP.

Other federal-provincial institutions like the tax collection agreements and the Quebec income tax abatement could be adapted to either the UISP or GI/ST option. Some provinces have also expressed interest in having greater flexibility in defining their income taxes under the tax collection agreements. While this is feasible under both the UISP and GI/ST, the simplicity and attendant efficiencies of the flat tax rate in the GI/ST would be lost if provinces were able to impose complicated rate structures.

Regional impact. The UISP and GI/ST as proposed both involve a substantial reduction in UI benefits. This would have a disproportionately adverse impact in Atlantic Canada. This impact might, however, be considerably offset by the proposed income guarantees. Unfortunately, the Macdonald Commission did not address this question and the prototype microsimulation model being used in this analysis is not yet sufficiently advanced to allow any quantitative analysis by geographic region.

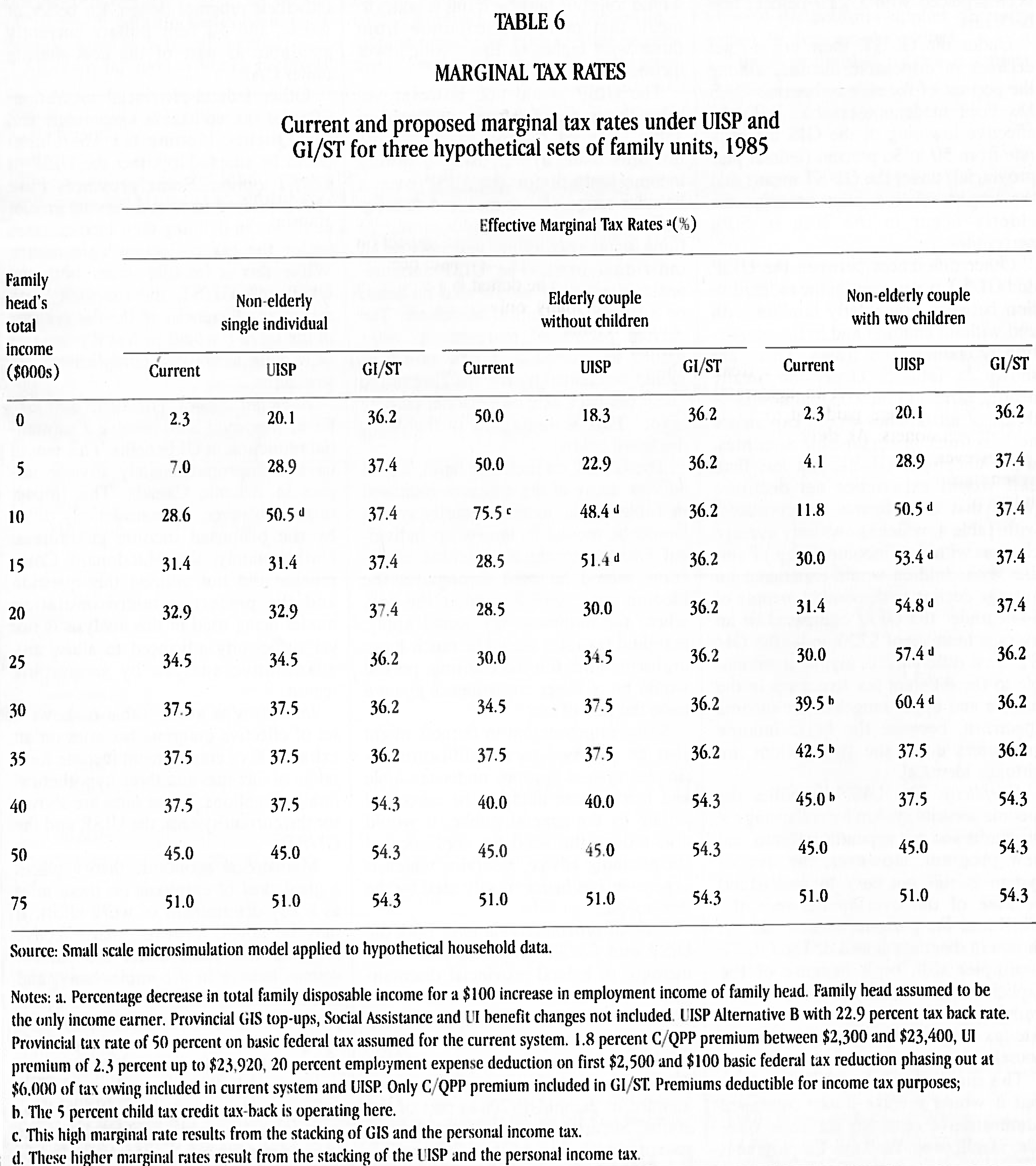

Incentives to work. Table 6 shows a set of effective marginal tax rates on an extra $100 of employment income for a range of incomes and three hypothetical family situations. These rates are shown for the current system, the UISP, and the GI/ST.

Mainstream economic theory places a great deal of emphasis on these rates as a key determinant of work effort. It may be noted, however, that effective marginal tax rates with much accuracy (say, within a five or ten percentage point range). This, in turn, makes it difficult to believe that people’s behaviour depends on these marginal rates in any precise way, contrary to most contemporary economic theory.

Still, the most striking observation is the way the UISP stacks upon the personal income tax system. This stacking results in effective marginal tax rates as high as 50 to 60 percent in the $10,000 to $30,000 income range (or higher for larger families). Such high rates may be expected to have some disincentive effects. ON the other hand, rates in the 20 to 30 percent range apply to incomes below $10,000. Compared to Social Assistance, which typically involves tax-back rates up to 100 percent, this would be a substantial improvement for the working poor.

The main observation regarding the GI/ST is the comparative regularity of the rate structure. The only complicating factor is C/QPP premiums which become a flat amount above $23,400. The rates are not much different from the current situation from $20,000 to $35,000 before the sur-tax cum minimum tax begins, and above $50,000. Below about $20,000, however, and in the $40,000 to $50,000 range, the GI/ST involves higher effective marginal tax rates. These higher marginal rates are coupled, though, with lower average tax rates up to $15,000 for a single non-elderly individual and up to $50,000 for a couple with two children under the GI/ST ($15,000 and $20,000 respectively under the UISP) because of the introduction of the basic income guarantees.

The general implication of Table 6 is that for most non-elderly households, the UISP and the GI/ST either represent no change or an increase in effective marginal tax rates. The main exception would be for those currently on Social Assistance who are able to work and able to find work. Also, this analysis takes no account of the incentive effects of Macdonald’s proposed changes to UI, which are assumed as part of both the UISP and GI/ST options.

Incentives to save for retirement. The UISP option has a favourable impact in the lower income ranges because the proposal is effectively equivalent to reducing the GIS tax-back rate from 50 percent to 23 percent. Thus, savings via RRSPs or company pension plans, while continuing to benefit from the same preferential up-front tax treatment, would be subject to lighter tax when benefits were paid out to lower income pensioners. As shown in Table 6, however, the UISP tax-back rates when stacked upon personal income tax rates around the $15,000 income level would be higher than at present. Thus, in the middle income ranges for the elderly, the UISP would provide less incentive for retirement saving.

In contrast, the GI/ST would have a positive impact on retirement savings for lower and middle income families in two distinct ways. First, the GI/ST would replace the 50 percent GIS tax-back rate and current income tax rate with the generally lower 36 percent basic flat tax rate (federal plus provincial) after retirement. Second, the GI/ST would also provide an enhanced up-front tax incentive in the lower and middle income ranges during working years. The reason is that RRSP and pension plan contributions would effectively be eligible for a 36 percent tax credit, since they would be deductible in computing taxable income under the GI/ST’s basic rate of tax.

Structural deficit. Both the UISP and GI/ST options being analyzed have been designed to have no net impact on the budget deficit if they had been in place in 1985. The deficit is a source of concern to many only in so far as it would remain once the economy returned to full employment—that is, to the extent that it is structural rather than cyclical. Because the UISP and GI/ST options tend to be more redistributive that the current system, they also tend to be more elastic with respect to real income growth.

This means that as the economy moved toward full employment, the federal deficit with the UISP or GI/ST in place would fall somewhat more quickly than under the current income security system.

Preliminary simulations suggest that a one percent increase in real incomes (distributed proportionately across all incomes) would result in a 23 percent faster rate of increase in the net contribution of the income security system under the UISP to the federal consolidated revenue fund than under the current tax/transfer structure; under a GI/ST, there would be a 48 percent faster rate. If full employment were to mean 5 to 10 percent higher real average incomes, this means that under the UISP the deficit would be $750 million to $1.5 billion lower, and under the GI/ST it would be from $1.5 to $3 billion lower, than it would be under the same conditions with the present tax and transfer system.

It is hoped that this initial and partial analysis will help further the substantive public discussion that the Macdonald Commission’s UISP proposal merits, as well as consideration of guaranteed income/simplified tax alternatives.