It seems there’s little fiscal room left. But with a slightly more modest medium-term debt target, we’re richer than we think.

As several commentators have noted, Budget 2015 has balanced the books, and largely exhausted the fiscal room going forward.

The books were balanced in large part by the cumulative effects of spending restraint applied over the past five years. Ultimately, this was aided by dipping into EI funds and selling assets –moves that make the numbers look slightly better in the near-term. (And there are other possible quibbles. For instance, despite a projected surplus in this fiscal year, federal debt still increases due to “off budget” losses.)

The government has also brought in some new tax measures whose foregone revenue costs grow over time (increasing Tax-Free Savings Account contribution room, cutting small business tax rates). On the spending side, they’ve committed to some increases that start a few years down the road (on infrastructure and defence spending). Then to ensure there’s little wiggle room for future governments, a proposed law will require a balanced budget each year –barring recessions, wars or natural disasters.

In the eyes of many pundits, the government has successfully constructed a fiscal architecture that will be very hard to deconstruct and eventually increase the size of government. Opposition parties, it seems, are now stuck in the unenviable position of having to reverse politically popular tax cuts (the cheques are in the mail!), or raise other politically unpopular taxes if they want to fund new initiatives, or they risk running deficits which might expose them to easy attacks.

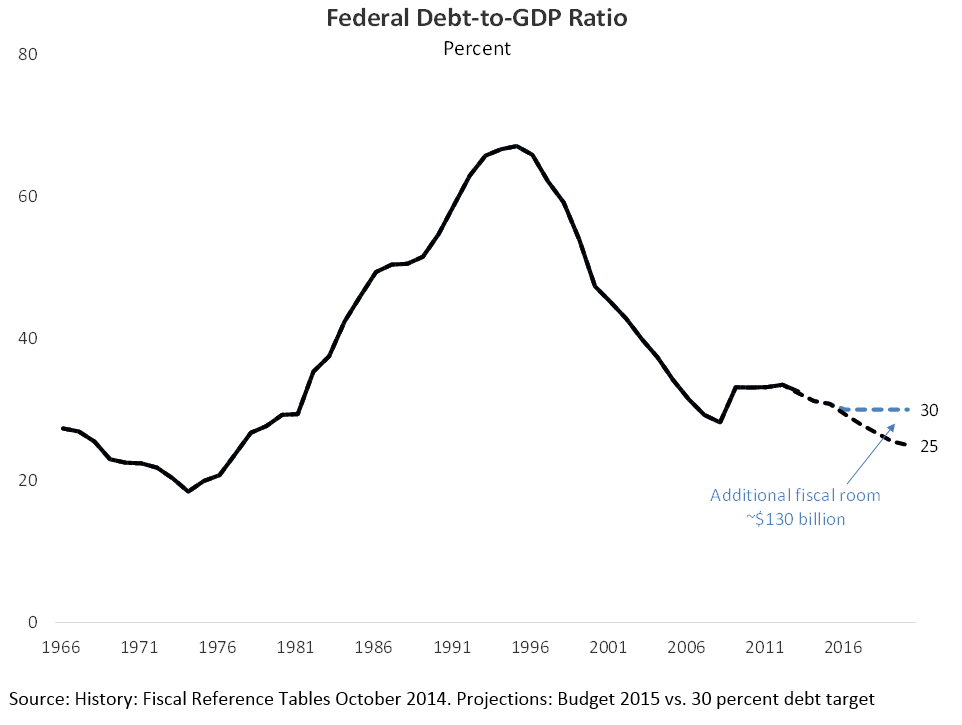

This is the government’s election strategy and the political discourse we should expect in the months ahead. But let’s not forget that the government’s joint fiscal policy targets of: (a) balancing the budget; and (b) reducing the federal debt-to-GDP ratio to 25 percent by 2021 are merely choices…even if (a) becomes the law of the land.

There are, however, other fiscally-responsible targets. An illustrative –and in my view, perfectly sensible –alternative is to keep the federal debt ratio at its current level of around 30 percent, rather than lowering it further to 25 percent over the medium term.

It doesn’t seem like much, but this one policy decision would provide a massive amount of fiscal policy room over the medium-term simply by pausing the current fiscal policy consolidation track. Crude back-of-the-envelope estimates based on the government’s projection (without altering other variables such as GDP), suggest that satisfying the 30 percent federal debt target could provide something in the neighbourhood of $125 billion in total fiscal room. This would start next year, and is summed over five fiscal years from 2016 to 2020.

This represents about $25 billion annually for new initiatives. To put this in context, it’s about 5 times larger than the government’s significant tax announcements in October 2014, which included expanded child care benefits and other actions that cost around $5 billion annually all together. So it’s a big number that could dramatically change the tone of Canadian fiscal policy discussions.

At the same time, despite being sizable, it’s unlikely to seriously threaten the government’s long-run fiscal sustainability. Estimates by Finance Canada and PBO, both suggest that there’s long-term room to spare at the federal level.

Moreover, by running looser fiscal policy over the medium term, Canada would have more macro-policy flexibility as monetary policy could be tighter (than it otherwise is to compensate for tighter fiscal policy), which could be used to modestly help address perceived imbalances in Canada’s housing sector and elevated household debt levels.

Now there’s a catch: instead of balancing the budget each year, as required by the new proposed law, this would allow for federal deficits of roughly 1 percent of GDP. (In dollar terms, the deficit, which is the numerator and also the change in debt, would grow in line with the denominator, nominal GDP, which is expected to grow by about 4 percent annually).

Admittedly, this requires a major attitude shift in public policy discourse away from the “deficits are always bad, surpluses are always good” view that has generally served Canada well since the mid-1990s. And so this approach would ideally include constraints on policy-makers to ensure that deficits don’t grow.

In effect we would need to get over a “stuck in the 1990s” mentality. At that time, Canada’s debt levels were high relative to other countries, debt charges were taking up an increasing share of revenues, and economic growth eventually strengthened (likely due in part to the fiscal improvements).

But times have changed and so too has the appropriate fiscal policy stance. Now public debt problems in Canada are largely under control and considerably better than other countries, long-term interest rates are at record lows, and trend economic growth is disappointing and slowing.

What about the provinces, you might say, they’ll bankrupt the country. This is certainly the area of longer-term fiscal worries for Canada. However, one encouraging sign is that –at least over the past few years for one of the main drivers of the provinces’ long-term fiscal problems –the growth in health care spending has slowed. Of course, this could easily change, but it’s another small reason to avoid excessive fiscal restraint.

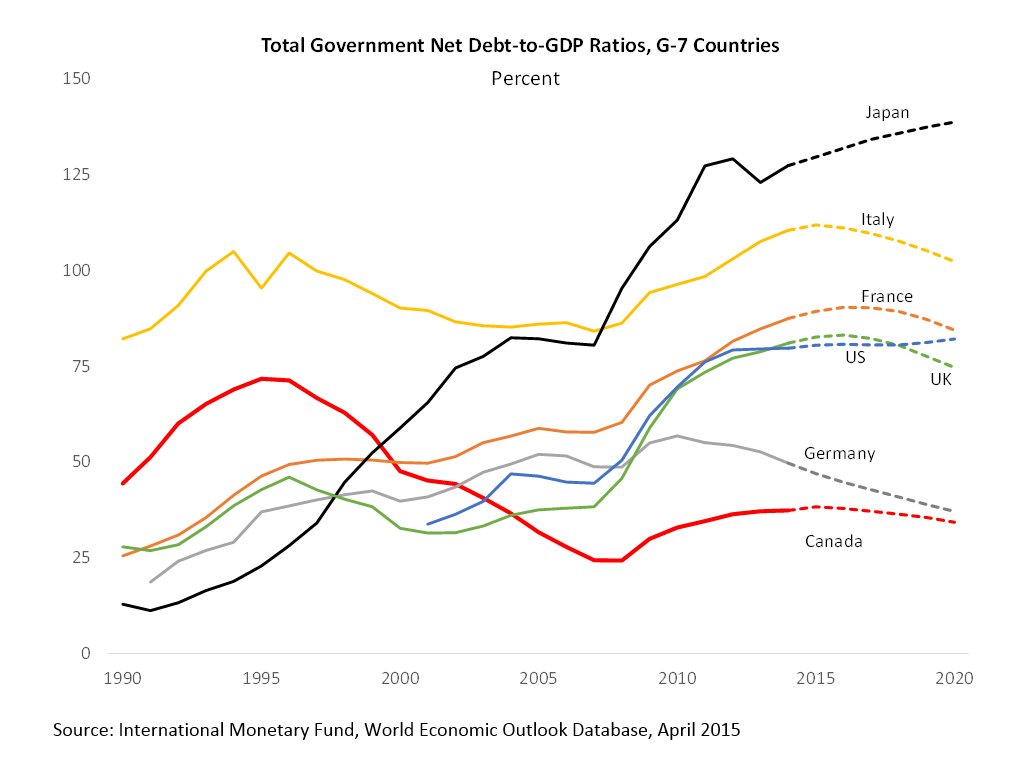

If you’re still worried, then compare the outlook for Canada’s general government net debt-to-GDP ratio to the rest of the G7 countries. We’re in better shape than the rest of the pack, including Germany, and expected to maintain this position up to 2020 in IMF forecasts. Moreover, as Annex 2 of the budget explains, Canada is doing far better than the rest of the G-7 after adjusting for different accounting treatments of public sector pensions.

It may seem like a radical proposal to some, but perhaps we should consider easing up on the fiscal consolidation at the federal level. It may be sufficient to simply lock-in the gains we’ve made and keep federal debt steady as a share of our economy over the medium term.

It may seem like a radical proposal to some, but perhaps we should consider easing up on the fiscal consolidation at the federal level. It may be sufficient to simply lock-in the gains we’ve made and keep federal debt steady as a share of our economy over the medium term.

If we did that, we’d find plenty of new fiscal room –far more than we used in recent months –we’d have some more macro policy flexibility and we might have more fruitful and open fiscal policy discussions in Canada.

Photo by Alex Guibord / CC BY-ND 2.0