Here are 10 developments that mattered for the Canadian economy and economic policy in 2014.

1. Falling oil prices

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

As the year ended, lower global oil prices became a dominant preoccupation. The associated fall in Canada’s export-to-import prices (weaker terms of trade) have already significantly lowered growth forecasts for nominal GDP and real gross domestic income in Canada for the fourth quarter of 2014 and into 2015.

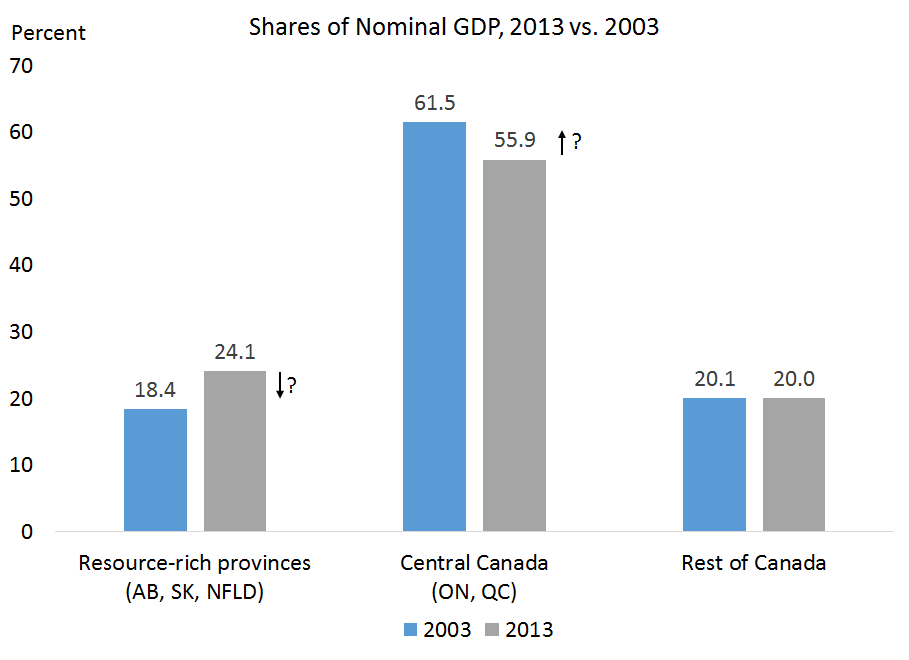

If lower oil prices persist, investment in the resource sector will slow further. There will also be disparate regional impacts: the share of Canada’s economy generated by the resource-rich provinces (Alberta, Saskatchewan and Newfoundland and Labrador) will reverse some of the past decade’s gains, the question is how much, as the central provinces of Ontario and Quebec enjoy some upside from the combination of a stronger US economy and a weaker exchange rate.

Softer oil prices will also hit government revenues in the resource-producing provinces. This will require tough choices and better fiscal management (might Alberta finally adopt a sales tax in 2015?); and may make it harder for the federal government to balance its books this year.

2. Is housing over-priced in Canada?

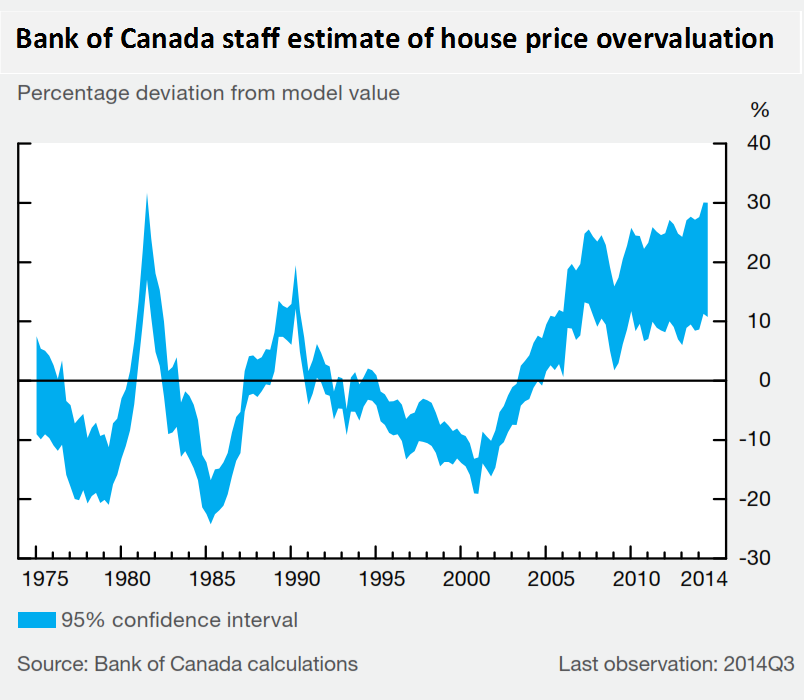

For a few years now, elevated housing prices in Canada have been a recurrent topic of debate. The OECD, the IMF, The Economist magazine, private sector banks and recently, the Bank of Canada have all suggested that housing prices in Canada are above fundamentals, with estimates ranging from 10-30% too pricey — most notably in Vancouver and Toronto, with potential over-building of condos. If prices fall in 2015, will it be a soft-landing, or might we endure a more disruptive US-style housing crash in some markets?

3. Household debt (and net worth) continues to creeps up

3. Household debt (and net worth) continues to creeps up

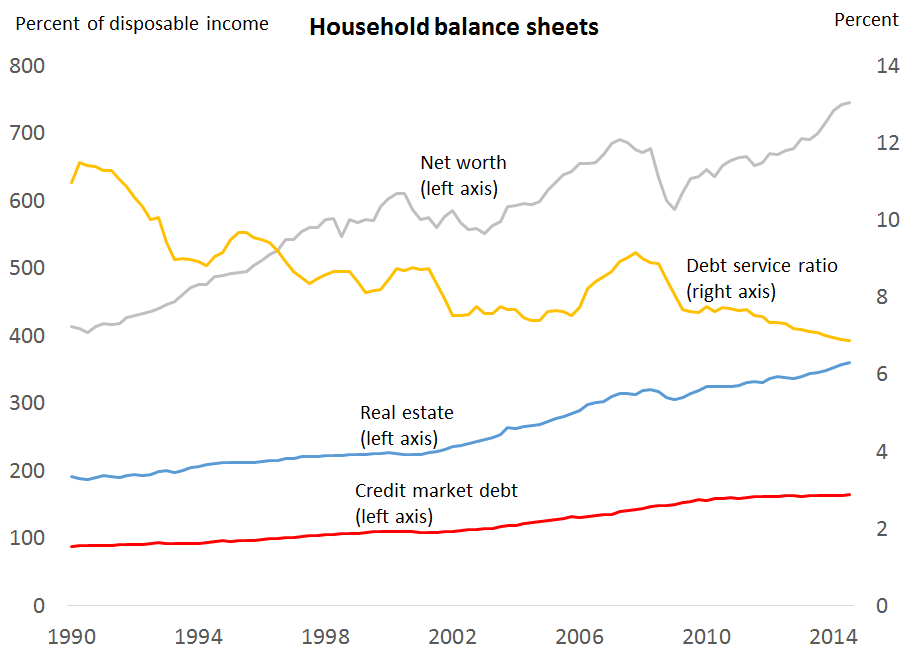

Many analysts continued to fret in 2014 about rising household debt in Canada — much of which is mortgage-related. Considering both sides of the household balance sheet, shows that net worth has also increased. Some commentators, therefore, are not too concerned — at least while the real estate assets are appreciating for which households are borrowing and debt-servicing costs remain near historic lows.

Of course a key vulnerability for Canada’s economy is that over-valued home prices may fall. And as interest rates eventually rise, the most-highly-leveraged households could be hit hard, restraining their consumption and imposing negative spillovers on the aggregate economy.

(Incidentally, House of Debt, one of 2014’s best economics books, is recommended reading that illustrates what went wrong in the US experience with highly-leveraged households in the Great Recession — which notably featured more sub-prime mortgages than in Canada).

4. US economy picks up steam

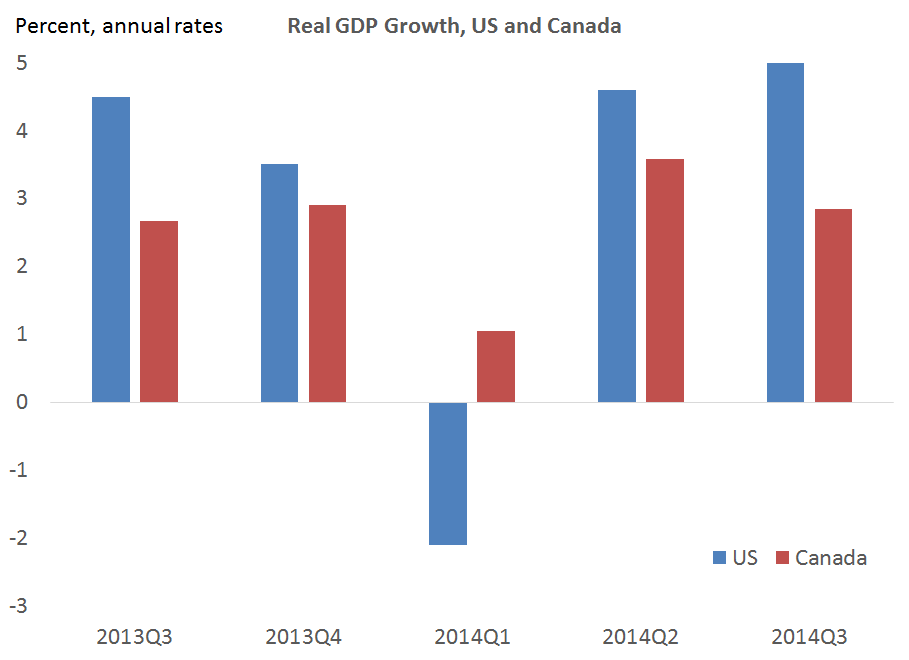

One welcome event in 2014 for Canada was the strengthening of economic activity south of the border. US real GDP growth has generally been strong, job growth was steady and the unemployment rate has tumbled (though the latter isn’t all good news as it partly relates to lower labour force participation).

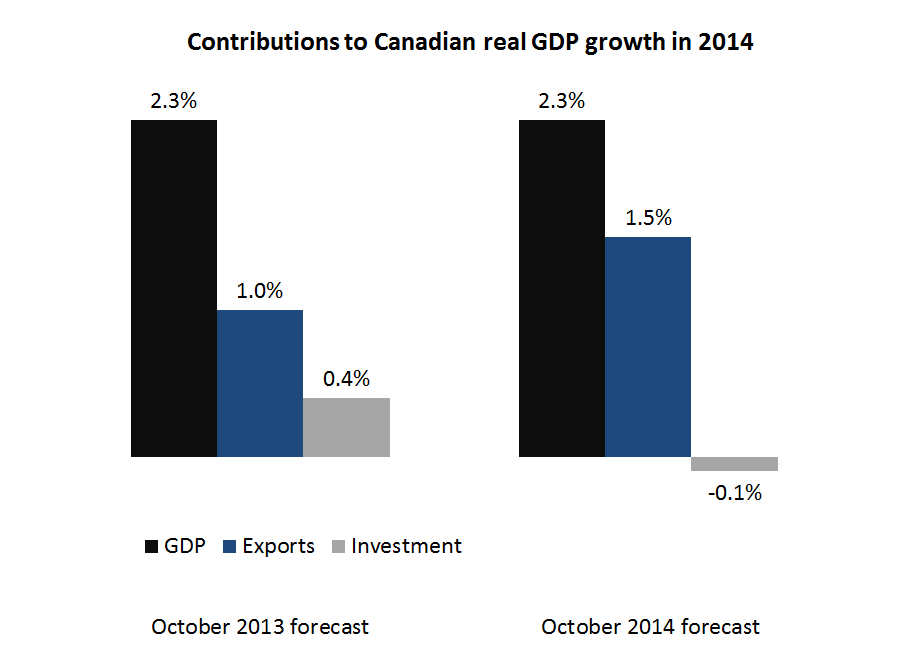

5. The shifting composition of Canadian GDP growth

Related to this stronger US growth, the long-anticipated ‘rotation’ of Canadian GDP growth away from household spending and towards export and investment-led growth inched along in 2014. More specifically, Canada’s exports finally showed signs of life, while business investment remained lackluster. In 2014, exports are poised to exceed the Bank of Canada’s prior expectations for the first time since 2010, but business investment will once again disappoint the Bank for the third consecutive year.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

The good news is that businesses in Canada are generally well-placed to invest in 2015, but before they do so, they need to use up remaining spare capacity and become more confident that demand will persist. 6. Inequality and the surprising distribution of income gains in Canada in recent years

6. Inequality and the surprising distribution of income gains in Canada in recent years

We’ve passed “peak-Piketty”, but inequality continued to be a key issue in 2014 and its importance show no signs of abating. One thing that surprised me was that more recent Canadian data suggest that after decades of highly unequal growth — with the top 1% enjoying a disproportionate share of income gains in Canada between 1982 and 2006 — this longer-term trend seems to have slowly reversed in recent years (though Canadian society remains less equal).

This chart on the distribution of income gains is from the government’s fall fiscal update. Expect to see variants of this used throughout the 2015 election campaign when the incumbent government debates the plight of Canada’s “middle class” with opposition parties.  7. Federal income-splitting: promise made; (modified) promise kept

7. Federal income-splitting: promise made; (modified) promise kept

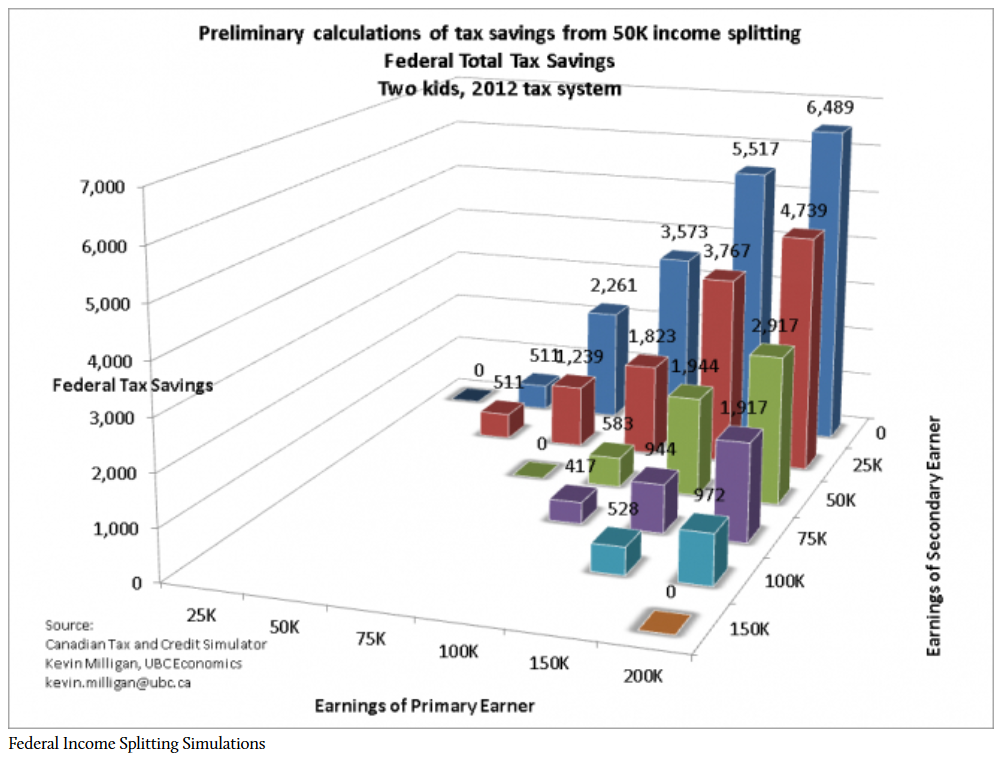

Income splitting was perhaps the most contentious and debated fiscal policy issue of 2014. This was mainly because of distributional considerations, where analysts on the left and right of the political spectrum agreed that it will disproportionately benefit higher-income households in Canada — Kevin Milligan‘s calculations are shown below.

To address concerns, the government ultimately introduced income-splitting with a few twists: it capped the maximum tax benefit at $2,000 dollars annually per household; it designed things to avoid provincial revenue impacts; and it expanded child care benefits as part of a broader package of policy reforms. Child care policy is set to be a prominent election topic for 2015, with each party looking to distinguish itself.

8. Shrinking future federal surpluses

8. Shrinking future federal surpluses

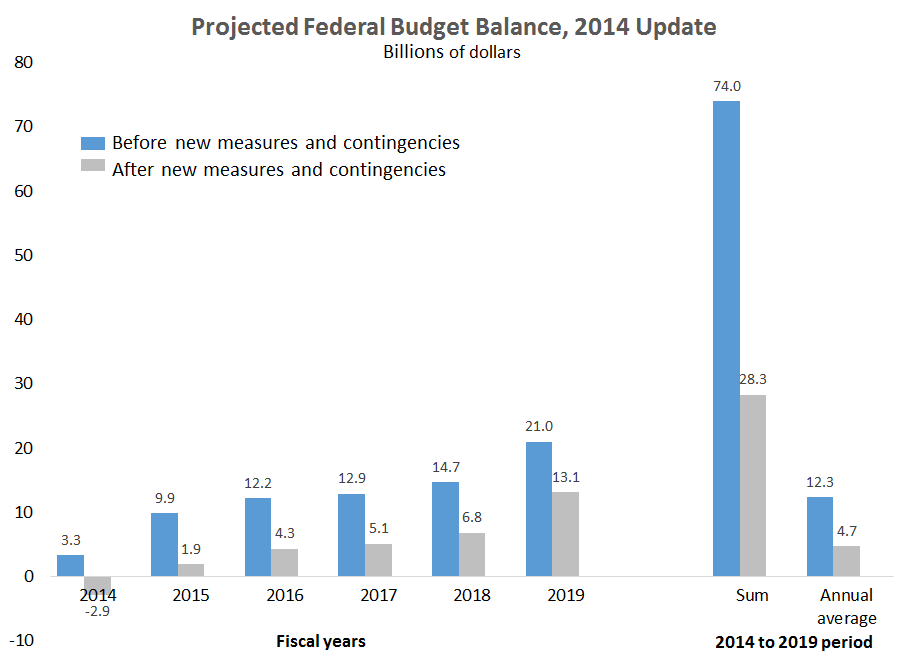

Continuing to look ahead to the 2015 election, the federal government used its first-mover advantage in 2014 by allocating anticipated federal surpluses and setting the status quo path of fiscal policy. Accounting for new measures (income-splitting, child benefits and a small business EI tax credit among others) and budgeting contingencies reduced the expected federal surplus from around $74 billion to $28 billion (summed over this fiscal year and the next five years). And since these numbers from the fall update there may be even less fiscal room come election time, should oil prices stay lower.

Opposition parties in 2015 will therefore face the challenge of: perhaps undoing recent moves; or emphasizing a larger role for the federal government in Canada; or even convincing voters that modest deficits can be tolerated when new programs are introduced, given the low and declining federal debt-to-GDP ratio.

9. Forward guidance disappears but interest rates may be lower-for-the-long-run

With Canadian policy interest rates holding steady since 2010, monetary policy has been rather uneventful in recent years. But in 2014, despite no change in the policy rate, Canada still experienced some notably policy shifts.

Governor Poloz released a discussion paper (in a new form of “unconventional” monetary policy) explaining why the Bank of Canada would no longer provide ‘forward guidance’ or hints about the direction of future policy changes, at least in normal times. The Governor argued that allowing more uncertainty about the future direction of policy puts more onus on financial markets to analyze incoming economic data and mitigates addictive “one-way bets” that may exacerbate leverage and market volatility.

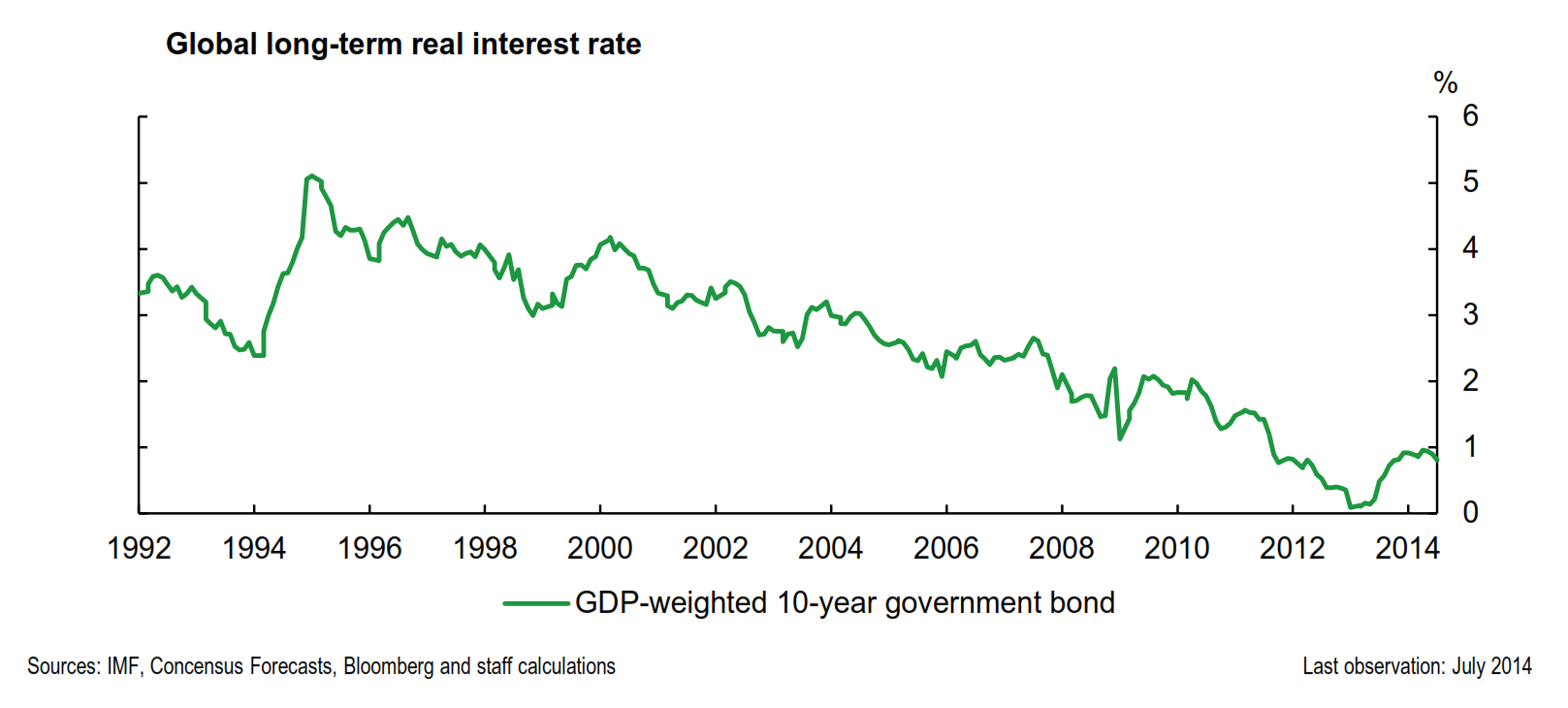

In addition, new Senior Deputy Governor Carolyn Wilkins made her first speech count – suggesting that when the policy rate eventually does normalize, it will likely top out at a lower level than was typical before the Great Recession. The Bank’s latest view is that a nominal policy rate of roughly 3-4% is “neutral” — more than one full percentage point lower than years ago — related in part to lower global interest rates. This is good news for those borrowing to finance purchases of houses or cars, but suggests that investors will have a tough time replicating the returns they enjoyed in previous decades.

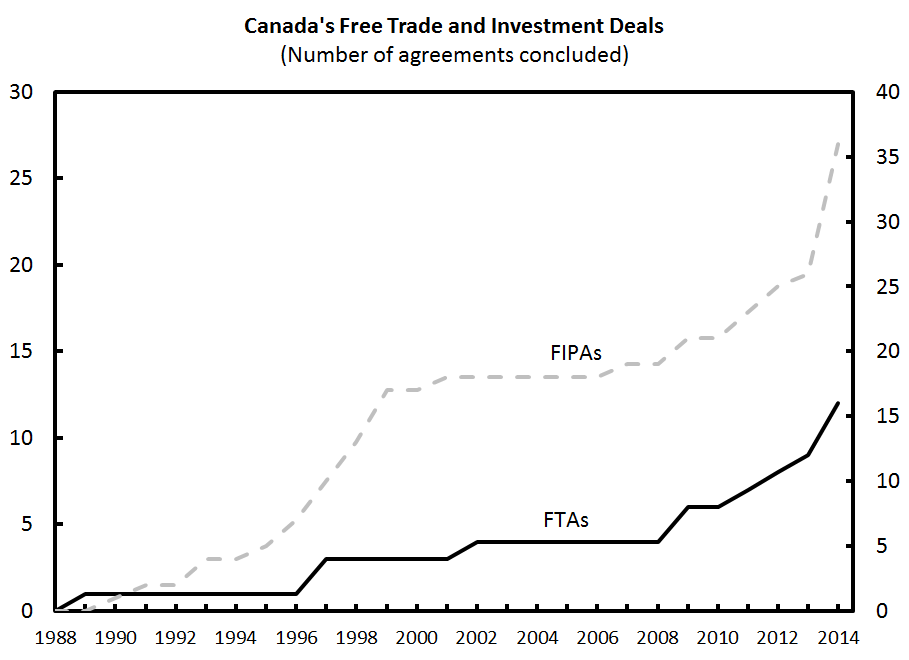

10. Trade policy keeps inking deals

10. Trade policy keeps inking deals

Canada’s trade negotiators were busy in 2014 signing several new trade and investment deals. On this trade side, the two most important deals were the more “offensive” Canada-EU deal (CETA) as well as the more “defensive” South Korean deal. Canada concluded several investment agreements as well, including those with seven different African countries. But by far the most important investment deal of the past year was the Canada-China agreement. This received much less government fan-fare than CETA, but together with the planned renminbi trading hub in Canada, has the potential to strengthening economic linkages between Canada and China in the future.

Also consequential in global trade policy in 2014 was the fact that the World Trade Organization (WTO) narrowly survived a truly existential crisis. Multilateral trade talks started the year on a high note, fresh from the first significant deal struck in decades, that was agreed to in Bali in December 2013. However, by the summer of 2014 in an unprecedented development, implementation of the Trade Facilitation Agreement (TFA) was in jeopardy — to the point that the WTO’s Director-General Roberto Azevêdo acknowledged that the organization was “truly at a watershed moment” and that failing to deliver could irreparably damage their credibility. The TFA was eventually salvaged late in 2014, but next year will also be an important test of the WTO’s ability to serve as a negotiating forum for global trade rules.

Also consequential in global trade policy in 2014 was the fact that the World Trade Organization (WTO) narrowly survived a truly existential crisis. Multilateral trade talks started the year on a high note, fresh from the first significant deal struck in decades, that was agreed to in Bali in December 2013. However, by the summer of 2014 in an unprecedented development, implementation of the Trade Facilitation Agreement (TFA) was in jeopardy — to the point that the WTO’s Director-General Roberto Azevêdo acknowledged that the organization was “truly at a watershed moment” and that failing to deliver could irreparably damage their credibility. The TFA was eventually salvaged late in 2014, but next year will also be an important test of the WTO’s ability to serve as a negotiating forum for global trade rules.

Stephen Tapp is a Research Director at the IRPP. Follow him on Twitter @stephen_tapp, or e-mail him at: stapp@irpp.org.