The global economic landscape of the past 10 years has not been kind to Ontario. Arguably, the two most important economic developments of recent years have been the emergence of China and a faded US outlook in the wake of the devastating financial crisis and the Great Recession. The former has put sustained upward pressure on commodity prices, in turn powering the Canadian dollar to modern-day highs. With few direct exports to China, limited commodity endowments and the relatively high share of manufacturing output, Ontario has not benefited much from the boom in China. However, the province has been hit especially hard by the surging loonie, as well as a weakened US economy, due to its heavy reliance on the US economy. Against this backdrop, it’s hardly surprising that Ontario has posted the slowest GDP growth among the 10 provinces over the five-year period from 2006 to 2011, despite recording one of the largest population increases (table 1). Similarly, the Ontario jobless rate remains stuck above the national average, a situation that was unheard of in the 30 years prior to the latest recession.

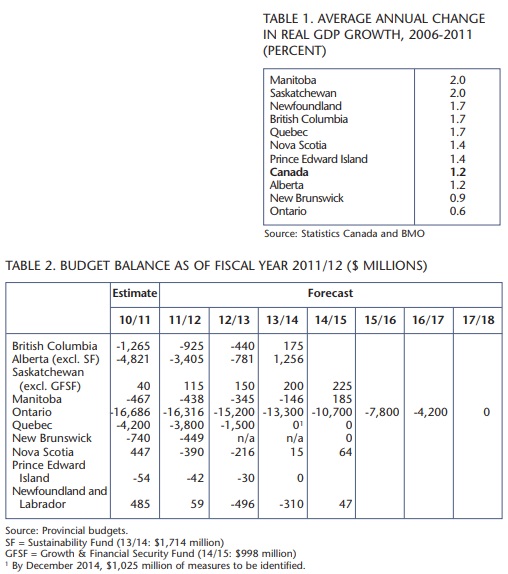

The struggles of the underlying provincial economy go a long way to help explain the fiscal difficulties that Ontario now finds itself in. The provincial government is continuing with its policy to eliminate the deficit, gradually, over the next six years. However, the province still faces the longest road to a balanced budget among the federal and provincial governments. Ontario’s fiscal hole is arguably the deepest in Canada, partly because Ontario’s economy is very sensitive to US economic developments (figure 1). This sensitivity placed, and continues to place, constraints on the pace of deficit reduction. However, by not permitting recent positive deficit surprises to more fully pass through to the medium term, the province makes its goal of balancing the budget by fiscal year 2017/18 that much more challenging. In fairness, Finance Minister Dwight Duncan did not succumb to the temptation in this year’s budget statement to broadly sprinkle the document with goodies, even though there is an election scheduled this fall under the fixed-date rules for Ontario. Nevertheless, over the medium term, we believe that deficit reduction delayed is potentially fiscal flexibility denied. If spending restraint decisions are hard to make now, when the economy is recovering and the interest rate backdrop is highly favourable, they will become even harder to make in the years ahead when the demographic demand for health care piles an even greater burden on provincial finances.

The Province of Ontario is projecting a $16.3-billion budget deficit in the fiscal year that just began in April (fiscal year 2011/12), which is still equivalent to 2.5 percent of GDP (table 2). This is a $1-billion improvement from last year’s budget, but as a share of GDP, it would still represent the largest budget gap in the country, including Ottawa. The modest improvement in the deficit reflects higher revenues owing to somewhat stronger economic growth, lower debt service charges owing to lower interest rates, and a reduced reserve fund for contingencies. These three factors represented a combined $1.8-billion improvement over last year’s budget, but projected program spending was bumped up a notch, in order to finish stimulus infrastructure projects by giving them an additional construction season.

The $16.3-billion shortfall reflects only a tiny improvement from the $16.7-billion deficit now estimated for the prior fiscal year (FY10/11), but at least it’s a baby step in the right direction. This could become a bigger step if the $1.4 billion in contingency funds and the remaining reserve aren’t tapped. The $16.7-billion deficit estimate for fiscal year 2010-11 represents a $2-billion improvement from last autumn’s fiscal update and betters last year’s budget projection by fully $3billion. So there has been some very real improvement in Ontario’s fiscal backdrop in the past year. The pressing question is whether the improvement is nearly fast enough, given the economic environment and longer-term challenges.

Reflecting the revenue and expense patterns described below (and a $1-billion annual contingency reserve), Ontario’s deficit is projected to continue declining during the medium term, to $15.2 billion in fiscal year 2012/13 (a slender $0.7-billion improvement over last year’s projection), and to $13.3 billion in FY13/14. The latter is identical to last year’s budget forecast. Despite a fiscal planning windfall that saw the deficit come in $3.0 billion lower in the fiscal year that just ended (and a whopping $5.4 billion lower in the prior fiscal year compared to the initial projection), the additional deficit improvement momentum completely peters out after two years. However, there is scope for additional deficit improvement if a significant portion of the reserve and contingencies is not spent, as has been the case over the last two years. The medium-term path to a balanced budget by FY17/18 remains unchanged, despite the more favourable starting point. Meanwhile, Ottawa is now actively discussing the possibility of balancing its budget one year earlier than the previous target of FY15/16. In other words, the federal government could balance three years ahead of Ontario, a hefty discrepancy.

Ontario’s revenue is expected to rise 2.2 percent to $108.5 billion in fiscal year 2011/12 as the economic recovery drives further growth in income tax receipts. Personal and corporate tax revenue will each rise more than 7 percent this coming fiscal year, while federal transfers are expected to drop 5.7 percent. The drop in funds from Ottawa partly reflects the drying up of stimulus, as well as the end of HST transition payments, and — importantly — is despite an expected rise in Equalization payments to Ontario to more than $2 billion. There were no major tax-related measures in this budget. Looking ahead, Ontario’s revenue is projected to rise at a 4.3 percent annual rate through FY17/18, a slightly slower pace than the 4.8 percent growth seen during the past decade. However, starting in FY13/14, the province has pencilled in five years of uninterrupted growth of about 5 percent per year, an outcome that is not unrealistic, but not overly conservative either, and would be seriously jeopardized by another meaningful economic slowdown, let alone another US-led downturn.

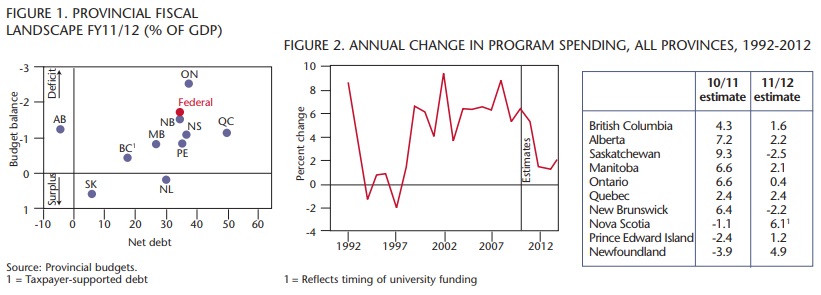

Total provincial spending in Ontario is projected to rise 1 percent to $124.1 billion in fiscal year 2011/12, including $10.3 billion in debt service costs. Program spending is expected to inch up 0.4 percent to $113.8 billion in fiscal year 2011/12, restrained by the fact that some temporary stimulus measures are winding down (figure 2). For example, transitional HST rebates will shrink to $1.4 billion this fiscal year before fully winding down, from $3.2 billion in FY10/11. Excluding this factor, program spending will grow 2.1 percent this coming fiscal year. While there are not many new big measures in this budget, at least one grabbed headlines: funding to create 60,000 new university spaces over five years, at a cost of just over $300 million per year by FY13/14. Overall, health care (+4.9 percent) and education (+4.5 percent) will continue to see growth this fiscal year, but then slow to 3.1 percent and 1.7 percent per year, respectively, through FY13/14 as the province attempts to control growth in these two critical categories. New cost savings of $1.5 billion through FY13/14 are identified in this budget, and include agency efficiencies, operating expense savings and efficiencies in the health care system.

Total provincial spending in Ontario is projected to rise 1 percent to $124.1 billion in fiscal year 2011-12, including $10.3 billion in debt service costs. Program spending is expected to inch up 0.4 percent to $113.8 billion in fiscal year 2011-12, restrained by the fact that some temporary stimulus measures are winding down.

Provincial infrastructure spending will total $12.1 billion in FY11/12, little changed from the prior fiscal year. Total infrastructure investment in the province, including federal transfers and partner investments, will be down 9.6 percent. Even so, it speaks volumes that provincial spending on infrastructure will actually creep up this year, despite the fact that the era of stimulus is over with the recession now two years in the rearview mirror.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

Looking ahead, the province is targeting program spending growth of 1.4 percent per year through fiscal year 2017/18, a stark change from the 7.8 percent annual growth over the past decade (note that the latter figure is inflated somewhat by temporary spending measures, but growth in the five years through FY08/09, before stimulus programs kicked in, was still running above 6 percent per year). On a real per-capita basis, program spending will shrink more than 1.5 percent per year through fiscal year 2017/18 (assuming 1 percent population growth), a level of restraint not seen in the province since the mid-1990s. Again, this slowdown appears more dramatic as a result of a boost to temporary spending, but real per-capita spending in the five years starting in fiscal year 2012/13, when those items are out of the calculation, is still slated to contract a bit more than 1 percent per year. If the discipline to hit these targets is maintained, and the economic expansion proceeds as forecast, Ontario’s budget could be brought back into balance without any further major policy response. However, it will depend on a level of restraint not seen in recent years and rely on the expansion remaining healthy for a prolonged period. And will while the expected rise in program spending in the next few years is certainly much more modest than in recent years, the fact that it is increasing at all in nominal terms underlines the stately pace of deficit reduction in the province, and the perceived lack of urgency among policymakers.

Ontario’s total long-term borrowing requirements are projected to be $35.0 billion in fiscal year 2011/12 (including $14.4 billion of refinancing). This is roughly $5 billion below the level borrowed in fiscal year 2010/11, reflecting the government’s decision to prefund some of the fiscal year 2011/12 requirements last year owing to very favourable financial market conditions (and the slightly lower deficit helped a bit as well). Boosted by the extra borrowing in the fiscal year that just ended, cash balances will be drawn down by $4.6 billion in the current fiscal year. The province expects to tap the domestic market for at least 60 percent, or $21 billion, of its funding needs and the remaining amount ($14 billion) in foreign capital markets. It is therefore critical that the province continue to maintain the very high standards by which it is currently judged by foreign investors. Net debt was estimated to be $217 billion as at March 31, 2011, or 35.4 percent of GDP, a figure that will continue to rise, reflecting persistent large deficits. The net debt-to-GDP ratio is projected to peak at 40.6 percent at the end of fiscal year 2014/15, above the highs seen in the late 1990s. However, debt service costs will remain below 12 percent of revenue in the coming years versus as much as 17 percent in the late 1990s, thanks to the world of very low interest rates we still find ourselves in. This interest ratio is manageable, but the growing debt load could pose a significant threat if interest rates rise materially in coming years. While we don’t place a high probability on that risk, it is an area of vulnerability.

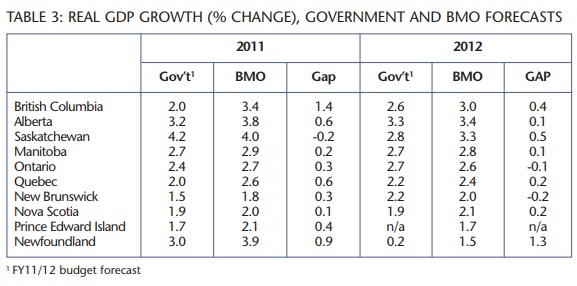

The Ontario economy has geared down from a strong post-recession rebound. Quarterly growth has slowed from a 6 percent-plus pace at the end of 2009 to a more modest 2.8 percent for all of 2010, tempered by softness in net exports and slower public-sector spending. These two areas, along with cooler housing activity, are the key factors shaping a less robust growth profile in Ontario than in some other faster-growing provinces, namely western Canada. A strong Canadian dollar should continue to weigh on net exports, though they won’t be nearly the drag on growth that they were in 2010, and auto production figures to be disrupted by parts shortages in the wake of the Japanese earthquake and tsunami. Meanwhile, real government spending growth slowed significantly in the second half of 2010, a theme that should persist as the province heads down the road back to a balanced budget. Still, there are some economic bright spots in Ontario as employment has rebounded to near prerecession levels. Overall, real GDP growth should cool modestly to 2.7 percent in 2011, and slow further to 2.6 percent in 2012 (table 3). This budget is based on the assumptions of 2.4 percent and 2.7 percent growth in 2011 and 2012, which we deem to be reasonable.

Looking further ahead, the medium-term economic outlook for Ontario will be challenged by the need for years of moderate fiscal restraint, whereas almost all other provinces and Ottawa will presumably be in balance by mid-decade and able to lighten up on the fiscal reins by that time. This will compound the challenges the province faces from the twin weights of the soaring Canadian dollar and the intense competition from emerging market manufacturers. Suffice it to say that policy-makers may soon regret not having taken more forceful action on making hay on the deficit front while the economic sun was still shining.

Michael Gregory and Robert Kavcic assisted in the preparation of this article.

Photo: Shutterstock