Section 36 (1) of the Constitution Act, 1982, commits all governments and legislatures to “promote equal opportunities,” “further economic development to reduce disparity” and “provide essential public services of reasonable quality to all Canadians.” Section 36 (2) enshrines the aspirational “equalization” principle that provincial governments should have “sufficient revenues to provide reasonably comparable levels of public services at reasonably comparable levels of taxation.”

Fundamental shifts in the global (and hence the Canadian) economy will make it increasingly difficult to realize the equalization principle in the decade ahead without damaging the economy and threatening national unity. Consistent with the overarching spirit of section 36, a more productive and less divisive objective would be to ensure that all provinces possess the fiscal capacity to provide public services of “reasonable quality,” while making investments that build the fiscal capacity of lower-income provinces and reduce income disparity through further economic development.

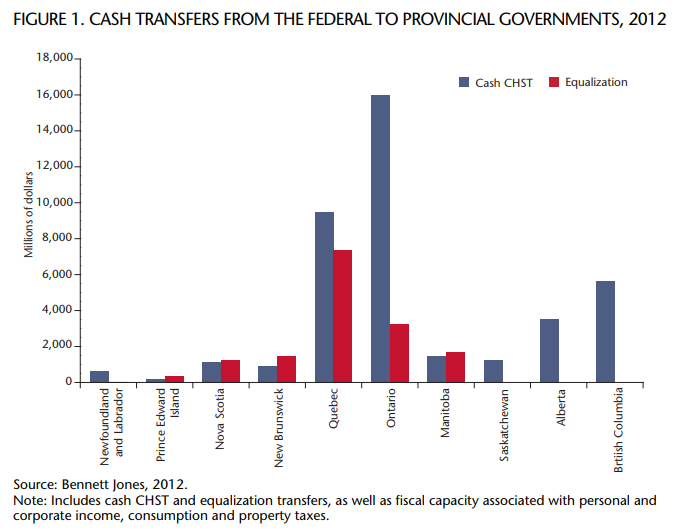

Currently, federal cash transfers to the provinces occur in two distinct ways: about two-thirds ($40.3 billion in 2012) in the form of Canada Health and Social Transfer (CHST) cash transfers to all provinces to support the delivery of specific services — health care, social welfare and higher education, and the other one-third ($15.4 billion) formula-derived equalization payments to lower-income provinces (see figure 1). These transfers represent a share of estimated total provincial tax capacity in 2012, which ranges from 9 percent in Alberta to nearly 40 percent in New Brunswick. Both programs are financed with revenues generated from the federal tax base, which taxes the income and consumption of Canadians without regard to province of residence. The net effect of such transfers, in concert with a progressive federal tax system, is a redistribution of income and services from high-income to low-income Canadian households and a transfer of resources both between and within provinces.

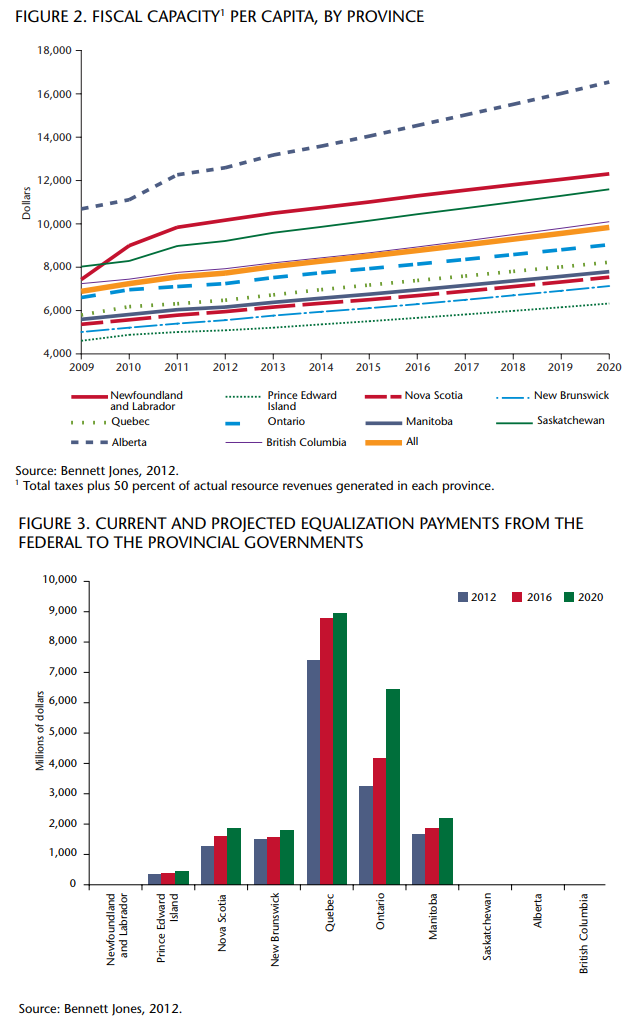

The current regime of federal-provincial fiscal arrangements is due to expire in less than two years. The federal government has already addressed the CHST, laying out in December 2011 a long-term plan that will restore equal per capita treatment (including for affluent Alberta) and result in cash payments growing at a 6 percent rate until 2016-17 and a rate of at least 3 percent thereafter. The government also announced that aggregate equalization payments will continue to grow at the rate of nominal economic growth and that officials will study and resolve “technical issues,” including the determination of fiscal capacity (figure 2).

This determination of fiscal capacity is currently accomplished through the application of the average Canadian tax rates for personal and corporate income, consumption and property taxes to each provincial tax base (to assess their revenue-generating potential), plus the addition of 50 percent of the actual (not potential) revenues generated by a province from natural resource development. Fiscal capacity therefore depends on a range of economic variables that are driven by the major forces shaping the global and Canadian economies.

Two prevailing forces are of fundamental importance. One is the projected continuing growth of the emerging market economies, particularly China, which will continue to boost both global demand for a wide range of commodities and the supply of competitively priced manufactures. The result has been a marked shift in the terms of trade, away from manufactured goods and services to natural resources — a shift that generally benefits Canada as a whole, but that has very different regional impacts.

The negative impact of the changed terms of trade on Canadian manufacturers has been reinforced by continuing slow US demand in the aftermath of the 2008 financial crisis, the second important factor in the current global economy. Beyond the general malaise of slow growth and high unemployment in the United States, which is of particular importance to Ontario (the province most dependent on Canada-US commerce), there is the continuing southward shift in the locus of North American manufacturing and automotive assembling, away from “Michigan, Ohio and Ontario” toward the “Southern United States and Mexico.” Ontario-based manufacturers are also facing a loss of cost competitiveness due to the appreciation of the Canadian dollar and rising Canadian dollar unit labour costs relative to the US.

The ultimate impact will be a continuing diverging of the fiscal capacities of the resource-rich provinces and the rest of Canada, and a continuing fall in Ontario’s share of the national economy below its share of population — for the first time since Confederation.

Ontario’s new status and the growing income gap between the four “have” and the six “have-not” provinces are creating unprecedented and unavoidable challenges that are leaving policy-makers boxed in with few viable options. For one thing, the maths no longer work. Populous Ontario changing places with thinly populated Newfoundland means there are still four have provinces, but the haves now account for less than 30 percent of the national population, with the six have-nots now accounting for 65 percent of the federal tax base.

As a result, raising the per capita fiscal capacity of all low-income provinces up to the national average cannot be achieved within the current program cap (that is, without raising federal tax rates), and the shortfall will grow into the future. Increasing federal tax rates to fund increased equalization payments becomes akin to a dog chasing its tail, with federal taxes from Ontarians paying Ontario. And even if all the have-not provinces received sufficient transfers to attain the national per capita average, they would still not be able to provide, at comparable tax rates, services that are comparable to those in the provinces with (well) above-average incomes.

This conundrum also creates new political challenges.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

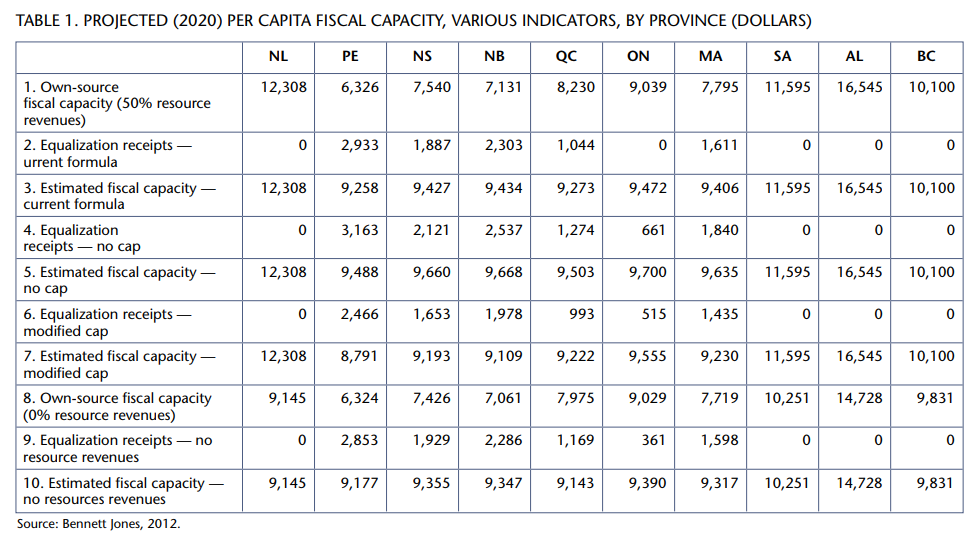

Under a base-case “moderate-growth” economic scenario, the existing equalization formula will cause Ontario to move from receiving a 21 percent share of equalization payments in 2012 to receiving 30 percent by 2020, with its payments rising from $3.3 billion to $6.4 billion. With Ontario’s equalization payments beyond 2012 growing at 9 percent, other equalization recipients can expect to receive a flow of funds growing at just under 3 percent, likely below the rate required to maintain services at current levels. It therefore remains to be seen how the traditional have-not provinces will respond to a call to make more room in the equalization boat for a struggling Ontario with large and growing needs (see figure 3).

Federal and provincial officials are beginning discussions on certain technical issues. One such issue might be addressing expenditure needs. Equalization in Canada has focused on the revenue side (provincial fiscal capacity), while ignoring the cost of providing “comparable social services” (expenditure needs). While some analysts have suggested moving to a system that measures both fiscal capacity and expenditure needs, we argue that deploying the latter concept should be limited to transfers for specific purposes (e.g., health and education), rather than equalization payments designed to fund social services in general. As a relatively easy first step toward a system that incorporates expenditure needs, and in light of the fact that health care costs will be outpacing nominal growth in the years ahead, consideration should be given to age-weighting the per capita health transfer, which would primarily benefit the aging Maritime provinces and Quebec.

Another issue might be removing or modifying the Equalization cap. Since the growth of equalization payments is constrained to the nominal rate of Canadian economic growth, this prevents raising the per capita fiscal capacity of all lagging provinces to the national average. The “shortfall” would be $2.0 billion in 2012 (12 percent of uncapped entitlements), which would increase to $6.1 billion in 2020 (22 percent). (To put the shortfall in perspective, a 0.5 percent increase in the GST rate would raise roughly $3 billion this year.) Uncapping Equalization payments would primarily benefit Ontario, which would receive an additional $3.4 billion in 2020, or about $1.1 billion net of the increased tax contributions from Ontarians that would be necessary to fund the increase (see table 1, lines 1, 4 and 5).

Alternatively, one could consider changing the allocation of the shortfall, which is currently spread across receiving provinces on the basis of their respective populations (i.e., an equal per capita reduction), and not in proportion to their pre-cap equalization entitlement. Modifying the allocation method would favour Ontario, to the detriment of the Maritimes and Quebec (see table 1, lines 6 and 7).

Another (always controversial) issue is the treatment of resource revenues. Currently, the equalization formula measures potential income, consumption and property tax revenues, and 50 percent of actual resource revenues. Eliminating resource revenue from the formula would not affect the federal tax base or total equalization payments. It would better align provincial fiscal capacities with the federal tax base, stabilize and narrow the range of fiscal capacities, avoid a potentially divisive issue concerning the pricing of renewable resource revenue (hydroelectricity) in hydro-rich Quebec and Manitoba, and reflect that the sale of a nonrenewable resource revenue can be likened less to the generation of income than a one-time conversion of a capital asset into capital funds that should be re-invested.

Removing resource revenue from the formula would work primarily to the benefit of Quebec (the “have-not” province with highest resource revenue per capita). As well, it would still leave Alberta’s 2020 fiscal capacity about $4,500 per capita higher than second-position Saskatchewan and approximately twice those of the Maritime provinces. This is because Alberta’s high fiscal capacity is due more to the high level of employment and corporate income than to resource royalties (see table 1, lines 8, 9 and 10).

Canada is a political, monetary and economic union. Transfers play an important role in preserving the integrity of the union — not just to promote equality of opportunity and ensure the provision of basic services to all, but also to minimize instability when economic cycles produce adverse and unequal regional impacts.

However, transfers can also play a counterproductive role if they act to mask inexorable structural change, delay necessary adaptation and create the illusion that the unsustainable can somehow be sustained indefinitely. Ultimately, they can destroy unity by creating resentment, disrespect and distrust. In the long run, unions can be sustained only when all members are able and willing to fully participate and contribute to the union.

Equalization is a zero-sum game of income redistribution that increasingly generates more resentment than satisfaction. Adopting some or all of these technical changes to the equalization formula may mitigate the problem but will not be a sustainable solution to today’s unprecedented challenge — a challenge that is not cyclical and destined to quickly disappear, but structural and longer-term.

We believe the “solution” lies elsewhere: we need to focus less on the equality (or comparability) and more on the quality (or adequacy) of public services; less on federal transfers that redistribute income to “equalize” fiscal capacity, more on federal investments that will create more income and build the fiscal capacity of today’s lower-income provinces. We need policies that promote positive provincial convergence and the development of competitive manufacturing and service industries, and that also reflect the practical reality that Canada’s economic prosperity and political equilibrium ultimately depend on the economic strength of all provinces, especially populous Ontario.

In short, we need to think and look outside the equalization and transfers box, outside the narrow confines of subsection 36 (2) of the Constitution Act, 1982, and look to the broader economic objectives of subsection 36 (1).

Photo: Shutterstock