Over the past year, the fanfare of the “Asian Century” mind frame that essentially takes Asian growth dynamics has finally hit Canadian shores, and large swaths of the policy community are abuzz with notions of a “pivot” from slow-growing crisis-stricken partners in the United States and European Union, toward fast-growing emerging markets in Asia. Truth be told, though, the momentum of an economy of Canada’s size and complexity is more like a large oil tanker that simply does not pivot or change direction easily. After decades of Canada following a comfortable economic strategy that placed access to the US market at its core, pulling off a pivot to Asia, and to China in particular, will need more than catchphrases; it will need a serious strategic analytical rethink by Canadian policy-makers.

Make no mistake: the structural pattern of Canada’s economic development is not well-suited to taking advantage of dynamic emerging markets in a shifting global landscape. Instead of directly engaging with emerging market counterparts, Canada’s large companies and their suppliers, many foreign owned in strategic manufacturing sectors, generally act as regional “junior partners” to US multinational corporations. Put another way, Canada faces the potential for the “real” globalization of its economy, and at issue are the terms on which its government, firms and workers are able to manage the course of their economic destiny. Some policy discussions have tiptoed around the topic, but it seems the unspeakable words are still “industrial policy.”

While other policy-makers and analysts, some in these pages, have offered reasonable and even pragmatic economic advice on different elements of an Asia strategy, most are generally cut from the same free trade-only approach and for granted. To some extent, this is not surprising; even the Economist’s January issue on state capitalism painted all such varieties with more or less the same brush strokes. Others find little contradiction in professing greater recognition and legitimacy of the role of government in directing growth in emerging markets, but then reflexively return to orthodoxy in advising (if more targeted) bilateral and/or multilateral free trade agreements with the now familiar restrictions on state action. This approach is largely a dead end that reveals more about a given commentator’s predilections for only certain kinds of policy advice and less about the real strategic options to effectively engage Asia.

Such blind spots can be debilitating. As John Williamson recently claimed, “The West is still living with the consequences of its decision to call the East Asian crisis a comeuppance for crony capitalism,” which only further fuelled the problem of global payment imbalances in the lead-up to the Great Recession. To inject more pragmatism into the debate and in light of China’s centrality to an overall Asian strategy, this article argues that a meaningful pivot entails a deeper understanding of China’s variety of state capitalism through an analysis of the current stage of its economic system: its construction, functionality, ambitions and evolution, rather than principally by reference to something it should be or is not. Only such a pragmatic approach can reveal “gamechanging” insights and opportunities that go beyond immediate concerns with increasing the current pattern of bilateral trade and investment flows, to deeper issues of unlocking some of Canada’s built-up structural weaknesses.

Getting to know the Chinese better may not be a bad thing. Clark Manus, president of the American Institute of Architects, noted: “The US political establishment is mostly attorneys and other people who are involved with political science. In China, the highest-ranking officials tend to be engineers. They see a problem, they allocate money and effort toward a solution.” Indeed, identification of common problems and structural weaknesses, such as a lack of globally competitive “national champions” and sustained intellectual property (IP) deficits — a recent Canadian International Council study reported 2009 IP deficits (net royalty and license fees) of roughly $4.5 billion for Canada and $10 billion for China — could be the grounds for well-crafted partnerships that could ultimately bolster the economic strengths of the parties involved.

To this end, and to contribute to the growing demand for strategic public policy analysis to better inform a Canada-China strategy, this article builds on a 2011 Economist Intelligence Unit (EIU) report entitled “Heavy Duty: China’s Next Wave of Exports” by replicating for the Canadian context a key part of its analysis that uses an “export radar” methodology. In providing this brief comparative analysis, the article shows the recent export trajectories of both countries, to better illustrate China’s stage of economic development in relative context. The article then shifts to examine features of China’s state capitalism policy framework — including its ambitions to rise to the apex of global supply chains using a controversial “indigenous innovation” strategy — in order to highlight opportunities that could also be creatively leveraged in Canada’s favour.

In some ways, the short 12-page EIU report is both economically seminal and heretical. Seminal because the historical international division of labour where China acts as a cheap platform for production of labour-intensive, low-end goods — clothing, textiles, footwear, toys, etc. — and for low value-added assembly of more sophisticated electronic goods (high import content) is becoming less distinct than in the past.

With China’s wages rising and technological capacity improving, exporters will move up the value chain to increasingly encroach on core product markets shares of developed countries, notably in third-country export markets of other developing countries.

With China’s wages rising and technological capacity improving, exporters will move up the value chain to increasingly encroach on core product market shares of developed countries, notably in third-country export markets of other developing countries. The report focuses on trends showing that domestic Chinese heavy-equipment manufacturers, particularly in the construction machinery sector, are playing an increasingly prominent role in driving the country’s exports, which is estimated to lift the share of China’s exports produced by domestic companies past the 50 percent mark by 2012.

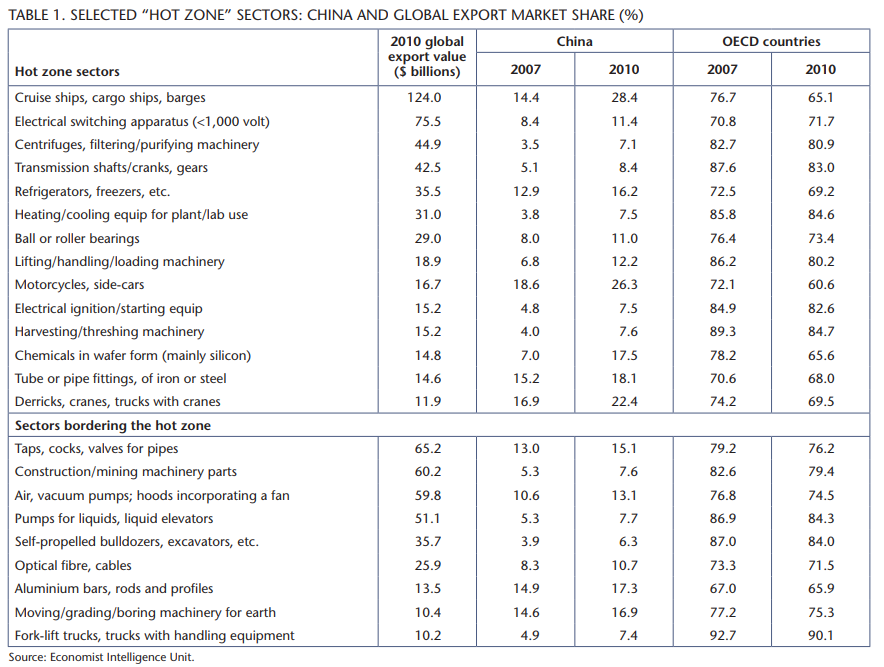

At the heart of the EIU’s report is the China manufacturing “export radar” graph that provides an overview of the sectors in which Organisation for Economic Co-operation and Development (OECD) member countries are currently facing the evolving reality of Chinese export competition. The export radar breaks down a total of 217 merchandise export markets/sectors (at the HS-4 level), each with a global export value of at least $10 billion in 2010, by plotting each export market in terms of OECD countries’ share of global exports for that product in 2007 (horizontal axis), against the four-year percentage point change in market share experienced by China from 2007 to 2010 (vertical axis).

The radar is then segmented into four quadrants according to the average market share change by China, in conjunction with the average share held by OECD countries. As a result, the topright quadrant is labelled the “hot zone”: export markets in this quadrant represent sectors in which OECD economies held a dominant market share (i.e., greater than 70 percent of world export market share in 2007), but also in which Chinese exporters have gained significant ground over the period examined (i.e., greater than two percentage points).

A total of 37 sectors are located in the hot zone of China’s export radar, representing a global export market value of $927 billion in 2010. Across these sectors, the OECD countries’ share has dropped from 79 percent in 2007 to 74.7 percent in 2010; as for China, its share rose from 8.5 percent to 14 percent. Many of these gains are coming in nonOECD markets: in 2008, for example, in the machinery sector alone, 71.5 percent of all such imports to Brazil, Russia, India and South Africa came from the OECD countries. By2010,thissharefellto63 percent, whereas China’s share rose from 17.5 percent to 21.8 percent during that same period.

As seen in table 1, most of the sectors found in or bordering near the hot zone involve heavy industry capital equipment and parts, indicating improvements to Chinese production related to precision metal-cutting/ shaping and in metallurgical processes that have upgraded their ability to supply components with a greater level of strength, durability and precision. While the EIU notes that these hot zone sectors still account for a relatively small portion of world trade — for instance, China has yet to make a large dent in the $553 billion auto export market, the $310 billion packaged pharmaceutical market or the $85 billion aerospace market — structural change in Chinese production and export patterns are showing credible signs of movement toward the mid and high range of global value chains.

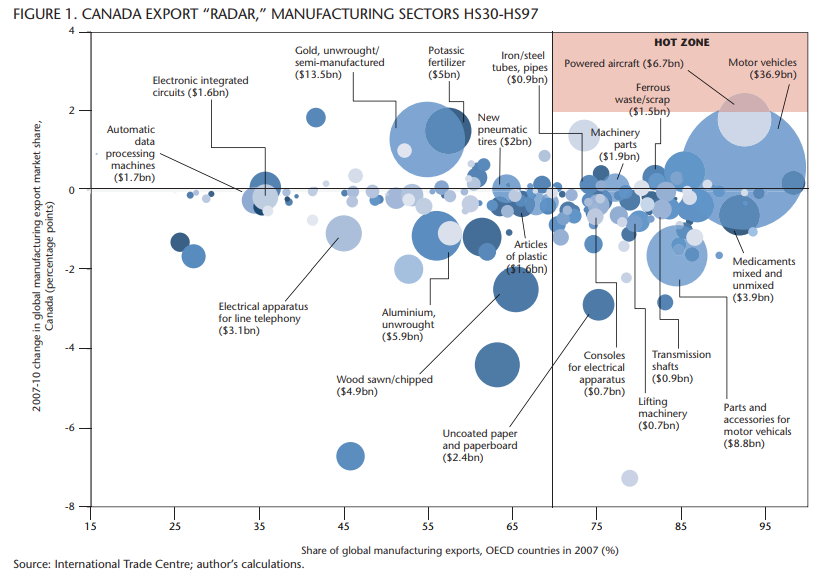

To provide a contrast to China’s export radar, figure 1 presents Canada’s export radar according to the same parameters used by the EIU report, as described above. Due to time limitations, the main difference is that the Canada radar only includes 181 merchandise export markets (instead of 214), with the “missing” sectors found in HS28 (inorganic chemicals) and HS29 (organic chemicals). The other alteration is in the size of the bubbles, which represents Canada’s 2010 global export value for a given export market, rather than the total global export value. Figure 1 also labels some of the export markets to give a rough sense of where different sectors are situated on the radar according to their coordinates along each axis and the size of Canada’s export value.

While a more thorough analysis is certainly needed, some observations on China’s and Canada’s export radars can be made in terms of differences related to respective stages of economic development. The broad structural makeup of sectors in their economies is represented by the size and location of the various export markets distributed across the four quadrants of the radar.

Some aspects of Canada’s export radar are to be expected, such as the large contribution of the auto and aerospace industries and related parts sectors that play an outsized role in driving Canada’s exports. Motor vehicle production, in which OECD countries held a 92 percent share of world exports, represented about $36.9 billion in Canadian exports in 2010. This is by far the largest export market segment in which Canadian-located producers have gained 0.6 percent in global market share from 2007 to 2010. Of all the market sectors surveyed, Canada’s exports of powered aircraft, worth $6.7 billion in 2010, had the highest global market share increase at 1.8 percent. Other obvious large export market sectors can be more closely linked to increasing commodity prices: for example, mineral or chemical potassic fertilizers accounted for $5 billion in Canadian exports in 2010, which raised Canada global market share by 1.5 percent.

In comparing China’s radar to Canada’s, though, what is striking is the shrunken size of Canada’s “hot zone,” which appears largely unpopulated by any market sector where OECD countries hold a dominant export market share and where Canadian exports are gaining global market share by greater than two percentage points. Indeed, a large proportion of all the market sectors surveyed have only relatively small values of Canadian exports and are located within the range of +/one percentage point change in Canada’s global market share. Thus Canada’s radar vis-à-vis China’s radar has a “downward tilt” since none of the market sectors where Canadian exports are gaining global market share have surpassed +2 change in percentage points. In this sense, China’s radar has a wider scope insofar as individual Chinese export markets show greater variation in gaining (and losing) global export market share whether inside or outside of the hot zone.

To some extent, Canada’s shrunken hot zone could be a reflection of Canada’s status as a more developed and diversified economy that is not in the middle of “catch-up” growth that is more common among emerging markets. Nonetheless, the fact that a large proportion of Canada’s export markets do not already have strongly established market shares, and do not appear to be gaining global market shares in sectors where OECD countries remain dominant, does not bode well for Canada’s higher value-added manufacturing export performance — whether to OECD countries or otherwise.

According to International Trade Centre figures, from 2001 to 2011, Canada experienced a significant decline in its share of world exports: this was a result of its natural resource (agriculture and mineral) exports falling from 5.0 percent to 3.5 percent as a share of world natural resource exports, a change of 30 percent. Meanwhile, Canada’s share of world manufactured exports also dropped from 3.9 percent to 2.2 percent, a change of 45.0 percent. Combined, the weighted change in its share of world exports was an overall decline of 39.5 percent. Such ominous trends are supported by Bank of Canada research indicating that between 2000 and 2010 Canada’s share of global exports nearly halved, the second worst trade performance in the G-20 (behind only the UK). Moreover, Canadian exports are concentrated in slow-growing advanced economies (85 percent of exports) — particularly the US market — meaning that stripping out exports to the US market could make the “downward tilt” of Canada’s radar even more pronounced.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

What makes the EIU report especially interesting is the manner in which many of the capital equipment and parts sectors found their way into the hot zone in the first place. Since a wide range of modern industries — such as automotive, aerospace, mining and construction — relies on machinery as key inputs to stay competitive the government labelled the sector a “pillar industry” at an earlier stage of the reform period and along with other “strategic sectors” regards it as the foundation of the manufacturing industry. This is the “heretical” part of the report, at least for those with less familiarity with East Asia, since it links sustained and selective state support for specific industries with China’s ability to credibly and aggressively move up the value chain.

As was often the case in other priority industrial sectors, to spur continued reform and modernization of production, the government took a gradual “dual-track” approach to opening up by delaying import liberalization and requiring US, Japanese and European firms to establish joint ventures (JVs) or cooperative production agreements without relinquishing Chinese majority ownership. This was the case in the metal-cutting machine tools sector: in the leadup to China’s entry into the World Trade Organization (WTO), total expenditure on metal-cutting machine tools increased from $1.4 billion in 1997 to $7 billion in 2006, with domestic demand met both by higher-end imports and by low- to mid-end domestic production either by JVs or by Chinese companies.

As part of the government’s formal adoption of a multifaceted “indigenous innovation” strategy in 2006, a State Council plan for the industry was issued in the document entitled “Opinions on the Revitalization of the Equipment Manufacturing Industries.” Calling for “mastering” and “absorbing” core technologies along with other criteria to reach global competitiveness, the plan listed 16 broad equipment manufacturing sectors in which domestic companies should expand market share, such as nuclear/thermal/gas electricity generation, electricity transmission, steel, energy, rolling-stock and railroads, pollution control, urban infrastructure, machine tools, agriculture, textiles and aerospace.

This vaguely worded plan was followed up in 2009 by another State Council document called the “Equipment Manufacturing Industry Adjustment and Revitalization Plan,” which in addition to setting out more sectors in which to encourage domestic production (some overlapping with the 2006 document) outlined a policy package with the following features:

- Value-added tax (VAT) preferences for higher value-added products/ equipment;

- Strengthen procurement preferences and oversight of government projects in support of domestically developed technologies and domestically owned intellectual property rights;

- Creation of a technically detailed procurement “list” to support these initiatives;

- Support and encouragement for insurance companies that write policies for domestically developed machinery technologies;

- Creation of four large research and development bases to support innovation;

- Preferential duties on imports of critical machinery not domestically produced and on key raw material inputs;

- Preferential VAT rebates for exports of higher value-added products/ equipment, increased allocation of export credits and procurement preferences for large projects outside of China;

- Various financial instruments to assist the restructuring and merging of domestic companies, including low-interest-rate loans, issuance of stock and/or bonds, and encouragement of financial institutions to provide financing for Chinese firms conducting domestic and overseas mergers and acquisitions deals;

- Consumption subsidies for products/ equipment that conserve on energy/ resources, as well as on agricultural machinery with emphasis on quick administration of these subsidies for farmers;

- Greater information sharing related to policy guidance, project planning, corporate restructuring, capacity utilization, exports/imports and other relevant information to production;

- Improvement of product/equipment quality assurance and certification.

The development of China’s construction equipment sector provides another illustration of the policy levers at play. Born out of the decades-long boom in domestic investment and demand, the sector was certainly distinct from the narrowly specialized low-value-added processing trade assembly operations that rely on export markets, but also grew up without JV arrangements. Thus the development of the construction equipment industry, and capital equipment industries more broadly, has been more organic — that is, involving greater levels of domestic ownership and a relatively more comprehensive domestic supply chain.

A key turning point in the development of China’s domestic construction equipment sector was the October 2005 bid by the Carlyle Group, a US private equity firm, to invest $375 million for an 85 percent stake in Xugong Construction Machinery Group, China’s largest construction gear maker at the time. Controlled by the local government of Xuzhou city (in Jiangsu province), Xugong received approval at the local level but was blocked by the ministry of Commerce of the central government. Carlyle revised its offer twice, restructuring the deal as a 50-50 joint venture and later offering to take a minority stake of 45 percent to allay Beijing’s fears of foreign ownership in a strategic industry.

After three years, however, Carlyle ultimately dropped its bid for Xugong in 2008, in what was seen as a touchstone case of Beijing’s stance on foreign investment in sensitive sectors. As a result, most international private equity activity in China today consists of taking minority stakes in firms that are private, about to go public or already listed on domestic stock exchanges.

Today, China’s three largest “national champions” in the sector (Xugong, Sany Heavy and Zoomlion) dominate the domestic market in cranes, cement mixers and earth movers, while also gaining market share in more sophisticated product categories such as hydraulic excavators.

Certain facts surrounding the case are intriguing. For one, Beijing’s blocking of the Carlyle-Xugong deal came only two months after the failed takeover bid of the US firm Unocal Oil Company by the China National Offshore Oil Co. in August 2005. Morever, pressure to halt the Carlyle-Xugong deal was heightened by a nationalist Internet campaign to stop the sale of state assets at knockdown prices. Reflecting perhaps the heat of interprovincial competition, the campaign was led by Xiang Wenbo, chief executive of Sany Heavy Industry (based in Hunan province), a rival to Xugong that would later surpass it as the country’s biggest construction equipment maker (by sales revenue).

Today, China’s three largest “national champions” in the sector (Xugong, Sany Heavy and Zoomlion) dominate the domestic market in cranes, cement mixers and earth movers, while also gaining market share in more sophisticated product categories such as hydraulic excavators. For now, China’s exports of construction gear are mainly destined for other developing country markets, where Russia and Brazil are the largest importers of China’s earthmoving equipment and India is the biggest buyer of its cranes. However, the acquisitions of niche German high-tech concrete pump-maker Putzmeister by Sany Heavy in 2012, of Schwing Stetter by Xugong in 2012 and of Italian concrete pump-maker CIFA by Zoomlion in 2008 suggests that penetrating the difficult US and European markets may not be mission impossible after all.

From the above, perhaps it is not surprising to often hear of China’s more comprehensive approach to industrial development and planning across a variety of sectors. Its version of state capitalism has been described as strategically deploying powerful policy, administrative and financing tools to guide publicand privatesector players into fulfilling greater economic development aims. In times past, China’s sectoral plans like the ones described above would not be taken seriously. Today is a different story. As Andy Rothman at CLSA AsiaPacific Markets put it: “The Chinese Communist Party is the most liquid financial organization in the world.”

While China’s development story is certainly making forward strides, it also still has a long way to go. Nowhere is this more apparent than in its steadfast determination to pursue an “indigenous innovation” campaign in proactively fostering domestic IP. The key feature of the campaign is the linking of government procurement preferences, where China’s WTO commitments remain flexible, to products whose IP is owned and originally trademarked in China. Other aspects include active support for Chinese technological standards that are bestowed to state-owned or state-backed enterprises, the formulation of “mega-projects” and increased research and development spending in targeted sectors, and the trading of domestic market access to foreign firms based on their willingness to share technology.

Faced with a pushback from foreign governments and business lobbies after the release of a Guidance Catalogue of Indigenous Innovation in late 2009, Chinese officials have made some mollifying changes in subsequent draft regulations. The outcome of the matter remains uncertain. Critics have been cautious over whether changes up to now have been genuine or simply cosmetic, likening the process to a game of “whack-a-mole” whereby a new manifestation of the indigenous innovation issue will pop up the moment an earlier one is seemingly addressed.

While these kinds of cases require careful calculation of how best to defend corporate and public interests, it has also become quite clear that the Canadian economy also suffers from weaknesses in its own systems of “indigenous innovation.” As the Jenkins report illustrated, “While Canada produces IP in abundance, it is less adept at reaping the commercial benefits; too many of the big ideas it generates wind up generating wealth for others.”

Might there be greater scope for collaboration between Chinese policymakers, who are now at the stage of taking IP more seriously, and seemingly indifferent Canadian policy-makers who need to take IP more seriously? With their penchant for planning, it is a solid bet that Chinese leaders have a good sense of what kind of IP assets they need and/ or would like to develop in industries of the future. Canadian leaders are thus at a crossroads: Should China’s policy ambitions be seen as an opportunity for partnership or as a threat that should be actively disarmed? Given Canada’s (and China’s) context, it would be pragmatic to try to selectively capitalize on China’s indigenous innovation campaign in efforts to address some of Canada’s structural weaknesses at the same time.

Such an approach is not without risk, but is ultimately the key in pivoting to China, Asia and international markets, more generally. This kind of shift in mind frame cannot be achieved overnight, but nor are such concepts completely alien to Canada, as implied in the blocked foreign takeovers of Potash Corp. in 2010 and MacDonald, Dettwiler and Associates Ltd. in 2008. What is lacking is a more coherent use of policy tools to (a) strategically guide the activity of privateand public-sector actors to generate pressure for upgrading and diversifying national production; and (b) ensure that a fair share of the benefits from these investments in knowledge, technology and value-added production flow to Canada.

How does one change the direction of a large oil tanker? In discussing lessons from Chinese central banking and how to shape or influence investor sentiments, David Daokui Li, former academic member of the People’s Bank of China Monetary Policy Committee, offered some free advice on the broader principles underlying a more coherent, if unconventional, approach to state intervention: “Steer early and steadily, while staying patient and not expecting instant response.”

Parts of this article are drawn from a recent NSI occasional paper, entitled “China’s Move up the Value Chain: Implications for Canada.”

Photo: LMspencer / Shutterstock.com