The short story of Budget 2012, the landmark of new majority government, is one of continuity. The structure of the federal economic house is well in order and the government has made a number of important moves to enhance productivity, competitiveness and resource development. But what of the Canadian framework as a whole? Having been billed in advance as a “transformational” budget that would give significant attention to preparing Canada for the demographic and socio-economic pressures on the horizon, where are we left as a country? Our role in this thematic on the 2012 federal budget is thus to focus on selected federal-provincial dimensions as they relate to the socio-economic and fiscal interfaces. Toward this end, attention will first be directed to the budget’s impact on the pension reform debate on the one hand and the income support and aging challenges on the other. In the second half we explore how the federal budget ought to expand its horizon to include some key aspects of the complex federal-provincial and interprovincial fiscal interactions, particularly in the area of health care and the recent renewal of the Canada Health Transfer (CHT).

Turning then to the pension issues, given the far-reaching debate that has taken place over the last year about Canada’s retirement income system and the various signals from the government in the lead-up, the reforms proposed in Budget 2012 to Canadian pensions and retirement benefits are mostly without surprise. As expected:

- The age of eligibility for Old Age Security (OAS) and General Income Supplement (GIS) will rise from 65 to 67 over the next decade and a half;

- Federal government pensions will be restructured to increase the share of contributions from employees as well as to raise the normal retirement age to 65 for new entrants.

One of the few surprises on pensions was the announcement of an actuarially adjusted deferral for OAS payments beginning in 2013. This will provide a marginal bonus to workers who continue to work past the basic eligibility age. This is similar to the current provisions of the Canada-Quebec Pension Plans although, unlike the pension plan, OAS will not offer a comparable penalty option for early retirement.

When we add to this list the introduction earlier this year of the Pooled Registered Pension Plan (PRPP) — a new voluntary pension plan announced by Ottawa to increase pension coverage in the private sector — we see a broad strategy across several pillars in the retirement income system. Whether these measures, as a package of reforms, appropriately address the long-term challenges of demographic change is a mixed story.

With regard to the changes to OAS/GIS, the government has framed its concern around two different but related issues: on one hand, a labour market need to mitigate the decline of the working-age population in the next several decades by extending retirement ages; and, on the other, by ensuring fiscal and intergenerational sustainability of the program, which is the largest single draw on general revenues.

On the first concern, it is somewhat curious that Ottawa would start a discussion with Canadians about the need to work longer through the vehicle of OAS/GIS. Although OAS/GIS is one of the few areas of exclusive federal jurisdiction in the area of retirement policy, it is not well suited to effect broad changes in labour-market behaviour. As Finance Minister Jim Flaherty has emphasized, OAS/GIS is not a contributory pension, it is a “social program” whose primary objective is to provide a basic income floor that protects Canadians from poverty in old age. For middle- and high-income Canadians who have a diverse source of retirement income, OAS/GIS is a not a significant trigger for retirement.

With regard to the changes to OAS/GIS, the government has framed its concern around two different but related issues: on one hand, a labour market need to mitigate the decline of the working-age population in the next several decades by extending retirement ages; and, on the other, by ensuring fiscal and intergenerational sustainability of the program, which is the largest single draw on general revenues.

More significant are the provisions for early retirement and the normal retirement age set out in contributory pension plans. The government would have been better placed to start here, using the upcoming CPP/QPP tri-annual review as an opportunity to begin looking at the linkages between the plan and other workplace pensions. Any changes necessary in OAS/GIS could then have followed once a comprehensive approach had been worked out with the provinces. This may still happen but it is imperative we consider all changes as part of the integrated whole that is the retirement income system.

With regard to the changes to OAS/GIS, the government has framed its concern around two different but related issues: on one hand, a labour market need to mitigate the decline of the working-age population in the next several decades by extending retirement ages; and, on the other, by ensuring fiscal and intergenerational sustainability of the program, which is the largest single draw on general revenues.

To the extent it is necessary to encourage Canadians to work longer (and there is certainly evidence Canadians are actively responding to a combination of financial pushes and labour market pulls to stay in the workforce longer), there are also huge differences in the retirement patterns across income groups, which any change in OAS/GIS should recognize.

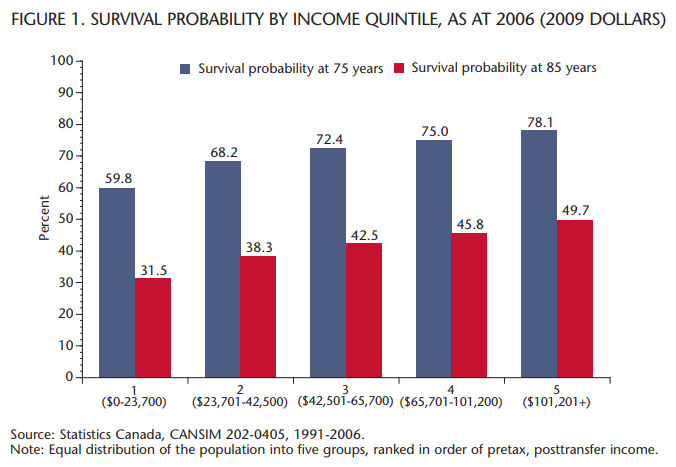

As shown in figure 1, the probability for survival beyond age 75 is only 60 percent for the bottom 20 percent of earners (1st income quintile), those who rely predominantly on OAS/GIS (and CPP/QPP where possible). This is a full 15 percentage points lower than the life expectancy for middle-income earners (in the 4th income quintile) who still receive a moderately clawedback OAS benefit. For the latter group, there are many other sources of income available to offset shifts in OAS/GIS, such as private savings and CPP/QPP, not to mention higher stocks of human capital, all of which make the transition potentially more adaptable than for people with lower-incomes.

Shifting the eligibility age of OAS/GIS to later in life will invariably affect those most in need. Writing in an op-ed for iPolitics (March 27, 2011), Michael Wolfson, former assistant chief statistician of Canada, estimated that if the age of eligibility were moved to 67 today, the poverty rate among seniors would double.

Given time and proper policy design, this problem is not unmanageable. Thanks to the resilience of the retirement income system overall, the actual number of seniors who would be pushed into the definition of poverty is small in absolute terms, approximately 70,000, Wolfson estimated in 2011. Furthermore, the timetable announced by the government provides 11 years before any change in eligibility is phased in. If necessary, governments can adapt various measures to help low-income Canadians make the transition. One way we suggest is to amend the deferral provision announced in the budget so that, like CPP/QPP, recipients could also take a benefit earlier than the normal eligibility age with a corresponding penalty. Ideally this would be made available as of 65, thus covering the gap as the normal eligibility age rises to 67. Because the benefit would be reduced on an actuarial basis by the difference between the age of eligibility election and the normal eligibility age, this would provide a flexible approach to easing low- and modest-income seniors through the announced changes without undercutting much of the savings already assumed.

Changing the clawback rules would also have been far more efficient for cutting costs in OAS/GIS while still protecting the eligibility of low-income groups and, by implication, mitigating any spillover to provincial and territorial social assistance. Others have also suggested the time is right to revisit the smart, but perennially unsuccessful, proposals of the Mulroney and Chrétien governments for a super seniors benefit. This would involve integrating all the major tax and income transfers targeting seniors (OAS, GIS, pension credits, GST credit, etc.) under the umbrella of a single, means-tested and fully indexed benefit. Not only would it help bring rationality to the first pillar of the retirement income system but, linked together, could serve as a powerful tool for affecting social policy and labour mobility.

This is to say we are in a time of major transition in our retirement income system, a process that won’t end simply with the changes to OAS/GIS in this budget. Indeed, what the system will look like in the next decade and beyond is still uncertain, perhaps more so now than only a few months ago. Before the eruption of the OAS/GIS question with the Prime Minister’s speech at the World Economic Forum in January, pension reform was moving on a single track with the implementation of the PRPP, a signature initiative of the Harper government that all finance ministers had endorsed in principle at the end of 2010. Then, in the shadow of OAS/GIS, the Ontario and Quebec provincial budgets in March announced major departures from the federal framework for PRPPs.

Ontario, placing its position on pension reform among a laundry list of policy disputes with Ottawa, expressed significant concern with the conceptual design of the PRPP and announced that its future collaboration on the pension plan will be closely tied to broader efforts to expand the CPP/QPP. Quebec, for its part, will proceed immediately with the PRPP, but with a number of material changes. Most importantly, its plan will be compulsory for all workplaces of five or more employees where registered savings vehicles are not currently offered. Employer contributions will still be voluntary. This decision to essentially legislate mandatory pension coverage, similar to models in other OECD countries, is precedent setting in Canada. We have yet to hear other provinces weigh in officially, but the moves by Canada’s two largest provinces unquestionably take us to a place in the policy debate where few expected to be.

We should remember that pension and retirement income policy are a unique construct of both concurrent jurisdiction and provincial paramountcy. Both levels of government are required participants but due to their regulatory role, the provinces hold a critical balance.

The inner workings of governmentWho’s doing what to get federal policy made. In The Functionary.The inner workings of governmentWho’s doing what to get federal policy made. In The Functionary.

The inner workings of governmentWho’s doing what to get federal policy made. In The Functionary.The inner workings of governmentWho’s doing what to get federal policy made. In The Functionary.

We should remember that pension and retirement income policy are a unique construct of both concurrent jurisdiction and provincial paramountcy. Both levels of government are required participants but due to their regulatory role, the provinces hold a critical balance. A certain measure of provincial and federal variation is thus to be expected, witness the QPP. Yet for most of the last half century, Canada’s retirement income system has proceeded on the basis of a high degree of harmonization and cooperation. Current turbulence is therefore worrying, particularly if it results in policy that is significantly different across jurisdictions. So far, this is where we are headed.

In a broader context one clearly gets a sense that the contours of the current pension debate are also significantly influenced by the state of intergovernmental relations more generally. This will take much longer to fix.

Since on the one hand it is hard to imagine a federal budget that has shed so little light on the provincial fiscal reality as does Budget 2012 and, on the other, it is also hard to imagine a provincial fiscal reality that is so complex and troublesome, an already noted major theme of this budget commentary is that the federal budget ought to embrace a much broader fiscal perspective in order to provide a more comprehensive and more balanced overview of Canada’s fiscal challenges and choices. In the extreme, the most important budgetary trade-offs may not be between, say, more money for the military or more tax cuts at the federal level nor between, say, more money for health care or more money for education at the provincial level. Rather, the key societal trade-offs may be interjurisdictional, e.g., between additional federal spending on the military or additional provincial spending on health care. While these examples are intended to be illustrative and not necessarily realistic, they nonetheless make the related points that Canadians need to have a more comprehensive overview of Canada’s fiscal landscape and that the federal budget document (or an accompanying annex) is the logical place to do this.

By way of advancing the case for this move in the direction of Ottawa adopting a national rather than only a federal fiscal perspective, the obvious launch point is a comparison of federal and provincial debt and deficits. For fiscal year 2011/12 the federal deficit is estimated to be $24.9 billion while the all province deficit (calculated from provincial budgets) was not far off at $23.6 billion. For the current fiscal year, the respective deficits are $21.1 billion and $19.0 billion (PEI is not included in this estimate due to the absence of future year projections). Drawing from the provincial budget projections for 2013/14, the all-province shortfall will be approximately $11.8 billion, while the federal deficit will be smaller, at $10.2 billion. Not only will the aggregate provincial fiscal deficits also exceed the federal deficit in 2014/15, but Ontario’s projected $10.7-billion deficit dwarfs Ottawa’s $1.3billion deficit.

On the net debt front, the worsening aggregate provincial fiscal situation is far more evident. In fiscal year 1989/90, the federal net debt level was three times as high as the all-province net debt — $360 billion vs. $124 billion. A decade later, the federal debt was 2.2 times the all-province debt ($564 billion vs. $256 billion). By 2012-13, the relevant budget projections indicate that the all-province net debt level will balloon to approximately $512.9 billion whereas Ottawa’s debt will come in at $602 billion, less than 1.2 times the provincial debt.

While both Ottawa and the provinces will face fiscal challenges as our population ages, the demands on the provincial public sector will arguably be considerably more difficult to handle. Along these lines, two federal policy initiatives merit attention. The first relates to the 2012 budget provision relating to OAS. In order to ameliorate the impact of an older population on OAS, as of 2029 the retirement age will be 67 rather than 65. In the same analysis by Michael Wolfson noted earlier, he also attempted to estimate the fiscal savings of this change if instituted in 2011. Wolfson’s simulations reveal that Ottawa’s saving would be in the order of $3.5 billion, while the loss to the provinces (largely from reduced tax revenues) would be roughly $500 million. This provincial loss does not include the costs to the provinces if these seniors were to resort to provincial social assistance. Note that these are annual, not once-and-for-all, savings.

The second policy initiative, arguably even more costly to the provinces, was the pre-budget announcement that the 6 percent CHT escalator will continue until 2016/17, after which the escalator will be the larger of the rate of increase in nominal GDP and 3 percent. In Renewing the Canada Health Transfer (January 19, 2012) the Parliamentary Budget Officer (PBO), Kevin Page, assessed the CHT alteration in terms of the fiscal implications for both Ottawa and the provinces. The PBO’s underlying assumptions are that on average the new CHT escalator will be 3.9 percent and that provincial health spending will increase, again on average, by 5.1 percent (i.e., this is slightly more conservative than the range estimated by David Dodge and Richard Dion in their 2011 C.D. Howe paper Chronic Health Care Spending Disease). In general terms, over the longer time horizon the PBO forecasts a falling net-debt-to-GDP ratio for Ottawa (and eventually a positive net asset position) whereas the all-province ratio will rise dramatically and unsustainably. In more detail, Page notes that over the longer term “provincial-territorial governments would need to raise revenue, reduce program spending or some combination of both (by $49 billion in 2011-12 and increasing over time in line with nominal GDP) to achieve fiscal sustainability” whereas “the federal government could reduce revenue, increase program spending or some combination of both (by $7 billion in 2011-12 and increasing over time in line with nominal GDP) while maintaining fiscal sustainability.”

To be sure, the provinces do have time to alter their health care parameters in order to accommodate the reduction in CHT growth. And in the spirit of the Conservatives’ “open federalism,” the Prime Minister has promised a hands-off stance with respect to the manner in which the provinces choose to bring their health care systems in line with the reduced CHT growth. Since both the OAS and CHT initiatives benefit Ottawa fiscally and have negative impacts on the provinces’ positions, they are but the latest version of the long but not so venerable tradition of non-negotiable federal downloading to the provinces, the most egregious exemplar of which was Paul Martin’s 1995 one-third slashing of the then Canada Health and Social Transfer. This serves to harken back to the Council of the Federation’s 2004 unanimous proposal for uploading pharmacare to Ottawa. The obvious rationale was the dire fiscal straits of the provinces (soon thereafter to be improved by Martin’s generous 10year deal, including the 6 percent CHT escalator) although a substantive policy rationale for uploading would be that since Ottawa controlled the patent legislation it also controlled the timing of the access to generics. In any event, Ottawa turned down the offer, no doubt influenced by the desire to avoid falling into the provincial dilemma of becoming saddled with expensive and open-ended spending programs.

The essential point here is that since policies relating to health care are iconic programs there ought to be much more in the way of information on how these budgetary initiatives will affect the country’s overall fiscal position in general as well as the likely impact on the policy areas in question.

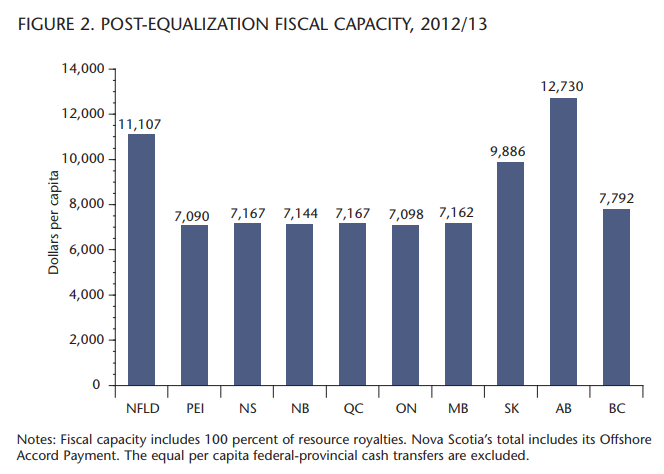

However, focusing only on the all-province fiscal aggregates masks the dramatic interprovincial fiscal inequities driven by energy royalties/ rents that in turn affect the ability of the individual provinces to deal with federal downloading. The extent of these provincial fiscal differentials is patently clear from figure 2. The provincial per capita totals are the sum of 1) fiscal capacity as defined by the equalization formula, with 50 percent of resource revenues entering the formula, 2) the per capita value of the other 50 percent of resource revenues, 3) the per capita value of equalization for the recipient provinces and 4) the Offshore Accord offset, which applies only to Nova Scotia. The unconstrained calculation of equalization totalled $18,556 billion.

However, the equalization cap limited equalization to $15,442 billion, so that after the requisite scaling downward the per capita values of equalization are Prince Edward Island ($2,378), Nova Scotia ($1,347), New Brunswick ($1,993), Quebec($943), Ontario($249), and Manitoba ($1,368). Excluded from figure 2 are the equal per capita values for the federal-provincial cash transfers (the Canada Health Transfer and the Canada Social Transfer). This would add roughly $1,200 per capita to each province’s total in the figure, but it would not affect the dollar differential across the provinces.

Not surprisingly, the three highest fiscal capacity provinces are those with high fossil energy royalties/rents — Alberta, Newfoundland and Saskatchewan. What is surprising, however, is that Alberta’s $12,730 fiscal capacity is over $5,600 or 80 percent higher per capita than is Ontario’s fiscal capacity (with similar fiscal differentials for the other equalization-receiving provinces). By way of an aside, most Canadians would likely also be surprised to note that Ontario is essentially tied with Prince Edward Island in having the lowest per capita fiscal capacity. And if one were to incorporate what it costs to provide public services (i.e., wages, rents, and the like across provinces) Ontario would hold down the bottom rank by a considerable margin. These caveats aside, the figure 2 degree of fiscal capacity disparity between the top four and the six recipient provinces will, if it persists, of necessity lead to either or both of superior public goods and tax havens in the resource-rich provinces. Indeed, Alberta currently falls in the tax haven category since it forgoes some of its $12,730 potential fiscal capacity because it has chosen not to levy a provincial sales tax.

Under s.36(2) of the Constitution Act, 1982, Ottawa is “committed to the principle of making equalization payments to ensure that provincial governments have sufficient revenues to provide reasonably comparable levels of public services at reasonably comparable levels of taxation.” So why not ramp up equalization to reduce the figure 2 interprovincial inequalities? Two reasons immediately suggest themselves. The first is that this would be prohibitively expensive because the equalizationreceiving provinces now account for 71 percent of the all-provinces population which, in turn, means that every addition a one-dollar increase in the equalization standard (stemming, for example, from a one-dollar increase in energy revenues) leads to a 71-cent increase in equalization. The second reason is that Ottawa cannot constitutionally tax the energy royalties, so that while the rents accruing to the energy provinces lead to an increase in equalization, Ottawa’s source of revenues to pay for this equalization increase comes from taxes that coincide more or less with provincial population shares. Phrased differently, with just under 40 percent of Canada’s population, Ontario residents would (via their federal taxes) end up paying roughly 40 percent of the additional equalization arising, say, from rising energy revenues.

A forthcoming IRPP publication (Courchene’s Policy Signposts in Postwar Canada) delves into more detail with respect to these interprovincial fiscal equity issues, both by way of highlighting related problems (e.g., that the energy-export revenues have led to the appreciation of the loonie that in turn has wrought havoc with manufacturing and led to the descent of Ontario into the have-not province category) and by elaborating on selected ways in which these fiscal equity issues might be ameliorated (e.g., revenue-testing the federal-provincial cash transfers and/or creating provincial sovereign wealth funds).

However, the message for present purposes is that these disparities have now reached a point where they have the distinct potential for undermining interprovincial as well as federal-provincial fiscal and political comity. If one adds to this that the thrust of Budget 2012 is clearly in the direction of endorsing a resource-based industrial strategy with the obvious likelihood of further rising energy revenues, then Ottawa can be faulted for not bringing these interprovincial fiscal inequities and their likely consequences to the attention of Canadians. This is yet another reason for Canada’s premier fiscal and policy document to move in the direction of becoming a national and not just a federal blueprint.

Photo: Shutterstock