Who’s really getting squeezed?

Paul Kershaw

Notwithstanding the national malaise about the slow performance of Canada’s economy since 2008, economic indicators show that Canada is more prosperous than ever before. Our economy is now more than twice as big as it was in 1976. After adjusting for inflation and population growth, it produces around $35,000 more per household than it did then.

Yet many of us don’t feel better off, which is contributing to what has become widespread talk of a “middle-class squeeze.” It is a powerful phrase that resonates with many Canadians and, to no one’s surprise, it has been grasped by those seeking political office as a useful mantra. But the focus on the middle class as an amorphous whole distracts attention from a more significant economic reality: it is mostly younger people in their mid-40s and under who are being squeezed out of the middle class. Meanwhile, the data show that the median Canadian age 55 and over (yes, the very middle of that older demographic) is doing better than the equivalent person did a generation ago as measured by income and wealth.

After adjusting for inflation, Statistics Canada data show that the typical 25-34-year-old working full-time is earning wages that are 11 percent (or about $3 an hour) lower than people of the same age did in 1976. By contrast, the median 55-64-year-old is making wages that are 3 percent higher than the same age bracket did in 1976. The trend is even better for the older demographic when we measure household income: those older households are earning incomes about 20 percent higher than their counterparts a generation ago.

Young people’s wages are losing ground, despite the fact that those under 45 are far more likely to have post-secondary education than their parents (they also have more student debt, because inflation-adjusted tuition is double what it was in 1976). As people cope, there has been a rise in dual-earner households. Yet after adjusting for inflation, two young people still bring home little more than what one breadwinner often did in the mid-1970s.

The result? The working generations under age 45 are being squeezed — squeezed for time at home, and squeezed for money, because they carry higher student debts and mortgages while earning lower wages. And when they choose to have kids, they are squeezed for child care services, which remain in short supply and often cost the equivalent of another mortgage.

No political party is advocating fixing this generational income inequality. Those politicians tripping over themselves to cater to a “beleaguered” middle class make little allowance for generational differences, in large part because older Canadians wield greater political clout. This demographic bulge votes in greater proportions than younger Canadians.

And it is better organized. Since 1985, Canadian seniors (later joined by baby boomers) have lobbied effectively for their demands and desires through CARP (originally an acronym for the Canadian Association of Retired Persons). CARP explicitly notes on its website that translating research about healthy aging into public policy is made easier by the “political clout” that comes from “bringing like-minded people together.” CARP has built a membership over 300,000 people strong and vows to “march to a million” members.

But while we applaud CARP for advocating on behalf of our mothers and grandmothers, someone also needs to ask who will advocate for the squeezed younger generations.

Building on the CARP model, the Generation Squeeze campaign is building an organization that speaks for younger Canada. The aim is not to work against the interests of our parents and grandparents, but to build equal generational power to which all political parties will respond with a better generational deal. Among the policy goals are safeguarding the foundations of medical care and Old Age Security for the aging population, while also adapting to the squeeze on the incomes, time and services available to those under 45.

Let’s look at the statistical basis of this generational gap. Income gains are just the tip of the iceberg when it comes to gauging the wealth of the average Canadian nearing retirement. Adjusted for inflation, average housing values of $383,000 have nearly doubled since 1976 ($203,000), leading to massive gains in personal wealth for those who entered the housing market a few decades ago. Statistics Canada data reveal that the median person age 55-64 enjoys household wealth that has risen by around 100 percent over to the previous generation.

But what’s been good for a generation phasing into retirement has been bad for their kids and grandchildren. The typical 25-34-year-old working full-time today will need to save for 10 years to put away the 20 percent down payment needed to buy a home in a school district with average house prices. That’s twice as long as it took the typical young worker a generation ago, even though today’s down payment often purchases a smaller yard, a condo or a suburban home that requires a longer commute.

Governments have been slow to recognize these gaps. The federal and provincial governments currently allocate around $45,000 a year per retiree on important programs like medical care and retirement income supports, compared with $12,000 per person under age 45 for school, medical care, post-secondary, employment insurance, family tax breaks, child care and parental leave.

We all know spending per retiree should be higher than spending for younger Canadians. It is a fact that we are more likely to require health care in our later decades, and Canadian values do not expect citizens to continually sell our labour throughout old age to make ends meet. High amounts of government spending on seniors are not the problem. The problem is the slow pace of adaptation for younger generations.

But the solution lies in replicating past decisions to increase social spending on retirees. In the mid-1970s, 30 percent of Canadian seniors were poor. We fixed that by championing and adapting a pension and medical system that was able to wrestle the low-income rate among seniors down to between 5 and 7 percent — a rate lower than for any other age group in the country. Because we now spend around $50 billion more per year on medical care than in 1976 (when measured as a share of GDP), and another $30 billion on Old Age Security and the Canada/Quebec Pension Plans, my 98-year-old grandmother is not poor today; and my parents, in-laws, aunts and uncles have a far reduced risk of economic insecurity compared with the generation that retired before them. We must sustain these achievements.

But is also time to adapt social policies to meet the challenge of younger generations facing deep declines in their standard of living. Although we are not likely to reverse the fact that younger Canadians now earn many thousands of dollars less per year and pay housing prices that are hundreds of thousands of dollars more, there are policy solutions by which we could mitigate these trends.

Family policy is a prime mechanism to address the issues behind the squeeze. Better benefits for new moms and new dads would ensure that it doesn’t cost younger generations the equivalent of a second mortgage in lost income when parents share 18 months at home with a new baby. Ten-dollar-a-day child care would mean parents would not have to pay the equivalent of another mortgage to allow both partners or lone parents to work.

Such changes would save one-earner, two-earner and single-parent families tens of thousands of dollars before their children reach age six, with which they could pay down the average student debt, reduce by years the time it takes to save a down payment or pay off a mortgage. Or this money could simply make it easier to deal with rent, benefit from the power of compound interest to save for retirement and afford slightly more work-life balance. Indeed, since the federal government added to the time squeeze for younger generations in 2012 by adding two more years of work before they are eligible for Old Age Security (qualifying at age 67, not 65), we should consider changes to employment practices that would free workers to have an extra few hours a week at home each year before they retire.

Paying for these policy changes would not require a dramatic change in the generational spending gap outlined above. In fact, we could pay for these three changes by increasing the annual public allocation currently made per Canadian under the age of 45 from $12,000 to $13,000 — a mere extra $1,000 per year — and target this pooled investment to the expensive moment in people’s lives when they start their homes, jobs and families. All the while, we could retain annual spending per retiree around where it is now, at $45,000, to safeguard the medical care and retirement income support our aging family members expect.

We can pay for this investment in younger Canada either by reallocating existing expenditures (e.g., reduce less-efficient social spending, subsidies to industry and unnecessary tax expenditures) and/or by rolling back some of the tax cuts of the last decade. (Total government revenue fell five percentage points of GDP between 2000 and 2010, which represents a drop of around $80 billion in annual revenue.)

The only other option is the status quo — which is a bad deal for younger generations.

It is time for politicians and policy-makers to stop ignoring intergenerational discrepancies within the middle class. The very housing trends that have driven up wealth for the median person in the older demographic mean millions of young Canadians face an economy that makes it harder to buy a first house, harder to spend time at home as their parents did and harder to save for a retirement that may not come with the same guarantees enjoyed today. We need social investments to address this generational gap. We need boomers and seniors to get on board for a better deal for their kids and grandchildren.

And, most of all, we need younger Canadians to recognize that political parties of all stripes respond to those who organize. If we build for ourselves an organization with political and market clout that matches CARP, governments are much more likely to adapt policies to address the pressing challenges of our generations with the same conviction they now devote to our parents and grandparents.

§§§

Would you want to be in your mother’s shoes?

Tammy Schirle

I’ve met many people determined to convince me that their generation got a raw deal. They will pick and choose statistics to make their point, and every counterpoint is met with a “Yeah, but…” Ask who is better off — early boomers (born between 1946 and 1955) or some of Generation X (born 1971-80) — and the conversation starts to sound like a typical argument between teenagers and their parents. Neither understands the efforts and trials of the other. But it also raises the interesting matter of how to evaluate intergenerational inequities in well-being. And for that, we need to put the facts in context.

We could begin by comparing the financial well-being of boomers and youth. For example, in 2012, families under age 35 had a net worth of only $25,300, while those aged 55 to 64 had a net worth of over half a million dollars. Yet that discrepancy simply reflects the time it takes to accumulate assets over one’s lifetime. We could compare public spending on individuals. Provincial health expenditures on the average man aged 60-64 was $4,591, while expenditures on the average 25-29-year-old man were only $2,076. However, this merely reflects a deterioration in health with age in the context of a universal health care system (the average 90-year-old man costs over $26,000!). Such contemporaneous differences are not informative for judging the lot of different generations.

To evaluate well-being across generations, we need to compare apples with apples — realistically, an impossible task. Appropriate comparisons would need to see what happens to each generation over their entire life cycle — from infancy to death — and try to derive an all-encompassing measure of lifetime well-being. We simply don’t have the data to do that. And even if we could collect the data, we’d have to wait until today’s youth die before we could reach a conclusion about which generation enjoyed a better life.

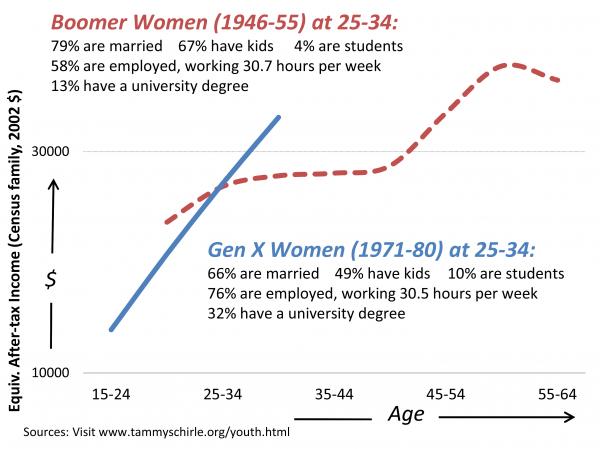

The best we can do is compare well-being at similar points in the life cycle, while appreciating the full context for judging well-being. I tend to think about most aspects of individual well-being in terms of three interrelated dimensions: family, work and leisure. I also tend to think about women in each generation. It’s among women that we can see some interesting similarities and also remarkable contrasts. Let’s consider the early boomer women and those from Generation X. The best available data allow us a chance to compare them between the ages of 25 and 34.

What do those data tell us? When they were between 25 and 34, most early boomer women were married (79 percent) and had kids (67 percent). The typical early boomer woman gave birth to her first child around age 24. A large portion were employed at ages 25-34 (58 percent). On average those who worked did so for 30.7 hours per week. Only 13 percent had a university degree at this age. If working full-time, they could expect to be paid a wage rate 75-80 percent of what men aged 25-34 received.

The women in Gen X were less likely married (66 percent) or mothers (49 percent) when they were between ages 25 and 34. Typically, Gen X women had their first child around age 27-28. They were more likely to work at ages 25-34 (76 percent), and on average they worked 30.5 hours per week.

The averages mask an interesting trend, however. In Gen X, a higher percentage of women worked part time than did boomers. And a higher percentage also worked 40 hours or more per week. Almost a third of Gen X women had a university degree at ages 25-34. And those who worked full-time were paid at a wage rate that was 90 percent of what men aged 25-34 received.

Between the ages of 25 and 34, the resources flowing in to support the household were remarkably similar across the two generations. The average after-tax income (adjusted to account for family size and to 2002 prices to account for inflation) of an early boomer family whose oldest member was aged 25-34 was just under $27,000, and the income for a Gen X family was just over $27,000.

In contrast to women in their generation, Gen X men aged 25-34 were less likely to be employed full-time than their early boomer counterparts. But the Gen X household had a lower after-tax income at earlier ages, and had much higher incomes than boomers when in their 30s. While only the crystal ball can tell us what their future holds, there are many reasons to expect the lifetime income of Gen X households will far exceed that of the boomers. The main reason is the higher level of education for men and women, and women’s greater attachment to the labour force.

The rest of the story is our interpretation of the data. I look at Generation X women and see a group that invested in themselves when relatively young, going to school and starting careers before establishing their families. It’s a costly investment of time and money, but they expect their lifetime earnings to be much higher than those of their mothers, with smaller penalties for job interruptions. Choices to delay parenthood and marriage appear to result in better relationships: divorce rates have been on the decline in Canada. Overall, I would argue that a measure of the generational gap that considers one’s entire life cycle will clearly demonstrate women in Generation X are much better off than the boomers.

Of course my interpretation of the data reveals my personal experience and bias.

My mother was presented with few opportunities in her youth. With the expectation that she marry young, have several children and stay home to raise them, there was little reason for her to pursue higher education. As a single mom with no support later in life, with no work experience and little education behind her, moving forward in the labour market was tough. Her male counterparts with similar education and skills could find jobs with high enough wages to support a family; she could not. She struggled to balance training, work and kids for many years, eventually settling into a stable career path. By the time she could afford to contribute to retirement savings, she felt it was a lost cause.

I think of myself, growing up knowing that a university education — in a male-dominated field — was an option, and I was encouraged to pursue whatever option appealed to me. Certainly, I maxed out the student loans (and did my share of complaining in my pre-Millennium Scholarship days), but they were quickly paid off when school was done, and I now reap a great return on that investment. I postponed marriage and children until I knew I had a solid foundation to support an independent life.

I struggle to balance work and family in ways my mom never imagined — she didn’t have to worry about breastfeeding in her office or making it to work without peanut butter fingerprints on her pants.

But my husband and I (combined) enjoyed a full year at home with our infant child with full job protection and generous benefits that my mother could not imagine. (Nor could she imagine a husband taking the role of primary caregiver to an infant!) Quality child care is expensive, but it’s only for a couple of years, and the price is not high enough that I’d give up my career or my chance to be a mom. There are many things about my life that might seem harder than my mom’s, but when I look at the big picture, I would not dream of trading places with her.

Perhaps other women come at this with a different image in mind. Many stay-at-home moms in the 1970s and ’80s would not have wanted anything else, even if it brought more money into the household. They focused on their contribution to the household’s well–being, offering quality child care and organizing the family’s affairs. They may have spent many hours volunteering their time outside the home. The cost to their careers was viewed as a small price to pay. They may have gradually moved into the labour force to supplement the family income, even going back to school, as the family grew older.

Their daughters of today may be feeling pressured — socially or -financially — to go to school and define careers when they would rather follow in their mothers’ footsteps. Investments, particularly in housing, seem overwhelming. Several years of child care and inflexible work schedules seem an insurmountable problem. They sometimes hunger for the simpler lives they see their mothers had.

The point is that different perceptions of well-being make it impossible to conclude in any definitive way that one generation as a whole was better or worse off than the next. Things are not harder or easier. It is simply different.

An agenda that tries to arouse generational conflict misses the hard social problems that have nothing to do with anyone’s measure of a generational gap. We have small pockets of seniors living in dire poverty and need to find the best policies to help them. A nation that values opportunity and freedom to choose a path for oneself must find a route to ensuring all young people have access to education and training. Concern that many people aren’t saving enough for their retirement, even when they are able to do so, must translate into steps that help them save. These concerns can straddle generations. It’s where our focus should be.

Photo: Shutterstock