Without a doubt, we are currently living in the most challenging economic times since the Great Depression of the 1930s. Governments and central banks around the world are taking aggressive and, in many cases, unprecedented steps to stimulate our national economies in a way that they hope will reverse the negative impacts created by the global financial crisis and put countries on the road to positive and sustainable economic growth.

Beyond the broader macroeconomic picture, how are Canada’s small and medium-sized enterprises (SMEs) – those companies that represent over 99 percent of Canada’s enterprise base — responding to these tumultuous times? In the news, we are accustomed to hearing about the ebbs and flows of our industrial giants, such as AbitibiBowater, Air Canada, Bombardier, General Motors, Nortel, RBC and Suncor Energy, among others, but what about this next tier of companies?

Canadian SMEs are critical to Canada’s economic prosperity. When discussing this economic subsector, though, we need to go beyond the one-size-fits all approach, particularly as it pertains to those companies that are active in international business. Based on our separate research and consulting work in the Canadian SME community over the past 15 years, we have identified six distinct types of SMEs that engage in trade. In this article we will outline the six types and propose strategies for them to stay competitive on the international front during and after the recession that the Bank of Canada now says ended in the second quarter.

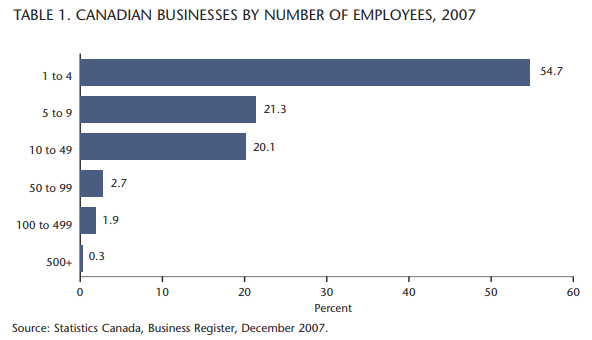

SMEs are an integral part of the industrial fabric of Canada. Of the approximately 1.1 million employer businesses that exist in our country, 97.8 percent are small enterprises (fewer than 100 employees), 1.9 percent are medium-sized enterprises (100 to 499 employees), and the remaining 0.3 percent are large enterprises (500 or more employees; see table 1).

Their contribution to Canada’s economic prosperity is also significant. The following list highlights a number of the more noteworthy facts:

- On average, small businesses that have fewer than 50 employees contribute about 23 percent to Canada’s gross domestic product (GDP).

- As of 2007, SMEs employed approximately 7 million individuals in Canada, or 64 percent of the total labour force in the private sector.

- Small businesses created approximately 100,000 jobs in 2007, accounting for over 40 percent of all jobs created in Canada.

- In 2003 (the latest year for which Industry Canada has published this particular information), SMEs accounted for $5.3 billion of the total $13.4 billion (39.5 percent) spent on scientific research and experimental development in Canada.

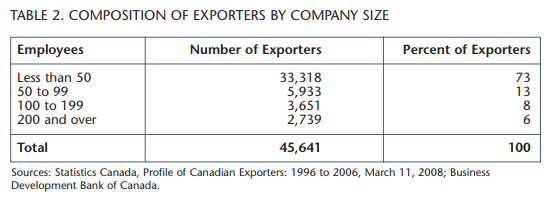

On the international trade front, Canadian SMEs are active, but the impact of their exporting activities on Canada’s economic performance is relatively minor — as compared to large enterprises. In 2006, for example, the largest 4 percent of exporting establishments accounted for 84 percent of the total value of merchandise exports. Those exporting less than $1 million per year represented 72 percent of all establishments, but only 1.5 percent of the total value.

However, these statistics do not tell the whole story. In its 2004 Report on Trade, the Canadian Federation of Independent Business stated that 51 percent of Canadian SMEs engage in trade — either directly through exports or imports (36 percent), or as part of a supply chain that helps other business contribute to Canada’s trade activities (15 percent).

As the forces of globalization take even deeper root in Canada, and as our industrial base of predominantly small and medium-sized enterprises respond to the challenges of an increasingly integrated and competitive economic environment, the number of SMEs active in international commerce — either directly or indirectly — will undoubtedly rise.

As the forces of globalization take even deeper root in Canada, and as our industrial base of predominantly small and medium-sized enterprises responds to the challenges of an increasingly integrated and competitive economic environment, the number of SMEs active in international commerce — either directly or indirectly — will undoubtedly rise. Given this situation, we believe that it is important for government and industry to go beyond the traditional grouping of SMEs as a homogeneous group and segment them along lines that reflect their distinctive roles and positions in Canada’s international trade system. Not only will this lead to the development of government policies that will better respond to the unique nature and challenges of our trading SMEs, but commercial plans and strategies can be developed by, or for, senior managers of these enterprises that will enable them to more effectively compete in the global economy.

- SMEs that are an intimate part of the value chain of a flagship multinational enterprise (MNE). Firms that supply Bombardier, CAE, Nortel or other large Canadian MNEs face an ongoing dispersion of the MNE’s value chain to various countries around the world. For example, on May 29, 2008, Bombardier announced that its facility in Querétaro, Mexico, will manufacture the composite structure for its all new Learjet 85 business jet. The Querétaro site will also manufacture the electrical harness and perform subassembly systems installation. Those Canadian-based suppliers of Bombardier that have been vendors of materials for the composite structure, or parts for the electrical harnesses of previous Learjet programs, must now take the necessary steps to establish themselves as approved vendors in Mexico — assuming the Canadian suppliers want to grow with Bombardier. Initially, a particular Canadian supplier, given its experience with Bombardier Aerospace and technological advantage over Querétaro-based vendors (depending on the product class), may be able export product directly to Mexico, but as the depth and capabilities of

Bombardier’s supplier base in Querétaro improves, the Canadian vendor will have to think about establishing a manufacturing/ supply base in Mexico. Bottom line, as our Canadian champions, like Bombardier, direct their manufacturing operations to markets across the globe to enable them to be more competitive, Bombardier’s Canadian-based suppliers need to adopt a global mindset if they hope to remain an integral part of this MNE’s supply chain.

Research interviews with hundreds of executives in SMEs and MNEs by Karl Moore have revealed the importance of linking with Rugman and D’Cruz’s concept of flagship firms (Multinationals as Flagship Firms, Alan M. Rugman and Joseph R. D’Cruz, Oxford University Press, 2000). They suggest a Five Partners Model of business networks forming around a flagship multinational. Rugman and D’Cruz’s system has two key features: the presence of a flagship firm, which pulls the network together and provides leadership for the strategic management of the network as a whole; and secondly, the existence of firms that have established key relationships with the flagship.

The Five Partners Model of a business network encourages economic exchange among partner organizations through co-operative, non-equity relationships. Specifically, the partners are a leading “flagship firm,” which is an MNE; key suppliers; key customers; select competitors; and the non-business infrastructure (NBI). The NBI comprises government, non-traded service sectors, educational institutions, social services, trade unions, trade associations and non-profit cultural organizations, providing highly diversified perspectives to the firm. The business network’s governance structure depends upon (1) asymmetric control of the network’s strategic purpose by the flagship firm and (2) structuring aspects of the partners’ business systems (value chains) to create a network business system.

The key implication of Rugman and D’Cruz’s model is to carefully consider the SME’s alignment with key MNEs. Becoming a supplier to a flagship firm creates a potential for SMEs to supply globally, in some cases leading to foreign subsidiary opportunities.

Canadian media may question Bombardier’s plan to manufacture the composite structure and electrical harness for its Learjet 85 business jet in Querétaro versus Quebec or Ontario, but Bombardier is — as the company puts it — a global transportation company with a presence in more than 60 countries around the world. To remain competitive in the aerospace industry, it must organize its manufacturing portfolio in such a way that allows it to effectively respond to international competitors, a global customer base and the multiple demands (governments, unions, employees and suppliers) of the countries in which it has have physical operations.

In the 2008-09 economic downturn, the news is filled with examples of large industrial enterprises scaling back production or laying off workers in response to tepid demand conditions. In this context, SMEs must be particularly sensitive to the operating dynamics of their MNE clients and be ready to offer them supply solutions – in Canada and abroad — that will enable MNE — to reduce costs and effectively weather the economic storm. In this case, the SME’s economic well-being is completely tied to the economic health of its larger and geographically dispersed buyer.

- SMEs that are the canadian subsidiaries of foreign MNEs. This group of Canadian SMEs generally does not generate a great deal of attention in government of industry circles — perhaps because they are not perceived as “truly Canadian.” We feel that this can often be a mistake. While many of these subsidiaries are primarily sales and service arms of foreign MNEs, they also have the potential to earn international or global subsidiary mandates, or responsibilities that would allow them to add significant numbers of interesting and challenging jobs to Canada’s economy.

Karl Moore, in collaboration with Julian Birkinshaw of London Business School, has carried out research on how subsidiaries earn these mandates. Their findings tell us that a larger number of subsidiaries could expand their contributions along various elements of the MNE’s value chain. The good news is that for most industries, Canadian companies would rank among the top 10 or so national subsidiaries that are typically on the short list of subsidiaries to be considered for devolved international responsibilities. It is a limited set of subsidiaries to choose from because of the need for world-class capabilities, sophisticated infrastructure and a familiarity with leading — edge products and customers when choosing where to locate MNE activities.

In order to understand this phenomenon a broader perspective helps demonstrate the evolutionary path for many global MNEs. What is the number one advantage of being a global firm? Ten years ago economies of scale and scope may have been the answer. Today, it is increasingly clear that the top advantage is the ability to harness learning and innovation throughout the worldwide network of the global multinational. Therefore, the critical question becomes how to harness this potential capability.

Research interviews with several hundred executives of large MNEs in Europe, North America and Japan suggest it is by lead subsidiaries, which capture international or global responsibilities in MNEs.

In the 1980s and into the 1990s, holding a watching brief may have been sufficient participation in one of the three regions as long as you had considerable activities in the other two. Today, leading firms need to harness capabilities in the other two non-home regions. For example, it would be naive to suggest that Finland is the only country claiming mobile phone innovation. Other leading countries active in this industry include Sweden, home of Nokia’s rival Ericsson; the US, wit industry giant Motorola; and South Korea, with Samsung. People no longer search for innovative ideas in one place. Today, multinationals must be quick to adopt new ideas from Europe, North America and Asia, because these are the key areas for innovation and R&D.

Upward mobility means transferring to the head office, and naturally, not everyone wants to move with their families to New Jersey, expensive London or faraway Tokyo. All in all, this centralizing aspect of a global strategy means considerable losses for lead subsidiaries.

In the last 20 years, adopting a global strategy meant centralizing decision making in the home country of the MNE. This development may be a natural outgrowth of a global strategy. However, it often has a dysfunctional impact on the lead subsidiaries. Under this approach, the interesting and strategic parts of the decision-making process are taken away and made elsewhere. This reduces the subsidiary’s role to one of implementer — clearly less exciting and less strategic. The result: fewer higher-income positions and a generally de-motivated senior staff. Also, it becomes more difficult to recruit clever and ambitious young people from their country, as one can only rise so far in the subsidiary. Upward mobility means transferring to the head office, and naturally, not everyone wants to move with their families to New Jersey, expensive London or faraway Tokyo. All in all, this centralizing aspect of a global strategy means considerable losses for lead subsidiaries.

Over the past few years, we have seen a more positive side of this trend. Multinationals are increasingly questioning why adopting a global strategy requires global activities to move to only the home country. The seemingly obvious yet critical idea: centralizing aspects of your global activities not only in the home country but, for some aspects of global strategies, whether product management, manufacturing or R&D or marketing, in lead subsidiaries. This idea has been labelled “decentralized centralization.” From a head office perspective, this means harnessing multiple points of innovation in all three regions of the Triad (North America, Western Europe and Asia), creating a net increase in the overall innovativeness of the MNE’s global network. From the subsidiary CEOs’ viewpoint, this allows them and their managers to be involved in global strategic decisions and execution beyond their national borders. The result: more jobs and highly paid positions, and a better environment in which to recruit and retain the best and brightest.

The challenge for Canadian subsidiaries is clear: ensure your place as a lead subsidiary capable of international responsibilities, be it in R&D, manufacturing, marketing or customer support. Many subsidiaries have managed this.

We and colleagues have conducted interviews with leading Canadian and European subsidiaries for over a decade on this topic. This research suggests that many Canadian and European subsidiaries can successfully compete for broader responsibilities within the network of their parent firm. Lead subsidiaries, especially those operating in the Triad, usually have earned their roles rather than been given them by an authoritarian head office. CEOs of lead foreign subsidiaries have a special role to play in transforming their subsidiaries into more than mere sales and service outlets. Specifically, they can lead the development of world-class business capabilities that position their subsidiary to win broader regional responsibilities for achieving corporate goals. Therefore, a subsidiary’s capability could be its skill in developing and manufacturing a product line. For example, Pratt and Whitney Canada manages a critical line of engines for P&W worldwide. Likewise, Panasonic in Spain handles key aspects of pan-European strategy.

The research shows that foreign operations build their stature in the global corporate network by working diligently to establish world-class capabilities, and by communicating those competencies to the head office and other lead subsidiaries.

One of our most important findings was that the senior team of the subsidiary, especially the lead subsidiary CEO, was central to a subsidiary winning international mandates. Thus, it is critical for Canada’s economy to encourage CEO’s and their teams to aggressively pursue international responsibilities so that this networking continues to grow.

From the perspective of SMEs, this is a variation on the theme of flagship firms, except that this phenomenon is potentially more advantageous. The key challenge for the SME in this case, as with flagship firms, is to develop supplier relationships with MNEs that hold international or global mandates. There are two critical differences between Canadian subsidiaries and flagships firms, though.

Firstly, flagship firms are more apt to understand their affiliation with MNEs as a monogamous relationship with a certain degree of loyalty, whereas with Canadian subsidiaries, this is not as important. Secondly, there are many more Canadian subsidiaries that are or could be lead subsidiaries than there are Canadian MNEs that could play the role of a flagship firm.

- SMEs that have gradually gone global These SMEs follow the more traditional model of firms that go international over a number of years. The more recent trend is those firms that are increasingly international as well as adopting a global strategy. This is new, and exciting. When does SME have a global, as opposed to an international, strategy? There are no hard and fast rules. International business researchers have suggested various criteria. For instance Alan Rugman and Karl Moore have proposed having a minimum level of sales in all three parts of the Triad; others have argued for other measures. Academic debate aside, more Canadian SMEs have moved on from the past and gone global.

A central concern for these firms is establishing global routes to market or channels of distribution. One firm that has done this is the Trudeau Corporation, a designer and marketer of kitchenwares located on Montreal’s South Shore. With only 170 employees, the vast majority in Canada, Trudeau sells in 40 countries around the world. To accomplish this distribution Trudeau has set up three managers in Europe and one in China to establish relationships with distributors in those important markets.

There are many more Canadian subsidiaries that are or could be lead subsidiaries than there are Canadian MNEs that could play the role of a flagship firm.

Like other Canadian SMEs that are expanding into international markets, Trudeau has taken a number of years to establish a global presence. In a recession, the path to commercial success is, without a doubt, longer and more complex, but that in no way should deter these companies from their international efforts. In fact, when SMEs are facing a soft domestic market, we believe that they should proactively pursue commercial opportunities outside of Canada to better facilitate sales growth.

- SMEs that are going global from conception. Some of the most intriguing and certainly ambitious of SMEs are those that are going global from conception. Typically, this occurs in technology-based industries where shortened life cycles, high R&D costs and sheer opportunity drive firms to take this approach. However, nonhigh tech firms are also considering this strategy. For example, Hexago is a technology-based firm and global provider of network products. A sample list of its customers includes Korea Telecom, Chunghwa Telecom, NTT, France Telecom, AT&T, KDDI, WIDE Project, T-Systems, Teleglobe, Cyberport, Spawar, the US Department of Defense’s Defense Information Systems Agency (DISA), the US Air force, General Dynamics, BAE, CERDEC-Army, Boeing, Panasonic, NEC, Surfnet, Ukerna, AARNet and Renater — an impressive set of global customers. Established in 2002, presently Hexago has just over 50 employees, the bulk of whom are in Canada, while key sales and marketing staff reside in China, Korea, India, Hong Kong and Malaysia. At the outset, the founders of Hexago saw themselves as competing on a global basis and did not adopt a careful, slow internationalization process — more conventional for SMEs’ early phases.

For this group of SMEs, there is an overriding need for founders with the heart of a lion, ambition and drive, as well as parallel support from the Canadian government to help with financing and the building of global connections.

- SMEs with an exclusive or dominantly North American strategy. Alan Rugman of Indiana University has written a great deal about the about the importance of region. Two of his books, The End of Globalization (AMACOM; 1st edition, 2001) and The Regional Multinationals (Cambridge, 2005), have had considerable impact. In an article in Strategy and Business, Rugman and Moore argue, “Much of the rhetoric around globalization is out of sync with reality and multinational executives would do well to avoid its siren call. The action has always been regional, and will remain so…We focused a recent research study on the activities of the Fortune Global 500.” It is widely accepted that a relatively small set of multinational enterprises account for most of the world’s trade and investment. Indeed, the largest 500 MNEs account for over 90 percent of the world’s stock of foreign direct investment and they themselves conduct about half the world’s trade. Their importance is paramount; where they lead, so goes the world. But some of the results were surprising. The 500 MNEs are not “global” businesses, in the sense of having a broad and deep penetration of foreign markets across the world. Instead, most of them have the vast majority of their sales within their home triad of North America, the European Union, or the Japanese market in Asia. The activities of these firms tell us the Triad economies are still paramount. Region is where the action is at. As our research demonstrates, very few large MNEs are truly global. Consequently, a regional focus may be more appropriate for smaller SMEs.

Three of Canada’s leading men’s suit manufacturers, Jack Victor, Peerless and Samuelsohn, have adopted a strong regional focus strategy by centring the majority of their value chain in North America. The Canadian industry faces tough competition from China and other Asian suit-producing nations, although Canadian businesses can use the physical and cultural proximity to the US as leverage. While it can take weeks to have a suit made and shipped from Asia, these firms can have suits delivered to US retailers often on a nextday basis. Also, Canadian manufacturers have a deep insight into the American men’s suit market and are able to produce products which are highly successful in the US. Though Peerless does some manufacturing in Asia, all three have retained the bulk of their production in Canada, and perhaps more importantly have kept their critical design, marketing and sales activities in Canada.

- Family owned and operated SMEs. Canadian family businesses are a significant part of Canada’s SME population. A large number of Canadian family-owned firms will be undergoing a generational change in ownership and operation. Our five previous categories would certainly include some family-owned SMEs but we chose to put them in their own category because of some unique challenges they face. According to “The First Success Readiness Survey of Canadian Family-Owned Businesses,” by the Deloitte & Touche Centre for Tax Education and Research at the University of Waterloo, an estimated 27 percent of Canada’s family business leaders will retire in the next five years, another 29 percent in six to 10 years, and an additional 22 percent in 11 to 15 years.

Many of these firms were started decades ago by boomers who are now entering their late 50s and early 60s. Many are actively looking for successors outside their own immediate families.

Research suggests that Canadian family business owners are more apt than their US counterparts to “cash out” of their businesses as they approach retirement age rather than hand the business over to one of their children. Boomers are looking to impart their business to an ambitious younger person in their 30s or 40s, someone with a decade or more of business experience yet with the energy, determination, ambition and need to achieve more typical among those in a younger age group. We believe that as this generational handover occurs, these younger people will be quite open to international expansion. This is a specific group that the Canadian government should target. A number of business schools across the country have opened or will be shortly opening centres for family businesses. We encourage the government to consider working with these family business centres to develop programs that target these firms and their potential for international business.

Traditionally, most financial institutions and government policies have regarded SMEs as a homogenous group. We have outlined six types of SMEs and briefly suggested their parts to play in Canada’s globalization efforts. We think it is important to segment SMEs because at times they adopt quite different strategies on their path to going international and are best helped by support that is tailored for their needs. Beyond government and other support, we have also suggested ways that senior management of these SMEs can effectively exploit their strengths as they go global, even in the toughest of economic times.

Photo: Shawn Goldberg / Shutterstock