Last week’s federal budget showed deficits with no promised date to eliminate them. In response, several analysts warned that we might be headed down a dangerous path that could eventually spiral into a fiscal crisis like the one Canada experienced in the mid-1990s (e.g., see here, here, here and here). Kevin Milligan argues that such comparisons are premature:

“The 2016 budget does not put us on the road to 1995. We are not on the road. We are not in the car. We have not even put on our shoes, had breakfast, or gotten out of bed. In order to make the 1995 crisis happen again, we would need to see sustained deficits on the order of $100 billion for a decade. If deficits approach those levels, I will have my debt-crisis bomb decorations ready for my future Maclean’s posts.”

And his post includes some scenarios to support his point. I agree with Milligan and will present a different perspective. Inspired by Jason Kirby’s comparisons to old budgets, let’s see what we can learn from the prevailing economic thinking of those in mid-1990s who faced a fiscal crisis.

Over two decades ago, a new Liberal government came to power offering a New Framework for Economic Policy. That document contains a key fiscal policy insight that still applies today: what matters for fiscal sustainability isn’t only the rate of interest or economic growth viewed in isolation, it’s the difference between these two factors, and the current level of debt.

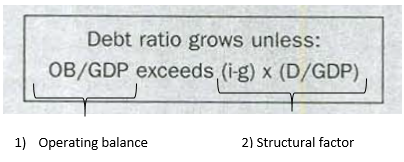

These factors must be considered together, and that document provides an equation to do so, which has two parts:

This says that the debt-to-GDP ratio will rise unless the government’s operating balance (as a share of GDP, OB/GDP, which is the difference between government revenue and program spending) is greater than a second composite term, which that document called a “structural factor”. This factor is equal to the effective interest rate on government debt minus the growth rate of nominal GDP (i-g) multiplied by the current debt ratio (D/GDP).

This equation provides a useful way to understand fiscal sustainability. As that 1994 document showed, during the late 1940s through to the 1970s, economic growth greatly exceeded the interest rate on government borrowing. This acted as a strong fiscal tailwind that naturally reduced the debt-ratio.

Things changed for the worse in the 1980s and 1990s. Interest rates spiked above economic growth rates — causing this fiscal tailwind to become a headwind — and the debt ratio rose steadily. Once those negative debt dynamics took hold they were hard to reverse. That’s why the federal and several provincial governments needed to undertake significant fiscal consolidations in the 1990s.

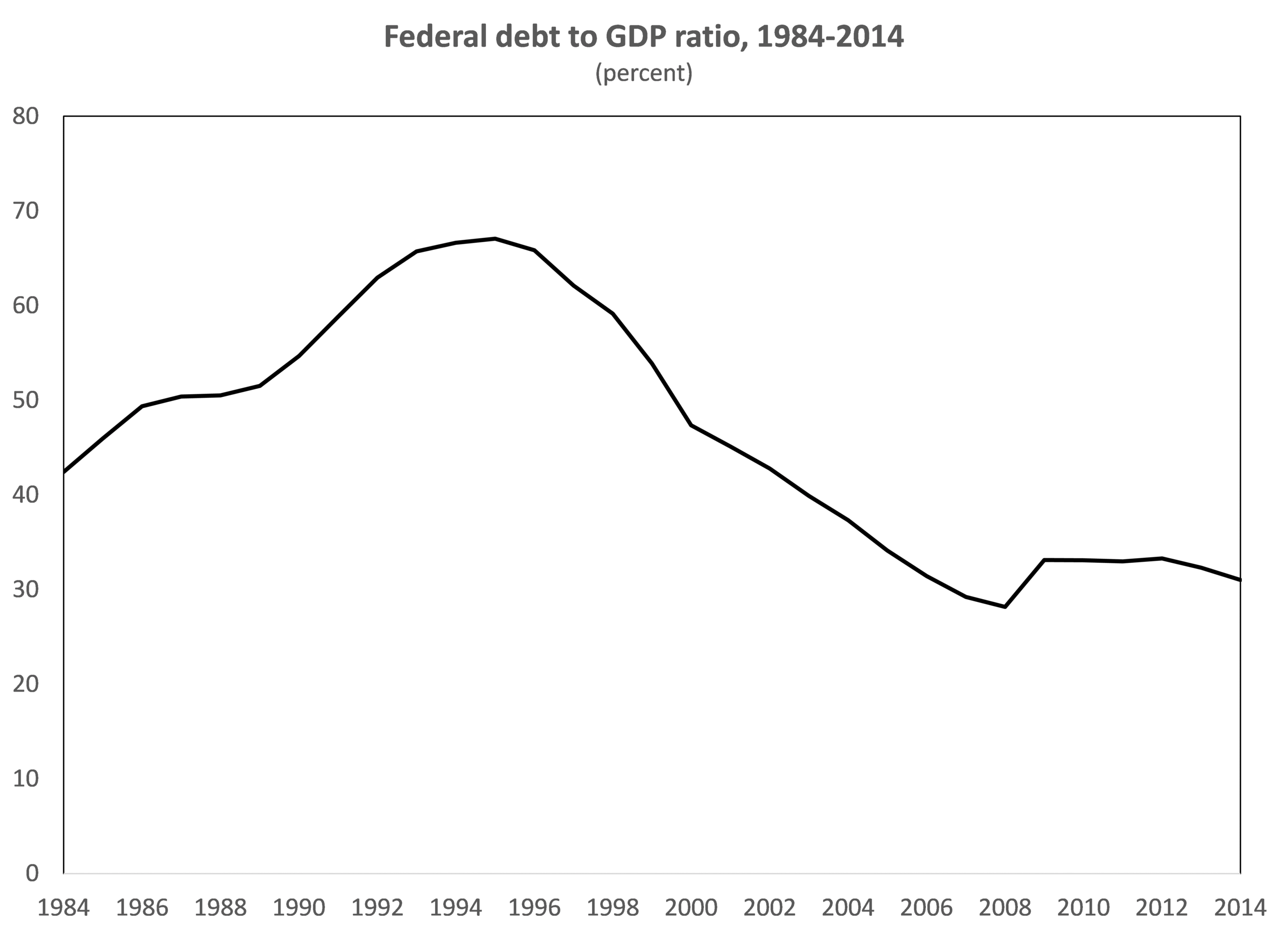

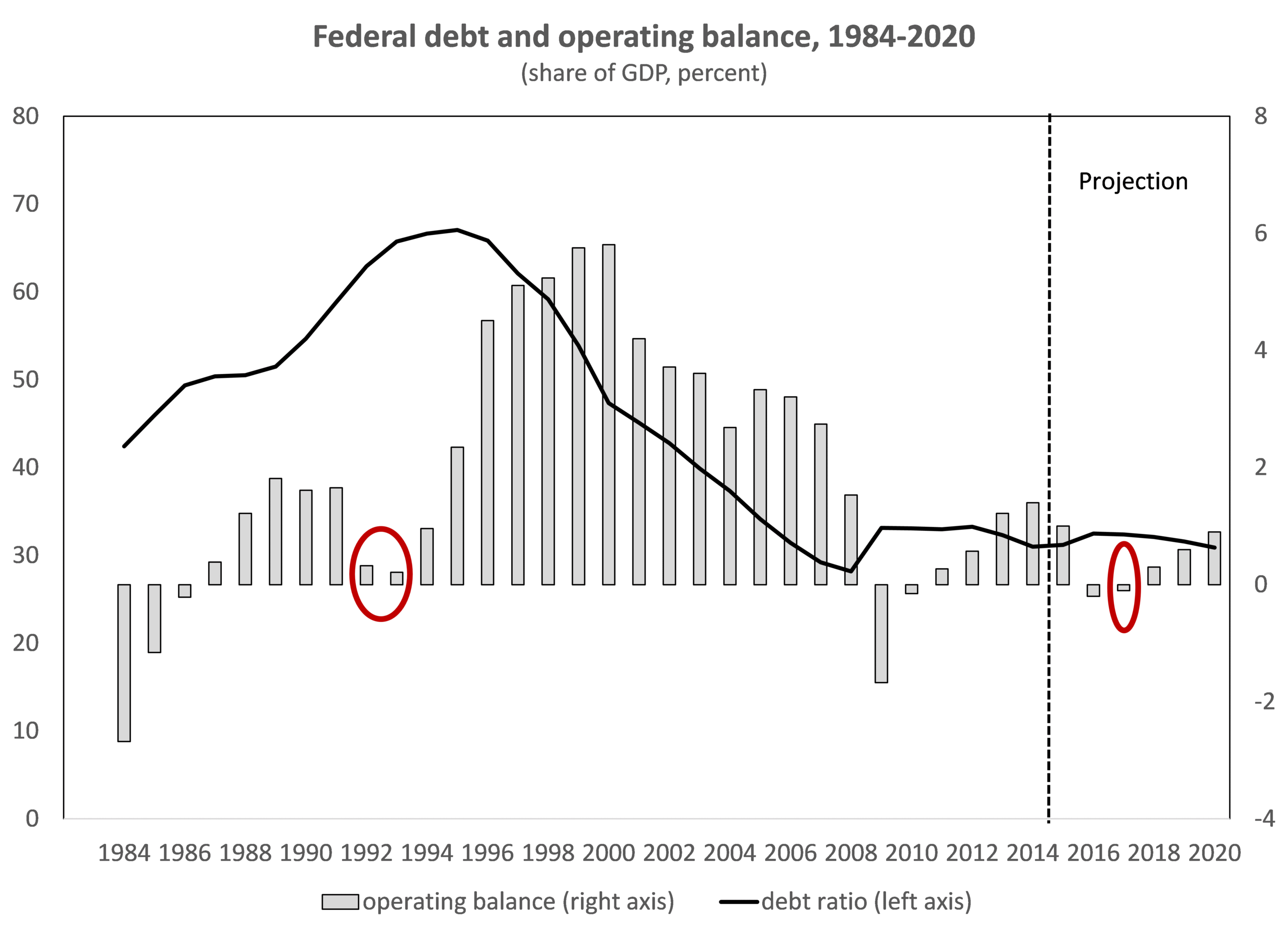

The figure below shows that the federal debt ratio increased steadily until those drastic fiscal actions were taken in mid-1990s. The debt ratio then fell continually up until the global financial crisis in 2008-09, when it was pushed up and sideways:

In the time since Canada’s fiscal crisis, there have been some important developments that matter for today’s fiscal policy context. First, federal debt levels have fallen dramatically. This frees up some spending that was needed to service past debts.

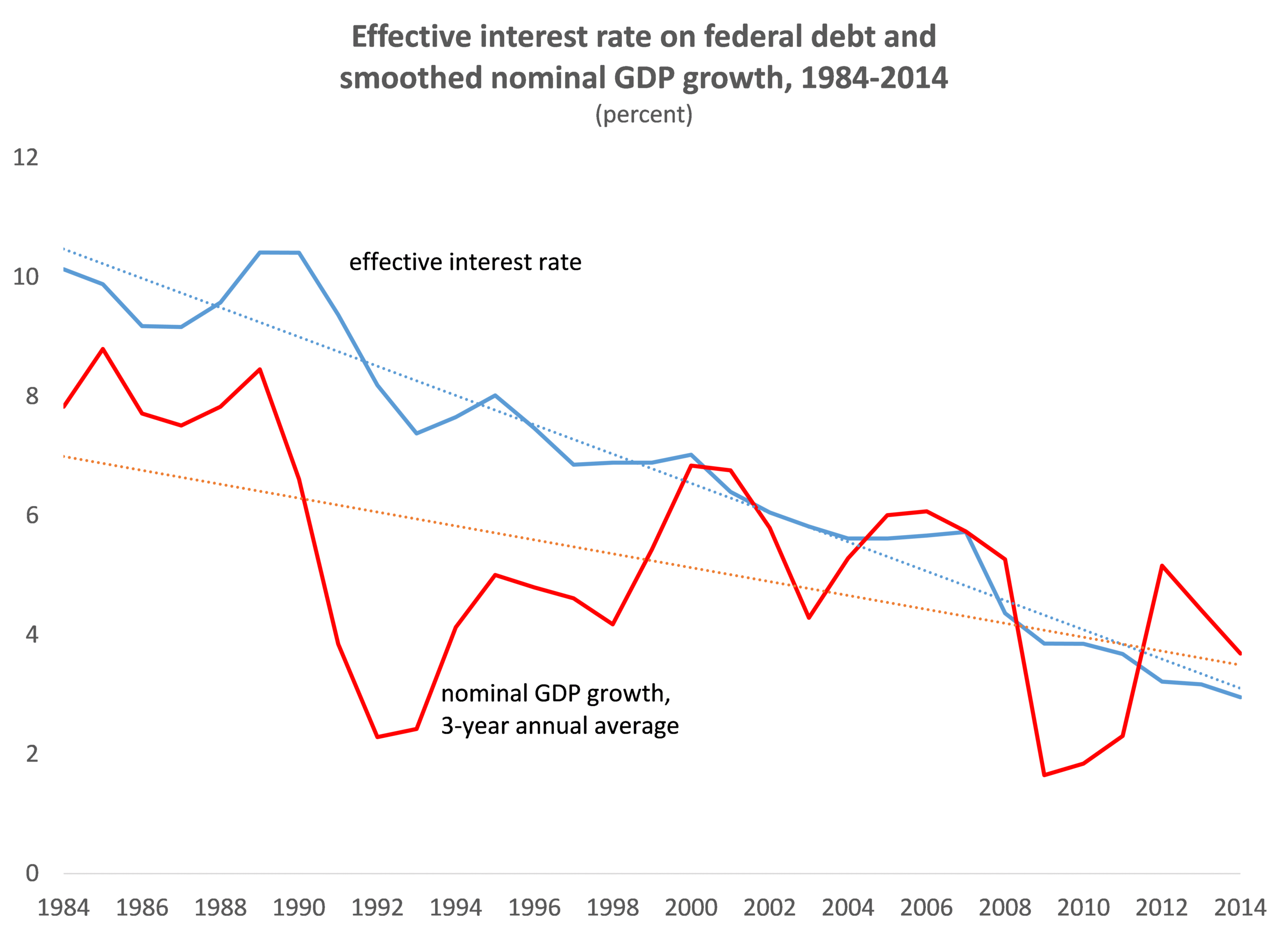

Second, government borrowing costs (shown in blue in the figure below) have fallen more than GDP growth (in red, where the dashed lines show the respective trends of each series).

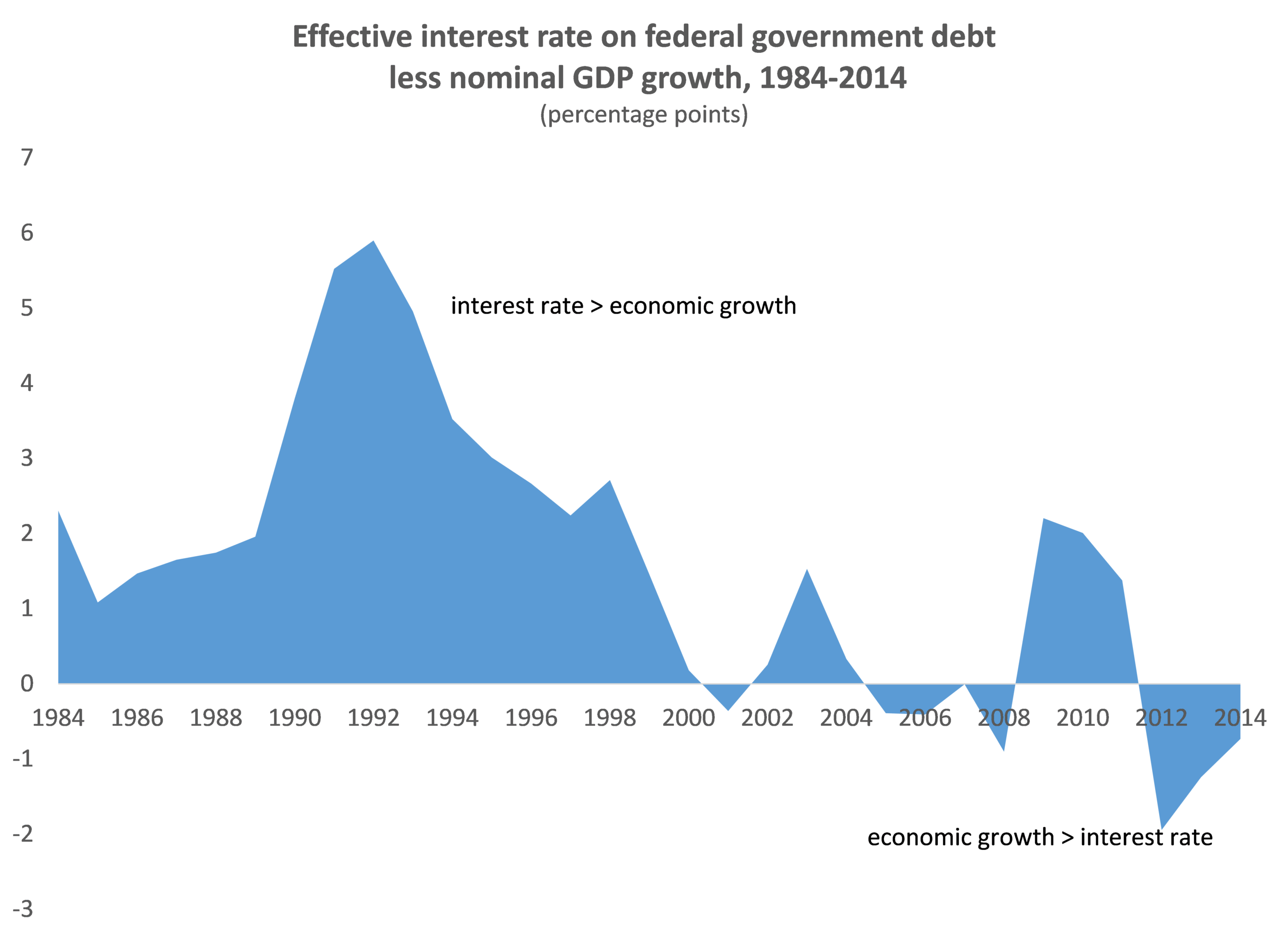

The next figure shows the difference between these two series (the i-g part from the second term in equation above) On net, this is a positive fiscal development. Because the economic growth rate now generally exceeds these historically-low borrowing costs, it’s become much easier to hold the debt ratio steady.

This makes today’s fiscal situation very different than in the early 1990s. Back then, federal debt was high, and interest rates were much higher than economic growth. These fiscal headwinds meant that Canada needed to run continued, sizable operating surpluses of over 3% of GDP (roughly $60 billion in today’s dollars) in order to stop the debt ratio from rising.

Today that’s not needed and there is much more fiscal room. In 2017-18, for instance, the government expects to run a small operating deficit (in the right red circle). This underlying fiscal performance is actually worse than we had back in the early 1990s (left red circle). However, this time around the debt ratio is still expected to fall, whereas it rose sharply back then, despite the operating surplus. The figure also shows that in the mid-1990s much larger and sustained operating balances were needed to finally bring the debt ratio down.

Evidently, federal debt dynamics have changed dramatically since the 1990s — and for the better. We now have a much lower starting point for the federal debt ratio. Borrowing costs have fallen more than economic growth. These fiscal tailwinds should make it much easier to hold the debt ratio steady over the current government’s mandate.

Of course, today’s situation doesn’t rule out worsening debt dynamics in the future. However, to tell a compelling story, the fiscal hawks that worry about Budget 2016 deficits need to include the more challenging provincial outlook, and show plausible numerical scenarios where interest rates rise quickly, GDP growth slows further, and the debt ratio climbs steadily.

Without providing such analysis, any speculation that Canada is headed for an imminent fiscal crisis remains an easy talking point that’s unhelpful.