Capping an individual’s overall tax preferences may be a simpler ”” perhaps even a politically-feasible ”” way to address the growing web of micro-targeted tax policy.

Canada’s tax system is increasingly being used, not simply to raise revenue, but to achieve a vast array of policy objectives through specific credits, deductions and exemptions.

These so-called tax expenditures generally promote worthwhile activities that receive broad public support. For instance, few people would argue against encouraging: retirement savings; charitable donations; children’s activities; parents’ care of disabled dependents, etc. …which are just a few from a long and rapidly-growing list.

And while there are undoubtedly benefits to these policies individually, collectively they represent a significant drain on government revenue. A report by the PBO demonstrates that the cost of these tax expenditures is large and that Canada is a worse offender than most. It valued the cost of our tax expenditures at over $100 billion at the federal level in 2009 ”” worth over a quarter of total spending. (See this Finance Canada report for itemized cost estimates.)

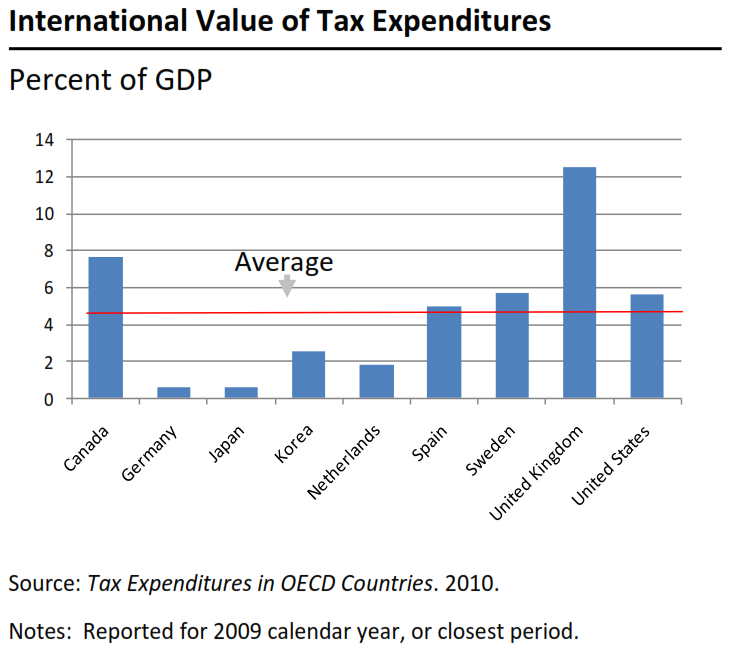

This figure shows that, among the nine advanced countries for which comparable data exist, Canada had the second highest reliance on tax expenditures, worth nearly 8% of GDP, and notably higher than the convoluted US tax code.

When economists complain about tax expenditures (which we often do), we argue that they:

1) are inefficient ways to delivery programs.

– subsidizing activities that would have happened without the tax incentives;

2) are inefficient for the broader economy.

– requiring higher tax rates to raise revenue on narrower tax bases, which reduces incentives for economic growth;

3) hurt the government’s fiscal position.

– reducing revenues and therefore worsening the government’s budget balance;

4) are regressive.

– providing larger tax benefits to those with higher incomes;

5) complicate the tax system.

– making it hard for people to comply with the complex web of tax rules (and do their own taxes) which enriches tax professionals;

6) are opaque.

– because they aren’t subject to the Parliamentary oversight that similar spending programs would receive.

These arguments have largely convinced other economists that tax expenditures should be limited, but they have failed to convince politicians to act.

Attempts to remove existing tax preferences on a one-off basis will be fiercely resisted by those who benefit from these rules, so politicians naturally worry about a possible loss of votes. At the same time, politicians love to create new tax credits that might attract votes. These announcements are highly-visible, concrete and easy to explain and trumpet at election time; their key political virtue is that they can be targeted to specific constituents.

The resulting economists-versus-politicians stalemate on taxes underscores the importance of a new paper by Martin Feldstein (an American economist) who offers an elegant and simple solution: limit the amount by which people can reduce their taxes with exclusions and deductions.

Feldstein’s proposal sets a cap on the allowable reduction in tax liabilities at a fixed percentage of income. For the US tax system, he advocates setting this limit at 2% (with possibilities for some exemptions, and options for a more progressive design, and a phase in period for the policy to take effect).

Because this approach doesn’t ultimately go after the underlying tax preferences, it is not a perfect solution ”” but it may nonetheless be a practical one to an enduring problem.

The strategy is politically savvy precisely because it uses a macro rather than micro approach. It deals with all tax preferences together in a single proposal, rather than incurring a never-ending series of one-off battles with specific beneficiaries.

This new proposal to address tax expenditures is an excellent one, and is particularly worthy of consideration in Canada, given the large cost of these programs and their rapid expansion in recent years.