It is not a sure thing Quebec will double TFSAs – that’s important, and here is why

In the lead up to yesterday’s budget, with its anticipated changes to family income splitting and the enhancement of tax-free savings accounts, some provinces likely grumbled privately about the knock-on effects such policy choices by Ottawa would have on their own treasuries.

Because all provinces (except for Quebec) have joint tax collection agreements with the federal government they are obligated to adopt the same definition of taxable income, as determined by Ottawa. And though it operates its own parallel system of tax collection, Quebec has often preferred, out of simplicity, to harmonize many of its income-tax policies with the federal model. For these reasons, one would naturally assume Ottawa’s decision to raise the TFSA contribution limit from $5,500 per year to $10,000, retroactive to January this year, would result in a seamless and coherent implementation across the country, almost immediately.

Hold on.

Largely un-noticed in English Canada is a statement that Quebec Finance Minister Carlos Leitao made yesterday afternoon following the tabling of the federal budget. The official press release from his department doesn’t specifically address the issue of the TFSA, however, in a scrum with reporters the Minister suggested he was surprised by the announcement and would not immediately commit to following along with the TFSA changes.

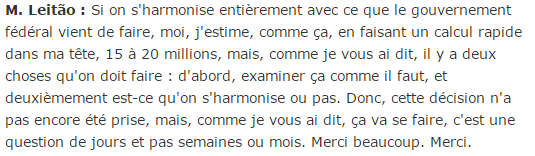

Here is a copy of the pertinent part of the transcript from Leitao’s comments. In essence, he expects the doubling of the TFSA to cost Quebec about $15-20 million a year in forgone revenue, and says a decision on how the province will proceed will be forthcoming in the next few days.

Source: https://bit.ly/1IJKqxg

There are many reasons to expect that despite the very reasonable concerns expressed by the Minister, Quebec will ultimately replicate Ottawa’s TFSA policy. Were it not to do so, financial institutions would have to adjust their reporting processes, and even potentially introduce a new version of accounts to handle the differentiated approach between clients resident in the province, and those in the rest of Canada. Implementation of the existing unitary system has been fraught with many challenges that would only be amplified under a two-track approach.

For example, for workers who end up moving between provinces, what will happen with past and future contribution room? How would Quebec treat capital gains, dividends and interest income accruing on assets within the TFSA but which were accumulated prior to residing in the province? There are many ways each of these issues could be dealt with (e.g. one might take the view the past is the past and we only care about contributions going forward), but in principle this just goes to show what kind of administrative mess financial institutions and tax authorities might be facing.

In the likely event Quebec forgoes its complaints and adopts the federal model, there is still an important point here.

One of the great benefits – and at times challenges – of a federation like Canada’s is the ability for experimentation among provinces to create a sort of ”œlaboratory of ideas”.

If, on the very small chance, Quebec decides not to follow the federal government’s lead in raising TFSA contribution limits we will have a grand experiment on our hands. In that scenario, more than three-quarters of the country will be living and working in an environment where TFSAs will eventually be able to shelter most, if not all, of the wealth Canadians have available outside of a pension account or real-estate. For the highest income earners in society, who do ”œhave” the $10,000 a year on hand to max out their TFSA, this will likely result in a major shift away from capital taxation. We will also have about a quarter of the population living in a comparable jurisdiction with a slightly smaller but similar model.

Rare as natural experiments are in economics, this is even more significant in the context of tax policy because of the way in which a common definition of taxable income impedes variation. Given today’s common definition, provinces are often limited to playing with the effective rate of taxation through statutory rates or non-refundable tax credits. Since they can’t touch what counts as income per se we don’t often get to measure a major change in the tax structure, like the doubling of the TFSA, against a proper counter-factual. In other words: how would the world have turned out if we hadn’t raised the TFSA contribution thresholds?

Quebec may yet offer that possibility. If it does, we will get a real test of how the TFSA changes, on their own, affect such things as the distribution of income, economic growth and savings behaviour””all of which reflect intense debates within economics today about whether and how investments should be taxed.

—

Thanks to Kevin Milligan and Scott Cameron who provided helpful thoughts as I was preparing this post.