The world economy is now, thankfully, in recovery after the Great Recession. But what sort of global recovery will it be? Where are the shoals and safe harbours? As Churchill noted, “It is always wise to look ahead, but difficult to look farther than you can see.” This recovery will test our powers of sight and foresight.

Why is this so? Over the last six months the world has emerged from the most devastating financial crisis and recession since the 1930s. This global recession was a unique combination of demand-supply imbalances — primarily housing bubbles in the US, the UK, Spain, Ireland and elsewhere; and balance sheet imbalances — primarily subprime mortgages and their offspring infecting financial institutions in the US, the UK, continental Europe and elsewhere. And the crisis and the recession have to be superimposed over the tectonic shifts in demographics, the rise of Asia and globalization.

It was not a typical recession, and it will not be a typical recovery. We are facing a decade of global change, volatility and uncertainty. It would be unwise for Canada to plan on a “global business as usual” basis. To put more starkly, as Mohamed El-Erian, CEO of the large US investment fund Pimco and a former top International Monetary Fund (IMF) official, recently observed, “The world is on a journey to an unstable destination, through unfamiliar territory, on an uneven road and, critically, having already used its spare.”

For Canada, which escaped relatively unscathed from both the global financial crisis and the worldwide recession, the question is how we manage risk and opportunity in the decade ahead. I believe we should focus on two distinct but interrelated parts. First, we should strive for no less than world-best macroeconomic fundamentals. The clear lesson to be drawn from the Canadian experience in the global financial crisis is the value of strong balance sheets — government, financial sector and corporate — as well as fiscal probity, monetary credibility and prudent regulation of the core financial system. Second, we should focus on Canadian competitiveness and agility in a rapidly changing world, and this means dealing effectively with our productivity and innovation deficits.

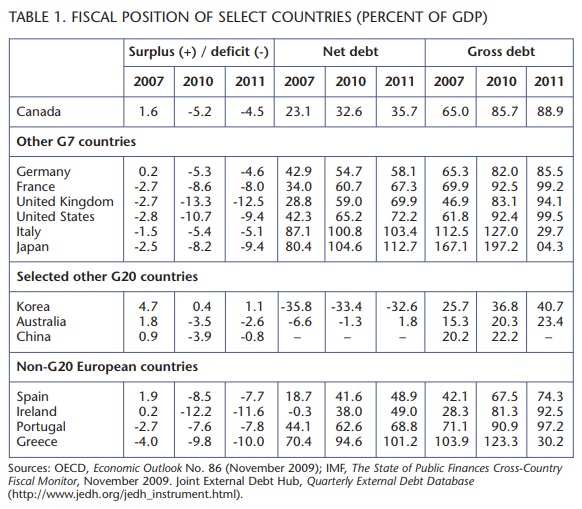

Beginning in the mid-1990s Canada put itself in an enviable international fiscal position, with 10 consecutive years of surplus resulting in the lowest net debt-to-GDP among the G7 countries (see table 1). To achieve this, we reduced our government-spending-to-GDP and government-employment-to-population ratios very significantly; combined with declining debt servicing, the structural surplus these reductions created allowed us to cut corporate tax rates below US levels and make a number of strategic investments, including public sector R&D.

Today, one of the most troubling hangovers from the Great Recession is large fiscal imbalances that are primarily in industrial countries, not emerging ones. To give some perspective, the IMF estimates that the aggregate fiscal deficits of the G7 countries will total US$2.7 trillion this year, with the US alone struggling with a deficit of almost 11 percent of GDP, or US$1.5 trillion. If these deficits persist, they risk putting upward pressure on real yields, as private sector financing begins to recover; and as debt and debt servicing rise, they will crowd out other priorities in governments’ fiscal plans. The IMF estimates, on a current policy basis, that US gross debt will be over 100 percent of GDP by 2015, and net debt will be over 85 percent. The UK is on a similar debt trajectory, while Japan could have a gross debt near 250 percent of GDP. Such deficits and debt pose a possible constraint on future growth in systemically important countries like the US, Japan and the UK. But, as Greece has so amply demonstrated, in a pervasively globalized world, large and unsustainable deficits in smaller countries can also pose systemic risks.

For Canada, which escaped relatively unscathed from both the global financial crisis and the worldwide recession, the question is how we manage risk and opportunity in the decade ahead.

In all this, Canada has by far the best fiscal position in the G7, with a federal deficit of around $50 billion this year (31/4 percent of GDP) and a total federal-provincial government deficit of 5 percent of GDP. With the built-in two-year termination of federal stimulus spending, the federal deficit should halve as a share of GDP next year. But getting back to fiscal balance will be constrained by two factors. First, measures taken as a result of the recession and countercyclical fiscal policy will add $165 billion to our national debt and raise permanent debt servicing costs correspondingly. And second, Canada suffered more of a “nominal income recession” than a “real income recession,” with nominal GDP falling by 4.6 percent compared with a real GDP decline of 2.3 percent. Since we tax nominal incomes not real incomes, tax revenues will be depressed until this lost nominal income is recovered, and this points to the importance of the pace of recovery over the next several years.

While Canada’s starting point is enviable, the lesson learned from the financial crisis is the value of fiscal balance and the relative protection a strong fiscal position affords our economy and society. In an uncertain world, this suggests a return as rapidly as possible to fiscal balance, which is symmetric to the contracyclical injection of stimulus in the recession and would also take some pressure off interest rates in the medium term. We should also consider reintroducing a contingency reserve to fiscal planning to increase the certainty in international markets that we will make our fiscal targets, thus increasing our macroeconomic advantage.

I shall turn now to the second element of building a Canadian advantage in this changing world, the need to address our productivity and innovation deficit. The basic facts of Canada’s poor productivity performance are well established, but they are neither well known nor well understood. There are basically two ways to improve a country’s standard of living. The first is to have more people in the workforce or have those in the workforce work longer hours, so that in total we produce more stuff. The second is to improve productivity, so that each worker produces more stuff for each hour they work. While Canada has long relied on the first way to generate almost half of its living standard gains, the demographic reality of an aging population means that in the future we will have to rely almost exclusively on productivity growth. And our recent performance in that respect is not good.

Let’s look at how productivity growth has evolved, with a particular focus on the business sector. Labour productivity growth in the Canadian business sector grew at a very strong 4 percent average annual rate over the immediate postwar quarter century (1947-73), then sagged to a 1.6 percent average annual pace over the next quarter century (1973-2000), and then fell again to an anemic 0.8 percent average annual growth rate over most of the past decade (2000-08). And as the average number of hours worked by Canadians increased over the last two decades, our productivity growth per hour worked was weaker still.

Looking at productivity comparisons across countries, we see a similar message. Using the common international measure of productivity, output per worker per hour worked, Canada was an astounding 17th among OECD nations in 2007, worse than almost all the euro economies, the Scandinavian countries and the United States. But, thankfully, Canadians work more hours than the OECD average, so our total output per worker ranks 8th among OECD countries, better than those of most European nations but far behind that of the United States. US comparisons are particularly important and worrisome. In 2007, Canada’s business sector productivity (measured per worker) was only 75 percent of that of the US, despite the highly integrated nature of our North American economies. And equally concerning is the trend: on this same measure Canadian business productivity was over 90 percent of comparable US productivity levels in the early 1980s.

At the sectoral level there is a fairly wide dispersion in productivity performance within and across sectors in Canada, and more so than in the US. This suggests faster adaptation of new technologies and processes by US business, and likely more competition. There has also been much stronger productivity performance in the US manufacturing sector, and this in turn has been particularly concentrated in the production of goods and services associated with information and communications technologies (ICT). Furthermore, in the service sector, which tends to dominate both economies, the US service sector has sustained broad-based and consistently higher productivity growth than Canada’s for more than a decade now.

There are a number of developments that suggest the economic risks the productivity deficit poses to the Canadian economy are becoming greater. The Canadian dollar is now over 95 cents US and this really bites when the Canadian productivity rate is just 75 percent of that of the US. This is exacerbated by the risk of a slower than usual recovery in the US and is compounded by sluggish European growth. Rising natural resource prices, driven by China and India, continue to be a boon for Canada. But these same Asian countries are rapidly becoming Canada’s competitors further and further up the value chain.

Looking forward, any productivity strategy needs to incorporate at least four core elements to be effective, bearing in mind that there is no single, simple or immediate fix to our structural productivity problem.

First, we should focus on more innovation. Innovation is a core driver of sustained increases in our productivity growth. It creates the new products and processes that will allow Canadian business and Canadian workers to move up the value-added chain and compete on quality and service and newness, not exclusively on cost. The life cycle of products is increasingly shifting to higher specialty goods and services with shorter life spans, and more technology-intensive production. In such a world, where competitiveness is increasingly defined by creativity, Canada cannot sustain above-average living standards and below-average innovation performance.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

The problem is that Canada is not an innovation leader, but it can and must become one. While Canadian public sector investment in research, primarily through universities, is equal to that of the top OECD countries, it is quite a different story in private sector investment in innovation.

In 2007, Canada’s business sector ranked 14 among all OECD countries in business R&D expenditures as a percentage of the economy. Its business R&D spending is only 1 percent of GDP, well below the OECD average of 1.6 percent of GDP and roughly half of what the US spends. Countries like Korea, Finland and Sweden are in another league again, spending almost 3 percent of GDP on research and development.

To get a perspective on the scale of the business-sector innovation deficit, consider the following: for Canada to raise business spending on R&D to just the OECD average would require an additional $10 billion per year. And even with such an increase, on average Canadian business would still be far from the top quartile of innovation performance among OECD countries.

Investing in leading-edge equipment can also drive innovation through adaptation. But, here too, Canadian business invests far less per worker than its US counterparts. This is most pronounced in ICT, particularly in the service sector.

Where does this leave us? In a recent paper entitled Making Innovation Make Sense, for the Public Policy Forum’s “Innovation Next” Conference, I offered several suggestions for a way forward. Here are some of them.

- Establish “best-in-global-class” sectoral innovation benchmarking.

- Strike an expert panel on the venture capital industry in Canada.

- Focus more public sector R&D investment on creating global centres of excellence that are relevant to the future competitiveness of the Canadian economy.

- Review the effectiveness of tax incentives for R&D and innovation, including whether we have an optimal balance between tax support and direct support for collaborative research.

- Tackle the “basket of disincentives” to commercialization, drawing from the report of the Expert Panel on Commercialization.

- Develop and market a “Canadian brand.”

Second, we have to win the talent hunt. A highly skilled workforce is essential to driving productivity in a knowledge-intensive, global economy. The importance of the labour force is underscored even more by demographic trends, whereby many countries will soon have a larger proportion of the population that is outside the normal working age than is in it. With fewer people working, it is simple arithmetic that each has to produce more (i.e., be more productive) just to have the same supply of goods and services. This points clearly to the need to focus on education.

Canada needs a focus on talent. In a knowledge-based economy, high school completion and rigorous minimum literacy standards should be givens, not aspirations. We have fewer Canadians with university degrees than do many of our competitors, and we have fewer still in the scientific and technology disciplines. And while immigration is the main avenue through which we can offset our demographic trends, its effectiveness depends on the extent to which we attract well-educated immigrants of working age with the skill sets needed.

Third, shifting demand means shifting markets. Global GDP is shifting to Asia. But Canada’s trade linkages are akin to the portfolio of a cautious manager who is overinvested in traditional markets and underinvested in new and promising, but risky, markets. Canada needs a clear and focused market-enlargement strategy to respond to the long-term rise of Asia.

To get a perspective on the scale of the business-sector innovation deficit, consider the following: for Canada to raise business spending on R&D to just the OECD average would require an additional $10 billion per year. And even with such an increase, on average Canadian business would still be far from the top quartile of innovation performance among OECD countries.

Such a strategy must include new economic partnerships with the Asian triangle of China, Japan and India. It should also involve expanding the Americas Strategy toward Brazil, as well as the conclusion of a new-generation economic arrangement with Europe. These arrangements should be oriented less to trade in goods (leave these to the WTO) and more to the treatment of services, investment, R&D, intellectual property and dispute settlement arrangements. It also should respond to the paradox that Canada is a trading nation but not a nation of traders, by encouraging more firms, particularly small and medium-sized enterprises, to engage in trade.

Fourth, we need more engagement and new attitudes. Canada is a market-based economy, and the vast majority of productivity gains must come from business. Attitudes matter, and to change attitudes we need sustained engagement on the key issues of productivity and innovation.

To help create such engagement on making productivity and innovation make sense, I believe Canada should consider establishing a “productivity and innovation council of Canada.” Its mandate would be to encourage innovation and productivity among Canadian businesses, with a focus on benchmarking Canadian business to global best practices, sector by sector. Its remit would be to business and governments, never losing sight of the collective public interest in creating a more innovative and productive country. Its structure would be independent of both government and business, it would be established by federal statute, and it would initially have a 10-year term. It would have the capacity to carry out sector-based benchmarking of innovation and productivity differences among countries for Canadian business.

Its effectiveness would be determined by the credibility of its leadership and the rigour of its benchmarking analysis. And its objectives should be ambitious: to make Canada a top-quartile innovation performer within 10 years, close at least one-half of its productivity gap with the United States and increase Canadians’ standard of living by $5,000 per capita.

The global situation Canadians will face over this decade will be complex, uncertain and changing. There will be a positive premium on firms, sectors and countries that are flexible, have solid fundamentals and anticipate the global drivers of change that all nations are experiencing. In this environment, economies that are innovative and productive will have a much better chance to achieve sustained growth, increase living standards and create good jobs than those that are not.

There is no reason for Canada to be a productivity and innovation laggard; there are no insurmountable obstacles before us. The challenges and the solutions lie in our hands. Canadian firms can be as productive and innovative as Swedish, Dutch, Korean or American firms. We need to benchmark our productivity and innovation, sector by sector, to the world’s best. If productivity and creativity are going to drive the economy of the future, being average will not be good enough.

Photo: Shutterstock