The Prime Minister’s visit to China — a success by many accounts — may signal a long overdue shift in the economic dimension of Canada’s foreign policy to where the action is, in the dynamic emerging markets, of which China is number one. Although the US will remain our most important market, President Barack Obama’s knuckleball on the Keystone XL pipeline should be a wakeup call and prompt a broader recalibration of Canadian policies and priorities for global growth. The emerging markets — many growing at twice the rate of Western industrialized markets — offer complementary and more dynamic opportunities. They also pose new risks against which conventional approaches will not suffice.

Key elements of an effective strategy are trade and investment policy initiatives; better incentives for innovation; new investments in infrastructure along with streamlined regulatory approaches for their approval; and more coherent immigration, education and training policy reforms. Harnessed together under a unique partnership between governments and the private sector, these changes can enable Canada to turn the global trend to its advantage. But we will need to be creative and committed, to target the markets with the greatest promise and use our comparative strengths selectively, with equal parts of persistence and shrewd networking, to meet our goals.

A few facts anchor the premise:

- Since 2009, most of the world’s economic growth has come from major powerhouses like China, India and Brazil, along with the dynamic economies of Korea, Indonesia, Turkey, Mexico and Poland.

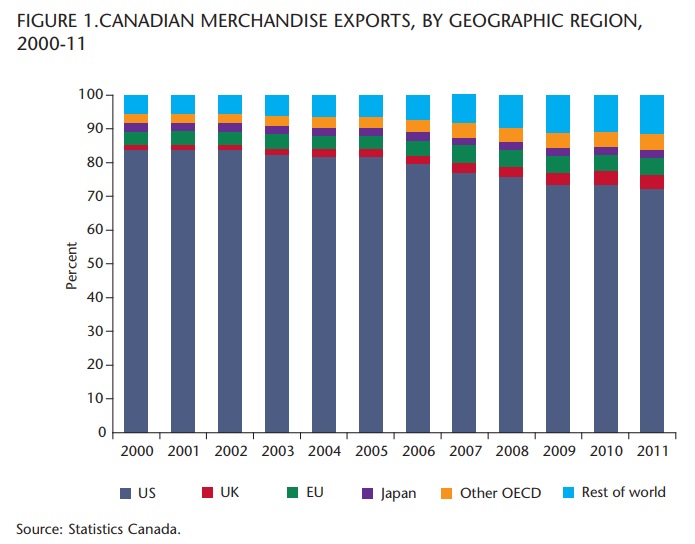

- Today, less than 10 percent of Canada’s exports go to these markets.

- By 2020, Canada will not likely be on the list of the top 10 world traders.

Although the risk premium of doing business in many of these fast-growing markets is high, it is discounted to some extent by relatively high savings rates, better infrastructure, a burgeoning middle class, and macro policies that have reduced systemic risk and stand in sharp contrast to the recent behaviour of most developed countries.

However, the underlying challenge is that in many of these emerging markets, governments and stateowned enterprises play an inordinate role in directing economic growth. Basic principles of supply and demand operate in business environments heavily influenced, as the Economist observed in January, by the “visible hand” that governments play. Conventional rules for international trade and investment are, therefore, not as useful in determining outcomes or resolving disputes.

Canada has a lot of what many of these markets need — potash, oil, natural gas, uranium, copper, iron, nickel and agricultural products. We also excel in financial services, aerospace and information technologies, which are also increasingly in demand. There is scope as well for Canadian producers to make better use of the emerging markets’ global value chain capabilities, where we have been too reliant for too long on our adjacent market — the US.

Others, notably Australia, have been smarter and quicker in recognizing tangible benefits from the emerging markets. China has invested more than $14 billion in Canada since 2005 but more than $40 billion in Australia during the same period. With an economy similar to Canada’s, Australia has much deeper links with Asia, notably with China. Australia’s trade with Asia grew from 19 percent of the total in 1950 to 50 percent in 2010 — almost half of that with China — whereas only 12 percent of Canada’s trade is now with Asia. Australia takes in three times more Chinese students annually than Canada. The differences are not due to distance. It takes the same amount of time to fly from Sydney to Beijing as from Toronto to Beijing; the same time to ship from Sydney to Shanghai as from Vancouver. From Prince Rupert the shipping distances are even shorter.

Too often, we wring our hands about being “over-dependent” on our resource base — a natural strength that other countries envy. Similarly, we underestimate the significance and global reach of our banks and insurance companies and the prowess of our high tech firms. If we expect to take better advantage from new avenues of global growth, we have to become more confident, more assertive and more astute in promoting what we do best. We need to leverage these strengths more adroitly in the emerging markets to obtain maximum benefit.

Prescriptions for future success begin with trade policy. Our approach to trade negotiations needs careful recalibration, separating the wheat from the chaff when choosing priorities, concentrating more selectively on countries that offer tangible growth opportunities for Canadian exporters and investors and channelling our negotiating expertise where there are the best prospects for beneficial outcomes.

The shot gun approach — launching a myriad of negotiations but concluding very few and none with a major Asian economy — needs to be realigned to markets where Canada’s comparative advantages will work best. Over and above negotiations with the EU, where growth is sputtering, we need to identify bilateral and/or regional prospects that offer significant promise and deploy increasingly scarce negotiating resources accordingly. These are tough markets in which to conduct business. Negotiations will not be for the faint of heart. Success requires a combination of persistence, networking and smart tactics. Instead of the traditional free trade template, we should seek to customize agreements on a case-by-case basis and, where relevant, take proper account of the extent to which counterpart governments direct economic decision-making. Canada’s approach should reflect hard-headed analyses of what we need and what we are prepared to give in a coherent series of negotiations.

Too often, we wring our hands about being “over- dependent” on our resource base — a natural strength that other countries envy. Similarly, we underestimate the significance and global reach of our banks and insurance companies and the prowess of our high tech firms.

To be effective, Canada’s chief trade negotiators require more authority to represent and defend the national interest. Adding the provinces and territories to the negotiating table for the EU negotiations was not a constructive precedent. It has made the negotiations unwieldy, to say the least, and may dilute the result. While the provinces obviously need to be involved in aspects affecting their jurisdiction — e.g., provincial procurement practices — substantive trade negotiations cannot be advanced by committee. The trade and commerce power of our Constitution should not be compromised. The more we divide our attention and our effort among ourselves, the less we will achieve. Close collaboration with stakeholders with a direct interest in the outcome is ultimately in the interest of all Canadians.

Talks are already underway with India. Negotiations with Korea were stalled primarily by reservations in Canada about the implications for Canadian auto manufacturers, concerns that, surprisingly, were not shared by their US counterparts. These negotiations should be re-engaged as a matter of priority. Discussions of an economic partnership agreement with Japan also offer attraction, and may, parenthetically strengthen Canada’s ability to conclude with Korea. While much of Japan’s dynamism has faded in recent years and it is by no means an emerging market, it is still an economy of weight for Canada and the repository of innovations in many sectors like aerospace and life sciences with scope for collaboration. Japan is still the world’s third largest economy and one of the wealthiest, with a per capita GDP of $US46,000. A world leader in a number of high tech and precision industries, Japan provides vital inputs for Canadian industries, as well as highly valued products Canadians consistently buy. Conversely, Japan is a major importer of Canadian commodities — energy, minerals and food. In an increasingly turbulent world, Japan has obvious concerns about securing reliable and secure sources of energy. Canada’s financial, engineering and architectural services are also in demand.

Talk of free trade with China may be overly ambitious, but there may well be subsidiary trade and investment agreements along the lines of those concluded during the Prime Minister’s recent visit that would broaden the range of ties with Canada. These could, for instance, ensure better control of intellectual property and provide more certainty for Canadian investors.

Indonesia and Turkey are two other rapidly growing Asian markets worthy of priority engagement. Already a NAFTA partner, Mexico also merits greater focus.

The Trans-Pacific Partnership (TPP) is a concept much in vogue and, once US intentions and capabilities for a serious trade negotiation are more evident, i.e., after the November election, Canada should explore carefully what might be achieved and what the expected tradeoffs will be. Inevitably, Canada’s supply management programs for dairy and poultry will come under scrutiny in a broader, regional negotiation, so calculations of the potential economic benefit will have to be sufficient to offset political negatives on the home front. With proper sequencing, bilateral initiatives could reinforce a regional approach.

Investment policy is the second pillar for success. Canada has benefited enormously from a relatively benign environment for foreign investment. We will need to maintain a welcome mat, especially for expanded development of our resource base, but it is worth debating whether more clarity would help ensure that the national interest is properly served by such investments. The opaque nature of Investment Canada’s rulings is a source of some confusion for foreigners and Canadians alike. More certainty can only come from more transparency. Measures designed explicitly to prevent dominant control of key sectors or to prevent the wholesale loss of head office functions in Canada should be part of the debate.

With many emerging markets the playing field is uneven, in part because cost of capital considerations for state-owned enterprises, backed by massive sovereign wealth funds, are not identical to those of private investors and, more generally, because of the overt role of government in economic affairs. Should Canada seek some form of reciprocity from the country of the investor in its calculation of net benefit, especially for investors from countries that have explicit restrictions on foreign investment? Conventional theories about the advantages of “openness” are fine, to a point, but political realities, including the fact that quasi-market economies play by different rules, cannot be ignored. Also worthy of consideration is the extent to which access to Canadian resources should be used more as a bargaining chip for our trade and investment policy objectives.

The trade and commerce power of our Constitution should not be compromised. The more we divide our attention and our effort among ourselves, the less we will achieve. Close collaboration with stakeholders with a direct interest in the outcome is ultimately in the interest of all Canadians.

Some may see efforts to inject greater clarity into rules governing foreign investment as a move towards protectionism, but that is a reflex judgement that has less resonance in an increasingly unconventional global economy. Foreign investors who find the current review process ambiguous would be better served by clearer rules and certainty about the verdicts.

We live in an age where innovation is constant and entrepreneurship is at a premium. Studies suggest that Canada is lagging in both. We constantly lament our sagging productivity rates and our seemingly low appetite for risk. One reason why we consistently fall behind the US on productivity is that commercialization of new ideas is a real problem in Canada. The Jenkins panel report lamented that “while Canada produces IP in abundance, it is less adept at reaping the commercial benefits. Too many of the big ideas it generates wind up generating wealth for others.”

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

Canada’s government spends more proportionately on R & D than almost all OECD countries ($7 billion annually) and yet sees little commercial dividend from the investment. The Canadian Advanced Technology Alliance (CATA) claims that government-sponsored R & D provides “feedstock for other nations growth.” In other words, foreign firms based in Canada capture R & D for profits in other markets. Canada remains essentially a renter of technology.

CATA contends further that the gulf between academic research and business application seems to be growing, not shrinking. At a minimum, instead of more studies with recommendations that gather dust, we need to give business firms in what the government has deemed to be priority sectors for innovation — health and life sciences, information technologies, energy and natural resources — a more direct role in guiding and administering government programs intended to promote commercially viable technology transfers.

The most alarming findings from market research conducted by the Jenkins panel were that more than half of the businesses polled were not aware of the federal R&D programs. Two-thirds complained that the application processes were too burdensome. The alphabet soup of different money pots cries out for a “one stop shopping” approach and for more targeted support.

Biotechnology is frequently cited as a priority sector, and yet the chronic lack of venture capital in Canada means that we have more stranded research than product development.

Some, however, is scooped up by multinationals that then command sales and profits outside Canada. Studies cited by the science journal Nature indicate that investments over the past decade in the life sciences and biotechnology can yield better returns than those in other forms of technology. And yet, during the same period, new start-ups in all fields in Canada dropped by more than 50 percent (from 1,007 in 2000 to 444 in 2011.) To address the venture capital shortage, a fund modelled on the highly successful Yozyma Group in Israel could be established to provide a catalyst for start-ups in key sectors having potential in international markets.

Some Canadian firms worry about the impact that a steady transfer of IT jobs and related technology offshore will have on the productivity of Canadian businesses. Because much of IT can be done from remote locations, there is no real incentive to retain employment in Canada. They recommend that incentives be given to stimulate and retain IT employment at home as an alternative to outsourcing. They urge that R&D programs assess the impact on productivity and employment and that trade negotiations seek to level the playing field in terms of market access.

The Canadian International Council (CIC), has criticized the government’s indifferent approach to the retention and accumulation of intellectual property. Others express concern about the lack of protection if IP in emerging markets like China — clearly an area where the conventional rules of the past — do not meet the challenges of the present or future. Not all innovation or efficiency comes from R & D. Sharper business practices and competitive market pressures can often be the best prod for productivity. Greater exposure to and involvement with supply chains in major emerging markets can provide that tonic.

Part of our productivity problem is structural. Small and medium enterprises (SMEs) may, as many politicians claim, be the best engines of growth because they represent almost two-thirds of employment in Canada. But many of our small or medium-sized companies depend heavily on the very few, big companies in Canada for much of their global success. We have not only too few big companies, but also a disproportionately high number of small companies with fewer than 100 employees. Not surprisingly, we also lack a culture of collaboration among companies whereas, in the major emerging markets, governments “encourage,” i.e., direct, collaboration across the board. We need tailored, coordinated strategies that will enable our small companies to become globally competitive medium-sized firms. Programs like QC100 in Quebec, intended to promote peer learning for CEOs of medium-sized companies with global expectations, should be expanded and drawn more directly into discussions that shape policy priorities.

Size does matter. That is why we need to support the few “national champions” we do have — domestically and globally — to bolster their success. Terms like “economic nationalism” may have pejorative connotations for some, but actions calibrated to serve the national interest and bolster the potential of Canadian firms to grow domestically as well as in a much tougher global environment should not. The government should not attempt to pick winners or indulge in fantasies about industrial policy, but it should give particular attention and support to key sectors that have been designated as priorities for Canada’s economic growth. A pragmatic balance between economic theory and political reality is needed.

Modern infrastructure will be essential to Canada’s growth prospects.

Programs like QC100 in Quebec, intended to promote peer learning for CEOs of medium-sized companies with global expectations, should be expanded and drawn more directly into discussions that shape policy priorities.

Almost $300 billion of projects are planned over the next two decades in Canada — from the Lower Churchill hydro project in Labrador to the Conawapa project in Manitoba and pipelines to the west and east coasts intended for shipments of oil and liquefied natural gas. These projects, properly regulated and financed, will provide essential facilities for broader export growth and serve as major drivers for our own economy. And yet, infrastructure gridlock, if left unchecked, will thwart needed action on all. Progress on these projects requires distinct and determined political leadership. Avoidance of duplication and some streamlining of timelines is in order and, as a recent C.D. Howe study concluded, regulatory processes for the approval of hydro facilities or pipelines should not be encumbered with broader societal issues that are outside the purview of existing regulatory agencies.

Also in need of recalibration are immigration, education and training policies that will enable us to seize the opportunities from the changing global trend. People with skills to build the new infrastructure we need, to develop our resource base and to deploy the export potential of innovative technologies. It is more than ironic that, at a time of 7 percent plus unemployment, Western Canada suffers from a lack of talent and basic skills to support its growth. Meanwhile, immigration policies skewed more toward volume than employment hit hardest on provinces like Ontario and Quebec, which can least afford the associated costs of disproportionate annual intakes. The immigration minister’s indication that he plans to “transform” the backlog of applications into an employment pool for selection would be a step in the right direction.

We also have a temporary workers program bringing in almost 200,000 workers annually, in part to fill the low-skilled jobs Canadians refuse to take, but also to fill the strong demand for high-skilled IT jobs. Our educational institutions are not graduating sufficient numbers with skills that our economy needs. Instead, we see too many graduates with skills scarcely in demand.

The skill deficiencies are not just in high tech fields. Getting a qualified plumber or electrician can be as difficult for many Canadians as finding a family physician. More educational emphasis is needed on basic skill development. We desperately need, as well, a more compelling apprentice program to fill the gap, and Germany offers a compelling model worthy of emulation.

Education and training are clearly areas of provincial jurisdiction. The provinces should be encouraged to work more coherently and more systematically to build centres of excellence in higher education both to equip our students with the knowledge and skills they need and to attract more foreign students.

The challenge is clear, as are the potential dividends. The need for focus, determination and leadership is vital, as is the need for shrewd analysis, hard-nosed negotiation and tight collaboration between governments at all levels and the private sector. Canada has enormous assets that can be used as leverage in expanding our access to the emerging markets. It is time to move beyond rhetoric, sort out key priorities and marshal our resources toward clear objectives in tune with the changing global landscape.

Above all, Canada needs to set aside the comfort blanket that easy access to the US market has provided for the past half century. The US will, of course, continue to be important for the foreseeable future and, barring bizarre actions by an unpredictable Congress or the Administration, a stable outlet for much of what we produce. But we do need a broader, less complacent vision, a smart strategy, one that prompts us to train our sights rigorously on the compelling opportunities of the emerging markets, namely, as the Prime Minister stated pointedly in Guangzhou, countries who “want to buy what we produce.”

Photo: Shutterstock