As the chair of this year’s G8 Summit and co-chair of the G20 Summit, Canada will play a central role in shepherding through highly anticipated changes to the world’s financial regulatory structure. That we should happen to be the host of the summits, of course, is the luck of the draw; that others might be looking to Canada for leadership is anything but.

World leaders recognize that Canada had areas of strength that permitted it to weather the financial crisis better than most countries.

Believing that we may indeed have answers that they do not, others around the world have been paying more attention to Canadian views of late than is typically the case. For instance, the momentum has been gathering steadily in support of a global tax on financial transactions; if it does not materialize, it will be in large part because Canada’s experience demonstrates that it would not be necessary to achieve the reform goals. Similarly, the Canadian government has been strongly opposed to proposals to increase the amount of capital required to back mortgage loans, arguing — correctly — that such a move, at least in Canada’s case, would diminish one of the strengths that underpin our system.

Canada has received well-deserved recognition for the resilience of its banks and insurance companies and, as a leader, has a legitimate role to play in achieving a global consensus on financial reform. Given the stability of our economy and our banking system, many countries believe that Canadian representatives on the Basel Committee and in the G20 negotiations have the opportunity and the ability to exercise leadership in the crafting of a global framework for stability.

Certainly, there are many features of Canada’s system that are worth emulating. These, taken together, have allowed Canada to get through a storm relatively unscathed. To suggest that they are exclusively Canadian, however, is unfair. Still, it is instructive to study Canada’s experience and try to isolate the various factors that contributed to our resilience.

The first feature of the Canadian banking system is its diversification. History and evolution have caused our banks to adopt the “universal bank” model. Because Canada did not have unit banking laws, as did the United States, the national consolidation of personal banking took place here almost a century ago. The existence of a large branch network and brand equity has provided all the Canadian banks with stable retail and commercial deposits and a healthy loan-to-deposit ratio. And for more than 20 years, Canadian banks have also been permitted to own investment dealers. This adds an extra layer of diversification.

The universal bank model is inherently one of balance: it balances wholesale and retail; it balances assets and liabilities (as we collect deposits from individuals and businesses, and lend to both); and it balances the traditional banking business with the complexities of investment banking.

The universal bank model is inherently one of balance: it balances wholesale and retail; it balances assets and liabilities (as we collect deposits from individuals and businesses, and lend to both); and it balances the traditional banking business with the complexities of investment banking. Our core deposits are well diversified geographically — as are our loans, which are spread out not only across all the regions, but also among different industry sectors and consumers to diversify the risk.

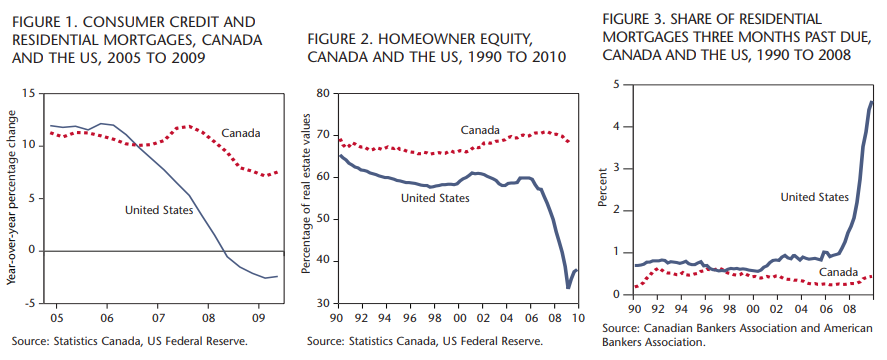

As noted, one strength of the Canadian banks is the nature of our participation in mortgage lending. Canadian banks tend to originate mortgages and hold them on their balance sheets, whereas US banks tended to securitize their mortgage assets and get them off the balance sheet — including subprime mortgages, which precipitated the financial crisis. In Canada, home mortgages exceeding 80 percent of a home’s value must be insured. This incents home buyers and homeowners to ensure they have more than 20 percent equity in their homes. This also lowers the risk of the asset, making it more attractive for banks to retain the asset on their balance sheets. On-balance-sheet mortgage assets generate steady revenue streams, which contribute significantly to the stability of Canadian banks. Increasing the risk weighting of residential mortgages — as international authorities are considering — would have the perverse effect of incenting Canadian banks to get mortgage assets off their books and move out along the risk curve (see figures 1-3).

Besides promoting diversification of risk, the universal bank model also encourages a customer-centric approach to the business. The model compels us not only to know our customers, but to know which customer we are serving.

As a universal bank, we constantly work to understand how the various businesses can complement one another, recognizing that the strength that comes from diversity requires that we strive to optimize the whole. Relying on any one business segment, however profitable, has consequences; it can call into question the stability of our business as a whole, our commitment to our other customers — and even the structure of our balance sheet.

The breadth of knowledge and experience with different financing vehicles that derives from being a universal bank was driven home during the financial crisis.

For years, we witnessed the growth of asset securitization. This growth had the positive effect of supporting the expansion of credit available for working capital. As the expansion grew in excess of the capacity of the banking system, new players emerged. Over time, the market’s belief in the seemingly unlimited liquidity of funding markets eroded the discipline of players all along the value chain. Specialized firms broadened their participation in the market beyond agency activities and became principals. And as it turned out, the degree to which managers of off-balance-sheet vehicles would feel compelled to support those entities was gravely underestimated. What almost everyone missed was that the disintermediation of the banking system had so far exceeded the capacity for any group of institutions to stand behind off-balance-sheet transactions that it would contribute to the liquidity crisis.

For those market participants lacking historic experience as extenders of credit and the breadth of perspective of a universal bank, a ready response was not available. Many failed to grasp that the underlying transactions themselves would be critically important when the market became illiquid.

It is one thing to be invested in a loan portfolio when there is a secondary market where the portfolio can be traded; in a mark-to-market world, the secondary market provides a ready reference price. But what happens when the secondary market evaporates, as it did during the financial crisis?

Institutions that have experience as extenders of credit recognize that there are at least two ways for them to get their capital returned: one way might be through a sale on the open market, but the fundamental way out is to have the borrower pay them back at maturity. If the borrower has insufficient cash flow, bankruptcy, liquidation and collateral are the third way out.

During the financial crisis, some fundamental principles unravelled: there were many times when it was hard to tell for sure who the underlying borrower was, and whether it was going to pay you back.

Many believe that Canadian banks fared as well as they did in the financial crisis simply because they had managed, by and large, to avoid these types of offbalance-sheet vehicles. This is not, in fact, the case. It was not avoidance that spared the Canadian banks but their credit management capabilities.

Good management is the second distinguishing feature of a successful financial system, and one that we have benefited from in Canada. Again, no one nation has a lock on good management, but it is the same everywhere: good management is an intentional process.

Ultimately, banking comes down to a focus on the customer, sound risk management policies and the sound judgments of employees, which is really rooted in culture. It starts with the board of directors and senior management and has to run throughout the bank. Bankers should have a strong belief in the fundamentals, particularly with respect to credit risk management. Going forward, successful banks will be ones centred on “risk culture” — a culture that centres on employee judgment in all day-to-day business decisions. Methodologies and analytics create a foundation for accountability throughout the organization, but judgment decides at what price the risk is simply not worth it. Everyone at BMO has the ability — and the obligation — to ask the question “Does this make sense?”

All the Canadian banks have an enviable record when it comes to their loan loss performance. Since 1991, BMO’s realized provisions for credit loss have averaged 0.43 percent of average loans, which represents the best performance of the group.

When I think about the reasons for this performance, I attribute it to the management of credit risk at the transaction level, and experienced, tenured and highly qualified lenders on the front line.

It is here that structure and supervision can have a material impact on loss experience. And, at the total portfolio level, it is clear that the discipline of integrated risk modelling drives more effective pricing for risk and limits portfolio concentrations. The notion of balance comes into the picture again here as well. At its best, risk discipline ensures that you find a way to make the right decision for the customer and are certain that you have been paid for it. If the balance is right, the same amount of energy goes into ensuring that customers are well served and ensuring that the bank’s capital is protected.

We have worked deliberately over the years to instill within the culture of the bank a strong respect for the fundamentals of our business, particularly with respect to credit risk management. Since the early 1990s, we have integrated “capital at risk” measurements into our risk management procedures. The concepts of expected loss, loss given default and exposure at default as the foundations of risk diversification were institutionalized by the mid-1990s and proved to be of real value during the crisis. We discovered, however, that in a severe scenario, value-at-risk models may fail to capture potential exposures.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

Following a careful review of our risk management policies, a number of principles emerged that now guide our overall approach. Of these, culture is probably the most critical.

In short, management matters. Management cultures are different among different companies, and can be different by geography. This is true in all jurisdictions and in all sectors, and it is certainly true in banking the world over, because it is the link between the business model and the regulatory structure.

The regulatory and supervisory framework in Canada, clearly, is the third advantage from which we have benefited. Our system is not perfect, but it served us exceptionally well during the financial crisis.

Canada’s regulatory and supervisory authorities were much more conservative regarding capital levels, and they raised their requirements when warning signals appeared in 2007. That conservatism extended to their definitions of what qualified as capital. The fact that Canadian banks are universal banks and that capital ratios are applied on a consolidated basis ensured that the investment banking activities did not become overleveraged.

Canadian regulators and supervisors also encourage discussions among themselves, resisting any temptation to operate in silos. Looking back at the global financial crisis, I think one of the important and extremely positive characteristics of the Canadian experience was the early, open and frequent dialogue between the Minister of Finance, the Governor of the Bank of Canada, the Superintendent of Financial Institutions and the CEOs of the banks and insurers. There is a high level of trust between all of us — which ultimately served Canada and its financial system well.

Frequent conversations between regulators and the regulated minimize the risk of misunderstanding: one is attentive not only to the words that are spoken, but also to the intent behind them.

The strength of Canada’s regulations and supervision, to listen to some commentators, is its focus on principles rather than rules. I think the distinction is exaggerated. One cannot have one without the other, I would argue, and Canada has both.

A rules-only system has no obligation to manage for the intent of the rules, which leads to a culture of living by the letter of the law rather than its spirit. That said, principles without rules can be too open to interpretation. Rules can be very helpful, because they deal with specifics. If the discussion is always hovering at the conceptual level, it can be difficult to apply it to the situation at hand.

What distinguishes Canada’s regulatory approach is not that it is principles-based as distinct from rules-based; it is the insistence that the people who follow the rules have a clear understanding of the principles underlying them. It is no different than what we expect from teaching our children the difference between right and wrong; we hope that the principles we set out will supply all the context they need to be able to weigh a novel set of circumstances and make an independent judgment.

The diversified structure of Canada’s financial system, good management and an effective regulatory and supervisory structure reinforced by good dialogue when it mattered most — plus a little bit of good fortune — produced the conditions that allowed Canada to weather the financial crisis. With those conditions in place, Canadian financial institutions succeeded in making the right choices to insulate themselves from many of the issues that brought down other financial institutions around the world.

The key choice we made was to maintain sturdy capital levels. While other systems around the world allowed capital ratios to slip to bare minimums, Canada’s regulators set higher requirements and encouraged us to exceed them. In addition, regulators elsewhere allowed banks to have significant amounts of non-common equity capital to satisfy tier 1 requirements, while we in Canada did not.

There is a clear consensus that one of the root causes of the financial crisis was excessive leverage in many of the world’s banks and investment dealers, exacerbated by a lack of common standards for the quality and level of capital. The remedy, undoubtedly, will be higher standards and common definitions of what should constitute tier 1 capital.

Yet even under new, higher standards — though, as yet, undetermined — the Canadian banks are very likely to be among the best capitalized.

The G20 Summit in Toronto at the end of June will consider the various proposals for financial reform, and will attempt to harmonize the processes already under way in developed countries.

The most significant reform contemplated in Canada is the creation of a national securities regulator, which will streamline and harmonize the regulatory function here.

In terms of reforms under way elsewhere at the national level, the real attention is on the United States, where some of the most sweeping changes in decades are being contemplated. Because of the central role it plays in world markets, the US needs to complete these reforms as quickly as possible. This is a critical precondition to having a global discussion about what is the right level of capital — which is the most pressing issue to resolve.

The direction for the global discussion was set at last year’s G20 meeting in Pittsburgh, where world leaders agreed that reforms should include consolidated regulation, caps on leverage, more and better capital requirements, mutual assessments of national systems and other reforms that will, hopefully, make international cooperation more effective and lessen the likelihood of another global financial crisis such as we experienced between 2007 and 2009.

The hope of achieving consensus is still strong. In the months since Pittsburgh, however, some important differences of opinion have arisen that threaten to derail the very goal of a consistent global reform process — because unless reforms are consistent across the board, the lure of regulatory arbitrage will inevitably find a new batch of risk takers whose actions could be capable of putting the broader system in jeopardy again.

It would be a major cause for concern if the reforms simply stalled due to a lack of stamina — for example, if policy-makers were to ease up on their commitment to deal with the issues, now that there are signs everywhere that the recession is over or at least ending.

We are hopeful this won’t happen, because, surely, the one thing we can agree on is that the status quo failed us, and that financial reform is necessary and to the benefit of all market participants. And as they develop these reforms, policy-makers are right to be looking broadly for inspiration, not just in Canada but wherever they can find it.

Our financial system in Canada performed well in the crisis because the parts of the system worked well together. We demonstrated the importance of not having “white space” and overlap when it comes to regulation and supervision, when gaps and ambiguity could threaten the system.

We have a strong and balanced universal bank model. We have empowered regulators and supervisors. We had higher capital requirements than many other nations. Our regulatory system is principles-based, as well as prescriptive, to ensure that bankers understand the intent of the rules and manage for safety and soundness. Going forward, there are no single fixes. There is a risk now of global financial reform not dealing with the causes and needed reforms on a systemic basis, and being overly reliant on higher capital. Canada, as co-chair of the G20 Summit, has a legitimate leadership role to play in achieving a global consensus on financial reform, as we move from crisis to stability. For banks that are well capitalized, like the Canadian banks, we expect to see an unprecedented period of opportunity to grow our businesses and to be well compensated for the risks we retain.

Photo: Shutterstock