Today, the world faces two truly momentous trends. The first is primarily political and has major economic ramifications. The second is primarily economic, but has huge political ramifications. First, the economic collapse of the traditional communist system is driving tremendous political changes, both in the old Soviet Union, in China and in most countries around the world. These countries have been forced to rediscover the principles of Adam Smith, the role of the market price system and modern mixed economies; to reduce the role of government; and to allow a thriving private sector, private property, stock exchanges and all the tools of modern finance — venture capital, IPOs and publicly listed corporations.

The second trend is more immediate, equally momentous and more immediately relevant to the North American economy. That is, the spectacular growth in Asia, which was led by Japan, and is anchored in a profoundly rich economic structure built around private-sector, domestic-led growth; a superbly educated population; and a voracious appetite for the newest and best technological and production processes available anywhere. Now, at the start of this new century, the Asian region accounts for one-third of the world GNP. It embodies the richest country, measured by per capita income — Japan, the hugely successful Asian Tiger — but now extends to emerging markets like Vietnam, Indonesia, the Philippines and the huge-population markets of India and China. Globalization and the rise of Asia should be Canada’s economic priority.

Travel anywhere within Asia and the importance of Japan is noticeable: in the levels of foreign investment; in the Japanese brand names; in the desire by local companies to benchmark their performance against leading firms like Toyota, Honda or Canon; and in the growing desire to have young people study at Japanese universities.

Much is made of the rise of China as the most powerful of the BRIC countries (Brazil, Russia, India and China). Indeed, the BRIC countries’ GDPs will be equal to those of the G7 countries in less than 20 years, according to present linear projections. But another trend, which is rarely discussed openly or publicly, is the new corporate nexus between India, China and Japan. This quiet shift is the new context in which to explore the present bilateral relationships between Canada and countries in Asia, with potential bilateral free trade agreements between Japan, China and South Korea.

These trends relate to the unalterable trends of globalization. The three main drivers of globalization — financial capital, technology, and trade — are integrating countries and their industries in ways that are unprecedented, even a generation ago. Clearly, the impact of China and India in the global business community has no precedent. It forces all managers to ask a simple question: Do we have an India or a China strategy for exports, investment, strategic alliances and talent search? From the very limited strategic perspective of the nation state, India and China affect global competition in direct and indirect ways. The direct ways are the new listing of Indian and Chinese companies that want to be global multinational enterprises (MNEs). The stereotype of Indian and Chinese companies — information technology (IT) and software for India, low-cost labour manufacturing for China — ignores the range of sectors from advanced household appliances to semiconductors; from telecommunications to space technologies — in which these two countries have already developed significant innovations. But India and China do count, not just because of their population and trained labour force, but because they need to import so many technologies, managers and products. That is why they have a profound indirect impact. They have their own strategies to link with other countries: joint ventures; research alliances; direct investments abroad; subcontracting in rich countries; and building global supply chains for parts, components and finished products and the means of distributing them to overseas markets.

India and China are only the start of the convulsions occurring in global business. Two entire continents, South America and Africa, are awakening to globalization. No two areas are so rich in natural resources. No two continents could affect so many industries with sophisticated innovation — from agribusiness to petroleum, minerals to fashion. But these continents need to make their own choices. Some countries want to play the global game. Who will be left out? The same issues apply to the Middle East, which is steeped in civil war and ethnic and religious conflicts but has staggering wealth. Even a cursory check of the changes occurring in Dubai, for example, raises the basic question for the region: the answer shouldn’t be why the problems but why not the global solutions.

Canadians generally pride themselves on their country’s role as a middle power, as a joiner of a host of multilateral institutions: the WTO, the UN, UNESCO, NATO, the Commonwealth; la Francophonie; NAFTA, the G7 and G20; the World Bank, the IMF and now the OAS. This alphabet of institutions is an important reminder to Canadians about the world’s interdependence and reliance on peace for wealth creation through an open trading system. Canada’s soft power has allowed this country, located in the middle of the two military superpowers, the Soviet Union and the United States, to punch above its weight, as measured by defence spending, population or investment in science. But is Canada playing its cards well? Is it keeping up with the Joneses, as Americans might ask, which might include getting a seat on the UN Security Council?

More specifically, has this widespread participation in international institutions blinded Canadians to what is a startling reality; namely, that almost threequarters of our export trade is with one country, the United States, and of Canada’s 1,200 export products, only 26 account for slightly less than 50 percent of total exports. The United States and Japan are the only two technological superpowers, and Canada, with its low research spending, increasingly risks losing out in the financial and technological trends overtaking the world economy. This is not a new warning: globalization means a new era of 24-hour trading; stunning new advances in such areas as microelectronics, biotechnology and advanced materials; and trade developments that are profoundly challenging the often fleeting advantage of a commodity-based economy.

Now, at the start of this new century, the Asian region accounts for one-third of the world GNP. It embodies the richest country, measured by per capita income — Japan, the hugely successful Asian Tiger — but now extends to emerging markets like Vietnam, Indonesia, the Philippines and the hugepopulation markets of India and China. Globalization and the rise of Asia should be Canada’s economic priority.

The arc of history now favours Asia’s development. China’s output has increased sevenfold in 20 years, and on some accounts, its GNP rivals that of the United States. For more than two decades, Asia’s high but steady growth; its position combining the huge, low-cost labour of China; and the emerging markets of Indonesia and Vietnam have combined with the huge intellectual investments by firms from Japan, Korea, Singapore, Hong Kong and other Asian Tigers. It has cultivated some of the most successful technology-driven multinationals, the world’s largest trading firms and the most technologically literate population in the world. Where would the Ontario auto industry be today without the sophisticated Japanese car plants of Toyota, Honda and Suzuki? Today, Japan is leading the Asian charge for a new era of major overseas investments — in energy, autos, high-tech manufacturing, telecommunications, computers and software, and even retail. This is in not only the United States (where the strong yen relative to the dollar is another advantage), or in the European Community, but it is a new global force, the corporate alliances with India and China. Canada is in a catch-up phase in most of the Asia countries.

Japan’s rising growth and technological development have been emulated throughout Southeast Asia and now China and suggest new Asian organizations and institutions. Australia’s initiative for a Pacific Rim organization and a free trade agreement with Japan are examples of these, but the new context suggests four basic options over the next decade, or even sooner. The first option is the status quo: separate national economies, but growing trade and investment interdependence, led primarily by Japan’s export of capital, technology and aid, but also from South Korea, Malaysia and China, reinforced, to be sure, by a strong American military defence and economic presence in the region.

A second option, and one that is likely to happen sooner rather than later, is an administrative organization, such as an OECD of the Pacific, modelled on the Paris-based organization of the rich 30 nations of the West. A third option of more serious change would be a Pacific trade block, now called tentatively the Trans-Pacific Partnership, which currently excludes Canada, Japan and Mexico, but no one seriously wants competing trade blocks in Asia or the rise of virulent US protectionism aimed specifically at China. The fourth, even more distant option is the rise of a yen block, or a renminbi block, based on the yen or the renminbi serving in time as a convertible currency alternative to the dollar or the euro and acting as a reserve currency for Asian monetary authorities. Some steps already exist, such as a renminbi bond market and renminbi bank deposits in Hong Kong, and foreign central banks have been able to hold renminbi deposits since August 2010. Whether the Chinese government continues to pursue its policy of promoting the use of the renminbi as a reserve remains an open question, where manufacturing exporters stand to lose international competitiveness, one of the reasons both the mark and the yen remained below the dollar in currency rankings.

Slowly, perhaps reluctantly, corporate Canada has responded to these challenges, in part by the forward-looking strategies of the federal government, now advancing free trade agreements with Europe, Japan, India and South Korea. These trade negotiations build on the success of the trade agreements with the United States and Mexico and in the absence of real progress on the stalled Doha multilateral round of trade talks. The Trans-Pacific Partnership round is a dramatic shift of thinking in the works, just like the proposed free trade agreement with China, Japan and South Korea.

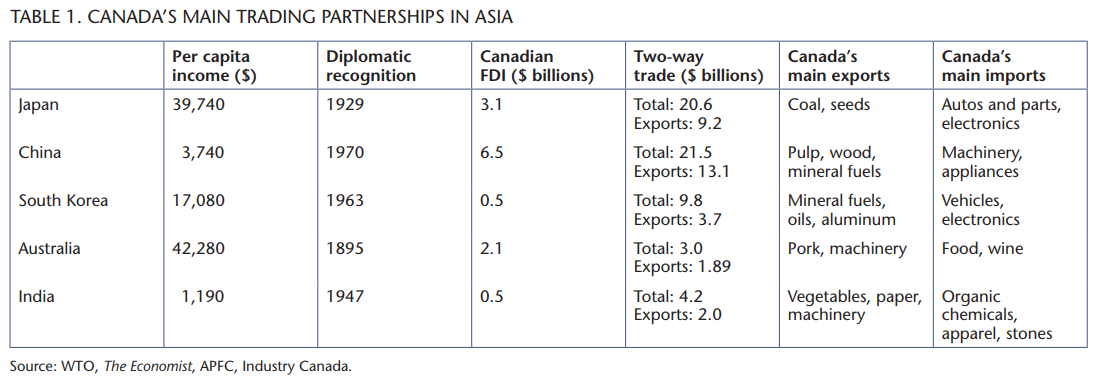

In the past four decades, in part arising from Prime Minister Pierre Trudeau’s 1970 decision to recognize China (in advance of America’s recognition in 1979), Canada has cultivated closer ties with Asia, such as regular ministerial visits, bilateral meetings with heads of state, trade missions, opening of regional consulates beyond the national capitals and more commercial ties between leading business groups and industry associations. In reality, however, the trend of Canadian trade and investment bilateral relations is friendly but sporadic, successful but hardly overwhelming (table 1). Each Asian country has its own domestic problems to sort out, starting with protectionist forces in agriculture and highly protected national champion sectors.

How should Canada position itself not only for Asia’s development and Canada’s benefit, but also for the benefit of all of North America? The global changes in trade, investment, finance and technology now offer Canada new opportunities to become a truly significant player in the global economy, matching its unique, three-ocean geography straddling the largest and most dynamic market, the United States —but not forever. Properly aligned strategies in energy, national resources, higher education and financial services, with each of the major stakeholders playing a pivotal role, would make Canada uniquely qualified to link Asia with all of North America. Consider the case of transportation, so necessary to build commerce, trade flows and high-paying jobs across this vast, disparate nation.

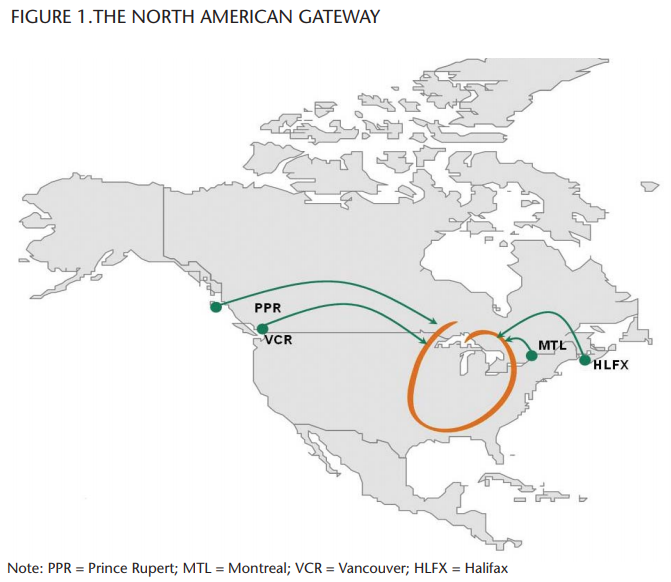

Today, Canada has a rare opportunity to be a transportation leader involving global supply chains with Asia (figure 1). As Canadian leadership did with the transcontinental rails, the St. Lawrence Seaway and the TransCanada Highway, today’s leadership can make Canada the 21st-century logistics gateway to North America for the flow of commerce from Asia and Europe to this entire continent. Canada, bordering on three oceans, has the potential to enhance world-class container ports — Vancouver and Prince Rupert on the Pacific, and Halifax and Montreal on the Atlantic — linked with quality intermodal rail and truck operations to most of the population of North America. The United States, facing continuing political gridlock, won’t seize this opportunity, and local stakeholders won’t let the needed ports, rails, pipelines and highways be built.

National transportation policies must be integrated with Asian trading hubs and new supply chain configurations. Up to one-third of the content of exports of goods and services now come from components and parts and sub-assembly from other countries’ exports.

Closer inspection shows Canada’s unique advantages: the flow of commerce within North America is becoming increasingly congested, reducing corporate productivity through delays and traffic congestion, and lowering overall productivity and driving up all costs. As shown by numerous studies over many years, including the American Society of Civil Engineer’s Report Card, the United States federal and state investments in port, rail, road and airport capacity are increasingly constrained by shortage of money, social concerns about noise, wasted fuel, environmental challenges, traffic congestion and the politics of partisan gridlock among stakeholders.

Global trade requires ever bigger ships and larger aircraft, fewer but more strategic port developments, shifting traffic corridors through the Panama and Suez canals and global gateways, and new, integrated technological and communications links with inland transportation (freight forwarders, transport expediters, third-party logistic providers, railways and trucking). National transportation policies must be integrated with Asian trading hubs and new supply chain configurations. Up to one-third of the content of exports of goods and services now come from exports of components and parts and sub-assembly from other countries’ exports.

Globalization and the new era of Asian growth dictate why Canadian companies and their employees must refocus their thinking. Global logistics have a transcontinental reach and call for new measures of human resource training, new forms of communications and unprecedented measures of global cooperation, strategic alliances and planning. This collaborative integration of suppliers, corporations and customers (industrial and consumer) now constitute what the Economist calls the “physical Internet.” Global supply chains prefer just-in-time systems, but failure to act quickly allows would-be partners to take alternative strategic action based on just-in-case.

This dimension forces new thinking and new network approaches to understand how Canadian industry fits into global transportation supply chains, employed the world’s best security, IT systems, and state-of-the-art infrastructure. Because neither the US-Canada nor the NAFTA trade agreements linked trade flows with transportation issues, Canada can design its own approach as a North American gateway. Canada needs to invest in a national strategy, linking the Pacific Coast ports, the Atlantic Coast ports and the St. Lawrence-Great Lakes corridor. But any initiatives along these lines require a massive educational process, showing Canadians why the country intends to be a global player in international trade and is willing to invest the time and money to design a transportation system that has global reach and global impact.

Canada can’t wait because the world is not standing still. From Thailand to Vietnam, from new ports in China to well-established ports like Singapore and Hong Kong, there are new gateway linkages on the East Coast of the United States. Three strategic stakeholders — shipping companies, terminal operators and port facilities (air cargo and sea ports) — are accelerating corporate transformation as part of changing global and regional trade strategies.

China alone has shifted the global trade axis away from the Atlantic-centred market of Europe-North America to the Pacific Rim markets like Japan, China and India, and away from the traditional developed triad economies (Europe, North America and Japan) to the emerging markets around the world. This new mix, even when China is excluded, now accounts for one-third of world trade (28.8 percent of merchandise exports, 26.3 percent of imports). China adds about 5.5 percent, but its trade is growing at 20-25 percent per year.

For the many states and provinces, with their abundant natural resources and trade links in potash, wheat, coal and energy with Japan and other Asian countries, the attractions across the Pacific are great even without China.

The second trend is equally profound for the global economy. East Asian economies in Asia are following a similar path to Japan’s in the 1970s and 1980s, now being emulated by China. They are accelerating their industrial growth by moving up the value chain to more sophisticated products, components and technologies. All over Asia, factories operate with state-of-the-art equipment, the latest industrial processes imported from Japan, the United States or Europe, with managers and engineers trained in reputable foreign universities. Despite growing trade integration among leading regional groupings, led by Europe with the highest level of intra-regional trade, at 71 percent in 2011, intra-regional trade in Asia is climbing steadily, at 53 percent, higher in fact than NAFTA at 50 percent intra-regional integration.

These trade patterns and container flows (figure 2) affect other factors, such as physical infrastructure and IT and technical prowess, including skilled workers, tools for productivity enhancement and managerial qualifications. What was true two decades ago about Japan, which trained engineers while the United States trained lawyers, now applies to Asia: India and China each produce more engineers than Europe and the United States combined. India and China are shifting their industrial production away from labour-intensive and commodity-intensive product lines to sophisticated technology-intensive output, as Japan did a generation ago.

High-value products and services become trade-intensive and become part of global supply chains.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

The rise of India and China, following the startling rise of the Asian economies in the last decade, and Japan a generation ago, all represent a tectonic shift in the global economy. China, with over a billion people — 300 million of them attending elementary school — by itself shifts the global economic order toward Asia. Combined with India, with another billion people, or 40 percent of the world’s population, these two countries have immediate and long-term effects on the global economy, global methods of governance and global trade regimes, including bilateral trade agreements. North America, with a legacy of immigration, educational ties, trade and transportation links, stands to gain enormously from its Pacific Ocean location. For the many states and provinces, with their abundant natural resources and trade links in potash, wheat, coal and energy with Japan and other Asian countries, the attractions across the Pacific are great even without China. Less than 25 percent of world trade, measured by value, occurs with countries sharing a land border (China has 14 land borders — the United States has only two).

Global gateways — ocean ports (e.g., Singapore, Shanghai, Los Angeles) and mega-hub airports (e.g., Chicago, Tokyo, Frankfurt and London’s Heathrow) — now revolutionize the tools of corporate logistics. There are new trade routes, new transportation modes like ever larger ships, new forms of online tracking systems, new container modes of transport, intermodal transport and techniques to load, unload quickly and re-sort loads. There is growing awareness of pollution on the oceans and the carbon imprint of combining long distance with old, obsolete planes and ships, and rising political attention to unregulated transport in emerging market countries.

Canadians have slowly increased their Asian trade exposure but too often with a mindset focused on North America. Much of the transport focus has been through the prism of north-south and especially the states lying contiguous to Ontario and Quebec. Since the Canada-US Free Trade Agreement was signed, later expanded to become the North American Free Trade Agreement, Canadians have reoriented their trade links away from a national focus (east-west) only to a North American focus (north-south). In transport and trade policy, this has culminated in new arrangements, such as the Open Skies air pact with the United States and a powerful railway system developed by CN, not only across Canada (like rival CP), but north-south to the Gulf of Mexico, with a large terminus in Memphis and strong market share in big container markets like Memphis, Detroit and Chicago.

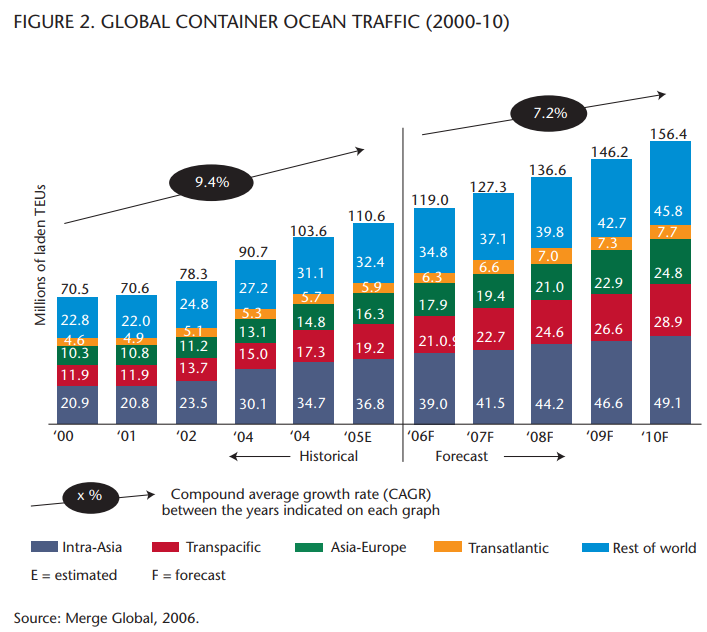

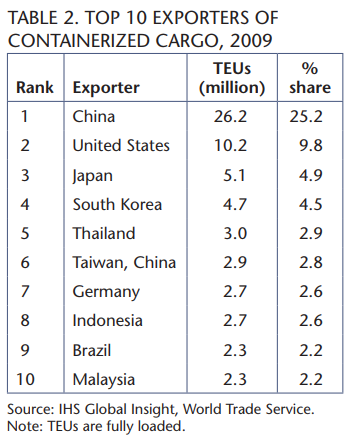

For over 30 years, Canadian policy-makers have been concerned with the country’s gateway strategies — transportation links via air, oceans, Great Lakes and rail — that shape Canada’s exports and imports flows. Initially, Japan’s import needs were one of the first priorities, as that country’s dramatic growth led to an apparently insatiable demand for Canadian raw materials — timber, coal, grains, pulp and paper — and an equally dramatic rise of Japanese exports like automobiles and consumer electronics. Container flows were two ways. As Pacific Rim trade with North America grew, West Coastports—Los Angeles and Long Beach, Seattle and Vancouver — have faced increasing port congestion, as the flow of containers across the Pacific skyrocketed, from 2 million TEUs in 1970 to 20 million TEUs in 2009 (table 2). (A TEU is a transport term meaning a 20-foot equivalent unit. Most containers in North America are 40 feet, some are 53 feet.)

Global logistics are changing the patterns of sourcing, transportation modes, supply chain management and indeed corporate strategy itself, as firms attempt to reposition their market domain in a world of global competition. Canada has the opportunity to be the North American gateway for goods and services from Asia for the entire continent, if Canada at large seizes the opportunities. Today, Canada has focused on five separate gateway strategies, linking transportation needs to local partnerships and stakeholders. From east to west, the five gateways are these:

- Atlantic Gateway

- Ontario-Quebec Continental

- Gateway

- CentrePort

- Arctic Gateway

- Pacific Gateway

On a global basis, Canada’s constant challenge is to recognize that international trade is based on an ocean-going transportation system. Seaborne traffic covers over 90 percent of international trade. The containerized portion of this passed a milestone in 2004 with 360 million TEU of throughput in the world’s ports. For Canada, the challenge now is to design a national transportation system that is state of the art to deal with the world’s biggest market, the United States, and that reinforces Asia’s role in that competitive market.

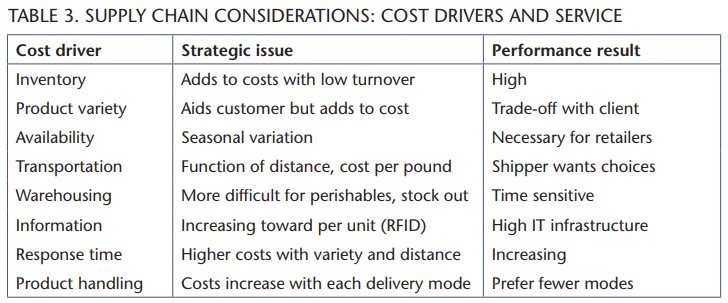

Dramatic trends are revolutionizing the management of global supply chains and its varying components (table 3). Information technology pervades all aspects of complex operating systems, but some sectors have trailed state-of-the-art developments — transportation is one, hospitals are a second. This position is changing rapidly. At the first level are the components of the transport system — for example, the ships, terminals, trucks and ports. As each component part becomes more complex, so do the intermodal connections, which are now best seen as complicated networks requiring on-line communications tools that themselves form a network that is stretched across the continents, using satellite transmission, global positioning systems (GPS), and sophisticated transmission devices, software and bar codes.

Companies have to balance two potentially competing systems: the management of low-cost shipping across long distances, which means a mix of ocean shipping (for lower cost per unit) and intermodal transport to meet just-in-time requirements for final deliveries.

In the postwar period, Japan’s industrial growth was the fastest wealth-creation economy in world history. This is happening today in Asia broadly, led by China, the world’s largest exporter in 2010 and likely to become the world’s largest trading nation by 2015.

Increasingly larger ships or aircraft for air cargo require new ground-to-air or ocean-to-land communications devices that provide information for the first mile and the last mile of the journey of a container or parcel. This means a dramatic shift in port-to-port or airport-to-airport links. The communications must stretch from the first mile — the factories where goods are made and shipped overland — to the last mile — where the goods leave the port of embarkation and are shipped overland to the end user. In the past, these communications tools were national or regional in scope, as trade focused on regions with geographic proximity — for example, Nova Scotia to Ontario, Washington State to California or Suez to Germany.

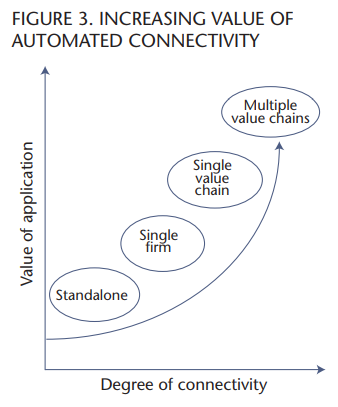

Low-cost manufacturing, growing country and regional concentration on national comparative advantage, technological sophistication, economic geography and just-in-time manufacturing — these factors alone and in combination — have all changed the information logistics necessary for global trade. Too often, domestic firms have pursued low-cost advantages of cheap labour in China and India, where the differences are 20:1, but often ignoring the enormous increases in transportation and logistics costs from low-cost inland factories. In China and India, for example, inland factories lack easy access to roads and inland water routes to move goods to deep-water ports. Transportation bottlenecks on roads, highways and railroads, plus complications in electricity supply, have increased the cost of logistics and transportation. IT connectivity, depicted in figure 3, illustrates how international supply chains form a complex organizational network. Indeed, a major American trucking company has invested in China to serve as an inland road carrier for Chinese factories but also as a freight-forwarder for Chinese exporters.

At the second level are the global supply chains of multinational manufacturers and global retailers which depend on imported parts, components and finished products. Not only are supply chains impaired because of transportation bottlenecks, but tracking of goods through the supply chain needs to become fully integrated with a global forecasting schedule. As Canadian shippers, retailers and manufacturers know well, when the US government imposed new preclearance conditions in the post-9/11 environment for customs and security and the US Treasury transferred its customs department to the Department of Homeland Security, both importers and exporters have had to re-examine their IT infrastructure.

The transportation firms as well as the individual importing and exporting countries now must invest heavily in IT infrastructure — software, hardware and new radio frequency systems, mobile phones and BlackBerrys. On a global basis, this IT imperative is especially complex because there is no common standard architecture or IT platform. Increasingly, from China to the United States, the system preference is wireless communications across all components of the transport value chain and all elements of the supply chain, away from the tyranny of cables and copper-wire based systems common in North America, allowing newer entrants (countries and companies) to join standardized 4-G and 5-G wireless networks, including with Internet-based platforms.

An example of the profound changes taking place in global transport is the case of the CN North American rail network of 30,000 kilometres of track linking three coasts. In the past, over 1,000 workers at CN managed repairs and inspections but were isolated from overall scheduling and tracking of its 4.8 million carloads of freight. Performance across the system was measured in days. Now, massive investments in IT and management systems involving mobile work stations, BlackBerrys and laptop computers provide an integrated monitoring system, with a clear tracking capability customized for each customer of CN’s freight operations across the North American continent.

New IT systems allow an online, integrated end-user-functional model. Global retailers and manufacturers are applying combinations of radio frequency identification systems (RFID) and GPS. Bar codes, of course, are now a standard tool applied to everyday items, whether books or the items in a shopping cart or packages of courier companies like FedEx or UPS.

New software systems illustrate the pent-up demand for IT investments to solve transportation bottlenecks, not only to contain costs like stockouts, fuel consumption and shrinking order delivery times, but to deal with border security and enterprise resource planning for inter-modal transport. Best-practice firms are increasing their connectivity tools to involve multiple value chains, and pushing the integration into easy-to-use tools, such as cell phones, PDAs (personal digital assistants) like BlackBerrys and other electronic tools like digital smart tags and de-activation devices.

Around the world, production and location decisions may change, as firms wish to source production of parts and components closer to manufacturing and service functions. This impact is especially complicated for North American firms, because the continent has been the main source of inter-regional competition. The rise of Asia, from Japan in the 1980s to China and India today, forces a fresh look at global logistics and the consequences of a truly North American Gateway. Energy costs and currency fluctuations add an element of risk management, thus requiring closer integration of tasks from the board to operating managers. Truly, the firm is only as strong as its weakest link. As more goods flow across borders, the composition of trade changes: bigger economies export more than small economies, the weight of goods to the value of goods changes (i.e., the weight/value ratio tends to drop, away from bulk goods) and more goods embody parts, components and other inputs, including services and IT, from foreign suppliers.

Global trade, regardless of country, is now accompanied by more than physical infrastructure. Export firms differ from domestic companies because the export market, even when many common features exist (laws, language, distribution channels), carries a higher risk premium: risk is a function of the differences in markets, not the similarities. And companies must pay for this risk up front, although the risks may be mitigated later by higher payoffs (profits) once the lessons of the new market are learned. Various risk elements — quality of infrastructure, IT systems, labour unrest, currency fluctuations and regulatory uncertainty — reinforce each other, because they constantly reduce or add to cost per unit of output, and shorten or lengthen the time to manage coordination.

What brings these elements together is new alliances and partnerships. No longer is the question of global logistics an operation planning tool for domestic advantage. What happens on one side of the world now affects what occurs in the local neighbourhood. To some, the world may be flat, a happy digital view promoted by Thomas Friedman. But in global logistics, it is a very bumpy, complicated ride. The failure of so many domestic manufacturers and retailers too often illustrates that the back-office tool of global logistics is downplayed by senior management and the boardroom. For some Canadian sectors — the railroads, retailers like Canadian Tire, the fertilizer producers, Global Terminals and selected others — there are notable exceptions.

The leadership of the federal and provincial governments and of Canada’s leading corporations can and should focus on high-leverage investments to keep Canada at the forefront.

In the postwar period, Japan’s industrial growth was the fastest wealth-creation economy in world history. This is happening today in Asia broadly, led by China, the world’s largest exporter in 2010 and likely to become the world’s largest trading nation by 2015. However, serious analysis of the Asian economies illuminates their many corporate strengths, their will to succeed, their capacity to absorb and apply technology, and their desire to combine Western industrial and entrepreneurial strengths with Asian Confucian culture, their respect for education and family, and long-term horizons, measured in decades, not quarterly returns. Fortunately, Canadians are now aware of the growing relations with Asia, and both corporate and government policy portends a real signal of future cooperation across a wide spectrum of global and bilateral issues.

Canada needs to stay in this game as success means something to virtually everyone in the country. As David Gillen, professor of transportation at the University of British Columbia, observes, “This gateway is as much about stimulating exports from North America as it is about facilitating the effective flow of containers into North America. Imports plus exports, the service industries that support industrial activities and the governments that design long term policies mean that all of Canada will all benefit.”

The leadership of the federal and provincial governments and of Canada’s leading corporations can and should focus on high-leverage investments to keep Canada at the forefront. For government these include the following:

- Articulating a North American gateway strategy for Canada and the provinces

- Cultivating federal and provincial departments of trade, transportation and industry to coordinate North American gateway initiatives and have local champions for the strategy, expediting permitting and approvals, helping resolve First Nations issues effectively once and for all and, where necessary, facilitating financing needed for key investments

- Encouraging Canadian corporate participants to become more active in global supply chains, to advance productivity and innovation

- In a digital age, Canadian embassies in Asia need fewer diplomats and more bilingual commercial officers on the ground who are attuned to local business opportunities to link Canadian strengths at home and increase exporting in more products and services

- Assigning more commercial officers to key countries staffed with experienced, in-country personnel of appropriate stature and remuneration to assist Canada’s companies in participating in these export markets

Canada’s corporate leadership must make investments in the following:

- Developing in-market intelligence by opening commercial offices in Asian capitals and key cities, like CN and Magna in Shanghai or Manulife in Tokyo and Ho Chi Minh City

- Encouraging Canadian firms to learn the critical success factor of expatriate competition — feet on the ground, talent in the towers, using in-country expats and locals to leverage in-country assets for competitive advantage. To win, Asia is no place to play “on the cheap.” Formalizing effective programs for expatriate deployment in foreign markets, linking especially SMEs to new markets, Asian trading firms and large retailers and corporate groups

- Making an investment commitment, and foregoing short-term profitability for a long-term trade position in Asian markets

The “best practice” companies see the global world not as a challenge but an immense opportunity. For the first time ever, companies have learned to link the immense talents of rich and poor countries in unprecedented ways. The new global linkages combine physical resources; data flows and digital communications and financial flows combine to integrate international economies, some more than others. This view is apparent in the consolidation of global logistics through mergers and takeovers, on an ever-increasing scale, and in the need for a critical mass of skills. Response time should be a measure of customer need, not internal lead times. The opportunity to win in Asia is Canada’s to lose.

Photo: Shutterstock