Canada’s retirement income system has attracted much attention in recent years, and there have been pension reform proposals at the national and provincial levels. Many of the proposed reforms are thoughtful and appear to be feasible. However, as this debate has unfolded policy analysts as well as governments have failed to examine two critical questions. The answers to these questions may raise a lot of doubt about the nature, timing and extent of reform that is needed. First, is greater longevity really a problem for pensions? Second, what implications will changing trends toward work and retirement have in terms of the amount of income that is needed in old age?

Without clear answers to these two questions some of the reforms proposed to date, including those being debated in the current federal election, could have unintended and possibly large negative consequences. The good news is we can fill these gaps in our knowledge relatively quickly, but only if policy-makers and researchers are truly committed to evidence-based analysis.

In describing the current policy debate on pensions and the retirement income system, I refer to the latest, and one of the best, papers on the subject Lower Risk, Higher Reward: Renewing Canada’s Retirement Income System, by Tyler Meredith. This paper looks comprehensively at the challenges facing current and future retirees. It makes several well-argued policy recommendations, most of which reflect a broad consensus in the literature on the range of different policy issues involved. Meredith’s recommendations include the following:

- Enhance OAS/GIS benefits for singles with the goal of providing a minimum benefit equal to the poverty threshold.

- Ensure that eligibility for pension and retirement benefits better reflects long-run changes in longevity, including mechanisms to assist those who cannot work longer.

- Introduce a coordinated plan of increased mandatory retirement savings specifically focused on individuals who are not currently members of a private workplace pension plan. This can be done either by enhancing the CPP/QPP nationally or by revamping the federal legal framework for the Pooled Registered Pension Plan, with the goal of implementing Quebec’s Voluntary Retirement Savings Plan on nationally.

- Ensure regular reporting by the Chief Actuary of Canada on the state of income replacement for both current and projected future cohorts of retirees.

As is the case in most of the literature in this area, the paper starts from the presumption that increasing longevity is a major threat to the retirement security of many middle-aged and middle-income workers. In short, the argument goes, more of us than ever before do not have a pension. This fact, combined with longer life expectancy, means that an important cross-section of workers is headed for big trouble.

Is this really true? Without a doubt, not being part of a workplace pension increases the potential risk of undersaving. In what way this might interact with longevity and what kind of problem this may present in the future is not, however, clear.

How much undersaving would occur if, by the time new pension entitlements are phased-in, today’s cohort of workers (future retirees) continue to work past the commonly assumed retirement age of 65? Will the problem become larger or smaller over time? Is it likely to be a big or small problem when compared with the multitude of social issues that policy should address? Could other retirement income issues become even more pressing? We don’t know the answer to these questions.

The critical deficiency in much of the policy analysis in this area is that we look at problems in a static context; that is, we assume people who undersave during their working lives retire at the same time as everyone else, which on paper results in a drop in living standards. This leaves no room for possible changes in people’s behaviour, either in response to the challenge of undersaving later in life, or simply because they want the flexibility of working later in life.

“This raises the potential for a large misallocation of public funds.”

In a 2012 commentary published by the C. D. Howe Institute and in the recent IRPP Policy Horizons Essay, I argued that we may be overstating the extent of this retirement savings problem because we have we failed to grasp just how important changing patterns of work and retirement are to this equation. This could have many important consequences for how we think about not just pensions, but also larger social issues like poverty, inequality and aging policy.

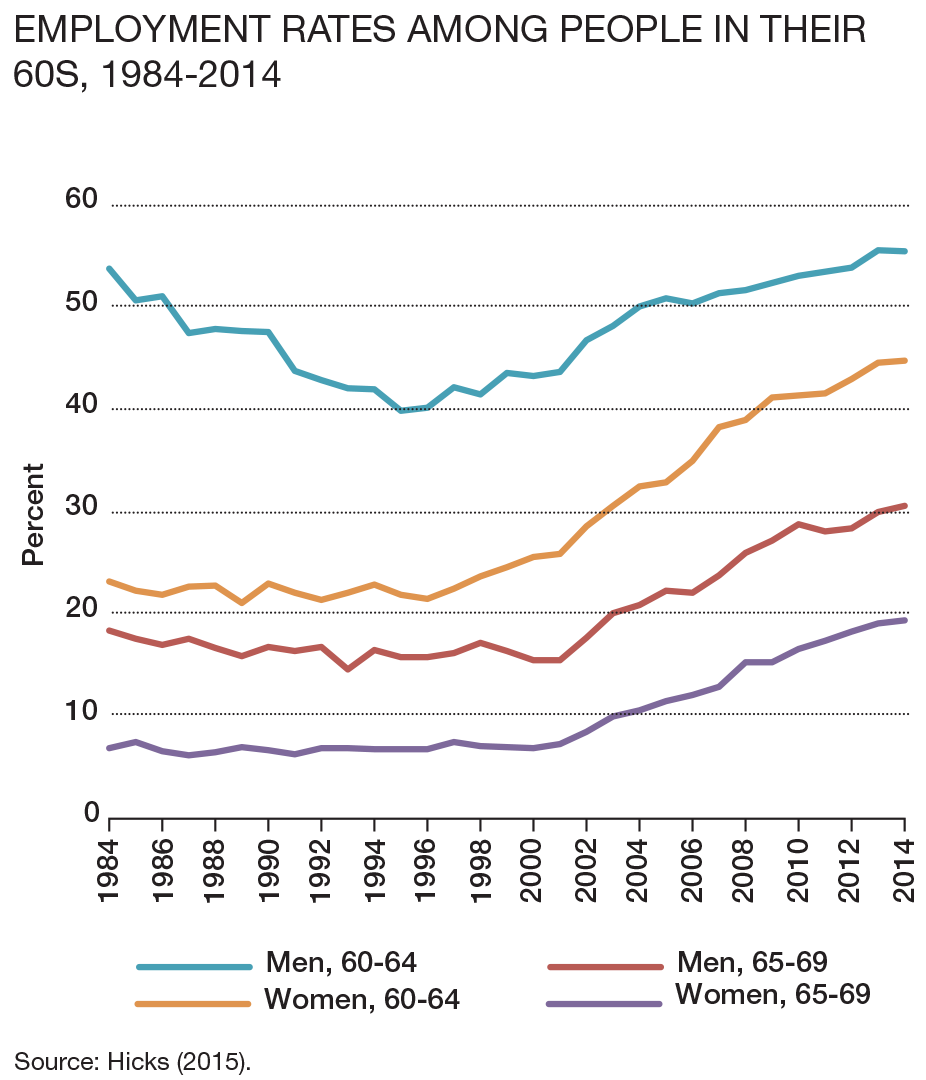

When we look at the data, we see two important trends in recent years concerning older workers. The first is attachment to employment later in life. Indeed, employment rates for people in their 60s, the traditional retirement years, have been growing dramatically and steadily for two decades now.

To the extent people are working later in life, the amount of income they will need in retirement also changes. When people work longer, the risk of long retirement diminishes. The important policy question this raises, then, is whether greater employment participation later in life will offset other factors that work against retirement security (i.e., less likelihood of participating in a workplace pension than in the past).

In a paper that has largely been ignored by the policy community, Statistics Canada researchers Yves Carrière and Diane Galarneau helped address this question. Using sophisticated life tables in order to compare how life expectancy, working-life expectancy and retirement expectancy have changed over time, they concluded there has been no increase in the risk of longevity (as measured by the relative length of retirement) for over two decades. I quote:

The working-life tables indicate a significant increase in delayed retirement starting in the mid-1990s. Expected working life [after a person reaches 50] was even higher in 2008 than in 1977. It was about 14 years for men and women in 1977, compared to 16 years in 2008.

The recent trend to delayed retirement also stabilized the expected length of retirement. The working-life tables show that the expected length of retirement increased from 1977 to the mid-1990s and has since remained relatively stable. The expected length of retirement expressed as a percentage of total life expectancy after age 50 was about the same in 2008 as in 1977.

But how does this fit with the conventional analysis that suggests retirement ages have not kept up with longevity? One implication of their work is that the trend we see playing out in average retirement ages masks a lot of heterogeneity below the surface, in which individuals who live longer are also those who work longer, and vice versa. Unfortunately, Canadian research has not gone far enough to tell us what this distributional picture looks like. This is an area where greater research and policy analysis is needed.

This brings us to the second major trend that has not been taken up in the policy debate: the growing complexity of the paths people follow as they progress through life.

Whereas in the past workers followed a pretty linear path through distinct phases of school, work and retirement, now that trajectory is more complex. As the demands for and distribution of care responsibilities have changed, and as educational attainment and lifelong learning have increased, more people come and go from the labour market at several points over the course of their lives. In the context of something like a pension system, in which benefits are closely related to a person’s age, this breakdown in the traditional path between youth and old age seriously challenges the notion that we can or should adopt a one-size-fits-all approach to how long people are expected to work, and when they are expected to retire.

As I lay out in further detail in the CD Howe and IRPP papers, the implications of a continuation or acceleration of these trends – as is likely to occur – are quite significant. A large number of workers – likely those who are more highly educated, healthier and in higher income categories – will continue to work past the age at which they can begin collecting pension entitlements. In the absence of a radical and fast increase in the age of entitlement to existing age-based public transfers and private pensions, an increasing number of seniors will receive more income than they need or planned for, with less income being available during earlier stages of life when it is more needed. This raises the potential for a large misallocation of public funds as individuals who can continue to work do so, while at the same time receiving both age-related entitlements and earnings that are at or near the peak of their lifetime potential.

And yet, this is not what we hear in the current debate over pension reform. If anything, we have gone in the opposite direction as opposition parties have promised to roll back increases in the eligibility age for Old Age Security, and as most proposals to enhance pension programs like the CPP or the Ontario Retirement Pension Plan have continued to use age 65 as the age at which most people are considered to have withdrawn from work. How we think about longevity risk is becoming an inconvenient truth.

The key problem is that most analysts work in an environment that makes it difficult for them to take account of the evidence that is so obviously in front of them. This arises from the way policy analysis is structured, from the short time frames most analysts work with, and from the perceived need to maintain policy momentum.

Most analysts have a mandate to shed light on only one particular policy area (pensions in this case), and to keep their noses out of other people’s business. Yet the trends in work and retirement affect many areas of social, economic and fiscal policy. It would be awkward, to say the least, if the assumptions used in analyzing trends in one program were out of sync with those used in, for example, fiscal and economic forecasting. It is much easier to use common assumptions; in the case of assumptions about work and retirement, those assumptions are deeply entrenched. The conventional literature on population aging was largely developed before the mid-1990s and looked back to earlier decades, when there were indeed strong trends to earlier retirement and longer life expectancy. Most existing econometric models and other research tools still make the assumption, counter to the evidence of more recent decades, that retirement ages will either remain unchanged for decades into the future or will stabilize at age 65.

With regard to time frames, most policy analysis is also restricted to examining first-order, shorter-term effects, and most forecasting is intended to be useful only in the shorter or medium terms. Here the use of status quo assumptions likely does little harm, even if they do run against the evidence. However, pension policy can only be analyzed sensibly in terms of the longer-term effects. As I argue in the IRPP Policy Horizons essay, we are on the cusp of radical, if gradual, shifts in social policy.

The existing social policy architecture reflects the declining stages of the welfare state social programs that reached maturity in the 1960s and 1970s. Those programs are running out of steam, in terms of the effectiveness of marginal reforms and meeting changing public expectations. If we can’t open our minds to how these programs are already beginning to evolve – and where this may go in the future – then we may be designing a solution to tomorrow’s problem with yesterday’s instruments.

Finally, it is important to remember that pension reform is not easy. A great deal of effort has gone into developing pension reform proposals in recent years, and a general agreement has emerged that one important problem to be addressed is the lack of adequate coverage in the labour market of workplace pensions. It is difficult, at this stage, to contemplate how further work might undermine the emerging consensus. While it is not clear how additional research might change potential policy prescriptions, without more detailed evidence we are flying somewhat blind.

Ultimately we should not hold up needed policy reform, but we must ensure that in making these reforms we are headed in the right direction, that we are taking into account the many different ways individuals, the labour market and the broader architecture of social programs will evolve over the next several decades. Which population groups have been retiring later and which have been unaffected by the general trend? How does this translate into family income? What are the characteristics of those who will win big from the trend toward receiving both work and pension income? Will those who are already rich become richer? We need answers to these and other questions.

Considering that it takes many decades for pensions to work their way through the life course to greater savings and wealth for individuals, what policy-makers do in this area will have long-lasting consequences. We need to get this right. Although we cannot predict the future, the next government should commit to serious research and analysis over the coming months in order to better understand the risks individuals face and how these might change in the future.