Canada is a small, open economy; our prosperity depends on international trade. But as the global economic landscape changes rapidly, many are apprehensive about what the future holds. Will political developments thicken our southern border? Can our companies compete in an increasingly interconnected and digital world? Can our economy attract more international investors and multinational producers? These are important questions that, if we act wisely, can be answered in Canada’s favour.

Ensuring a successful NAFTA renegotiation tops the list, but there’s much we can do unilaterally to liberalize our economy, ease restrictive foreign investment rules, facilitate cross-border production, boost our productivity domestically, and ensure gains from trade and technology reach as many Canadians as possible.

Canada’s Diversification Problem

The greatest immediate concern is our relationship with the United States under their new administration. There’s clearly much at stake — Canada exports more than three times as much to the U.S. than it does to every other country combined. Despite the federal government’s talking points on the importance of NAFTA for the US economy, it ultimately matters much more for us than it does for them.

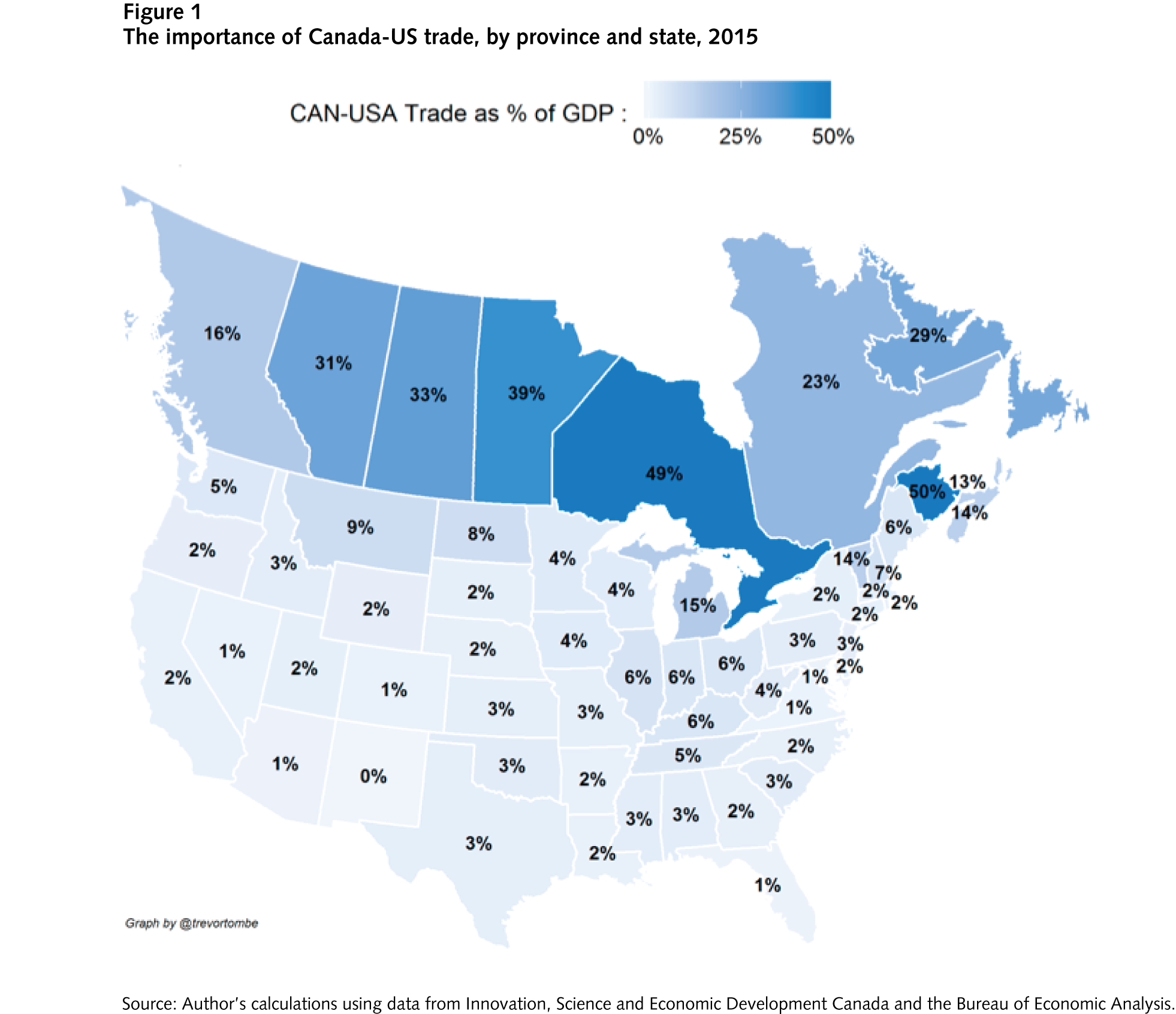

Canada-US trade is worth roughly one-third of Canada’s GDP, and it approaches close to 50 percent for some provinces (see figure 1). Meanwhile, south of the border, in only two states — Michigan and Vermont — is it worth more than 10 percent, while nationally, it’s only about 3 percent for the United States overall.

Though recent U.S. trade rhetoric may be alarming the current irritants are nothing new. The latest softwood lumber dispute, for example, is the fifth such dispute since 1980. President Donald Trump’s concern that Canada’s supply management system (which restricts trade and production in certain agricultural goods) harms their more productive farmers is neither new nor confined to the U.S. In fact, the most vocal opponent of our supply management system during the Trans-Pacific Partnership (TPP) negotiations was New Zealand. And while “Buy American” is a staple of Trump’s economic stump speeches, Obama’s stimulus package also included such provisions, and more recently New York state contemplated something similar.

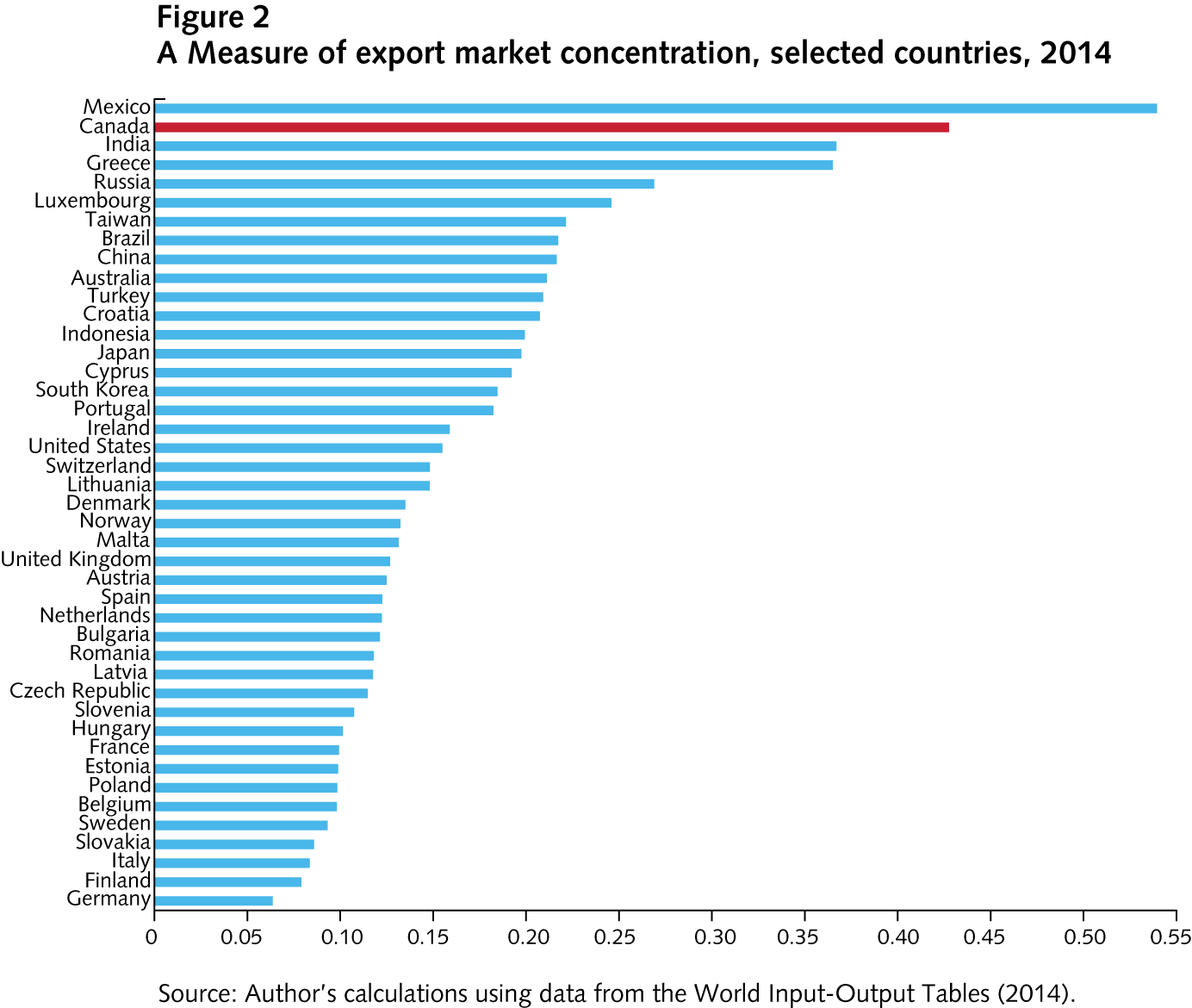

But new or not, these irritants reinforce a problem with Canadian trade: we’re highly reliant on the United States. In fact, Canada’s exports are among the most concentrated of the major world economies, behind only Mexico — the other NAFTA economy which depends even more on the US (figure 2).

We must therefore aggressively pursue opportunities to liberalize our trade with other markets. To their credit, the federal government is trying to do just that (as previous governments have done before). There’s much work to do, some of which requires no consultation or cooperation with other countries. Canadians pay about $5 billion in tariffs each year, built into the price of various imported consumer goods that we buy. For perspective, this is roughly equivalent to adding an extra percentage point to the Goods and Services Tax. Most of these tariffs are paid on imports from Asia. China accounts for nearly half of our import tariffs paid, TPP countries and other regional players who were in the TPP represent another quarter. Canada needs no one’s permission to unilaterally lower these tariffs.

Thinking differently about trade

Tariffs are only one piece of the puzzle. To truly open ourselves to global economic opportunities, we need to rethink global trade. It is now less about exchanging one good for another, and more about deeply interconnected webs of global production. We don’t make cars, so much as participate in long chains of automobile production that span the globe.

This is also true in many sectors. Roughly one quarter of our exports originate outside the country and 42% of the inputs (ie. component parts) we import are later exported within another product. Almost one-fifth of Canada’s exports are not even consumed where they are sent, but instead are embedded into yet another product and exported to a third country. Global supply chains are long and complex.

Ask someone what Canada’s top export sectors are and they’ll likely say energy or autos. But business and professional services and banking are much more important than is often supposed. To see this, consider a sector’s “value-added”, which measures how much more valuable output is relative to the inputs embedded within it.

Auto manufacturing incorporates so many imports from other sectors and countries that what it adds to the global production chain — it’s so-called value-added exports — is far smaller than the headline trade numbers suggest. In 2014, gross exports of autos were $56 billion, but the domestic value-added content of those exports was only $10 billion. Meanwhile, Canada’s banking sector is used as an input in so many of our exports that when we account for this we find financial service exports were $24 billion in 2014. Beyond banking, the OECD estimates that Canada’s business services’ exports were worth $184 billion when measured in value-added terms.

Perhaps most surprising is that Canada’s exports are often between a parent company and a subsidiary on either side of the border. So-called “related party trade”, which typically occur within the same firm, accounted for 53% of our exports to the United States in 2014, and 41% of our imports.

What does all this mean? Multinational firms coordinating increasingly long and complex global supply chains is the new trade reality. Firms headquartered in one location operate production facilities in another and sell to yet another. To fully participate in global value chains we thus need to be open to international investment.

Liberalizing foreign investment and multinational production

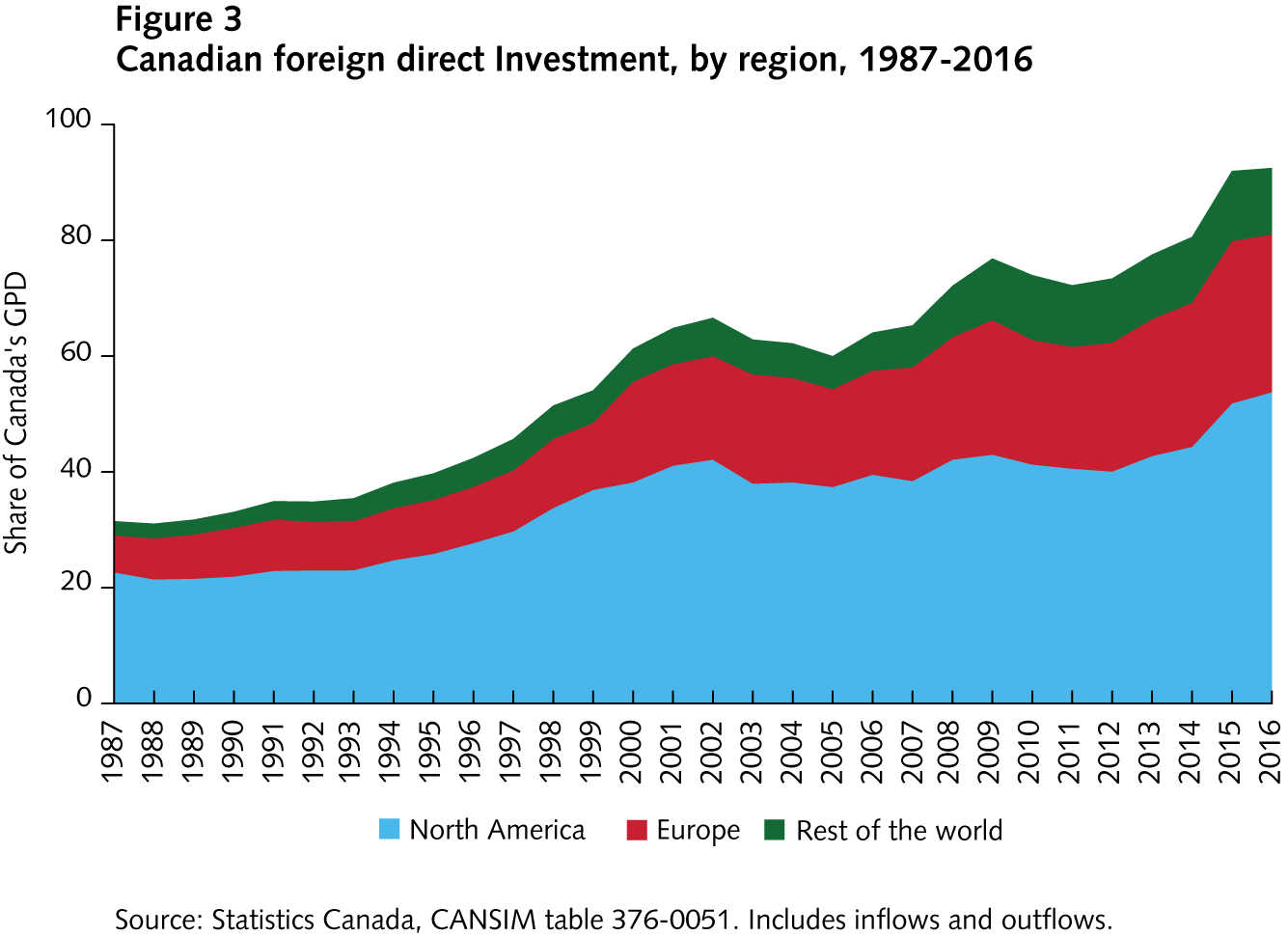

While international investment between Canada and our NAFTA partners is large — equivalent to over 40% of our GDP (see figure 3) — there’s much more that Canada can do to entice foreign investment, especially beyond North America. The TPP would have been a strong start, but with that opportunity languishing for now, Canada should act on its own.

The Investment Canada Act (ICA) empowers our federal government to block a foreign investment that exceeds $1 billion if they deem it not to be a “net benefit” to Canada. Politics often weighs heavily on such decisions (as the case of BHB Billiton’s failed acquisition of Potash Corp. demonstrated). And even though foreign investments are rarely rejected, the ICA’s provisions, which do not apply for similar domestic investments, increase risk and costs for foreign investors in Canada. Canada’s foreign investment policies, which cover sectors such as transportation, distribution and telecommunications, are among the most restrictive among OECD countries.

To be sure, Canada is not alone. The barriers to coordinating long global supply chains are large in most countries. In recent research, Keith Head and Thierry Mayer estimate such costs relative to tariffs and other traditional trade costs in the auto sector. Among OECD countries, traditional trade costs are roughly 8% (in tariff-equivalent terms) but are 50% for the combined cost of multinational production and sales. The costs include not only investment barriers, but also regulatory differences between countries. The gains from liberalizing these other dimensions of trade are large. Head and Mayer find that the TPP would benefit Canada’s auto sector by expanding multinational production here. This result is something completely overlooked in our traditional focus on classic trade costs and greater import competition from abroad.

Deeper reforms to Canada’s economy

Reforms to liberalize our domestic economy can also boost trade. Inter-provincial barriers harm our international competitiveness. This is true for a variety of business inputs, which face particularly burdensome internal trade frictions. With the recent deal on internal trade signed by provincial premiers, which came into force on Canada’s 150th birthday, internal trade costs will hopefully fall over time.

Not to be lost in this discussion is the fact that trade is not an end in itself, but rather a way to specialize production, increase productivity, raise incomes and lower prices, among other benefits. There are various ways to achieve these goals, even if foreign political developments limit international trade opportunities.

We can ensure our taxes are efficient and competitive, our public services and infrastructure are of high quality. We can liberalize our own domestic markets — particularly through smoother inter-provincial trade — and improve productivity from within. We can unilaterally ease restrictions on foreign ownership and investment activity in Canada. We can ensure Canadians have access to retraining and skills development opportunities, to ease the cost of switching between jobs and sectors, which is an especially important policy priority if globalization and technological change continue their rapid developments.

Policies that focus on improving and liberalizing Canada’s economic environment, while ensuring vulnerable workers are not left behind, are the keys to success in our new global reality. While Canadians often feel vulnerable to the whims of external developments — from global commodity prices to unexpected political developments — let’s not forget that there’s much we can do for ourselves, and few excuses not to.

This article is part of the Trade Policy for Uncertain Times special feature.

Shutterstock/Maxx-Studio

Do you have something to say about the article you just read? Be part of the Policy Options discussion, and send in your own submission. Here is a link on how to do it. | Souhaitez-vous réagir à cet article ? Joignez-vous aux débats d’Options politiques et soumettez-nous votre texte en suivant ces directives.