Linking ICT investment with other large physical infrastructure investments, such as buildings, roads, transportation systems, health and electricity grids, allows them to be “smart” and save energy, assist the aging, improve safety and adapt to new ideas. OECD, Investing in Innovation for Long-term Growth

Canada’s national transportation policies, ever more linked to global trade and supply chain management, now face two issues. The first is truly transformative: the staggering changes in global transportation supply chains, with ever bigger ships and aircraft, fewer but more strategic port developments, shifting traffic corridors through the Panama and Suez Canal and new, integrated technological and communications links with inland transportation (freight forwarders, railways and trucking) and new, strategic management tools. The second and related issue is the role of corporate supply chains as a strategic element of corporate decision-making. Globalization dictates why companies and their employees must refocus their thinking. Past emphasis on provincial, regional or even national supply chains must shift to truly global sourcing, marketing and transportation policies linking suppliers and customers across international boundaries.

A global view of the link between logistics, transportation, trade and corporate strategy suggests that global supply chains are now a corporate imperative for strategy making and seriously calls into question choices based on national or regional practices of Canadian firms. In short, corporate strategy requires a global view of supply chain innovation and new linkages for logistics, international markets and domestic transport systems.

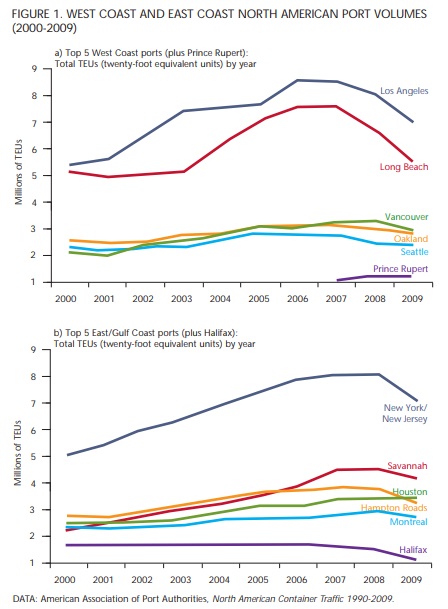

For Canada, and indeed for North America at large, ports like Vancouver, Prince Rupert and Halifax are ideally suited to address these two global supply chain challenges, because of location, their deep-water natural harbours and channels, and direct links to inter-modal transport like roads and rail lines. The volume of container trade on mega-carriers is growing so fast that bottlenecks on the US West Coast and the problems of the shallower ports on the American East Coast are the competitive challenges for Canada’s gateway strategies (figure 1). These initiatives require new thinking by all levels of government, the private sector and various stakeholders, because global trade and investment now directly integrate Asia with North America. Jobs, investment, immigration, training and education and national productivity demand new policy coordination, not only for Asian trade flows, but for new technologies, new skills and new forms of collaborative innovation.

Global trade, increasing at a faster rate than the global economy, is now shaped by profound changes in new supply chains, divorced from the national or continental perspectives of the past. In particular, new patterns of marine transportation, with supporting human resources — educated workers trained in new supply chain technologies — are being adopted in developing and developed countries alike. Global supply chains now involve a physical component — transport of goods via ships, rail and trucks; an information component — computers, software tools and PDAs; and a people component — skilled workers who deliver the products.

Clearly, British Columbia, with its legacy of Asian immigration, educational ties, trade and transportation links, stands to gain enormously from its ideal location, with spillovers for Canada at large. For the western provinces, with their abundant natural resources and trade links in potash, wheat, coal and energy with Japan and other Asian countries, the attractions across the Pacific are critical, even excluding trade with China.

Global maritime shipping is itself being transformed — bigger ships, more cargo in containers, bigger and more productive ports and terminals, and new forms of inter-modal transport. This integrated 9 package forms one element of the global supply chain, linking countries around the world on ocean transport routes and opening new job and trade opportunities. But this 6 transportation supply chain must be linked directly to the second global supply chain, which is company based. From Walmart to Toyota, McCain Foods to Target, global firms are integrating their supply chains as they enter new markets and source components and parts, process them and deliver finished goods, on time, to their customers. Supply chains are about three imperatives: price, quality and delivery.

The Atlantic Gateway, like the Pacific Gateway, can position Canada as a truly northern entry point for link to the global transportation network, and for global corporate supply chains. In Canada, two West Coast ports, Vancouver and Prince Rupert, and Halifax on the East Coast have the deepwater ocean channels, land area and terminal capacity to handle the new ships on order in the shipping industry. The West Coast ports of the United States already face massive congestion problems, and there is limited room to grow. There are other challenges — environmental and pollution concerns, labour relations and road congestion. Global shipping companies like Maersk are introducing megaships that lower transportation costs per unit shipped but are a challenge for ports that must accommodate them — the ports are too small, the water channels are not deep enough, and they lack inland transport, from terminals to rail and truck lines. As more goods are sourced from markets like China and India, global shipping companies are reconfiguring their trade routes, including within Asia itself.

Shipping companies are planning new transport corridors, through the Suez Canal, across the Atlantic Ocean to North America. Canada’s deep-water ports on the Atlantic coast are the closest to Europe and the Suez Canal, and potentially offer new trade and transportation routes to Asia. Containerization, the key platform for large container ships, is an organizational disruptive innovation for international trade and will reach 650 million TEUs (twentyfoot equivalent units) within a decade, from zero 50 years ago. The container is the ideal mode of long-distance transport for bulk cargo, dry cargo and now refrigerated goods, allowing easy transshipments of fresh and frozen goods (e.g., seafood, fruit and vegetables, flowers) in 20-foot and 40-foot boxes.

However, global shipping and the demand for scale economies via large megavessels are not the only transportation and infrastructure challenges facing Canada. As more firms located in Canada are engaged in global trade, corporations have to deal with a new strategic challenge: organizing innovative global supply chains. This innovation is complicated, involving inland transit in foreign countries to inland transit in Canada, with various transportation modes in between, from trucking to rail, in-sea shipping to navigating the Suez Canal or Panama Canal. In practical terms, global supply chains involve shipping from factories located in distant markets, across the global transportation networks, into stores and factories located in large consumer shopping clusters in central Canada and markets in the US Midwest. Like their corporate counterparts in the US, Canadian firms now need both West Coast gateways for cargo through ports and inland transport, and East Coast gateways and corridors. The reason is simple: supply chain economics requires a measure of balance, of inputs and outputs, of suppliers and customers, of a full container in one direction and a full container in the opposite direction.

The Pacific Gateway strategy is the most developed for Canada’s West Coast for goods from Asia, around the ports of Vancouver and Prince Rupert. The Atlantic Gateway strategy for the East Coast around the ports of Halifax and Montreal is less developed, owing to limited cooperation, rivalry among provinces and no gateway champion driving the necessary policy focus. Gateway strategies, including the Arctic, is a national transportation priority, not a regional issue, involving several forms of transport and intermodal connections, and numerous stakeholders. The two supply chains — one of transportation, one of corporate networks linking suppliers and customers — are intimately linked.

Canada’s traditional marine strategy has been dominated by security issues (fishing rights, smuggling and in-shore transport) and defence. Few of Canada’s leading ports like Toronto, Churchill or Quebec City are centred on international trade, especially container trade outside the North American triad. For the West Coast of Canada, there is a century-old link to Asia, dating from the ships run by Canadian Pacific to Yokohama, Hong Kong and Shanghai. More recently, the startling rise of the Asian economies — first with Japan a generation ago, then Southeast Asia and the Asian Tigers, and now China — represents a tectonic shift in the global economy.

China, with over a billion people by itself, shifts the global economic order toward Asia. Combined with India, with another billion people, its immediate and long-term effects on the global economy are simply enormous. Clearly, British Columbia, with its legacy of Asian immigration, educational ties, trade and transportation links, stands to gain enormously from its ideal location, with spillovers for Canada at large. For the Western provinces, with their abundant natural resources and trade links in potash, wheat, coal and energy with Japan and other Asian countries, the attractions across the Pacific are critical, even excluding trade with China.

But these changes in the global order do not exclude the rest of Canada. For instance, Ontario has more two-way trade with China than western Canada. Atlantic Canada has its own trade linkages with Asia, from education to French fries, pulp and paper to fisheries. Indeed, if trade is properly managed, Atlantic Canada stands to gain tremendously as another gateway to the world economy, for several reasons:

- Atlantic Canada is the Canadian gateway to Europe and new trade routes to southern Asia and, over time, the polar routes to Russia.

- Global trade routes are being transformed by new transportation modes: global shipping companies, ever larger ships and new hub-and-spoke supply chains that favour speed and cost, not distance or cost per mile.

- The new sophisticated freight forwarding companies, now with a global reach, allow small and medium-sized firms to contract out all aspects of international trade, including documentation, customs clearance insurance, and ideal mode of transport, on a one off or continuing basis.

- Inter-modal transport systems for inland shipping, like Centreport in Winnipeg, plus ocean ports or airports, combining rail and short-haul and long-haul trucks, require new techniques to load, unload quickly and re-sort loads for deconsolidation for short-distance shipping.

- A new global network of terminal operators, financed by private equity, increasingly integrate corporate supply chains from large deepwater ports via global shipping companies that operate ever larger ships (the ocean equivalent of the largest jumbo jets) into other strategically located deep-water ports around the world, reinforced by the latest communication devices, including RFID (radio frequency identification devices) technologies for online precision tracking.

Unfortunately for Canada, the world is not standing still. From Dubai to Vietnam, from new ports in China to well-established ports like Rotterdam and Hong Kong, there are new gateway linkages on the East Coast of the United States. Three strategic stakeholders — shipping companies, terminal operators and port facilities (air and sea ports) — are accelerating corporate developments as part of changing global trade strategies. Consider some recent developments:

- Enlargement of the Panama Canal to receive post-Panamax ships of up to 15,000 TEUs planned over the next 20 years.

- New rail services (two trains per day) linking Long Beach, California, to Atlanta, Georgia, to help diminish the congestion on the West Coast of North America.

- The development of new ocean ports in India for the shipment of manufactured goods like steel, textiles and autos, not only for the markets of Asia, but eventually to North America via the Suez Canal.

- New combinations of ocean shipping and air cargo transport to reduce trans-ocean cargo shipping from Asian ports to about 32-35 days for a round trip across the Pacific, or 65 days via the Panama Canal.

- In a post 9/11 world, new (and often untested) security initiatives, including the US Secure Freight Initiative of screening through imaging technology for nuclear products and weaponry, including in foreign ports and terminals.

- Global alliances and business cooperation agreements between shipping companies, terminal operators and railway companies to manage the dramatic new demands of just-in-time delivery around the imperatives of price, quality and delivery, where true real costs are quickly exposed because of traffic gridlock.

- New thinking about bottlenecks in supply chains caused by unforeseen events, including disasters like the Japanese earthquake and tsunami in Japan in 2011 that severely cut off components critical for computers, autos and aerospace products.

While global trade is central to Canada’s wealth, so too is the need to become a player in the global supply chain system. For Canadian firms, and for the public sector, that means new imperatives: having global operating scale, a critical mass of skills and trained people, and tight transportation links to global companies. Both supply chain systems, global transport and corporate, illustrate the basic imperative: the organization is only as strong as the weakest link.

For generations, Canadians have been increasing their global trade exposure, but mainly with a mindset that focused on North America. Except for a few industries, Europe is seen as a niche market. Outside the airline sector, much of the transport focus has been through the prism of North America, and especially the states lying contiguous to Ontario and Quebec. Since the Canada-US Free Trade Agreement was signed with the US, later expanded to become NAFTA, Canadians have reoriented their trade links away from a national focus (east-west) to a North American focus (north-south). In the transport area, this has culminated in new arrangements, such as the Open Skies air pact with the United States; a powerful railway system developed by CN, not only across Canada (like rival CPR), but north-south to the Gulf of Mexico, with a large terminus in Memphis; and strong market share in big container markets like Memphis, Detroit and Chicago.

On a global basis, international trade is based on an ocean-going transportation system. Seaborne traffic covers about 70 percent of international trade. The containerized portion of this passed a milestone in 2004 with 360 million TEUs of throughput through the world’s ports. (The conventional transport term TEU measures cargo in 20-foot units, but most containers in North America are 40 feet and some are 53 feet.) For Canada, the challenge now is to design a national transportation system that is state of the art to deal with the world’s biggest market, the United States, and that reinforces Asia’s role in that competitive market.

Two global trends are unmistakable. First, the international economy has already shifted dramatically, away from the Atlantic-centred market of Europe and North America to the Pacific Rim Asian markets like Japan, China and India; and away from the traditional developed triad economies (Europe, North America and Japan) to the developing world. This new mix, even when China is excluded, now accounts for one-third of world trade (28.8 percent of merchandise exports, 26.3 percent of imports). China adds about 5.5 percent, but its trade is growing at 20-25 percent per year.

The second trend is equally profound for the global economy. East Asian economies are following a similar path to Japan’s in the 1970s and 1980s, now being emulated by China: accelerating their industrial growth by moving up the value chain to more sophisticated products, components and technologies. All over Asia, factories operate with state-of-the-art equipment and the latest industrial processes imported from Japan, the US or Europe, with managers and engineers trained in reputable foreign universities. What was true two decades ago about Japan, which trained engineers while the US trained lawyers, applies to Asia: India and China each produce more engineers than Europe and the US combined. India and China are shifting their industrial production away from labour-intensive and commodity-intensive product lines to sophisticated technology-intensive output, as Japan did a generation ago.

Air cargo and ocean shipping are the manifestation of the way Asian countries use global logistics to link supply chains into new global JIT (just-in-time) systems. Historically, primary sectors like the oil industry used these ideas to link the source of oil production to refiners (often located in different countries, in part because of byproducts) and their distribution outlets, such as service stations. The Irving Group of companies illustrates this pattern. The Irving Group, a family-owned conglomerate located in New Brunswick, founded by K.C. Irving after he left Imperial Oil in 1924, operates vertically integrated operations in a number of sectors, from oil and gas to pulp and paper, food processing (Cavendish Foods), shipbuilding and media.

Irving Oil procures energy feedstock from the Caribbean or the Middle East, ships the product to its state-of-the-art Saint John refinery, and then markets the product at Irving service stations located throughout eastern Canada and New England, usually on Irving ships and its own trucking fleet. Other firms follow similar practices. In Japan, global manufacturers like Toyota locate their factories and assembly plants adjacent to deep-water ports, where the cost of shipping from, say, Nagoya to the port of London remains cheaper per car than transport by truck or railway from car factories located within Britain to the port of London. Today, JIT global logistics has extended to the retail sector, led by firms like Canadian Tire, Hudson’s Bay Co., Sobeys, Home Depot or Ikea.

For over 30 years, Canadian policy makers have been concerned with the country’s Pacific Rim gateway — transportation links via air, sea and rail that shape Canada’s exports and imports to Asia. In this period, Japan was one of the first priorities, as that country’s dramatic growth led to an apparently insatiable demand for Canadian raw materials — timber, coal, grains, potash, pulp and paper — and an equally dramatic rise of Japanese exports like automobiles and consumer electronics. Container flows went two ways. As Pacific Rim trade with North America grew, West Coast ports — Los Angeles and Long Beach, Seattle and Vancouver — faced increasing port congestion, as the flow of containers across the Pacific skyrocketed, from 2 million TEUs in 1970 to 20 million TEUs in 2009.

Air cargo and ocean shipping are booming sectors because more countries are linked to global supply chains, which are based around companies. China is the latest and most dramatic example, but countries as diverse as the BRIC countries, Vietnam, Indonesia, Egypt and now countries in Africa illustrate how global manufacturing extends around the world, depending on the sector (contrast oil with textiles or furniture production with cosmetics). The trend is clear: more trade means more JIT flows, involving bigger planes and ships, bigger airports and ocean ports, and vastly more people and companies to manage the supply chain, from freight forwarders and trucking companies to IT and security firms. Global supply chains require intense cooperation among companies, among manufacturing firms and retailers with transport companies, and between private companies and the public sector. As countries become more integrated through global trade, firms require a mix of more integrated services, and cooperation of specialized functions. In transport, this means intermodal transport services, including ocean shipping and containers, railways and ease of access to ports and factories, and truck services, often employing an integrated IT system to manage manifests, insurance and other aspects of the global supply chain system.

While global trade is central to Canada’s wealth, so too is the need to become a player in the global supply chain system. For Canadian firms, and for the public sector, that means new imperatives: having global operating scale, a critical mass of skills and trained people, and tight transportation links to global companies. Both supply chain systems, global transport and corporate, illustrate the basic imperative: the organization is only as strong as the weakest link. Any barriers — bottlenecks, time delays, quality defects or sundry imperfections — quickly add to real costs. The transportation supply chain, by definition, involves both the public sector and the private sector. International trade means that goods cross borders, so there must be customs and security inspection. And that means a changed view of economic geography, where population centres no longer decide the transport economics: the oceans do. Consider the changes in port economics.

Global trade and global logistics are realities. Canada needs to invest in a three-way national strategy, linking the Pacific coast ports, the Atlantic coast ports and the St. Lawrence-Great Lakes corridor.

The prospect of very large container ships coming into service makes Halifax the natural entry point for goods shipped from Europe or through the Panama Canal. In the US, new investment developments and new infrastructure, such as new terminals, warehouses and railway lines, show that the US is not a bystander in the changing global trade game. Consider recent developments at the US East Coast ports:

- In New York/New Jersey, a $760-million investment will deepen the port channel to 50 feet, and $1.6 billion will improve port infrastructure;

- The Norfolk, Virginia, port is investing $400 million in container terminals and new on-dock rail capacity.

- At the port of Charleston, North Carolina, a new three-berth container terminal at a former naval base will elevate capacity by 1.4 million TEUs to more than 4 million TEUs per year, double that of Vancouver. Crane operations have improved substantially, from 40 container moves per hour to 53 per hour, thus reducing what is called dwell time.

- New warehouse facilities in Houston constructed by Walmart (1.3 million wquare feet) complement a 1.4-million-square-foot warehouse for Home Depot and a 1.5millon-square-foot facility in Virginia for Target Stores.

- In Miami, there is a plan for $250 million of investments in port infrastructure, including port deepening by the US Army Corps of Engineers.

Part of the East Coast development in the US is driven by the staggering port development in China and, after some considerable delay, in India. In China, there are concrete plans for 100 new container loading berths, each with 500,000 TEUs per year capacity — the equivalent of Halifax. In India, there is a new 20-year plan for the development of ports and port infrastructure, to increase India’s port capacity from 750 million tons to 1.5 billion by 2012, and 2 billion in 2016. Private sector development in Indian ports now exceeds $2 billion and is growing fast. Added to competition from the US are new developments in Mexico and ports in the Dominican Republic and other Caribbean islands adjacent to the Panama Canal.

These issues are central to the global context of Canada’s northern gateway strategies. The question is: Are local and regional ports in the Atlantic region prepared to build a globally successful gateway extending to a national transportation corridor? Transportation infrastructure is only one part of Canada’s gateway strategies. Most manufacturing and service industries depend on quality transportation infrastructure, and as firms grow internationally, air, road and sea lines are central. For instance, how does Labrador deliver its iron ore to the steel mills of Hamilton and Pittsburgh? The answer: By train and bulk cargo on the St. Lawrence River. Today, the markets of Asia are open to Newfoundland via inshore shipping and container vessels. Transportation challenges constantly face the region, especially in air transport, so critical to the tourist, cultural and convention industries. For example, as PEI develops its golf courses as part of its tourist industry, inferior air service often means visiting golfers (and musicians) arrive on time, but without their luggage.

It may sound like a contradiction in terms, but Canada needs an Atlantic Gateway strategy to cope with Pacific Rim trade. Some corporations understand this paradox, like Canadian Tire, which operates a two-port logistics strategy. Two-way trade between North America and Asia, and between Canada and Asia, has increased dramatically. But global trade raises the need for complicated supply chains and means logistical problems for Canadian companies. Much of this trade is in complicated shipping modes — commodities like coal, wheat, potash and lumber, and manufactured products like capital goods, industrial machinery, transportation and aerospace parts, involving trucks, warehousing, trains and specialty ships. Canadian firms must reorganize their supply chains from a national to a global logistics plan.

Some of these goods are destined for the North American interior, especially to Chicago-area manufacturing hubs throughout the central North American population corridor. But the West Coast has its own challenges, such as a reputation in Asia for strikes (there has not been a strike action in a generation), antiquated facilities and minimal security. As noted, because of West Coast congestion, companies are addressing new shipping needs for East Coast ports. In the past, the cheapest routes were through the Panama Canal from China, South Korea and Japan into East Coast ports. Increasingly, there is a growing demand for state-ofthe-art shipping into the Atlantic coast ports of North America, like Montreal, Halifax and Saint John. Potentially, the Atlantic Gateway would bring together a new policy mix, involving the needs of importers (countries, companies and transport firms), the private sector (manufacturers, retailers and niche players), the transportation industry, the provincial governments of Atlantic Canada and the federal government.

For public sector policy-makers and for private sector firms, the prime focus for gateway options is the structure of the global shipping industry, and its container flows. The trends are unmistakable: scale and global reach. Scale now pervades all considerations: bigger ships, bigger ship owners, bigger and more complicated terminals, bigger port regions encompassing all aspects of inter-modal transport and bigger and more extensive strategic alliances across the shipping value chain.

Shipping companies have always sought scale — witness bigger cruise ships, aircraft carriers, oil tankers and container ships — because as a general rule, each doubling of ship size (in gross tonnage) reduces overall costs, both the cost per voyage and the cost per container, especially when the ship is fully loaded. The global reach of the shipping industry now extends across the value chain and the ocean corridors — Trans-Pacific (AsiaNorth America), Asia-Europe, and TransAtlantic (Europe-North America). Trans-Pacific trade illustrates the dramatic changes in the world economy, represented by the growing integration of the Asian economies and their global trade expansion, and the continued new investments in China and the rise of state-of-the-art factories there that integrate supply chains with those of Asian companies in, for example, automobiles, auto parts, consumer electronics, computers and aerospace.

Further, trade data clearly show the problem of shipping imbalances, partly reflecting seasonal imbalances but also the challenges posed by trade shipments: higher value goods like pharmaceuticals and machinery shipped from North America to Asia by air, and dry goods from China and Asia shipped to North America in ocean containers. Moreover, these container flows increasingly come in larger ships, those above 4,000 and 5,000 TEU capacity, replacing smaller ships of 3,000 TEUs or less. The move to new, large ships is dramatic. As of July 1, 2006, the world fleet of container vessels included 3,708 ships, with a total capacity of 8.7 million TEUs. The global order book of 1,130 ships involves 4.295 million TEUs (approximately 50 percent of existing capacity). By the end of 2008, ships of 6,000 TEUs or greater will represent 25 percent of global container fleet capacity, and there will be 1,250 vessels each with a capacity of at least 6,000 TEUs.

What Canada at large faces, and what policy-makers must understand, is how Canadian industry fits into global transportation supply chains. National policy has started to address the West Coast issue, with an investment package amounting to $591 million. BC is now an extremely active player in Asia at all levels, with regular visits by the premier, cabinet ministers, and private sector groups, and the Lower Mainland ports are integrating to form a new unified port authority. Vancouver is clearly the main container port in Canada, and West Coast container shipments are projected to double, from about 2 million TEUs per year to 5 million by 2020.

However, there remain a lot of assumptions about the second West Coast port, Prince Rupert. Here, First Nations land claims, port infrastructure and terminal construction are closely watched around the world, and by countries like Mexico, which sees its own port development as a possible competitor for the West Coast trade, possibly because, with China as a partner, time is on Mexico’s side.

Global trade and global logistics are realities. Canada needs to invest in a three-way national strategy, linking the Pacific coast ports, the Atlantic coast ports and the St. Lawrence-Great Lakes corridor. But any initiatives along these lines require a massive educational process, showing Canadians why the country intends to be a global player in international trade and is willing to invest the time and money to design a transportation system that has global reach. This is not only a job for governments at all levels, although the public sector must be part of the solution. It is not only the task of transportation experts to exert pressure on both the public and private sector, although they can demonstrate what other countries are doing. And the Canadian private sector must change its outreach programs by openly having its own Team Canada trade missions to demonstrate what the rest of the world, Asia in particular, is doing to play the global trade game.

As globalization proceeds, not as an offset to US-Canada trade or NAFTA enlargement and integration, but as a close complementary advantage, students of corporate strategy design strategic supply chains accordingly. The opportunity to lead is Canada’s to lose.

Canada has within its grasp a rare opportunity to be a global transportation leader. As Canadian leadership did with the St. Lawrence Seaway, today’s leadership can make Canada the 21st-century logistics gateway to North America. Canada has the potential to build worldclass container ports on the scale of those already being built and operated in Japan, China and Asia, linked with quality inter-modal rail and truck operations to most of the population of North America. The US won’t do this. The environmentalists and the NIMBY (not in my back yard) crowd needed ports, rails, pipelines and highways to be built. This opportunity to lead is Canada’s to lose.

And lose Canada might. Canada’s policy and electoral priorities are shifting from health care and education to environment and personal health, but the general issues of future wealth creation, productivity and innovation get only lip service from Canada’s political and corporate leaders. Financial investments in basic infrastructure and transportation are the strongest levers for wealth creation in Canada today, with huge implications for productivity enhancement and job creation.

Historically, Canadian transportation policy has a bias toward regional concerns, not national strategies. The national railroad was the last significant nation-building transportation effort, and that was started in the 19th century. Even the Trans-Canada Highway has been bogged down in inter-provincial rivalries, the narrow strategic outlook of domestic companies and short-term political considerations.

The Pacific and Atlantic Gateways, ocean bridges linking Canada and even the US to global supply chains, are part of a national transportation plan that is global in outlook, recognizes the links in intermodal transport systems and addresses the close integration of transportation, global trade, technology and talent. Canada-Japan linkages could have huge mutual benefit in these developments. Sadly, Canada is one of the few maritime economies without a national ocean strategy for gateways and corridors, which must include the Arctic. It is also one of the few industrialized countries without a national highway strategy.

As globalization continues, Canada must adjust its thinking, design and delivery on transportation strategies accordingly. Time is not on Canada’s side: changes are taking place in Mexico, and never discount what might happen in the US. An Atlantic Gateway is a national priority and a natural complement to the Pacific Gateway investments in new infrastructure. This initiative needs to be part of a three-way national strategy, linking the Pacific Coast ports, the Atlantic Coast ports and the St. Lawrence-Great Lakes corridor. But any initiatives along these lines require leadership and an intense educational process, showing Canadians why the country intends to be a player in international trade and is willing to invest the time and money to design a transportation system that has global reach.

Japan was the teacher for its Asian neighbours as a global leader in quality management of complex manufacturing, and for its advancements in various forms of clean technologies, including transportation vehicles of all types, from cars and trucks to ocean-going ships, passenger and freight rail, ports and port infrastructure. Clearly, a Canada-Japan alliance is a natural alignment with North American and Asian trade and investments.

As globalization proceeds, not as an offset to US-Canada trade or NAFTA enlargement and integration, but as a close complementary advantage, policy makers must design strategic supply chains accordingly. The opportunity to lead is Canada’s to lose.

Photo: Shutterstock