Fiscal policy has become uncommonly topical of late, first for what it had to do more of to combat the great global financial crisis and recession, and now for what it has to do less of to sustain the solidifying but still nervous recovery.

Whether it was Standard and Poor’s putting the United States on credit watch, Greece back in the headlines (and headlights) once again, the 11th-hour budget slugfest on Capitol Hill, the very public budget debates about affordability in Wisconsin, Portugal seeking a bailout package from the European Union (EU) and the International Monetary Fund (IMF) or the upcoming battle over the US federal debt ceiling, topics like debt-to-GDP ratios, debt-servicing-to-tax-revenue ratios and pension actuarial deficits that were once esoteric are now front-page news. And, given the depth and breadth of the fiscal problem in so many countries, it is unlikely that fiscal policy will soon stop being a front-page issue.

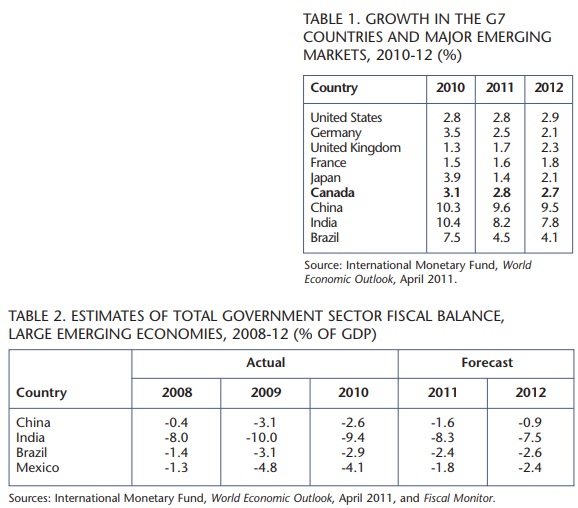

This reality frames the following questions: How do we put the fiscal genie back in the bottle? Are there any common grounds to be found in these contentious debates? The state of the economy is one; according to the IMF, the global recovery has solidified and broadened. Growth in the United States, Germany, Canada and a number of other advanced economies has picked up, while growth in major emerging economies remains strong (table 1). As the IMF observes: “Given the improvement in financial markets, buoyant activity in many emerging and developing economies, and growing confidence in advanced economies, economic prospects for 2011-12 are good, notwithstanding new volatility caused by fears about disruptions in oil supply.”

The risks to a sustained expansion are shifting from too little private sector demand to too much public sector stimulus — fiscal and monetary — and liquidity. Inflation pressures are already increasing rapidly in China and other major emerging economies, and beginning to appear in a number of advanced economies. In short, there is no longer a countercyclical case to be made for postponing fiscal restraint, in either advanced or emerging economies.

Indeed, the risks to a sustained expansion are shifting from too little private sector demand to too much public sector stimulus — fiscal and monetary — and liquidity. Inflation pressures are already increasing rapidly in China and other major emerging economies, and beginning to appear in a number of advanced economies. In short, there is no longer a countercyclical case to be made for postponing fiscal restraint, in either advanced or emerging economies.

The second area of broad agreement is that the extraordinary and coordinated fiscal and monetary stimulus implemented to stave off global economic depression and financial sector collapse was necessary, and it has worked. But the unique degree of international policy coordination among G20 leaders to deal with the great global financial crisis and recession may be difficult to sustain now that the urgency of the crisis has ebbed and divergent economic circumstances and policy interests are reasserting themselves. This could become evident in G20 disagreements about implementing financial sector reform measures, unwinding imbalances, appropriate roles for capital account restrictions and “exit strategies” from unsustainable fiscal situations.

In the current circumstances, one policy size does not fit all, and policy coordination is more difficult when circumstances do not coincide. With consensus and coordination harder to achieve, proactive policy responses may give way to more reactive responses that risk amplifying cycles. Being too slow to react to inflation pressures is an immediate policy risk, hampered by an unwillingness to let exchange rates adjust in China, the substitution of capital account restrictions for policy tightening in a number of emerging economies and the lack of a clear path in advanced economies to withdraw the massive liquidity overhang from financial markets without unsettling them and the recovery (table 2).

The third area of agreement is that current fiscal situations in many countries — of which the US is the most prominent and important example — are not sustainable. But as soon as the discussion shifts to how, how much and how quickly to reduce deficits, consensus is the first to collapse, and considered policy analysis is not far behind. The complexity of the fiscal debates and the elusiveness of the solutions become greater as discussions of fiscal restraint intersect with perspectives on the size and nature of government.

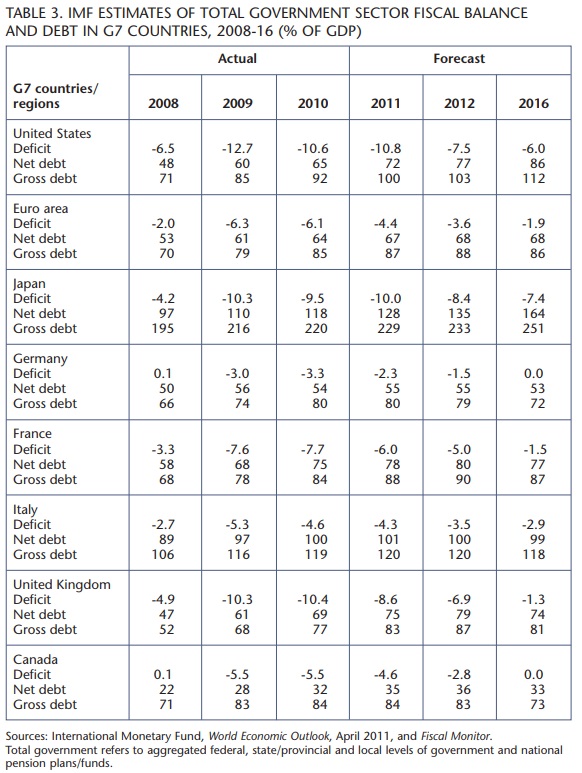

To get a consistent, cross-country snapshot of the fiscal challenges facing the United States, Canada and other G7 countries, an excellent place to start is with the IMF’s April 2011 Fiscal Monitor. It paints a stark picture of record government financing needs, rising debt ratios and fiscal sustainability risks in several systemically important countries, as well as in a number of smaller countries. Since the roles and responsibilities of the various levels of government differ across the G7 countries, I show in table 3 the IMF’s forecasts of fiscal balance for the total government sector (federal, provincial/state, and government and national pension plans), normalized for the size of the various economies. In the eurozone, which is anchored by Germany, the worry is less about the consolidated fiscal deficit and debt numbers than it is about their very uneven distribution across sovereign member states. The United States, unfortunately, is in another category.

The US total government deficit is estimated at 10.8 percent of GDP in 2011, with net debt at 72 percent of GDP and gross debt hitting 100 percent. Even with a sustained recovery, the IMF predicts there will be a deficit of 6 percent by 2016, an indication of how large the US structural deficit may indeed be. On its current fiscal track, without new deficit reduction measures, US total government net debt will approach 90 percent of GDP (and gross debt will exceed 110 percent of GDP) within five years. These are extraordinary levels of debt and structural deficits, even for the US, which has the world’s reserve currency and its largest economy.

Japan has been in a fiscal trap for some time, and this will only become worse as a result of the recent horrific natural disasters there. The Japanese fiscal safety net, domestic absorption of its government debt, will be tested by the huge refinancing it will need to rebuild the devastated areas of northeastern Japan. Italy, which remarkably avoided the extent of the increase in deficits experienced by the United Kingdom and France, is still constrained by its fiscal past, a great lesson to all of how high debt and debt servicing costs can handcuff governments.

Among G7 countries, Canada currently has a total government net-debt-to-GDP ratio of 35 percent, half that of the US and well below the EU average. The deficit of 4.6 percent will fall below 3 percent next year as legislated, time-limited stimulus measures end. The IMF expects the total government sector in Canada to return to fiscal balance by 2016, with net debt stabilizing near today’s ratio and gross debt just over 70 percent of GDP. Provided the federal government implements the quantum of fiscal restraint measures required to return to budget balance by 2015 as set out in the March 2011 budget, in the near term the main fiscal challenges will be significant structural deficits in several provinces.

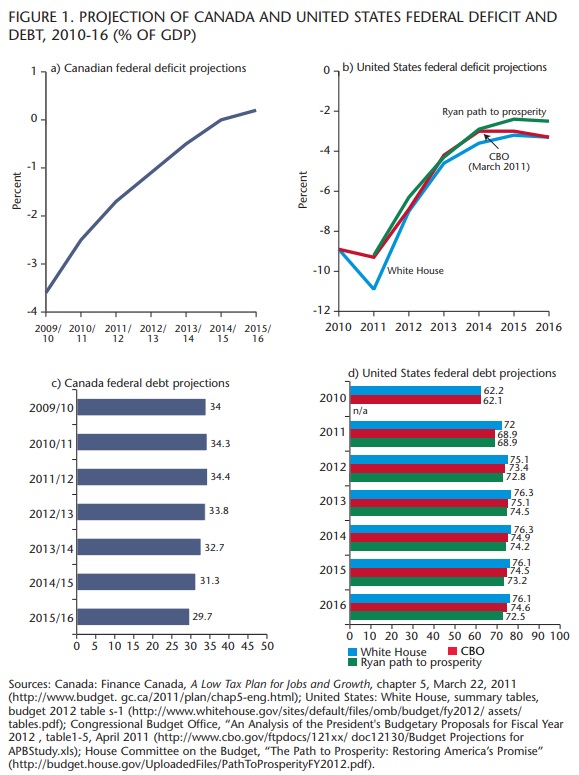

At the federal level in Canada the magnitude of the fiscal task ahead is quite different from that in the United States (figure 1a). The challenge in Canada will be to ensure that time-limited stimulus spending ends as planned, and then to enact sufficient fiscal measures to offset the increase in debt servicing costs that is due to the $160-billion increase in the debt since 2007 and any other noncyclical impacts on the fiscal framework, and to do so in a way that is structurally sustainable and improves government productivity.

The fiscal challenge in the US is in another league altogether, and there is a vigorous public debate under way about whether tax increases should play any role in deficit reduction, how deeply to cut and where, what types of expenditure reductions are consistent with views on the nature and size of government and how quickly they should begin. In addition, there is the problem of significant actuarial deficits in key social security trust plans. How the American fiscal debate will play out is anything but clear at the moment, and this fiscal uncertainty risks creating market volatility (figure 1b).

It is clear that our fiscal genie is huge, that its magnitude and the risks it poses vary across countries and that unsustainable fiscal situations in countries large and small can pose stability risks beyond their borders. Now, let us focus on how we might get the genie back into the bottle, with reference to the Canadian experience.

In the mid-1990s, Canada faced serious questions about the sustainability of its fiscal situation, including rising spreads on government debt (figure 1c). Canadian policy-makers came to the right conclusions: that fiscal gradualism was being swamped by debt dynamics; that growing out of the deficit neglected the inconvenient truth that servicing debt was a structural, not cyclical, problem; that an ever-increasing share of tax dollars going to debt servicing rendered the government less and less able to respond to urgent priorities; and that the greater loss of confidence came from inaction, not from resolute fiscal actions.

Disconcertingly, US government debt as a share of the American economy is fast approaching Canadian net debt peaks of the 1990s (figure 1d). And with no clear US fiscal exit strategy in sight, the IMF projects US net debt will continue to grow, reaching toward 90 percent of GDP by mid-decade.

In looking at areas for possible restraint, again past Canadian experience illuminates the ineffectiveness of across-the-board cuts to government operations, which typically starve capital and recruitment, and of attacks on waste and inefficiency, which have proven the fool’s gold of many restraint initiatives through the years.

What has worked is transparently eliminating or reducing programs, with commensurate reductions in budgets and employment; tackling inefficient tax expenditures, which are no different than ineffective programs; and considering targeted revenue sources. Credibility and confidence are enhanced by legislating multiyear fiscal restraint plans with built-in contingency reserves. What should also work today is to focus on improving the productivity of government operations, principally through restructuring the “back office” of government by abandoning outdated processes, investing in technology solutions and shifting to a smaller, more information-techology-enabled workforce.

Douglas Elmendorf, Director of the Congressional Budget Office, recently observed that the US faces a very large structural, not just cyclical, deficit, and that “U.S. fiscal policy cannot be put on a sustainable path just by eliminating waste and inefficiency; the policy changes that are needed will significantly affect popular programs or people’s tax payments or both.” And on the proverbial question of whether to reduce deficits gradually or quickly, he notes that a more rapid fiscal consolidation shifts more US savings to productive capital investments, reduces federal spending on interest payments, gives the government more flexibility to respond to unexpected problems and reduces the likelihood of a US fiscal crisis. All told, this is a pretty persuasive list of arguments for more deficit reduction, and earlier.

In contrast to previous global downturns, where financial sector and fiscal problems typically emerged in developing countries, we have now witnessed bailout packages for Greece, Ireland and Portugal. There is little optimism that Europe’s public debt woes are nearing a solution. Greece remains a worry to markets, judging by risk spreads of more than 1,500 basis points, fully 15 percentage points, over German bonds. The problem with Greece is not that the bailout austerity plan is unravelling, but that the numbers in the plan don’t easily add up with so much sovereign debt.

So is a Greek sovereign debt restructuring inevitable? It depends on how three irreconcilable factors are reconciled. First, Europe fears the contagion effects of a sovereign debt restructuring on other countries and the possible threats to eurozone stability. Second, German politics, which is rapidly hardening against bailouts, fears any actions that cost the German taxpayer money. Third, the EU and the IMF fear that any Greek debt restructuring would undermine the political will for continued austerity in Greece and elsewhere.

Where will all this lead? A plausible scenario is there will be a low-key, “muddling through” response by the EU and the IMF that restructures Greek sovereign debt implicitly, not explicitly, through maturity extensions, interest rate relief tied to new conditionality and secondary market buybacks. But this is in no way a solution to the fundamental problem of “fiscal free-rider” incentives in a monetary union without binding fiscal rules, combined with the large government sectors in a number of countries that are unaffordable, given their tax bases.

Now, more about our fiscal genie…and how we can make sure it stays in its bottle; there is a risk that it will catch a “second wind.”

This is because of a fiscal reality few are yet contemplating but none can avoid, and that is the challenge of longer-term fiscal sustainability. Within a few years we will be facing the painful intersection of a declining rate of growth in the labour force, thanks to our demographics; a declining rate of growth of productivity; and rising health and pension expenditures as our population ages.

Consider the inescapable math of sustainable nominal GDP growth: it is the simple addition of growth in productivity per worker plus growth in the number of workers plus inflation. Why is sustainable nominal GDP growth so important for fiscal sustainability? Because governments tax nominal income. Over the past 25 years in Canada, productivity growth averaged 1.3 percent, labour force growth 1.5 percent and inflation 2.9 percent yielding average nominal GDP growth of 5.7 percent. This is the growth framework upon which we have built our existing federal and provincial expenditure and tax programs.

Looking ahead to the medium term, however, declining productivity growth and aging demographics will negatively impact our longer-term fiscal frameworks. Productivity growth since 2000 has fallen to 0.8 percent, labour force growth has declined to under 1 percent and the Bank of Canada’s inflation target is 2 percent. Taken together, they suggest Canada faces a sustainable nominal GDP growth rate of around 4 percent. The US, with stronger productivity growth and somewhat better demographics, likely faces a sustainable nominal GDP growth rate near 4.25 percent in the medium term.

At the same time, demography-related spending on health and pensions will rise. For both countries, this fiscal reality suggests that current levels of government spending and revenues are not consistent with sustainable fiscal balance, unless we are able to raise productivity and labour force growth or restructure demography-related programs and systems.

This fiscal reality tale is a cautionary one. Governments have to make difficult decisions to rein in their deficits and rising debt starting now, with articulated and multiyear deficit reduction programs. This approach is multi-faceted: it needs to restore fiscal balance, to provide assurance to markets and to allow orderly adjustment to changes in programs, benefits and costs.

Governments need to embrace medium-term fiscal strategies that include enhancing longer-term growth as well as controlling spending. They need sustainable fiscal strategies that achieve budgetary balance, including financing investments to improve a country’s capacity to grow. Improving productivity growth, in the private sector and government, and enhancing the labour force through more skilled immigrants and more training are two of the most effective but underutilized tools in the fiscal sustainability tool box.

Getting the fiscal genie back in the bottle is only half the challenge; keeping it there has to be our longer-term preoccupation.

Photo: Shutterstock