Here are some quick reactions on the PBO’s latest report:

First, this should not come as big news to anyone who follows these issues closely. This report essentially puts numbers to the softer outlook for the Canadian economy — and thus the government’s bottom line — discussed at length during the election.

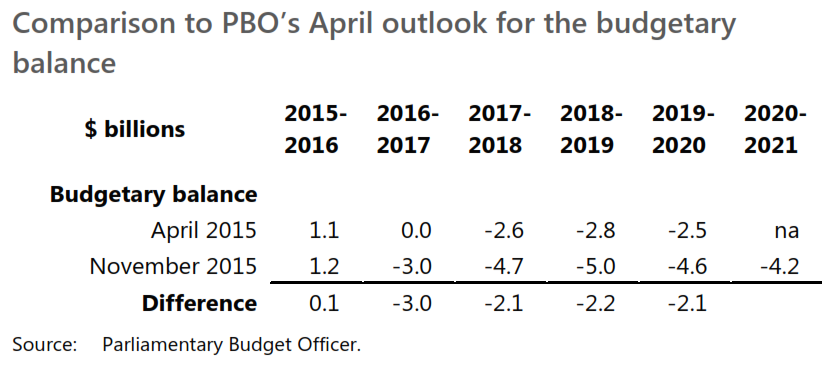

Not surprisingly, the current outlook is a bit worse than in the spring, and this seems largely due to lower oil prices and related investments.

While the direction of these forecast revisions were widely expected, the magnitudes involved aren’t large. On net, the deterioration is just over $2 billion per year for the government’s budget balance starting in 2016, relative to what the PBO expected in April. Economic developments or different modelling assumptions can easily shift these numbers by a few billion either direction.

The PBO thinks that the new Liberal government will inherit very modest deficits after this fiscal year, of roughly $4 billion a year on average — even before implementing their platform.

The PBO thinks that the new Liberal government will inherit very modest deficits after this fiscal year, of roughly $4 billion a year on average — even before implementing their platform.

So if I naively add in the Liberal platform by netting their new spending and revenues, then it’s certainly possible that annual deficits could exceed the $10 billion figure that was mentioned during the election.

And if you go further and account for the additional debt charges implied by the higher debt stock, this adds about $1 billion more to the deficit by the end of the projection.

But note that in this scenario, the deficit would peak at less than 1% of GDP, and the debt-to-GDP ratio — the more important indicator of the fiscal position — still improves over the projection. In sum, today’s news doesn’t fundamentally alter the federal government’s medium-term fiscal position, which remains pretty good.

Also this simple calculation assumes that implementing the platform doesn’t change the economic outlook. However, the increased government spending and middle-class tax cut could provide some modest upside to economic growth over the next few years.

(It also assumes that the Liberal cost estimates are correct, that the platform will be fully implemented as presented; and that the PBO economic and fiscal point estimates are correct. None of these assumptions hold in practice.)

In terms of the fiscal policy stance, if you think the new government was right to incur « modest deficits », then reasonable analysts would still think that deficits of either $9 billion or $16 billion both meet the « modest » criterion, in the grand scheme of a $2 trillion Canadian economy. So there’s no new reason to want the government to back-track on its policy agenda.

And if we suddenly fixate now on the $10 billion dividing line for judging the government’s fiscal performance, then we just repeat the same game as before that had a binary focus on $0 as a dividing line for surplus (good) vs. deficit (bad). Of course, this new line does afford the government $50 billion in fiscal room over the projection, so it does matter in that sense.

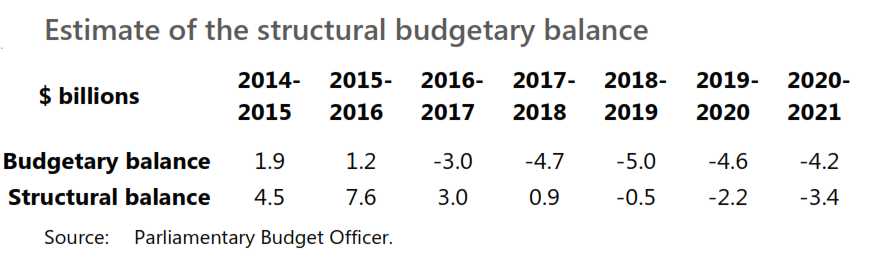

There is also the issue of whether the budget can be balanced by the end of the mandate. The PBO’s structural budget balance estimate sheds some light on this, and it shows a very small structural deficit in the outer years of the projection. This means that even if the economy is back operating at its potential in 2019, then the Liberals may still have some work to do if they want to hit that milestone. And as others have pointed out, their platform had few significant proposals to raise revenue as a share of the economy over their mandate.