By focusing too much on real GDP, Canadian recession debates are missing an important part of the story: our « trading loss ».

The chart below shows two indicators of Canada’s economic activity. The business press focuses a lot on one, but ignores the other.

The black line is real gross domestic product (GDP — here the expenditure-based, quarterly version) which gets all the attention.

The red line is real gross domestic income (GDI), a more arcane measure that gets little attention beyond a few economists.[1]

GDP versus GDI

GDP versus GDI

The two series are closely related, but distinct. Real GDP estimates the real value of what the Canadian economy produces, whereas real GDI estimates the real value of Canada’s purchasing power generated by this production. Organizations such as the Bank of Canada and the PBO have suggested that GDI is the more economically meaningful measure for Canada, yet it’s rarely discussed.

Some people prefer real GDI because it captures both production volumes (real GDP) and our real purchasing power from this production due to international price changes — the second part is the trading gain that’s largely due to changes in our terms of trade (the ratio of Canada’s export to import prices).

Research by Statistics Canada and the Bank of Canada finds that, over long time periods, real income growth is mainly driven by increased production. But over shorter periods of large relative price changes in global markets, the trading gain (or loss) can be quite important for countries like Canada, Australia, Norway, and New Zealand.

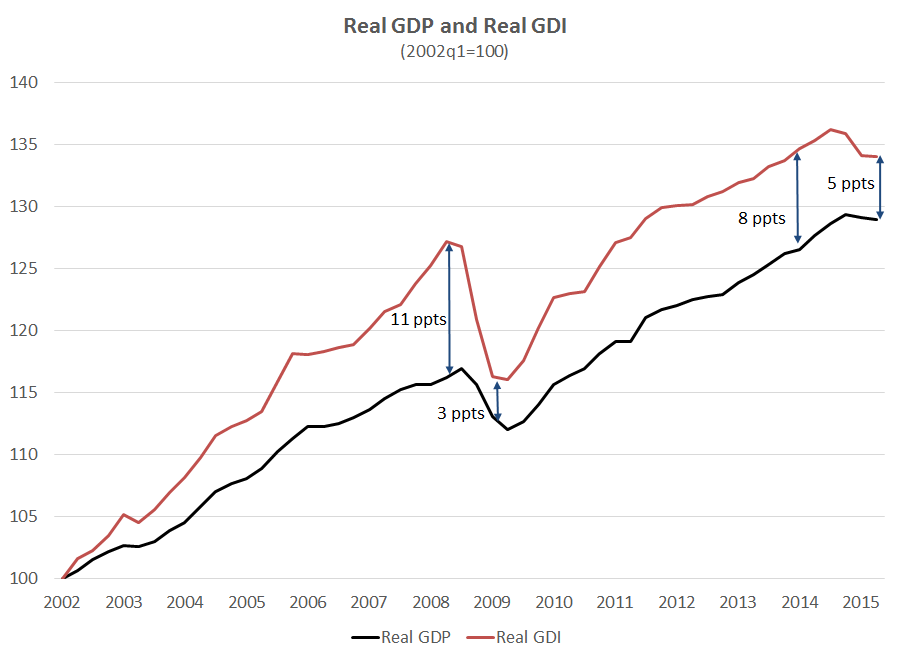

In the figure above, GDP and GDI are both indexed to 100 in 1981, showing that these two indicators grew by almost the exact same amount in recent decades.

But notice how the relationship between the two changed around 2002 when global commodity prices began to rise (the vertical line shows this break). Before 2002, Canada’s GDP slightly outpaced GDI; since then, GDI grew faster and was more volatile.

The recent period is blown-up here by re-indexing to 2002:

By now the story is familiar: between 2002 and 2008, the prices for the goods and services that Canada exports more intensively than other countries, such as crude oil and other commodities, rose much faster than the prices we paid for our imports.

By now the story is familiar: between 2002 and 2008, the prices for the goods and services that Canada exports more intensively than other countries, such as crude oil and other commodities, rose much faster than the prices we paid for our imports.

Why it matters

If we only look at real GDP during this period, and ignore real GDI, we miss about 40% of the overall gains due to the big improvement in Canada’s international purchasing power.

On the flip side, when commodity prices collapsed in the 2008-09 recession, GDI fell twice as much as GDP. So again, if we only look at GDP, we miss half the picture from the much bigger decline in our purchasing power due to our « trading loss ».

The excessive focus on real GDP in the current episode [2] — particularly the two consecutive quarters of negative growth — misses a crucial part of the story: the trading loss in Canadians’ international purchasing power due to the recent sharp drop in oil prices since the third quarter of 2014.

What can we do? Report supplemental metrics

Real GDI is reported in Statistics Canada’s official GDP release and has been for several years. But it’s given far less prominence and appears in a single sentence near the end.

Maybe there’s an easy way to provide a general audience with a complementary measure that provides a better view of Canada’s economic performance — particularly in the short-term when commodity prices move significantly.

Statistics Canada should consider following the lead of the US, where they’ve just starting releasing a supplemental estimate with their official GDP release — one that averages their income and expenditure-based GDP estimates. The Council of Economic Advisers calls this new measure gross domestic output (GDO),[3] and they’ve shown that it has generally been more accurate measure than the individual income or expenditure series.

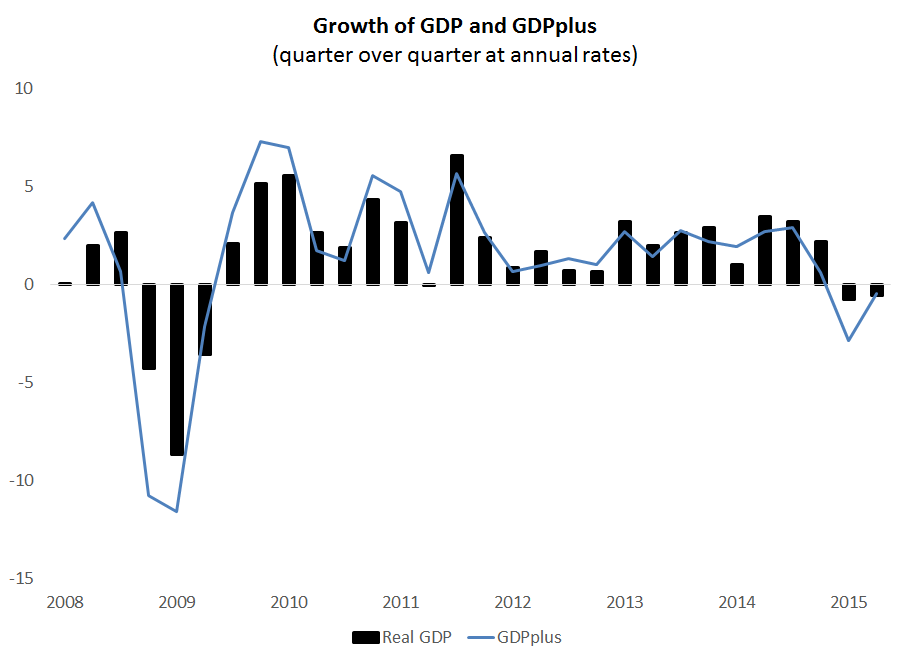

We could think of a catchy name for this new measure, maybe “real GDP-I” or “real GDPplus” (to borrow a phrase from the Philadelphia Fed). The idea is the same as when Statistics Canada reports supplementary unemployment rate to help counter various weakness inherent in any one measure.[4]

Averaging different series is a long-standing forecasting trick. It helps give a better read on the underlying situation by not placing all of your weight on one series (real GDP), while ignoring other useful, but related information (real GDI).

This new measure is shown along with real GDP in the figure below. By this metric, the downturn in the first half of 2015 has been worse than that conveyed by looking at GDP alone. Many of the on-going recession discussions in Canada miss this trading loss — and thus are unwittingly ignoring the broader picture of the economy’s weak short-run performance.