Several top economists are working to improve our understanding of how bad economic situations get worse and what to do about it.

Economics is often criticized.

A common complaint is that the profession didn’t see the Great Recession coming, and worse, that it failed to provide useful policy advice to address it.

The rumbling discontent of some critics is getting louder. For instance, at this year’s American Economic Association meetings (the AEAs, also known as the ASSA, is the profession’s largest gathering that occurs each January) a few ”œkick it over” protesters targeted this normally-subdued event to express their disillusionment with the field.

Many economists dismiss such criticism as uninformed or misguided. But, when done right, it can be constructive, by forcing those who provide influential policy advice to defend their work and consider alternative perspectives.

The problem with the most vocal and acerbic critics (including Black Swan author Nassim Taleb, whose tweet about the conference is shown below) is not that they complain that we can do better — they’re right, we can — the problem is that they ignore some excellent research that is taking place.

Today economists are at a gen conference #ASSA2015. If building collapsed would humanity suffer? No. Not the case with doctors, engineers…

”” Nassim NicholÙ†Taleb (@nntaleb) January 4, 2015

What I saw at this year’s AEAs was not a field dogmatically stuck in its ways, working on esoteric academic topics (yes, that’s there too). But many of the profession’s best are actively analyzing and debating important and unresolved issues that have broad societal reach ”” inequality, the possibility of secular stagnation, the recovery of the US labour market, how to apply insights from behavioral economics to improve public policy, and on the list goes.

Indeed, many serious economists are looking seriously at what went wrong in the past and are looking out for what might go wrong in the future ”” all with a view to identify policies that would improve things.

The ironic thing is that much like the economics protesters, many of the best economic researchers also want to ”œkick it over. » They just go about it differently. They are motivated to build models that better match data, resolve long-standing paradoxes, improve the measurement of things we care about, and collect new sources of information, and this work should not be overlooked.

Oilvier Blanchard (of the International Monetary Fund) is a case in point. His lecture humbly took stock of lessons from the crisis — which has reminded the profession that sometimes bad things happen, and when they do, it can be hard to get the economy back on track, even with well-designed policies.

There are situations where small shocks can get amplified (multipliers can be large, economic systems exhibit non-linearities and multiple equilibria). In these times, the effects of policy are more uncertain and implementing policies is highly contentious. Therefore, Blanchard cautions that it’s best to try to avoid these ”œdark corners” rather than have to escape them.

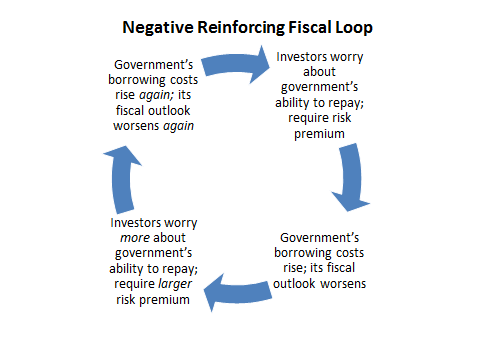

One example is the negative fiscal spiral that occurred in Greece and other peripheral European countries during the crisis.

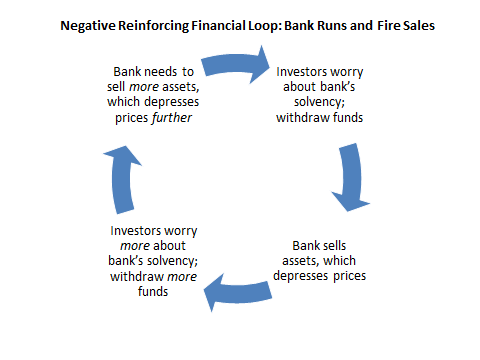

This logic also applies for financial spirals that can occur for loans to banks and other systemically-important financial institutions. In both cases, investors beliefs (optimistic or pessimistic) can be self-fulfilling:

This logic also applies for financial spirals that can occur for loans to banks and other systemically-important financial institutions. In both cases, investors beliefs (optimistic or pessimistic) can be self-fulfilling:

The interconnectedness of financial institutions can make things worse. One failing bank can act like a falling domino: it falls, which can take down another one, and another one, and so on.

The interconnectedness of financial institutions can make things worse. One failing bank can act like a falling domino: it falls, which can take down another one, and another one, and so on.

Europe suffered the perverse interactions that can occur between negative loops for a country’s government and its financial sector (which typically holds some of the government’s debt). Concerns that start as either worries about the solvency of the government or the financial sector can easily become concerns about both.

Economists are also concerned about the possibility that the monetary policy mechanism will once again become impaired (as occurred Japan for decades, and in the US since the crisis). For instance, Larry Summers predicted that there’s a ”œsubstantial likelihood” that the US Federal Reserve will be stuck at the zero lower bound again — we can expect another US recession in the medium-term, he said. And at that time, the policy interest rate will probably not be high enough to provide the room needed for rate cuts to return things to normal quickly.

Thomas Piketty‘s session clarified another concern regarding the difference between the rate of interest, r, and the growth rate of the economy, g. Piketty thinks that a larger r-g differential was not the primary cause of increased inequality in the US in recent decades. Instead, it acted as an amplifier that made things worse. A larger r-g gap makes it easier for the wealthy to earn higher returns on their savings than overall economic growth, and so inequality can perpetuate itself over time.

Atif Mian and Amir Sufi are worried about what happens when a housing boom that is fueled be leverage goes bust, and household consumption collapses for the most indebted families, with knock-on effects for the aggregate economy.

Fabien Postel-Viney and Giuseppe Moscarini think that the typical « job ladder » (whereby workers start out at smaller-firms and then move on to better-paying jobs at bigger companies) broke down in the last US recession. They think it has failed to recover since then, with the cascading effects that depress hiring throughout the economy.

All of these examples suggest that economists are looking to diagnose what went wrong in the crisis, some are developing early warning signs of what might cause the next crisis, and some are trying to design policy responses that would mitigate our chances of returning to the dark corners of our economic models — the places where amplifiers and negative feedback loops make it hard to escape what can sometimes seem like black holes.

*****

Recall the popular Sesame Street book where Grover is afraid of monsters lurking at the end of the book, while Elmo confidently walks on alone in search of the monster.

My message to the econ protesters is this: by all means challenge the economics establishment, press for better policies, better economic thinking and clearer communications. But be aware that many of the people you heckle have the same goals in mind. Let’s not ignore the good work that is taking place, and let’s not ignore that there are lots of Elmo economists out there. They are searching for what could go wrong — the proverbial monsters at the end of the book. The Elmos are the ones that will move the profession forward. And they’ll contribute more to address society’s economic problems than any of the protesters will.