Alberta is a rich province due to the fact the government and citizens of Alberta enjoy the benefits of a huge resource endowment in the form of oil and natural gas deposits. This endowment has been exploited within the structure of a royalty arrangement that, broadly speaking, balances the needs of industry to be rewarded for risky exploration efforts and, more recently, extraordinarily expensive oil sands developments with ensuring a fair share for the owners of the resource — the people of Alberta.

Unfortunately, a heavy reliance on resource exploitation carries with it the problem of wide swings in economic activity. With a large fraction of economic activity directly or indirectly tied to the energy sector, Alberta’s economy tends to vary with the price of fossil fuels. Booms and busts in economic activity are therefore as common in Alberta as booms and busts in energy prices.

In such economies, economists emphasize the need for governments to guard against allowing the volatility of the private economy to cause volatility in government spending. Thus a fall in energy prices should not be allowed to force cuts to spending on health and education nor should a boom in energy prices be allowed to fund an unsustainable expansion in these programs. The solution to this problem is to redirect the revenues gained from the sale of resources away from the government’s budget and toward saving. This is the solution to the problem of energy price volatility that has been successfully employed by energy-rich Norway. It is also the solution that has been long advocated by economists in Alberta and frequently urged upon the provincial government.

The Alberta government has not heeded the advice of economists. The provincial government in Alberta saved less than 10 percent of the $130 billion of natural resource revenue collected between 1970 and 2004. To the extent that resource royalties have been used to reduce income taxes and allow Alberta to finance high levels of public spending without the need of a provincial sales tax (Alberta is the only Canadian province without a sales tax) it would appear that the main role for resource rents in Alberta has been to augment private and public consumption.

In this article we describe the government of Alberta’s experience with the revenues it has collected from the exploitation of oil and gas and the particular challenges that the government has faced because of the province’s resource wealth. It is a story of failed efforts to keep energy price volatility from entering the provincial budget, with the result that budgets are allowed to balloon during energy price booms that are followed by harsh corrective measures after the inevitable energy price bust.

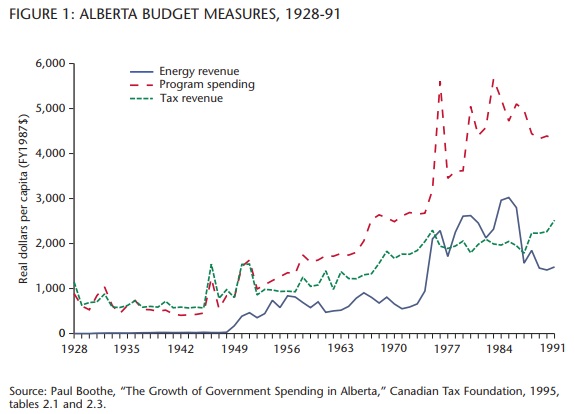

Figure 1 presents data from Paul Boothe’s monograph The Growth of Government Spending in Alberta, describing three time series on provincial government finances from 1928 to 1991. All three time series are measured in real (1987) per capita dollars. “Program spending” is provincial government spending on programs. “Energy revenue” measures the revenue collected by the provincial government by way of oil, gas and coal royalties and the investment income earned on savings. “Tax revenue” is defined as total revenues collected by the government less energy revenues. Thus “tax revenue” defines the revenue the government would have had available to fund program spending had it not had access to royalty income and the investment income earned on those amounts of royalty income that it saved.

The province of Alberta did not gain control of natural resources from the federal government until 1931. Gaining access to the revenues available as a result of controlling those resources did not, however, yield significant benefits during the 1930s and 1940s. Although energy revenue did flow to the government thanks to small oil and gas fields producing since the early 1900s, the dollar amounts were small. As a consequence program spending and tax revenue were closely linked and there was a clear price to be paid by taxpayers for new spending.

By August 1985 Saudi Arabia decided that it had had enough of this situation, and by early 1986 it had more than doubled its oil production. By mid-1986, the price of oil fell to a low of US$10 per barrel. Not surprisingly, the government of Alberta’s revenues took a catastrophic hit.

All of this changed in 1947 when a major oil field was discovered near the town of Leduc. After that, energy royalties grew quickly and by the mid1950s they were nearly as large as the total revenue gained from the taxation of individuals and corporations. After the initial growth in energy revenues they stayed more or less constant in real per capita dollars during the 1950s and 1960s. As illustrated in the figure, rather than save these revenues, the government used them to fund increases in program spending. As a consequence, a wedge was driven between tax revenues and program spending. Increasingly, new program spending was financed not by imposing tax increases on individuals and corporations but by spending the energy royalties earned on the province’s energy endowment. One might argue that to the extent Albertans own the natural resource, spending energy royalties is equivalent to taxation. Most would agree, however, that in the minds of citizens there is a clear distinction between the two, and the political implications of raising taxes on individuals as opposed to spending resource royalties are very different.

In the eight years prior to the first Organization of the Petroleum Exporting Countries (OPEC) oil price shock in 1973, the government of Alberta’s resource revenues averaged $290 million. The effect of the OPEC price shock, combined with the efforts of the newly elected (in 1971) Conservative government of Premier Peter Lougheed to negotiate a new royalty framework, contributed to a dramatic increase in resource revenues.

Although the rapid growth in energy royalties prompted a similarly rapid expansion of program spending, by 1976 tax and energy revenues combined were more than enough to fund program spending. This, plus the widespread expectation that energy revenues would continue to grow, prompted the government to introduce a savings plan. The result was the Alberta Heritage Savings Trust Fund (AHSTF), established with a special appropriation of $1.5 billionin 1976. The government further committed to depositing 30 percent of resource revenue that it collected into the AHSTF.

In the eight years following the first OPEC oil price shock, resource revenues averaged $2.5 billion per year. By the end of fiscal year 1982, the Heritage Fund had received $8.3 billion of resource revenue and had earned $2.65 billion in investment income. Despite $1.3 billion of spending on capital projects, the AHSTF was valued, at cost, at $9.7 billion in 1982. Had it grown only at the rate of inflation the $9.7 billion contained in the Heritage Fund in 1982, even with no additional contributions, would have been valued at $24.2 billion in 2010. As of December 31, 2010, the Heritage Fund was in fact valued by the Alberta government, at cost, at $15 billion. The real value of the fund has therefore been allowed to fall quite considerably over time.

The second OPEC price shock in 1979 gave added credence to the expectation that energy revenues would continue to grow. It was perhaps for that reason that in 1978 the provincial treasurer could afford to raise the possibility of increasing from 30 percent the share of resource revenue committed to the Heritage Fund.

The rosy budgetary picture of the 1970s came to an end when the federal National Energy Program (NEP) in 1980 and a deep North America-wide recession in 1982 combined to produce new challenges to provincial budget makers. The recession slowed the economy, and the NEP not only slowed the growth in resource revenues but prompted the provincial government to increase spending in the form of support to the energy industry.

Provincial support for the industry included a $5.4-billion program, introduced in 1982, consisting of royalty reductions and grants designed to increase the flow of revenue to the industry. In the same year the federal government would supplement this effort with its own $2-billion assistance plan. Measured in 2008 dollars, these two support programs were worth $17.2 billion, an amount considerably larger than the bailout offered to GM and Chrysler by the federal and Ontario governments in late 2008.

The effects of these events on the budget surplus were mitigated by the decision in 1982 to divert the investment income earned by the Heritage Fund to general revenues and to reduce the percentage of resource revenue deposited in the fund from 30 percent to 15 percent, two fiscal adjustments that at the time were envisioned to be temporary measures lasting only for two fiscal years but that would prove to be longer lasting. These measures, plus a renegotiation of some aspects of the NEP, caused resource revenues to recover and enabled the provincial government to remain in budgetary surplus until 1985.

As shown by figure 1, even though the National Energy Program of 1980 sent a significant portion of the government share of royalties to Ottawa, by the mid-1980s energy revenues flowing to the provincial government were now 50 percent larger than provincial tax revenues, and budgets remained balanced despite record program spending. Trouble, however, was on the horizon.

As Robert Mansell noted in a 1997 article, “Fiscal Restructuring in Alberta: An Overview,” the petroleum boom of the 1970s was never seen as a transitory, short-lived boom that would be followed by an inevitable bust, but instead was seen as establishing a permanently higher growth path for the Alberta economy. Signs that this optimism was unfounded soon became apparent. High and rapidly increasing world oil prices after 1978 had resulted in reduced demand for oil, and after 1981 prices began to moderate. The weakening demand for oil in the early 1980s was caused by the recession that struck the industrialized oil-consuming nations, by energy conservation by consumers, by the response of consuming households to conserve on energy needs by investing in energy-conserving changes to their homes and automobiles, and by consuming countries substituting away from oil to coal and nuclear energy. As Edward Kapels noted in his 1991 article, “The Fundamentals of the World Oil Market of the 1980s,” global oil consumption fell from 56 million barrels of oil per day in 1979 to under 45 million barrels of oil per day in 1983.

From 1982 to 1985, OPEC attempted to stem the reduction in world oil prices but it failed to enforce the production quotas it imposed on its members, and by 1985, the world price of oil stood at just under US$25 per barrel. Saudi Arabia through this period was the “swing producer” that cut its production to stem the falling prices that were caused in part by other OPEC members producing more than their quotas. By August 1985 Saudi Arabia decided that it had had enough of this situation, and by early 1986 it had more than doubled its oil production. By mid-1986, the price of oil fell to a low of US$10 per barrel. Not surprisingly, the government of Alberta’s revenues took a catastrophic hit.

Prior to 1986, the province’s most pressing concern was with the depletion of its resource base, but high oil prices were expected to solve that problem by finally making the exploitation of the vast northern oil sands economically feasible. With the collapse of oil prices in 1986, Albertans and their provincial government had to deal with a new economic reality. The collapse in world oil prices in 1986 — which saw the Canadian-dollar price of oil fall by 47 percent in real terms — devastated the provincial budget. The budget for fiscal year 1987 felt the brunt of a 63 percent loss in resource revenue and 30 percent loss in total revenue. Newly elected in 1986, Premier Don Getty noted that he had “inherited an economy and budget based on $40 oil — and the price of oil was $13.” The government’s immediate response was to grab more revenue. With fiscal year 1987/88 the government completely abandoned its efforts to save nonrenewable resource revenues and diverted all investment income earned by the now moribund Heritage Fund into general revenues.

On the expenditure side, the government largely behaved as if it expected the good times associated with high oil prices to return at any time. The spending side of the budget seemed stubbornly unable to respond in a significant way. Premier Getty remarked that trying to control spending after the prolonged period of strong revenue growth was akin to “turning the Queen Mary.” As a consequence, and despite the grab of additional revenues, the budget plunged into deficit after 1986 and would remain in deficit for the next nine fiscal years. By the end of fiscal year 1994, the provincial government had moved from a net asset position of $12.6 billion in 1985 to a net debt position of $8.3 billion: a $21 billion loss in wealth.

Despite evidence that the world market for oil had adjusted in a way that should warrant caution, the budgeting choices of the provincial government during the late 1980s and early 1990s reflected the earlier optimism that prices would resume their upward trend. Premier Getty’s quote about inheriting an economy and budget based on $40 oil when the price turned out to be $13 highlights how the Alberta government budget and economy had treated the extremely high prices of the late 1970s and early 1980s as a permanent condition. But the quote also misrepresents the nature of the Alberta government’s problems after 1986. Alberta didn’t have a revenue problem, it had a spending problem. In constant purchasing power terms, a barrel of oil after 1986 was worth more than at any time between the end of the Second World War and 1973, and as much as a barrel of oil from 1974 to 1978. So, from a long-run perspective, oil prices observed during the mid-1970s were in effect permanent. What proved to be transitory were the high prices observed from 1979 to 1985. Thus, the source of the government’s fiscal problems was the belief that the level of prices attained after a rapid escalation in price was sustainable. This misguided belief would again prove to be the government’s downfall 20 years later.

The 1980s proved to be a disastrous decade for provincial budget makers. The government’s heavy dependence on royalty income and its reluctance to either quickly cut those expenditures or quickly raise tax rates following the loss in energy royalties caused it to allow its strong balance sheet to deteriorate into one awash in red ink. Steadily growing servicing costs on a growing debt would make the inevitable fiscal adjustment larger and more painful the longer the government waited to make that adjustment. The reality that Alberta had been living through a transitory boom took a remarkably long time to sink in and it was only after eight years that the inevitable adjustments were made to put the province’s finances back on the road to fiscal rectitude.

Despite evidence that the world market for oil had adjusted in a way that should warrant caution, the budgeting choices of the provincial government during the late 1980s and early 1990s reflected the earlier optimism that prices would resume their upward trend. Premier Getty’s quote about inheriting an economy and budget based on $40 oil when the price turned out to be $13 highlights how the Alberta government budget and economy had treated the extremely high prices of the late 1970s and early 1980s as a permanent condition.

The inner workings of governmentKeep track of who’s doing what to get federal policy made. In The Functionary.The FunctionaryOur newsletter about the public service. Nominated for a Digital Publishing Award.

The inner workings of governmentKeep track of who’s doing what to get federal policy made. In The Functionary.The FunctionaryOur newsletter about the public service. Nominated for a Digital Publishing Award.

Concern over the long string of deficits that followed the collapse of oil prices in 1986 provided the focus of the election campaign in the summer of 1993. The 1993 provincial election in Alberta was fought over how to respond to the rapid accumulation of debt that had occurred over the previous nine years. All three major political parties supported taking strong steps to eliminate the deficit, and both the Liberal and Progressive Conservative parties advocated deep cuts to government spending in order to achieve it. The Progressive Conservatives, led by new leader Ralph Klein, were elected to a majority government in June 1993 on a platform of a 20 percent cut to spending.

The new premier proclaimed that Alberta had a spending problem, not a revenue problem, so that the elimination of the deficit would come from cuts to spending, not from increases in tax rates. Since the deficit was then equal to 20 percent of expenditures, a dramatic cut in program spending was required. The first budget of the new government called for not only a deep, but also a speedily implemented, 20 percent cut in spending to be completed by the end of fiscal year 1996. The promise to eliminate the deficit via a cut in program expenditures was kept. Relative to values at the end of fiscal year 1993, real per capita program expenditures had fallen by 31 percent by the end of fiscal year 1997 and the deficit had been eliminated. The price of adjustment was high. Cuts to spending on public health care, for example, were accompanied by the closure of hospitals.

While the most public of the new government’s efforts to regain control of its finances, cuts to program spending were not the only measures taken. The process of budgeting in Alberta would also change in the 1990s. Important in that period was the easily identified and understood target — a zero deficit — an unwavering dedication to meeting that target by both the Premier and the Treasurer, and the speed with which it was accomplished.

Most important of all, however, were the changes in legislation that provided a method for the government to build credibility by systematically meeting pre-announced deficit targets on the way to the goal of a zero deficit, and which enabled the government to manage a long-standing budgeting problem: the volatility of its revenues.

The strategy of announcing long-term fiscal targets as a way of imposing discipline on annual budgeting exercises proved to be highly successful. With the elimination of the deficit in 1995 the government introduced a new long-term fiscal target: debt elimination. In exactly the same way as former premier Lougheed’s governments tried to restrain expectations for new spending by formally committing to a savings target, the Klein governments used long-term fiscal commitments to provide guideposts for annual budgeting efforts to follow and force the government to constrain spending even in the face of rapidly growing resource royalties.

The target of debt elimination was met during fiscal year 2000. A new long-term fiscal target has not to this date been announced, though one has recently been suggested by a government-appointed panel. The Alberta Financial Investment and Planning Advisory Commission recommends the government adopt a long-term target of building a savings fund to $100 billion by 2030.

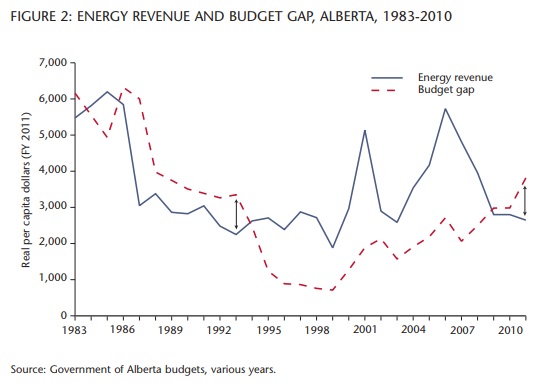

Figure 2 picks up the story left off by figure 1 by presenting budgetary data from 1983 to 2011. The data in the figure continue to be measured in real per capita dollars though now the base year has been changed to 2011. The data shown by the solid line measures energy revenues similar to those presented in figure 1. The data shown by the dashed line define what we call the “budget gap.” We define this gap as the difference between government’s spending on programs and the amount it collects in revenue from all sources except revenue gained from energy royalties and investment income spun off by the government’s savings funds. Thus the budget gap is the difference between program spending and tax revenue defined for figure 1 and measures the excess of what Albertans received by way of government programs over what they paid for those programs by way of taxes.

To illustrate how to interpret the figure, the per capita budget gap of $4,935 (or $11.8 billion in total) for fiscal year 1985 indicates the government was spending $4,935 more per capita than it collected by way of taxes from individuals and corporations. Clearly, such a gap would result in a budget deficit unless there was something to fill it. In 1985, the government enjoyed $6,196 per capita ($14.8 billion in total) of energy-related revenues and this was more than sufficient to fill the budget gap. So long as the budget gap can be kept below energy revenues, the government realizes budget surpluses and can accumulate savings.

Figure 2 illustrates a useful way of understanding how the government’s budget responded to the 1987 crash in energy prices. The boom of the late 1970s and early 1980s enabled the government to afford a large budget gap because energy revenues were more than sufficient to fill that gap. Following the collapse of oil prices in 1986, the government responded by cutting the size of its budget gap but not by as much as the fall in energy revenue. The level of energy revenues had fallen well below that required to fill the fiscal gap and so the government fell into deficit. Until 1993, little was done to reduce the size of the fiscal gap and so bring it in line with the new lower level of energy-related revenues. As a consequence the government’s budget fell into a prolonged period of deficits and rapid debt accumulation.

By 1993, the government of Alberta’s net asset position had been completely wiped out and it was now the owner of a considerable amount of debt. The election of Ralph Klein and the introduction of a no-deficit fiscal rule forced a realignment of spending so that it more closely matched the revenues the government collected from nonenergy sources. That is, the government dramatically reduced the size of its budget gap so that it fell below the persistently low level of energy-related revenues. In this way, the government moved into budget surpluses in fiscal year 1995 and it began to retire debt.

By 1999 the government had reduced the size of its budget gap sufficiently that energy-related revenue, which was then being generated while the wholesale price of oil in Canada was averaging just $27 per barrel, was sufficient to more than fill the fiscal gap and so enable the government to maintain budget surpluses even with low energy prices. So long as oil prices remained at or above this price, the government in 1999 had established a fiscal regime that was sustainable over the long term. This, however, was not to last.

Energy prices and energy-related revenues began to turn around starting in 2000. Energy revenues increased rapidly and, particularly after 2002, began a steady climb upward that peaked in 2006. The government responded to this influx of revenue with startling speed. Indeed, after 1999 there is a disconcertingly close relationship between movements in the budget gap and movements in energy revenues.

The government’s fiscal choices made during the 1999-2006 boom in energy revenues clearly suggest a return to the same optimistic view of the earlier boom of the 1970s: that higher energy revenues were permanent and so could be relied upon, to a growing degree, to fund program spending on health, education and social services. Financed by the growth of energy revenues, between 1999 and 2011 real per capita program spending increased by an average of 3.5 percent per year.

The only break in the relationship between energy revenues on the one hand and tax cuts and spending increases on the other occurred after 2008. But here the break was not in a way that would reduce the government’s reliance on volatile energy revenues. On the contrary, despite continued reductions in energy revenue the government continued to increase spending and introduce tax cuts and so caused the budget gap to grow. In an astonishing example of optimism in the face of falling energy revenues, in 2009 the government eliminated health care premiums for an annual loss of $1.2 billion of revenue. In 2006 it had given away $1.4 billion in the form of a one-time transfer to Albertans. These $400 cheques, provided to every Albertan, were taxfree and popularly known as “Ralph bucks” in reference to Premier Ralph Klein. In ways such as these the government increased its reliance on energy revenues, even as those revenues continued a precipitous decline.”

By the end of fiscal year 2011, government estimates show, the budget gap had grown to $3,815 per person (2011 dollars). This is larger than the size of the gap in 1993 ($3,350) and marks a more than five-fold increase in the size of the gap from what it was in 1999 ($712 per person) following the draconian cuts to program spending introduced by the Klein government. The earlier effort to reduce dependence on volatile energy revenues, which was the hallmark of the Klein government and its response to the earlier experience with boom and bust, has been completely unravelled.

In an earlier paper, remarking on data describing the government’s fiscal situation up to 2009, we warned of the danger that if the government did not act quickly and decisively to halt the growth in its budget gap it was likely to find itself in the same situation as a previous government 20 years previous. As figure 2 illustrates, since 2009 the budget gap has grown significantly larger. What’s more, energy revenues have fallen to the same real per capita value seen throughout the 1990s: about $2,600 per person. The net result of these adjustments is that the budget gap in 2011 exceeds energy revenues by almost exactly the same amount — $1,100 in real per capita terms and identified by the black arrow — by which it exceeded energy revenues in 1993. Thus the government in 2011 finds itself in the same budgetary situation that in 1993 was deemed a sign of a budgetary crisis of sufficient concern to warrant the 20 percent cut in program spending. It is indeed déjà vu all over again.

Since the early 1950s, the government of Alberta has enjoyed the benefits of having access to a large amount of revenue earned on the sale of nonrenewable resources. Unfortunately, the size of the bounty cannot be known with any degree of certainty and this makes budgeting challenging. Twice since 1970 the government has had to deal with a precipitous fall in energy revenues, first in 1987 and again starting in 2006.

In the earlier period the government allowed its budget to become heavily dependent on energy-related revenues — a notoriously uncertain revenue source. In doing so the government adopted a high-risk budgeting strategy that would demand painful adjustments to provincial government spending or tax rates should energy-related revenues suffer a precipitous decline. When that decline came in 1987, the government made the inevitable adjustment worse by delaying its implementation until 1994. For six years, from fiscal year 1988 to 1993, the government chose not to reduce the size of its budget gap to match the new, lower level of energy-related revenues. By that time draconian cuts to provincial government spending were required to re-establish a fiscally sustainable budget. While we appreciate that it is easy to have 20-20 rearview vision on these matters, we nonetheless find it difficult to understand how the government could have allowed its budget gap to be so unresponsive for so long to the evidence that energy prices would not soon return to pre-1987 levels. The inevitable fiscal adjustment — an adjustment that can be measured in closed hospitals and deteriorating public infrastructure — was considerably more painful than that which would have been required had action been taken earlier.

Following the fiscal adjustments necessitated by the 1987 fall in energy revenues, the government was in an enviable position. Spending levels and tax rates were at levels that ensured budget surpluses even while energy revenues were low. A commitment to match spending increases with increases in tax revenues — that is, a commitment to hold the budget gap constant — would have guaranteed long-term fiscal sustainability and growing savings. Instead, a new energy price boom in 1999-2006 encouraged the government to fund new spending and new tax cuts with uncertain energy revenues. This was a repeat of behaviour that necessitated the draconian spending cuts of the mid1990s. Despite the return of energy revenues to the level of the 1990s, the government continues to allow its budget gap to grow. In recent years, the growth has been funded by drawing down savings. Between 2010 and 2014, for example, the government estimates it will draw down its savings by another $13 billion.

The painful adjustments that were made in the form of draconian cuts to government spending during the mid1990s had their origins in two earlier budgeting choices. The first was the decision to adopt the high-risk budgeting strategy of allowing the budget to become heavily dependent on a volatile source of revenue. The second was the failure to act quickly when a precipitous fall in energy prices exposed the consequences of the first choice. It is unfortunate that during the latest energy revenue boom the government repeated the first budgeting mistake. It is doubly unfortunate that it appears to also be repeating the second mistake of delaying the inevitable adjustment to its finances. The delay is being financed by a rapid dissipation of financial assets. When these are exhausted, it will be time for another program of draconian spending cuts such as those introduced in the mid-1990s.

The long experience of the government of Alberta with the budgeting consequences of volatile energy revenues is worthy of study by other governments, particularly those that have only relatively recently begun to collect such revenues. The government of Newfoundland and Labrador, for example, estimates that in fiscal year 2011 it will have collected 34 percent of its total revenues from offshore royalties. Our suggestion to other governments is that they adopt the recommendation of economists to guard against allowing the volatility of the private economy to affect their budgeting choices.

The solution to this problem is to redirect the revenues gained from the sale of resources away from the government’s budget and toward saving. This entails the establishment of some form of a fiscal rule: a commitment to long-term fiscal probity that enables the government to resist the demands for unsustainable spending increases or tax cuts. As we noted previously this is the solution to the problem of energy price volatility that has been successfully employed by energy-rich Norway and that has been frequently urged upon the Alberta government. Unfortunately, it is a solution that has eluded the government of Alberta, which instead has adopted a high-risk budgeting strategy of funding health care and education with a volatile revenue source — a strategy that has, for the second time, come back to haunt it.

Photo: Shutterstock