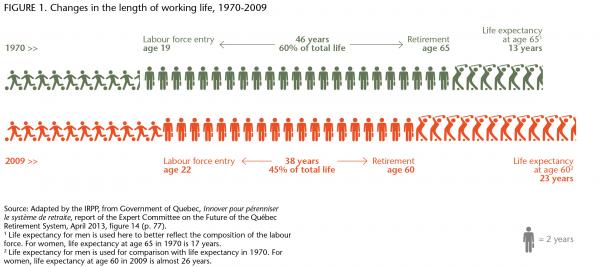

Quebecers are living longer than ever before. Those born in the province today can expect to live, on average, 10 years more than a Quebecer born in 1960. In 1960, a Quebecer turning 65 could expect to live another 14 years. By 2010, 75-year-olds could, on average, expect to live another 13 years.

These are dramatic demographic changes. The expanding population of seniors challenges us to ensure they live out these longer lives with dignity, and doing so requires a healthy pension system that, for many, is an essential source of income. These new demographics require us to examine whether a pension system designed to meet the needs of previous generations can accommodate the shifting — and increasing — demands of the next.

Our expert panel was asked by the Quebec government to look at the many problems that are weakening the provincial retirement pension system. But what started as a specific review of defined-benefit pension plans quickly broadened to cover the whole pension system.

Several issues stood out in the course of our review. Although the public pensions available to Quebecers are more than adequate for the lowest earners, the pensions have evident limitations for workers earning median or higher earnings. Given that nearly one in two workers does not have any form of pension and that defined-benefit plans are under considerable pressure, it was clear to us that our proposals had to be a solution for all Quebecers.

For this reason, in addition to the 15 out of 21 recommendations that specifically relate to defined-benefit pensions, the committee proposed one core innovation: the creation of a longevity pension that would be payable starting from age 75. The plan fits into the broad logic of the three values that informed the committee’s work: equity, transparency and accountability. And we believe that Quebec, and Canada if it chooses, can become one of the best places in the world for providing financial security for workers after they retire.

The committee looked first at the feasibility of enhancing the Canada Pension Plan/Quebec Pension Plan (CPP/QPP). But the CPP/QPP was developed 50 years ago in the context of a completely different demographic reality. We concluded the creation of a longevity pension that takes the new economic and demographic system into account was a better option.

The CPP/QPP and the longevity pension are completely different. The CPP/QPP is only partially funded and delivers benefits other than the retirement pension. The longevity pension will be fully funded and will deliver only a retirement pension. It would be a better option than enhancing the CPP/QPP in four ways:

- The contribution rate required to fund the plan would be lower.

- It would be fully funded and would operate independently, eliminating the risk of cross-subsidization.

- It would retain an important role for existing workplace pension plans.

- It would not encourage early retirement.

The committee reflected long and hard on the parameters to be employed for the implementation of the longevity pension. The age of eligibility — 75— was not chosen randomly. Today, being 75 is equivalent to being 65 when the CPP/QPP was created in the mid-1960s. The longevity pension will provide for retirement savings up to advanced age, without removing individual responsibility for saving.

And the plan is based on realistic assumptions. The cost estimated by the Régie des rentes du Québec is 3.3 percent of salaries, financed in equal part by employees and their employers.

It is useful here to outline the principal advantages of the proposed longevity pension.

First, it will be fully funded, so it will observe for the most part the principle of intergenerational equity. It will offer greater benefit to those who contribute for longer: that is, the young.

Second, a considerable number of people have no access to a collective savings plan and thus to any pooling of their longevity risk. For these people, the longevity pension will collectivize the risk of living longer, thus mitigating that risk.

What does this mean? A person who reaches the age of 65 today has a 1-in-2 chance of living to the age of 85, but has also a 1-in-10 chance of living to the age of 95. If one is managing one’s longevity risk alone, one has to have enough personal savings for 30 years, and not just the 20-year average. By pooling that risk, the longevity pension will reduce uncertainty about whether people will outlive their savings. It will reduce the amount that has to be saved for each individual’s retirement.

Third, the longevity pension is an efficient way to manage collective savings. The plan would have professional asset management and the administrative costs would be low.

Fourth, the longevity pension would reduce the pressure that people living longer puts on the cost of defined-benefit pensions, since the CPP/QPP and the longevity pension can be coordinated.

Fifth, the longevity pension would facilitate retirement planning. For example, one of the problems of defined-benefit pensions arises when members in the plan changes jobs. With the longevity pension, such people will not lose any benefits. The pension credits accumulated every year will be indexed according to salary, regardless of the number of jobs the worker has occupied.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

Sixth, the longevity pension would reduce the gap between members of defined-benefit plans and other workers. Everyone who contributes will have access to benefits.

Under the longevity pension, all Quebec workers would be covered, and contributions would be mandatory. It is meant to be not a social contract but a retirement plan, intended for the future. The level of benefits would be based on how many years workers contribute to the plan and the income they earn.

For each year that people contributes they would accumulate a pension credit equal to 0.5 percent of their earnings that year, up to the limit of the maximum pensionable earnings ($51,100, the same ceiling as in the CPP/QPP). People who have contributed for 10 years would have the right to a pension of 5 percent their indexed salary, starting at age 75. This rises to 10 percent after 20 contribution years, and to 20 percent after 40 years, and so on, with no limit on the number of years of contribution and credit.

Although we are living longer, on average, some demographic groups still have a lower life expectancy. Men and low-income earners tend to live shorter lives than women and those with higher incomes. Critics might argue that these groups would benefit less from the longevity pension, since it does not start until age 75. This problem is not exclusive to the longevity pension; it is also true of the current CPP/QPP, because the contribution and eligibility requirements are the same for all workers. To address this, the longevity pension guarantees benefits for five years; if workers die before they retire, their survivors would be entitled to the same benefits for five years.

As to the contention that a longevity pension would force people with low incomes to save pointlessly, since they are less likely to live long enough to collect the pension, again, the same situation applies with the current CPP/QPP. We do not exclude low-income earners from the CPP/QPP because they are also entitled to receive the Guaranteed Income Supplement (GIS), whose aim is to reduce poverty among the elderly by offering supplemental benefits, rather than being a financial tool for retirement planning.

Because salaries generally increase at a rate higher than inflation, and federal programs like Old Age Security (OAS) and GIS increase only at the rate of inflation, the value of these targeted retirement benefits is constantly falling behind. Moreover, since the OAS and GIS are entirely unfunded, their financing is subject to political decisions, which can impose risks for beneficiaries. (The federal government’s decision to increase the age of eligibility for the GIS from 65 to 67 years in the 2012 federal budget is a good example of this.) The committee decided to not put the most disadvantaged at risk by expecting them to rely solely on these programs.

The projected costs of the longevity pension were calculated conservatively, using an expected real rate of return of 3 percent, after adjusting for inflation. As the longevity pension would be fully funded, this rate is below that used for the actuarial analysis of the QPP, which uses a rate higher than 4 percent. This is particularly significant because only a small part of the QPP’s benefits is prefunded — less than 20 percent today — whereas the longevity pension would be fully capitalized.

Three values informed the committee’s work: equity, transparency and accountability.

Improving on a plan where the pension can be cashed in from age 65, but which would include the possibility of doing so from age 60, would require much higher contributions than a pension that kicks in starting at age 75. Since it would target better the longevity risk, the longevity pension would end up being less costly, for workers and for employers.

While an enhancement of the CPP/QPP should be totally funded, which the current CPP/QPP is not, the committee felt that it would be difficult to really separate the financing pertaining to current benefits from the funding of those associated with the enhancement. If the QPP was ever under pressure, there would be a risk that the QPP benefits could be cross-subsidized. Since the longevity pension would be separate, we can be sure that contributions to its funding would actually go toward funding it!

An overgenerous enhancement of the CPP/QPP would call into question the very existence of current pension plans. The committee believes in diversification and believes there is a place for private initiative. For a worker who has a workplace retirement plan and who earns around the maximum pensionable earnings, an enhancement that brought the replacement rate up to 50 percent, plus the OAS, would considerably reduce the coverage required from the workplace retirement plan, once the two were coordinated. The longevity pension would allow personal savings, company plans and personal choice in good measure to be preserved.

But most important, in the committee’s view: the longevity pension would not affect the continuation of active life into retirement. This is imperative, given the impact of an aging population on the availability of labour. By contrast, the CPP/QPP tends to encourage early retirement. In fact, two-thirds of Quebecers take retirement at age 62 or earlier. Opting to improve the current QPP would only exacerbate this phenomenon.

The longevity pension has been designed to manage the risk of more people living longer, without necessarily offering an incentive for people to retire earlier. It would avoid making young people contribute toward an early retirement they probably do not want. And we are convinced that this plan to deal with the challenge of people living longer lives could be a model for the rest of Canada as well.

The committee was chaired by Alban D’Amours, former president and CEO, Desjardins Group (from 2000 to 2008). The other members of the committee were René Beaudry, actuary, partner, Normandin Beaudry; Luc Godbout, tax specialist, Université de Sherbrooke; Claude Lamoureux, actuary, president and CEO of the Ontario Teachers’ Pension Plan (from 1990 to 2007); Maurice Marchon, economist, HEC Montréal; Bernard Morency, actuary, Executive Vice-President, Caisse de dépôt et placement du Québec; and Martin Rochette, lawyer, senior partner, Norton Rose. An English summary of the report may be found here.

Photo: vectorfusionart / Shutterstock