Canadians are beginning to realize the significance of Asia’s rising economic and political influence and the need to engage with the region. Bold leadership is now required to shape Canada’s response in a spirit commensurate with the region’s growing importance. Canada needs a generational, multidimensional economic strategy to support and advance its interests. Two pillars of this strategy should be a serious commitment to political security issues and engagement through state-to-state relationships that provide the foundation for commercial, political and other relationships.

In this article I begin by outlining some of the major changes underway in the Asian economies and then move to Canada’s indifferent record in the region. The discussion then moves to the economic challenges Asians face and the related opportunities implied for Canada. I conclude with a strategic proposal for Canadians.

Many in Asia claim this to be the Asian century. Within a decade the United States will drop to number two in the ranks of the world’s largest economies and Canada will move down within the top 20. The Asian Development Bank estimates that within 20 years Asia’s middle classes will number more than 2 billion people, and trillions of dollars will have to be invested in the physical and social infrastructure they — and the aging populations of countries such as Japan and China — will demand.

Asia is rapidly urbanizing: within a decade it will contain 13 of the world’s 25 largest metropolises, each with more than 10 million people. And Asia is integrating, as major investments are made in connectedness to facilitate intra-regional trade. Asian enterprises are also moving up the rankings of the world’s largest firms and financial institutions: in 2010, 23 of the top 100 of the Fortune Global 500 by total revenues were Asian, 11 from Japan, six from China and three from South Korea.

Asians increasingly “think Asian.” They are creating their own regional institutions in security, finance and trade — and inviting the United States to join. They are anticipating the move away from export-led development models focused on final markets in the advanced industrial countries. India and its dynamic service sectors aside, most East Asians participate in regional production networks organized around Chinese assembly platforms. These regional networks proved to be a double-edged sword in the global financial crisis when export demand in final goods markets evaporated, a shock that cascaded through Asian supply chains. The wake-up call prompted East Asian governments to begin shifting their growth strategies toward regional and domestic demand — which will require heavier reliance on other sources of growth, such as services and improved productivity, to replace low-cost manufacturing — and slower growth.

Unthinkable before the global crisis, slower growth in Asia now seems inevitable as social and political tensions rise over the side effects of rapid industrialization, rising income inequality and environmental degradation. Sustaining economic growth through productivity increases and innovation, which require institutional changes, is proving a challenge. In the decade ahead, we can expect growing pressures on Asian policy-makers to improve income distribution and services, particularly those that fulfill middle-class aspirations for housing, health, education, financial security and environmental quality.

Many in Asia claim this to be the Asian century. Within a decade the United States will drop to number two in the ranks of the world’s largest economies and Canada will move down within the top 20.

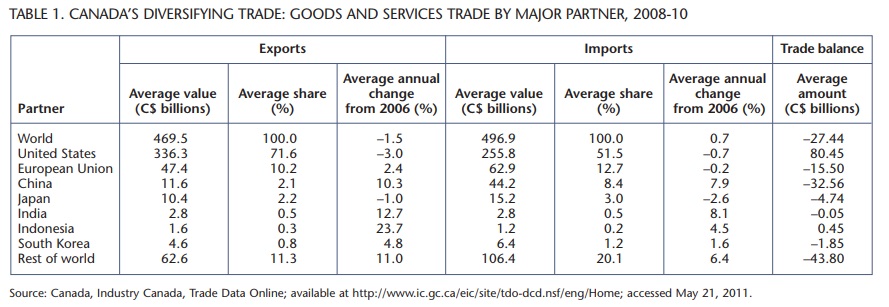

Despite the fundamental reshaping of the international economic landscape, the world’s largest trading relationship remains that between Canada and the United States (see the table below). Indicative of the recent sea change, however, is that China is now Canada’s second-largest trading partner, though Canada-China trade still amounts to just 10 percent of Canada’s trade with the United States. Canada’s next two most important Asian trading partners are Japan and South Korea, with India and Indonesia lagging far behind.

Even so, in the past five years Canada’s exports to China, India and Indonesia have grown at double-digit rates while those to the United States and the European Union have grown more slowly or even shrunk (see the table below). Flows of immigrants and students are also significant, with China topping the list of numbers of immigrants, followed by India, Japan and South Korea. More Canadians live in Hong Kong than anywhere else in Asia. Measured by stocks of foreign direct investment (FDI), however, the Asian economies remain well down the list as both destinations and sources, with both Japan and China trailing Brazil’s C$15 billion stock of FDI in 2009.

Canada’s nascent trade patterns reflect Asia’s challenges. These offer opportunities for Canadian businesses in areas ranging from demand for agricultural, energy and natural resource commodities to such services as construction, environmental and those demanded by the expanding middles classes such as finance, health care, education and tourism.

China’s commitment to green energy sources and a cleaner environment has triggered a wave of activity in clean technologies, including smart grids, carbon capture and storage, and battery storage technologies. These priorities could create major opportunities for Canadian firms in energy and other consulting services that assist, for example, in the design and expansion of conservation activities.

China’s targets for biotechnology and nanotechnology as areas for breakthroughs in basic research signal a larger set of educational opportunities. The state has planned a total investment of US$20 billion in biotechnology by 2030, while nanotechnology received some of the US$50 billion allocated to research and development funding in the 2008 stimulus package. Many of these resources have been allocated to the large universities and research centres, but smaller centres have also benefited and it is there that universities and firms are more open to foreign collaboration and to educational opportunities encouraged by local governments.

Within two decades, more than a billion Chinese and 600 million Indians will live in cities, making the quality of urban life a major issue in both countries. Both have ambitious plans to increase energy efficiency, mass transit infrastructure and water treatment and sanitation facilities, although India faces major challenges in these areas, particularly in its burgeoning second- and third-rank cities.

By 2030 as well, China is expected to have 300 million people of retirement age demanding high-end medical and health care services — opening opportunities for foreign partnerships in medical research and medical equipment production.

Another opportunity is afforded by the international expansion of China’s cash-rich enterprises, both state-owned and nonstate. They want access to natural resource assets, new markets, brands and technologies. Despite the high profile of Chinese FDI in the United States, its total is still less than that of South Korea, Brazil or India. That, however, will change. By one informed estimate, if China’s outward investments were to follow a trajectory similar to Japan’s in the 1970s and 1980s, Chinese investors would invest US$1 to $2 trillion abroad in the next decade, with much of it headed for the United States. Canada currently receives 75 percent as much Chinese FDI ($9 billion in 2010) as the United States ($12 billion); were that ratio to continue, hundreds of billions of dollars of Chinese investments could be headed for Canada.

In adapting to this economic gravity shift, Canada has many distinctive competitive advantages. It is the world’s largest producer and exporter of uranium and potash; the second largest producer of nickel, wheat and hydroelectricity; and the third-largest producer of natural gas, diamonds and renewable fresh water (of which it has 7 per-cent of the world’s total). Its cities are attractive and work well — the Economist’s Liveability Index ranks Vancouver, Toronto, and Calgary among the top 10 most livable cities in the world. Canadian-based firms compete globally in construction and infrastructure development; Canadian public pension and social security arrangements are sustainable; and its financial institutions are strong. What it needs is a strategy.

To understand why Canada needs an Asia strategy, we need look no further than Canada’s surprising failure so far to complete a free trade agreement with any Asian country. Talks with South Korea are stalled by auto and beef interests (Canada excepted supply management even before the talks began). Talks with Singapore are stalled by unrealistic demands for concessions equal to those given to the United States. And, as noted, Canada’s policies on supply management and intellectual property are blocking its participation in the Trans-Pacific Partnership (TPP). In each case, short-term domestic political considerations are outweighing the economic calculus of the national interest.

This ad hoc approach is risky and short-sighted. It invites ever-heavier reliance on developing and exporting natural resources and energy to sustain Canadians’ living standards, and, as Asian economies determinedly move up the value chain, Canadian non-resource-based industries will find it increasingly difficult to compete. Canadians need to think again about how to seize the opportunity and strategically re-engage with Asia, starting with determining what we want and how we should achieve it. Instead, Canada sits on the sidelines — a policy taker. To have a voice, Canada has to show up, to become involved in collective approaches to political and economic development that serve its deep interests in open markets.

Within two decades, more than a billion Chinese and 600 million Indians will live in cities, making the quality of urban life a major issue in both countries. Both have ambitious plans to increase energy efficiency, mass transit infrastructure and water treatment and sanitation facilities, although India faces major challenges in these areas, particularly in its burgeoning second- and third-rank cities.

Canada’s strategy toward China should be an integral part of its strategy toward Asia in general — the two should be mutually reinforcing. Canada’s goals in formulating an Asia strategy should be to promote cooperation with the Chinese where feasible and to reassure those who are concerned about an exclusive focus on China. China recognizes the value of multilateralism, not just because it used its accession to the WTO to restructure its economy and enter world markets, but because these institutions provide a way to pursue its objective of restraining US hegemonic behaviour.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

Within this strategic framework, there are at least five criteria to consider in choosing among alternatives and setting policies. It should

- Be generational and serve Canada’s long-term national interests; framed in this way, the strategy should, like deficit and debt reduction, be followed through by successive governments regardless of political stripe;

- Focus on the largest players that will have the greatest effect on our economic future;

- Aim to solve the difficulties Canadian businesses face in the region’s distant and unfamiliar economies through improved market access and greater participation in its production networks;

- Pursue technological collaboration that helps address Canada’s weak productivity performance and builds potential complementarities, recognizing that Asia’s dynamic economies will move up the value chain;

- Be aware of US interests — though Canadians might not realize it, strong moves to diversify the markets for our energy and natural resources will have geopolitical significance.

Here are the elements of the strategy:

Restore Canada’s presence in the region. State and high-level personal relationships are essential to the confidence and trust on which long-term agreements are built. Canada has been slow to seek membership in Asia’s evolving regional architecture. We have been active in the Asia Pacific Economic Cooperation (APEC) forum, but that body no longer drives regional integration. At the apex of the new generation architecture is the East Asian Summit; with the recent addition of Russia and the United States, some are pushing to close its membership, which would leave Canada out. Canada’s minister of defence has participated only once in the nine meetings of the Shangri-La Dialogue, the region’s leading security forum, while US and Chinese officials at the highest levels ensure they have a voice. Canada’s inaction in such matters signals that it is concerned only about bilateral relationships — a serious misreading of Asia’s evolving architecture. It is not yet too late; Canada should apply to join the East Asian Summit and participate in security dialogues and in both the Association of Southeast Asian Nations related activities and their regional and trans-Pacific counterparts. These initiatives are more likely to be successful if Canada identifies and builds relationships with economies — Indonesia and South Korea, for example — whose governments might be willing to serve as entry points to Asian regional institutions.

Develop the Canadian brand. Canada should develop itself as a brand, both at home and in Asia. At home, the proclamation of a Year of Canada and Asia would help build public awareness of the importance of that part of the world for Canada’s economic future. In addition to federal government participation in Asian institutions, governments and other interests within Canada should develop a cooperative Asia strategy. For example, Ottawa should engage provincial premiers in developing an integrated approach to Asia, one that sees them coordinating their Asian travels and aligning their policies in their areas of jurisdiction, including health, education and even FDI. Business groups and trade associations could publicly showcase companies with successful business strategies in the region and work to encourage visits to Canada by Asian tourists. Canadian universities should build on the country’s growing reputation as an education destination — already, international students are estimated to spend more than C$6 billion annually studying in Canada, 40 percent of it by Chinese and South Korean students. Universities and other educational institutions should also cooperate in developing channels through which young Canadians can create businesses in Asia or find employment in enterprises located there.

Some components of a brand are already apparent: Calgary is pursuing a global hub strategy for nonconventional petroleum and alternative energy development, Montreal is an aerospace and pharmaceuticals hub and Toronto aims to become an international financial centre. As some have noted, Canada could become an education hub for Asia, a hub for Asian multinational enterprises in the Americas, a major tourism destination and a supportive jurisdiction for water-intensive industry and green technology.

In adapting to this economic gravity shift, Canada has many distinctive competitive advantages. It is the world’s largest producer and exporter of uranium and potash; the second- largest producer of nickel, wheat and hydroelectricity; and the third-largest producer of natural gas, diamonds and renewable fresh water (of which it has 7 percent of the world’s total).

Ambitious targets are also needed. With export growth rates to major Asian economies ranging from 5 to 24 percent over the 2006 to 2010 period, Canada could aim to double the value of its exports to Asia by 2015. The level of Canada’s outward FDI is more difficult to target since it depends on the strategies companies adopt, but to the extent that inbound FDI is determined by Canada’s regulatory regime, a transparent, best-practice review process should be in place by the end of 2012.

Liberalize trade and investment. Canada should focus on trade deals as the centrepiece of any long-term regional strategy. So far, it has a number of foreign investment promotion and protection agreements (FIPAs) with smaller Asian economies but, until February 2012 when talks with China were completed, none with the giants. Two options, which are not mutually exclusive, should be pursued. Join the TPP. Canada should join the TPP, a proposed regional trade agreement currently being negotiated among Australia, Brunei, Chile, Malaysia, New Zealand, Peru, Singapore, the United States and Vietnam; Japan, Mexico and South Korea may also enter the talks. Joining the TPP would be the most efficient way for Canada to deepen its integration with other Asian economies but only if Canada is prepared to enact reforms in two areas where we are widely seen as being out of step with global standards: our supply-management systems that restrict imports of milk, poultry and eggs, and our relatively lax enforcement of intellectual property rights.

The TPP negotiations could be a game changer, for several reasons. First, the TPP includes Asian economies with which Canada should — but does not — have FTAs. Second, it is a high-quality agreement that includes services and investment, and so offers ways to address NAFTA’s deficiencies in services, regulatory harmonization and investment. Third, the TPP’s broader negotiating framework and multiple negotiating partners increase the opportunities for tradeoffs that are a vital part of any comprehensive agreement. Canada would not be alone in making such trade-offs — other participants, not least the United States, have agricultural issues. Australia and New Zealand successfully rationalized their own supply management programs by abolishing subsidies (in New Zealand nearly 30 years ago) and by buying out farmers (in Australia). Agriculture has been a sensitive issue for Chile as well, but it has agreed to phase out its tariffs by 2017 using safeguards during the transition period. Joining the TPP would send a strong signal of our commitment to Asia. Skeptics who doubt that the United States, in the end, will make concessions in sectors such as agriculture consider Canada’s exclusion from the TPP-9 negotiations a mixed blessing. But what are our options if the United States remains committed and Japan, Mexico and South Korea join the talks?

Create a China road-map. Alternatively, or in conjunction with that approach, Canada could pursue deeper economic ties with China. China has been invited to apply to join the TPP but the bar for admission may be too high. Canada should continue to work on a road-map for deepening the bilateral relationship. Indeed, one of the benefits of a higher Canadian profile in the region would be linkages that help us make our way in China. The end result, though, should be a comprehensive economic agreement between the two countries.

First steps to a deeper relationship have been taken through bilateral agreements in tourism, transportation, financial information, science and technology, marine and fisheries management, and the environment. China’s interests include education, people flows, access to energy and natural resources, and food security, which it is pursuing through enhanced trade and investment. It also seeks recognition of its market economy status earlier than the automatic WTO procedure at the end of 2015. For its part, Canada seeks access to Chinese markets for goods and services. Small and medium-sized Canadian businesses would benefit from access to Chinese global supply chains, and Canada needs Chinese capital to develop its infrastructure and natural resources.

At present trade is largely complementary but Canada buys twice as much manufactured goods from China as China buys in natural resources from us. In the long run the route to greater balance lies in trade diversification, with Canada selling more knowledge-based goods and services that China cannot produce. For this reason, the road-map should address China’s intellectual property protection and government procurement practices, as well as its licensing and ownership restrictions on foreign service providers, instruments China uses to promote its indigenous innovation goals. China has yet to join the WTO government procurement agreement. With the Doha round of multilateral trade talks stalled, Canada should be pushing these issues on a bilateral basis; as a quid pro quo, it could offer early recognition of China as a market economy.

FDI is a prominent bilateral issue even though a FIPA is in the works. China’s recent formalization of regulations for reviewing foreign acquisitions on national security grounds lacks detail on how they will be applied and how they will interact with the established FDI and antitrust review process. On the other side, Chinese and other foreign investors consider Canada’s investment review framework uncertain and lacking in transparency — its net benefit test seems both subjective and unpredictable. Canadians, for their part, are uncertain about the future behaviour of China’s state-owned enterprises, huge oligopolies or monopolies with close ties to government owners and regulators and unfamiliar with international rules of the road and market-based regulatory regimes in host countries. Canadians worry that majority owners make decisions on political, rather than commercial, grounds. To address these worries, a transparent national interest test should apply to both foreign-owned entities and domestic firms under similar circumstances.

Canadians need to understand the motivation and governance of Chinese enterprises that invest in Canada. To that end, trade associations, educational institutions and business partners could contribute by sharing positive experiences. We also need to be realistic in our expectations of China’s opaque and politicized corporate governance practices. We should encourage greater transparency, but we should not expect China to change overnight.

At present trade is largely complementary but Canada buys twice as much manufactured goods from China as China buys in natural resources from us. In the long run the route to greater balance lies in trade diversification with Canada selling more knowledge-based goods and services that China cannot produce.

Enhance the Canadian business presence. Canada is distinctive as a country of small and medium-sized firms: in 2008, between 80 and 90 percent of Canadian companies were that size and they were generating half of Canada’s GDP. These firms are at the forefront of those entering markets in non-OECD countries and account for nearly half the value of Canada’s exports to those countries. Yet what do we know about the most common barriers and constraints they face? For example, is small size a problem for Canada’s successful services firms and goods exporters? This matters, because their potential customers and partners in Asia are likely to be very large enterprises able to take advantage of scale economies far beyond the capabilities of smaller Canadian firms. Asian markets are also distant and unfamiliar, leading to higher transactions costs for smaller firms. We need innovative ways to overcome these barriers: the Canada China Business Council’s creation of an incubator in Shanghai is an innovative step toward networking bases to help smaller Canadian firms connect with suppliers, customers and potential partners in these markets. Canadian governments and trade associations also should cooperate on an action plan and engage in regular consultations on such goals as supporting the greater penetration of Asian markets by small and mediumsized firms. Instructive here might be the experience of such firms in South Korea and India, which are successfully developing their abilities as international niche players.

Strengthen productivity performance: a key to the future. Given the commitment of Asian economies to move up the technology ladder, Canadians can expect that future bilateral economic relationships will become less complementary and more competitive. Our lagging productivity performance relative to our US neighbours — Canada’s business sector output per hour is less than 80 percent that of the United States — gives some indication of the implied challenges. There is no silver bullet with which to improve productivity performance, but measures relevant to an Asia strategy include increasing competition in the domestic Canadian market through greater openness to international markets; increasing competition and cooperation among small and medium-sized enterprises and large firms within national clusters and across borders; enhancing the ability of Canadian financial institutions to support risk-taking; improving the protection of intellectual property; setting national learning goals; and developing imaginative ways to nurture young innovators.

A long-term strategy for deepening Canada’s economic relationship with rising Asia should include ambitious targets that require bold leadership and Canadian partnerships at all levels. It should be multifaceted, with regional, bilateral and Canada-US dimensions. It should include a new commitment to Asia’s evolving and increasingly significant institutional architecture. And it should include preparations at home to meet future Asian competition here as well as abroad. Such a strategy cannot be built overnight, but we must begin: the potential returns to Canadians are high, and so are the costs of an inadequate Canadian response to the evolving multi-polar world.

Photo: Shutterstock