The term Dutch disease refers to the phenomenon whereby a country’s specialization in the exploitation and export of natural resources leads to the appreciation of its currency and the subsequent decline of its manufacturing sector. More specifically, a resource boom, due either to a major discovery or to a significant increase in the price of the resource, results in high demand for the currency of the resource-rich country. As its value appreciates rapidly, local manufacturers find it difficult to compete both domestically and abroad. The main symptom of the Dutch disease is therefore a contraction of the manufacturing output and employment. The phenomenon was first observed in the case of the Netherlands in the 1960s (hence the name Dutch disease) following an important discovery of oil and gas in the North Sea.

Canada is a resource-rich country, and has traditionally been a major producer and exporter of oil, natural gas and a number of minerals. The concurrent resource boom in western Canada followed by the rapid appreciation of the Canadian dollar since 2002 and the subsequent decline in the relative size of the manufacturing sector, mainly located in Ontario and Quebec, re-ignited the debate about whether Canada has contracted the Dutch disease.

Relevant to the debate is the issue of whether recently closed businesses in the Canadian manufacturing sector would have been able to take up the slack caused by an eventual retrenchment in the resource sector or whether competition from China and other emerging nations has definitely rendered such businesses powerless to compete in world markets, even if they were able to benefit from a weaker dollar. In other words, is Canadian manufacturing losing lowvalue-added manufacturing jobs with limited potential to help Canada compete on world markets? Or is the Dutch disease destroying the fabric of an otherwise thriving and dynamic manufacturing sector crushed by a quickly appreciating currency and unfavourable financial conditions?

Arguments about the existence of a classic case of Dutch disease in Canada notwithstanding, it remains that persistently high commodity prices have precipitated a resource boom in western Canada and a strong appreciation of the Canadian dollar. This phenomenon, without a doubt aided by increased competition from China and other emerging countries, is causing Dutch disease-like symptoms in the Canadian economy, where manufacturing is undergoing major structural changes. Whether or not Canada’s experience exactly resembles that of the Netherlands, facts on the ground strongly suggest that Canada might suffer from its own strain of the Dutch disease.

Making the affliction particularly acute is Canada’s unique geography. As the resource boom and the manufacturing bust are occurring in different parts of the country, the concurrent reallocation of resources and jobs from manufacturing to services and resources, which would normally occur in a small country like the Netherlands, largely fails to take place.

Arguments about the existence of a classic case of Dutch disease in Canada notwithstanding, it remains that persistently high commodity prices have precipitated a resource boom in western Canada and a strong appreciation of the Canadian dollar.

Normally, the more serious impacts associated with the Dutch disease would be expected to occur in the future, once the resource boom has run its course. In the short run, there would merely be a substitution of jobs from manufacturing to the booming resources and services sector. It’s only in the longer run that the loss of jobs and lower GDP growth, which would follow an eventual unavoidable retrenchment of the resource boom, would be aggravated as an atrophied manufacturing sector would fail to fill the void left by the weakening resource sector.

In Canada, these long-term effects are a concern. For example, the heavily concentrated resources-based economy of Alberta may disproportionately suffer from an eventual end of the resources boom — and it did, to a certain extent, in 2008 and 2009. Yet, because of the country’s geography, certain regions of Canada suffer the adverse consequences of a resource boom almost immediately, not only once the resource boom has faltered. This is because the loss of jobs in manufacturing and lower economic growth occur in a concentrated fashion in certain regions of the country that are unable to benefit from the boom taking place in a distant region, due to a lack of labour mobility between regions separated by thousands of kilometres and regulatory and cultural barriers. The unfortunate nature of the disease in Canada thus poses particular challenges to both monetary and fiscal policies.

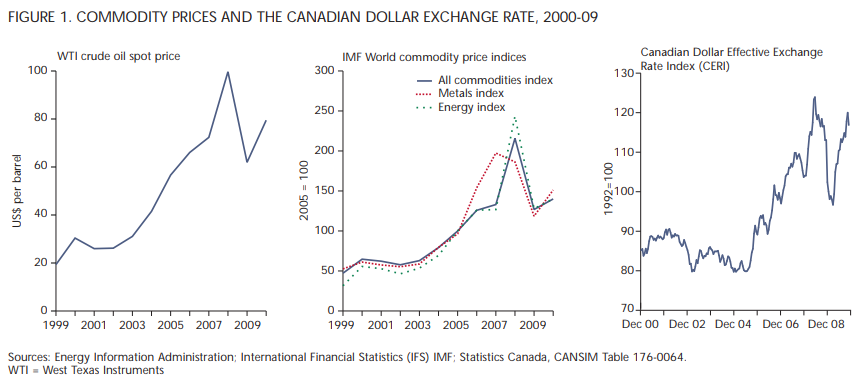

The initial problem with the Dutch disease is that massive exploitation and export of natural resources erodes the competitiveness of the manufacturing sector through the appreciation of the exchange rate. Foreign-exchange earnings of a resource-rich country increase rapidly as a result of rising resource export revenues, leading to the appreciation of its currency. The rapid increase in world commodity prices from 2002 to 2007, and again since 2009, has indeed hastened both a resource boom in Canada and the appreciation of the Canadian dollar, as can be seen in figure 1.

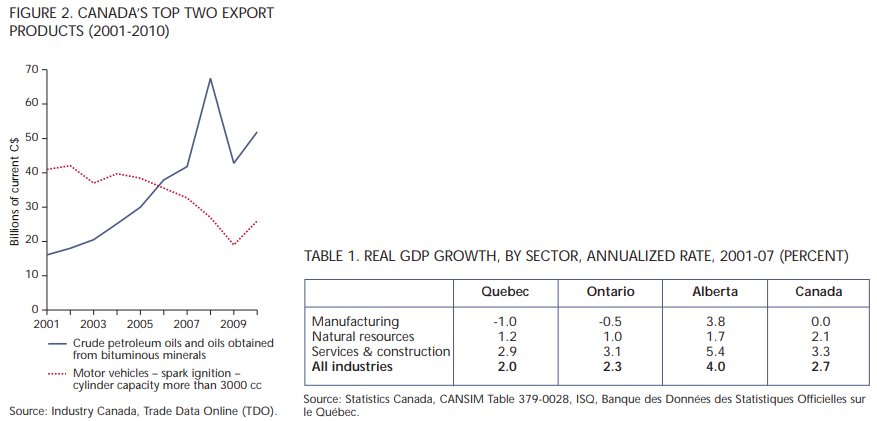

While a strong currency is a challenge to all exports, the rapid increase in natural resource prices gave a competitive advantage to resource exports relative to that of Canada’s manufactured goods. Consider, for instance, Canada’s top two export products, crude petroleum oil and motor vehicles. The price of crude oil rose from US$25.9 per barrel in 2001 to US$72.3 per barrel in 2007; during the same period, the Canadian dollar appreciated from US$0.63 to US$1.03. Although the appreciation of the Canadian dollar diluted the actual oil price upsurge in $C terms, the price still increased from $C43 per barrel to $C70 per barrel. On the other hand, according to data from the International Trade Center, the unit value of Canada’s car exports also rose in US$ terms from US$16,405 in 2001 to US$18,748 in 2007. In Canadian dollars, however, this translates into a substantial decline from $26,039 to $18,201.

It should therefore be no surprise that, over the 2001-2007 period, the value of Canada’s crude oil exports increased from $16 billion to $41.8 billion, whereas revenues from motor vehicles’ exports declined from $41 billion to $32.6 billion. And, accordingly, crude oil replaced motor vehicles as Canada’s top export product in 2006 (see figure 2).

Rising oil prices ensured output and employment growth in the petroleum industry. In contrast, given the rapidly appreciating Canadian dollar, most manufacturing firms have had to improve productivity substantially and reduce production costs in a short time frame to compensate for their loss of competiveness. For many, these efforts were not sufficient to remain competitive, while others did not have the resources to engineer the necessary productivity enhancements.

The effects of higher raw materials prices and of a stronger Canadian dollar on various sectors of the economy are a particular concern for regional wealth distribution. In Canada, 95 percent of oil reserves are located in Alberta, whereas 75 percent of manufacturing output is produced in central Canada (Quebec and Ontario). In 2009, the manufacturing sector represented about 15 percent of total GDP and 84 percent of total exports in central Canada, against 7.8 percent and 28 percent respectively in Alberta. The mining and oil and gas extraction industry, on the other hand, accounted for 19 percent of GDP in Alberta and 67 percent of total exports, but only 0.4 percent and 7 percent of total GDP and exports respectively in central Canada.

With such contrasting realities, when the price of raw materials rises quickly, especially in the case of oil, Alberta experiences a resource boom driving the appreciation of the Canadian dollar, which, in turn, hurts the economies of Quebec and Ontario.

The initial problem with the Dutch disease is that massive exploitation and export of natural resources erodes the competitiveness of the manufacturing sector through the appreciation of the exchange rate.

Between 2001 and 2007, the Canadian dollar appreciated strongly. During this period, manufacturing output fell by 1 percent in Quebec while employment dropped by 2.3 percent (annualized rates). Similarly, in Ontario, manufacturing output fell by 0.5 percent and employment decreased by 2.4 percent over the same period. In contrast, all sectors of the economy experienced growth in output and employment in Alberta (see table 1).

Most economists agree that the 2001-2007 rise in commodity prices, which led to the appreciation of the Canadian dollar, stems from the rapid growth of emerging Asian economies. According to IMF statistics, developing Asian countries grew at annual rates above 6 percent for the past decade.

As a result, fast-growing Asian infrastructure, industries and household consumption help drain energy and natural resources, as data from the US Energy Information Agency suggest. For instance, between 2005 and 2007, China and India accounted for more than 60 percent of the rise in world oil consumption.

Sparked by increasing demand from emerging economies, global demand for raw materials continues to grow rapidly and to push prices upward. Hence, after losing momentum during the 2008-2009 recession, commodity prices and the Canadian dollar have surged again in the recent recovery. The world oil price is holding its ground around $100 per barrel, and at US$1.03 in early May 2011, the value of the Canadian dollar was back to its November 2007 level, which it surpassed at US$1.06 in July. Manufacturing, however, has not fully recovered. In fact, it continues losing ground. Canada’s manufacturing output decreased by 12.6 percent between the second quarter of 2007 (recent peak) and the first quarter of 2011. Despite manufacturing GDP growth since the second half of 2009, albeit at small rates, the sector’s share of total GDP has remained below 13 percent for the past two years. From 2009 to 2010, manufacturing employment decreased by 2.1 percent, even as total employment grew by 1.4 percent. It is therefore increasingly relevant for policy-makers to seriously consider various policy options to address the adverse consequences of the appreciating dollar on Canadian manufacturing. There may be a need to adopt measures aimed at mitigating certain undesirable effects of the disease before it significantly and permanently damages the health of the national economy and strengthens political polarization between regions.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

There are various policy precedents for dealing with the Dutch disease, but Canada’s unique geography and jurisdictional context pose a particular challenge to their implementation. Norway, for instance, uses oil revenues to pay its foreign debt and has established a petroleum fund, which is mainly invested abroad. By investing resource revenues in foreign assets and thereby avoiding huge increases in domestic public spending, Norway is able to reduce the inflow of foreign exchange and curb the appreciation of its currency; it also avoids the state from becoming omnipresent in the domestic economy.

However, in Canada, the possibility of implementing such a policy is limited by the fact that the management of resource revenues falls under provincial jurisdictions. This means that Canada depends on the willingness of the province of Alberta, which manages 95 percent of Canada’s oil, to implement such a policy. However, addressing the appreciation of the Canadian dollar and its consequences on the national economy, particularly in central Canada, is not a priority of Alberta. Moreover, Alberta’s manufacturing industry is heavily tied to the fate and activities of its resource sector.

In other words, the short-term consequences of the Dutch disease are of no immediate concerns to the province of Alberta and its economic development agenda. According to Alberta’s Department of Finance, the province created a resource fund in 1976, the Alberta Heritage Savings Trust Fund, with the goal “to save for the future,…strengthen or diversify the economy, and…improve the quality of life of Albertans.” From 1976 to 1986, up to 30 percent of the province’s oil and gas revenues went to the fund but contributions ceased in 1987. Moreover, currently, the province does not have any policy aimed at redirecting resource revenues toward foreign assets.

Rather, the province has increased its spending on infrastructure and other programs. Such spending has created a boom in the housing and services sectors, putting pressures on consumer prices and wages. This has led to tight labour conditions and high inflation in western Canada, even as unemployment remains high in central provinces. This labour market dichotomy is in part the result of limited East-West labour mobility due both to the distance and incompatible provincial regulations as well as cultural and language barriers, especially in the case of Quebec for the latter.

The resulting inflation asymmetry across the two regions is thus a particular challenge for the conduct of monetary policy.

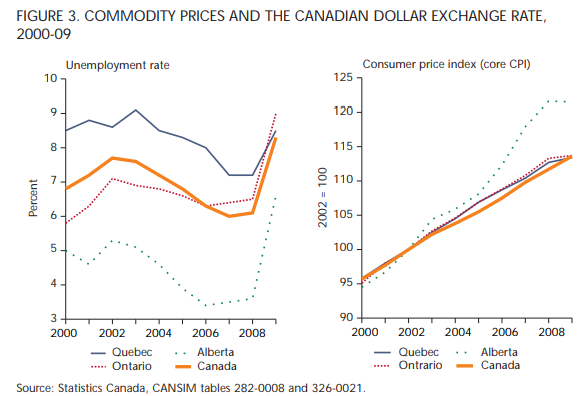

Under its current policy, the Bank of Canada raises or lowers the key overnight interest rate to keep the rate of inflation inside its target range of 1 to 3 percent. By “keeping inflation low, stable and predictable,” the Bank of Canada indicates that it seeks to provide “a climate that is more favourable to sound, sustained economic growth and job creation.” Over the last decade, inflation as measured by total Consumer Price Index (CPI) for Quebec and Ontario has been closer to Canada’s core CPI. Conversely, total inflation has been running high in Alberta (see figure 3). From 2005 to 2008, the average annual unemployment rate remained below 4 percent in Alberta but above 6 percent in Ontario, Quebec and for Canada as a whole. The situation prevails in 2011. From February to April, the unemployment rate in the prairies (Alberta, Saskatchewan and Manitoba) was below 6 percent, but remained above 7.5 percent in Ontario and Quebec.

Given the different inflation levels across the two regions, any change — or no change for that matter — in the Bank of Canada’s overnight rate will tend to benefit one region at the expense of another. In its April 2011 Monetary Policy Summary Report, the Bank recognized “upside risks to inflation in Canada” due to “higher-than-projected commodity prices and global inflation, and increased momentum in Canadian household spending” as well as “downside risks to inflation” relating to “headwinds from the persistent strength in the Canadian dollar and the possibility that growth in household spending could be weaker than projected.” The Bank thus estimated that the risks were balanced over the projection horizon and, therefore, maintained the target for the overnight rate at 1 percent.

This situation maintains favourable credit conditions for central Canada’s manufacturing firms struggling with a strong and appreciating dollar, but it also encourages spending everywhere in the country and thus contributes to increasing inflationary pressures in the booming Albertan economy. Yet, had the Bank of Canada focused on preventing excesses from building in Alberta rather than combating the effects of the Dutch disease in Ontario and Quebec, it would have raised rates.

The more acute challenges posed by the Dutch disease in the Canadian context make it even more important to try to find cures. Possible solutions, however, would likely require the participation of the different levels of governments.

Alberta, for instance, could resume saving resource revenues in its Heritage Fund and in even larger percentages than it did during the 19761987 period. The province could also strive to avoid huge increases in public spending other than those required to accommodate population growth. This would not only reduce inflationary pressures but also allow the province to save for the future. In addition, it would help mitigate the negative effects of the Dutch disease on Canada’s manufacturing sector.

Given the evident decrease in manufacturing employment, one pressing need is to provide new job opportunities for manufacturing workers. The OECD, for instance, in its 2008 Canada Survey recommends harmonization of employment insurance between lowand highunemployment regions and removing barriers to interprovincial trade, “especially those that hinder mutual recognition of professional credentials (notably in the building trades).” Increased East-West labour mobility can reduce unemployment and inflation asymmetry across the two regions and facilitate the conduct of the monetary policy.

As a result, fast-growing Asian infrastructure, industries and household consumption help drain energy and natural resources, as data from the US Energy Information Agency suggest. For instance, between 2005 and 2007, China and India accounted for more than 60 percent of the rise in world oil consumption.

Another way to enhance labour mobility is to provide training to lowskilled workers losing jobs in the manufacturing industry, in order to help them find new jobs in the high-skilled services sector. Alternatively, or in parallel, the development of the resource sector in traditional manufacturing regions can create new, alternative jobs. This would also help diversify Quebec’s and Ontario’s economies and provide these provinces with alternative sources of needed fiscal revenues. With a wider tax base, provincial governments would be able to afford reducing the tax burden of manufacturing firms, helping them to improve their competitiveness on global markets.

As mentioned earlier, the reality that resource booms don’t last forever strongly suggests that it is desirable to try maintaining a competitive manufacturing industry. However, in the particular case of Canada, the pains of a resource boom — that would normally be felt only following the end of the boom — are instead experienced early in other regions of the country as the resource boom is occurring.

To redress the situation, the federal and provincial governments could adopt strong competitiveness measures through more aggressive R&D investment subsidies and tax credits. Such measures would allow manufacturing firms to acquire and develop more efficient production technologies in order to remain competitive amidst conditions of a strong dollar. Government should also encourage organizational innovation that would embolden firms to focus on their core competitive advantages and to abandon unprofitable activities that would otherwise fall prey to lower-cost producers in emerging economies. This may mean that specializing in services to manufacturing industries that are booming in emerging markets may offer an attractive entry point in the global value chain. Moreover, such specialized value-added manufacturing activities usually are less capital-intensive and are often much less vulnerable to competition from emerging nations as they require skilled labour.

In Canada, the growth of such competitive manufacturing activities would not only reduce the East-West economic growth divide and wealth disparities, it would also ensure that, years down the road, when the oil boom is over, Canada remains competitive in sectors that cater to the manufacturing industry.

The opinions expressed here remain solely the athors’ own. They thank Diego Dubé, Jean Laneville and David Luchuk for comments.

Photo: Feng Yu / Shutterstock