Canadians don’t rank pensions very high on their list of today’s public policy priorities, but at the same time they are deeply concerned about the viability of both public and private pensions in the future.

There is a huge demographic divide between older Canadians, who have confidence in the system, and younger Canadians, who don’t. These are the principal findings of the latest Nanos Research poll conducted exclusively for Policy Options.

The poll was conducted by telephone from February 5 to 8, among 1,001 Canadians, with a margin of error of 3.1 percent, 19 times out of 20.

For the moment, Canadians are more concerned about the economy, debt reduction and even tax relief than they are about their public and private pensions. However, the dark cloud on the horizon is their worry whether the money is going to be there when they need it. The anxiety of Canadians on pensions churns below the water line, and it runs deep.

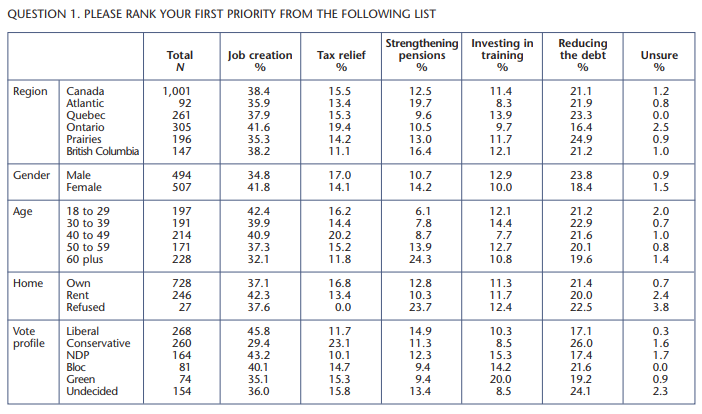

In our poll, 38.4 percent of respondents named job creation as their first priority, 21.1 percent selected debt reduction, 15.5 percent chose tax relief, while only 12.5 percent cited strengthening pensions (table 1).

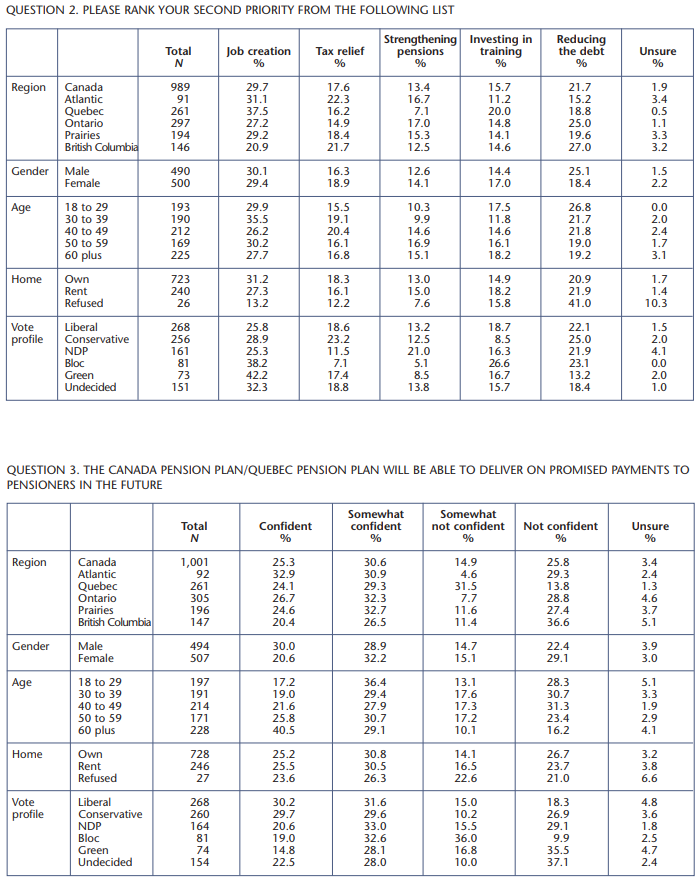

Asked to name their second priority, Canadians again chose job creation, debt reduction, tax relief and pensions in the same order as their first priority (table 2).

When asked about their level of confidence that the Canada-Quebec Pension Plan (CPP/QPP), as well as company pension plans, will be there for them when they need them, Canadians were concerned.

While more than half of Canadians are confident the CPP/QPP will be able to deliver promised payments to pensioners going forward, four Canadians in ten were less confident or not at all confident (table 3).

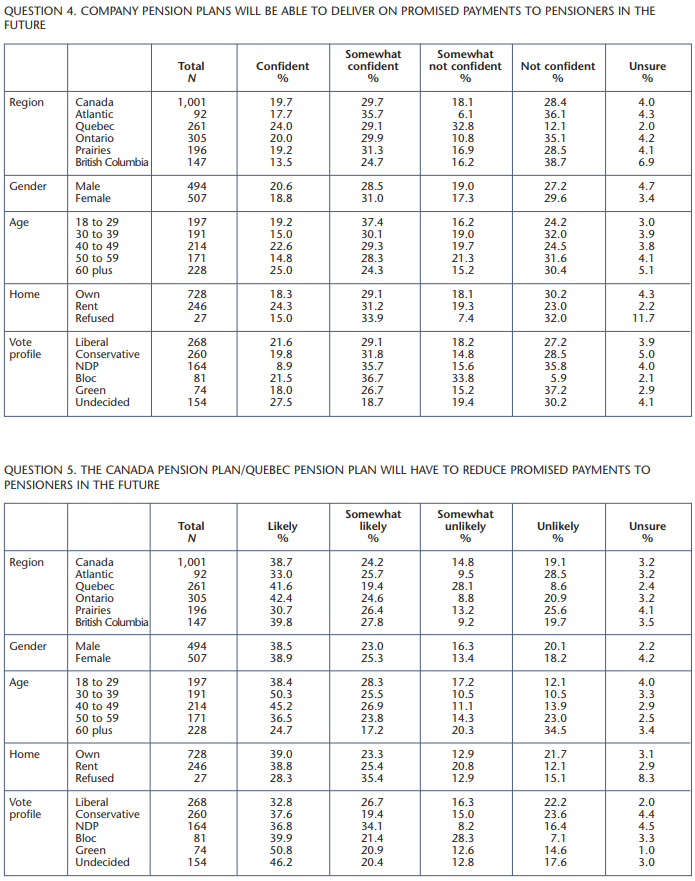

Canadians were nearly evenly divided about the viability of private pension funds delivering for them in the future. Altogether, 49.4 percent are confident or somewhat confident that private pensions will be viable in the future, while 46.5 percent were somewhat not confident or not confident (table 4).

There’s a very high level of concern that both public and private pension plans will have to reduce payments to pensioners in the future in order to remain solvent.

When we asked Canadians whether the CPP/QPP would have to reduce payments in the future, nearly two Canadians in three, 62.9 percent, said this was likely or somewhat likely, against only one Canadian in three, 33.9 percent, who thought this was unlikely or somewhat unlikely (table 5).

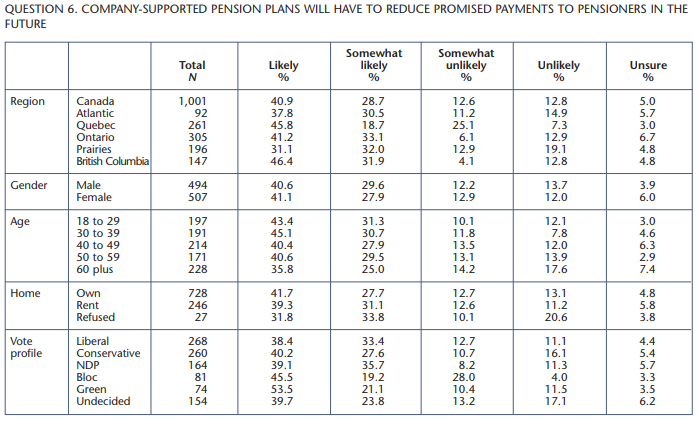

When we asked the same question about private pension plans having to reduce payments to pensioners, the level of those who thought it was likely or somewhat likely rose even higher, to 69.6 percent, while only 25.4 percent thought it was unlikely or somewhat unlikely (table 6).

In other words, seven Canadians out of ten believe the viability of private pension plans is at risk, while only one Canadian in four is confident of their liquidity levels in the future.

In terms of confidence about the liquidity of both public and private pensions, lack of confidence leads confidence by a 2-1 margin. That’s hugely problematic.

When we drilled down in the demographics, we found a striking lack of confidence about the future of pension funds by respondents in the 30-39 and 40-49 age groups. There’s a much higher level of confidence in the 60-plus age group, a demographic segment that is soon to retire or already retired and receiving the CPP/QPP, not to mention those who receive private pensions.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

Seven Canadians out of ten believe the viability of private pension plans is at risk, while only one Canadian in four is confident of their liquidity levels in the future.

For example, only 48.4 percent of Canadians in the 30-39 age group are confident or somewhat confident, while 69.6 percent of Canadians over 60 were confident or somewhat confident, about the CPP/QPP delivering for them.

Asked whether the CPP/QPP would have to reduce payments in the future, 75.8 percent of respondents in the 30-39 age group thought this was likely or somewhat likely, while only 41.9 percent of respondents 60 or over thought so.

Again, asked whether private pensions would have to reduce payouts in the future, the identical numbers of respondents in the 30-39 demographic segment, 75.8 percent thought so, while among the 60-plus group, the number of those who agreed rose to 60.8 percent.

A great demographic divide exists between younger Canadians and those who are nearing retirement or already there. Younger Canadians clearly lack confidence in the viability of public and private pensions in the future, while older Canadians, who are already receiving or about to receive their pensions are much more confident. In a sense, when you say “show me the money,” they are already receiving it, while younger

Canadians strongly doubt they’ll see it.

As the baby boomers, the largest cohort in history, near retirement, they are going to make a huge draw down on the CPP/QPP. They are also going to live longer than previous generations.

Combine an aging population with growing pension demands, and one can see that the viability of public and private pensions is tomorrow’s next big public policy issue. The conversation needs to begin today.

Photo: Shutterstock