“May you live in interesting times” is an ancient Chinese proverb that, depending on your audience, can also serve as curse. While it can and has been described in a multitude of other fashions, all would agree that the fall of 2008 certainly qualified as “interesting times.” While Ottawa coped with the impact of the global economic storm raging at full force, an interesting thing happened. Heightened by the sudden fall in stock prices — and by extension the pension funds, RRSP and other retirement savings dependent on the market — the issue of Canadians’ long-term retirement security moved to the forefront of our agenda.

While the issue had always been a priority since we’d formed government a few years earlier, we redoubled our efforts and started on a path that would lead to major, substantive federal reforms and open an unprecedented dialogue between the federal and provincial governments. Indeed, at the annual federal-provincial-territorial finance ministers’ meeting in late 2008, Finance Minister Jim Flaherty ensured the issue was front and centre — personally arranging to have two of Canada’s most respected authorities in the field, Jack Mintz and Claude Lamoureux, provide an overview on the state of pensions in Canada.

Shortly before that time, I was personally tasked by the finance minister with a key role in advancing the file. We both understood the tremendous emotions surrounding the questions and concerns here. It’s not difficult to understand why. Most pensioners laboured for decades under the belief that their years of loyal service would be recognized in their retirement years by the plan sponsors in the form of their contractual agreement — their pension, their nest egg. That’s why my approach had been shaped by the following frame: how can the federal government best ensure the right public policies exist to be sure pension obligations are fulfilled by plan sponsors to give those Canadians depending on them the peace of mind they have earned?

He gave me this important project out of concern for the long term.

At each stop along the way I quickly noticed a recurring pattern. While I would attempt to underline that we — as the federal government — could study only federally regulated private pensions, the conversations quickly moved into other areas. At each meeting, without fail, once the public microphones were opened to the participants, they made it clear they were looking to have a broader discussion of retirement income security in Canada.

I started my journey to make that happen at the aforementioned finance ministers’ meeting in a chilly Saskatoon in December of 2008. That day I outlined for the country’s finance ministers the federal government’s plan to release a public consultation paper on federally regulated private pensions that coming January. I also announced that we wanted to hear directly from Canadians. We thought this issue was too important to be left to politicians, bureaucrats and special interest groups alone. We wanted to hear as many voices and views from those who would be most affected by any potential changes.

We would go cross-country and hold in-person national consultations and invite any Canadian who was interested to make a written submission, on-line or otherwise. (On a side note, we originally settled on an April 2009 deadline for those written submissions but because of the overwhelming interest, we extended it later into the spring.)

In the spring of 2009 I began my cross-Canada consultations, and when I say cross-country, I mean cross-country — from Halifax to Vancouver to Whitehorse and everywhere else in between. What’s more, despite the challenging timelines and logistical challenges, we never once left anyone at a microphone who wanted to speak. Every single Canadian who wanted to have a voice on this very important file was offered an opportunity.

But at each stop along the way I quickly noticed a recurring pattern. While I would attempt to underline that we — as the federal government — could study only federally regulated private pensions, the conversations quickly moved into other areas. At each meeting, without fail, once the public microphones were opened to the participants, they made it clear they were looking to have a broader discussion of retirement income security in Canada.

In the field of public policy decisions there are certain groups that are extremely well organized and have the ability to get the attention of decision-makers. In this case groups such as the Canadian Labour Congress, Canadian Association of Retired People, the Canadian Bankers Association, “the Group of Seven” (seven of the larger federally regulated private pension sponsors in Canada), as well as life insurance groups, provincial and territorial partners and a host of others provided valuable input.

I found myself somewhat more intrigued by the unorganized and more spontaneous representations that I have witnessed over the course of my study. Often these would be personal, raw and unique stories of a special circumstance. These were our neighbours, our mothers, our brothers or friends. It wasn’t only at the microphone at an official meeting I heard them though, but also at an airport, in a cab or at a local Tim Hortons. This focused my efforts and determination that whatever policy decisions were to be taken in the future, the government owed it to Canadians to make sure that we would get it right. There aren’t any “do-overs” on this file. It’s just too important. Canadians deserve a dignified retirement.

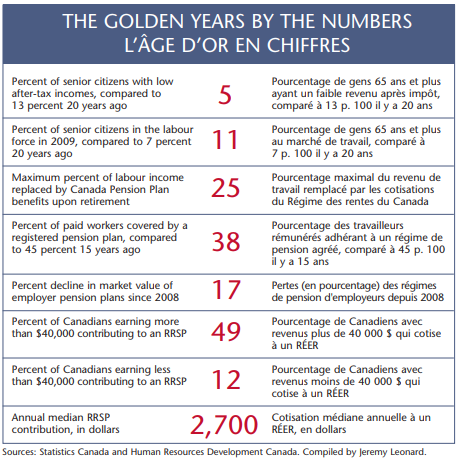

Reflecting back on this period, I have to note that an important part of this story has been largely overlooked. I am referring to Jim Flaherty, who worked tirelessly with Air Canada and its employees and retirees to help them make it through a very difficult time. We tend to hear of instances in which a company that is not federally regulated has failed or is failing, and the pensioners find themselves in an unpleasant situation. Respecting jurisdiction (only 7 percent of all private pension plans are federally regulated), Air Canada was an example of what can be accomplished when all parties involved decide to do the hard work to get it right instead of getting it over with.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

Respecting jurisdiction (only 7 percent of all private pension plans are federally regulated), Air Canada was an example of what can be accomplished when all parties involved decide to do the hard work to get it right instead of getting it over with.

In a similar vein, following the aforementioned consultations we held, the federal government announced significant reforms to federally regulated pensions that I humbly suggest got it right (see the document at www.fin.gc.ca/n08/09103-eng.asp). Among the changes, and one I’m personally proud of, is the requirement for plan sponsors who voluntarily wind up a pension plan to fund 100 percent of their contractual commitments to their plan members. As I travelled around the country, I heard troubling stories of various plan sponsors that had made the decision to stop offering a defined benefit plan to its employees, and instances in which the retirees did not receive 100 percent of what they had been promised because the Act did not require it. After I shared this with the Finance Minister, he agreed we owed it to protect Canadians from this.

As I indicated earlier, it was abundantly clear from talking to Canadians that they wanted a broader discussion of retirement income in our country. Shortly after talking to Minister Flaherty, we made that happen. That May, finance ministers from across Canada agreed to jointly study the adequacy of Canadians’ retirement income. This led to the creation of the Research Working Group on the

Retirement Income Adequacy of Canadians, consisting of political leadership, government officials and experts, which would (and did) report findings back before the end of the year at a federal-provincial-territorial “pension summit.”

At the December 2009 pension summit, finance ministers discussed the Working Group’s important findings and agreed to move forward on an examination of policy options to address issues identified in that indepth research. Again we’ll strive to hear from as many Canadians as possible on the opinions available, as we consider how best to put into action specific pan-Canadian solutions that benefit all current and future retirees.

I don’t think it would be possible for a person to be a part of this type of consultation process without being very affected by the comments and observations that were made by individual Canadians. From time to time at these meetings participants would lash out in anger either at the federal government, or at me personally based on the false assumption that I have a “gold-plated pension.” (For the record, I currently do not qualify for a pension — because I spent most of my adult working life as a self-employed farmer and I have not been around Ottawa long enough in Parliament to qualify for an MP’s pension.) Nevertheless, it easy to understand the anger and fear of many — and also the vague demands for government action in a multitude of forms. Of course a great many Canadians were also quite gracious and expressed to me their appreciation that the federal government was taking such a proactive role on the file and listening to their thoughts and concerns.

However, it must be remembered pensions are legally binding contractual agreements entered into between private entities — so we must tread carefully before we decide on how the federal government should be involved and the long-term implications of the involvement.

I firmly believe that there is a very important role for governments to play in the regulation of pensions, and that we need to assist Canadians to prepare for their retirement years, but that there is an important discussion that needs to take place about around what exactly as Canadians we expect of ourselves in providing for our own individual retirement. What’s my individual responsibility to prepare for my retirement years?

Aside from the simplifications and sweeping generalizations of a few select special interest groups, there seems to be general agreement on the extreme level of complexity of this issue. At times, I am very envious of those who at this point are absolutely sure they alone know the best course of action on this file. I am also thankful they are not in government, because I fear this would result in policy direction that would be dangerous for Canadians over the long term.

Whatever role I am asked to play in the future, I will take it on to the absolute best of my ability and am thankful for the opportunity to be part of this debate.

Photo: Shutterstock