To stifle financial speculation and ban the shenanigans that brought on the devastating stock market crash of 1929, the US Congress enacted a series of measures to save a moribund capitalist system. The Glass-Steagall Act of 1934, in barely 53 pages, mandated a new regulatory framework for banks and other financial institutions in the United States.

In stark contrast, under intense popular pressure countervailed by equally intense and effective lobbying, the US Congress finally adopted in July 2010 the Dodd-Frank Act as a putative response to the financial collapse the world experienced in the fall of 2008. In its draft form, the Act ran to some 2,315 pages; in its final official version (in eight-point type), the Dodd-Frank Act takes 848 pages to mandate a new set of rules for the US financial system!

A 53-page Act in 1934 versus an 848-page one in 2010 is a good indicator of the intricacy and complexity of financial markets in our time. But the Dodd-Frank Act is only the tip of a new US regulatory iceberg. The Dodd-Frank Act heaps upon US regulatory agencies dozens of unresolved issues with instructions for them to bring forth policies and rules to cope with these issues at a specified later date. In this manner, the US regulation of the financial system is at best a work in progress with an uncertain final shape.

The Financial Stability Board (FSB), an offshoot of the G20 that was set up to give substance to financial reform and coordinate and monitor its implementation, has issued its own voluminous documentation and multiple recommendations. Indeed, all G20 nations are committed to implementing, in a coordinated manner between now and the end of 2012, regulatory or supervisory frameworks along the lines of the FSB recommendations.

The Bank for International Settlements (BIS) and its Basel III Committee for Bank Supervision have also proposed an elaborate set of measures to strengthen the international banking system and improve its resilience and resistance to violent financial storms. The FSB and the BIS have a close working relationship. The European Union (EU) Commission has also produced an abundance of policy papers and proposals on these issues, which, in several instances, go beyond the recommendations of the FSB. The financial crisis, it seems, provided the EU Commission with an opportunity to take on new powers and to assert its authority over national regulatory bodies. The International Organization of Securities Commissions (IOSCO) has also issued a number of policy papers on key aspects of the financial system.

Although sound policies and some measure of luck Canada have shielded from the financial debacle of 2007-08, it is a member of the G20, an active participant on the FSB and a member of the Basel III Committee. As such, Canada must implement in some fashion the policy recommendations and regulations coming out of these bodies.

Of course, Canadian banks, along with all banks in developed economies, will have to abide by the Basel III Committee stipulations, under the watchful supervision of the Office of the Superintendent of Financial Institutions (OSFI).

My objective in this article is to provide an overview of what these long and complex policy documents aim to achieve, and to assess the adequacy of this regulatory response to the systemic crisis of 2007-08.

Of course, any proposed cure will derive from what are believed to be the causes of the financial system blowout in 2007-08. There is now a broad consensus on the immediate causes of that crisis but considerable divergence of opinion about the importance of each of these ”causes,” about the prime movers (what came first?) and thus about the appropriate policy response.

Here are the immediate causes, in a somewhat random order:

First, monetary policies driving down interest rates made private borrowing very attractive; made leverage of all sorts, including of bank balance sheets, very profitable; and made institutional investors very eager for alternative highly rated, interest-bearing investments with higher yields than government securities.

Second, inadequate regulation and supervision of the international banking system incited (some) banks to circumvent capital-adequacy rules and allowed bank behaviour that exacerbated the growing bubbles in the financial system when it should have dampened them.

Third, there was an implicit assumption that several key financial players had become too big and too critical to the system for governments to let them fail and go bankrupt; this observation usually comes under the heading ”moral hazard,” meaning that the assurance of a bailout induces the leadership of these organizations as well as their shareholders and other stakeholders to make or abet hazardous decisions and actions.

Fourth, there was the unregulated growth of a parallel (or ”shadow”) banking system made up of nonbank entities originating loans, bundling them and selling them; the business model of these entities required a continuous growth in the volume of loans originated.

Fifth, lax securitization rules allowed investment banks and ”shadow” banks to bundle increasingly risky loans and debts to be sold to investors worldwide; through this process of securitization, loan originators are disconnected from the risk of default, which is borne by the ultimate ”lenders” (actually institutional investors); this alchemy was bound to lead to lower credit standards and weak monitoring of borrowers.

Sixth, the reassuring ratings given to these securitized bundles of loans by rating agencies lured institutional investors into massive purchases of these financial products.

Seventh, contrary to a widely held belief, the unregulated growth of complex derivative products like credit default swaps added risk and interconnectedness to the financial system in ways that were poorly understood at the time.

Eighth, ”mark-to-market” (or fair value) accounting had dire consequences for the balance sheets of financial institutions in a time of stress, uncertainty and vanished liquidity. These accounting rules imposed on financial institutions a requirement to mark (up or down) the value of any financial instrument to reflect their latest ”market” value; if such value was not readily available, the entity was to value the financial instrument on the basis of an explicit financial model. These rules compounded the simmering problems when the market froze for some types of investments and the ”fair” value of these instruments nose-dived, creating huge accounting losses. In addition, large swings in the mark-to-market value of derivative products led to urgent calls for large amounts of collateral from counterparties at the worst possible time.

Ninth, accelerating and amplifying the brewing fiasco were the unregulated actions of hedge funds and other speculators; and large investment banks will behaving as traders and speculators. There was the massive, often ”naked” short-selling of shares of financial companies during the turbulent fall of 2008. Speculation, through credit default swaps, against packages of subprime mortgage loans, also amplified the brewing fiasco.

Tenth, grossly inadequate risk measurement models, anchored in recent past experience, failed to spot the looming crisis; in fact, these models actually provided false assurances to decision-makers.

Finally, the form and level of compensation in the financial sector promoted unbridled risk-taking and grossly overrewarded short-term performance; this ”cause” is the easiest to understand and the most politically explosive. It has been the object of a considerable public relations effort on the part of governments and their agencies.

Each of these specific ”causes” has received some attention from one or another regulatory body. Let’s briefly review the actions taken or contemplated by governments, agencies or regulators to deal with these immediate causes of the 2007-08 version of a financial crisis.

Low-interest-rate monetary policies. These remain a fact of economic life. So all efforts, as we shall see further on, aim at dealing in some partial way with the consequences by monitoring household borrowing; restraint leverage of financial institutions; and improving oversight of alternative investment funds.

International banking regulation and supervision. This issue falls squarely within the jurisdiction of the Basel III Committee for Bank Supervision and the BIS. The Basel III framework governs the level of capital that banks must maintain to ensure the safety of their liabilities (depositors). The previous accord, termed Basel II, had introduced the notion of self-assessed, risk-weighted capital adequacy. Banks were to compute their required level of capital (of various tiers) on the basis of the riskiness of their assets (loans, trading positions, etc.). Clearly, it was assumed, a borrower with a credit rating of, say, AAA represents very little risk of default, as compared to a borrower with a credit rating of, say, BBB. Therefore, bank loans extended to highly rated borrowers required little or no capital reserves.

Of course, banks are listed on stock exchanges and are valued according to their return on capital. The lower the amount of capital required for a given level of operations and profits, the higher the value placed on the bank.

When loans can be packaged and sold off to other investors, the bank doing so generates fee income with no capital requirement; when loans can be transferred to off-balance sheet entities (often with a guarantee from the bank), income is generated without capital requirement; when rating agencies give their highest ratings to securitized packages of low-quality loans, these ”assets” require very little capital, yet generate more income than government securities with equivalent ratings; when lenders can buy an ”insurance” against default of their debtor (called a credit default swap) and if the seller of that ”insurance” is highly rated and its fees for doing so modest, then the bank can transform a loan with a middling credit rating (thus requiring a substantial level of capital) into a highly rated loan requiring little or no capital, and so on. These operations resulted in actual leverage ratios that were much higher than what was shown on bank balance sheets, and in high levels of hidden risks.

After much discussion and debate with the banks, a new framework, Basel III, was proposed and has now been approved by the G20 leaders at their November 2010 meeting in Seoul. The Basel III framework ”[raises] the quality, quantity and international consistency of bank capital and liquidity, constrains the build-up of leverage and maturity mismatches, and introduces capital buffers above the minimum requirements that can be drawn upon in bad times.”

In clear terms, banks will have to raise their level of equity capital and other forms of capital; they will have to arrange for a ”conservation buffer” of capital on which they can draw in difficult economic circumstances; as well they must be prepared for national regulators to impose a ”countercyclical buffer” when their economy moves up on the cycle. Banks that do not meet fully these capital buffers will face restrictions on the payment of dividends and bonuses.

Banks were not too happy with this new framework; they claimed that it would curtail their ability to lend to businesses and reduce their profitability. They have lost this battle, but they gained a generous implementation schedule; they will have to comply with the new capital requirements and capital buffers only over a period that stretches out in some cases to 2019!

The ”too big to fail” syndrome. A G20 press release of November 2010 said, ”The G20 Leaders at the Seoul Summit on 11-12 November endorsed the Basel III framework and the Financial Stability Board’s (FSB) policy framework for reducing the moral hazard of systemically important financial institutions (SIFIs), including the work processes and timelines set out in the report submitted to the Summit.”

The G20 approved the work plan proposed by the Basel III Committee and the FSB to cope with the ”too big to fail” institutions, now labelled ”systemically important financial institutions” (SIFIs). The FSB and the BIS will come up with a list of global SIFIs by mid-2011 and, by the end of 2011, with measures to address the issues they raise for the international financial system. It is most likely that, at the very least, additional capital (or, in FSB/BIS terminology, ”loss absorbency”) requirements will be imposed on these global SIFIs.

The determination of which financial institutions will be declared SIFIs is the object of fierce negotiations, as the consequences will be huge for any financial institution so labelled. It is argued that the criterion should not be ”bigness” but ”interconnectedness.”

The unregulated growth of a parallel (or shadow) banking system made up of nonbank entities. What about financial players that could cause significant harm to the international financial system but are not ”banks” and, therefore, not subjected to the Basel III strictures?

Shadow banks, hedge funds and other speculative and alternative investment funds played a significant role in bringing down the international financial system. Should they be included in a list of potential SIFIs? What regulation or supervision would be applied to these nonbank financial institutions?

Already, the FSB proposal to include insurance companies within the range of SIFIs has generated controversy and a good deal of pushback by the insurers. The FSB and the European Union are moving carefully here, because they are uncertain as to how to proceed.

The US approach to the issue of SIFIs was to create a new body and dump the problem on it. The Dodd-Frank Act creates a new organism, the Financial Stability Oversight Council (FSOC), which has considerable powers in certain areas.

The FSOC has the authority to respond to emerging threats to the stability of the financial system, no matter which institutions are deemed responsible for this threat. Section 113 of the Dodd-Frank Act even empowers the FSOC to assert its authority over a foreign nonbank entity if it determines ”that material financial distress at the foreign nonbank financial company, or the nature, scope, size, scale, concentration, interconnectedness, or mix of [its] activities could pose a threat to the financial stability of the United States.”

Thus the FSOC’s authority may extend over speculative or hedge funds, private equity funds and other alternative investment funds, wherever they are domiciled, if the council believes that they are a source of risk to the American financial system. But it is left to this new organization to decide exactly how these objectives will be achieved.

So when it comes to dealing with threats to the financial system from nonbank financial institutions, the design of appropriate regulations and supervision is at best a work in progress.

Lax securitization rules. The global conflagration sparked by subprime mortgage loans stemmed from the process of ”securitization.” Mortgages that had weak credit profiles when taken individually were assembled into a portfolio and divided into distinct tranches with different yields and credit ratings.

Although they were based on loans with low credit ratings, several tranches, known generically as ”collateralized debt obligations”(CDOs), received high ratings from credit rating agencies, with most of the default risk presumably left in the lower-rated (or nonrated) tranches.

Institutional investors (pension funds, insurance companies, foundations), which are not allowed to invest in securities that have not received an ”investment grade” rating from recognized credit rating agencies, were attracted to these CDOs, which bore a yield slightly higher than other securities with the same credit rating. That is how and why subprime mortgages (in the form of CDOs) ended up in institutional fund portfolios all over the world.

There was much money to be made by loan originators (the infamous Countrywide Financial, Washington Mutual, New Century, Wells Fargo, etc.) and by investment banks packaging the loans and selling the tranches to investors (Goldman Sachs, Morgan Stanley, Lehman Brothers, Merrill Lynch, etc.).

There was a pernicious feature of this business model for stock-exchange-traded companies: to increase earnings (and earnings per share) as is expected and demanded by the financial markets, a firm must continually originate more loans this quarter than last quarter, more this year than last year. To feed this infernal machine, credit standards must be lowered even further, tricks must be found to lure borrowers with low early payments, promotion must be intense. As these loan originators took no responsibility for monitoring the loans and ensuring that payments were made and as they retained none of the default risk, there were no impediments to their originating activities.

The Dodd-Frank Act proposes to reduce the risks associated with securitized products by means of the following measures:

- Loan originators and those who transform them into securitized products will be required to retain at least 5 percent of the default risk. Furthermore, these entities are not allowed to use derivatives to sidestep this risk.

- The sharing of this default risk between originators and securitizers will be established by the regulatory agencies based on their judgment as to the quality of the loans submitted for securitization.

- Regulation of the credit rating agencies (which we deal with later), seen by many as the primary culprits for this fiasco, should provide a first line of defence against abuses of the securitization process.

In jurisdictions that did not participate directly in the subprime folly, the issue of securitization is dealt with gingerly, there are concerns that the very real benefits derived from proper securitization may be lost in the process of regulating the practice. Indeed, since the 2008 financial crisis, the securitization market has all but dried up.

The overly reassuring ratings given by credit rating agencies. Credit rating agencies were the butt of severe criticisms for their role in the years and months prior to the 2007-08 financial crisis. The whole credit rating process is rife with conflicts of interest:

- Credit rating agencies are paid by the issuers, by those asking for their securities to be rated. Revenues hinge on satisfied customers, particularly when a client may ”shop” for the agency that will provide the best credit rating.

- Institutional investors are often precluded from investing in securities that did not receive an ”investment grade” rating by a recognized rating agency (officially referred to as nationally recognized statistical rating organizations. This regulatory arrangement gives credit-rating agencies a formidable influence in financial markets).

- Credit rating agencies, while they have experience and are doing a fairly good job rating corporate or government debt, ventured into the unknown but very lucrative business of rating highly complex products (such as synthetic CDOs). Not surprisingly, without the required expertise to assess fully these new ”products,” rating agencies relied on their designers, usually in the employ of investment banks, to arrive at a rating process.

- The credit rating agencies, looking for new sources of income, began offering consulting services to issuers, creating a clear risk of conflict of interest: here’s a rating agency giving consulting advice on how to design a ”product” to receive an appropriate rating, and then the same agency rates this ”product.” Of course, as always, it was claimed that a Chinese wall separated the two parts of the organization!

- Recruitment of ratings agency employees by issuers, and especially by investment banks, raised another possible conflict of interest.

The Dodd-Frank Act directly tackles some of these issues and calls for additional studies on others. Generally, the Act mandates fuller disclosure and closer supervision of nationally recognized statistical rating organizations. For instance, the rating agencies will in future have to disclose the models and methodologies they use to arrive at their ratings. They will have to ”look back” at ratings given to an issuer over the last year when an employee of the rating agency takes up employment at this issuer or at any intermediary involved in the rating process. The Act also imposes governance rules and specific responsibilities on board members of rating agencies.

The Act calls for several studies to be completed in a stated time frame. Only when these studies are completed and new measures, if any, adopted, shall we know how credit agencies will actually be regulated in the future.

Although still engaged in a process of consultation, the European and Canadian authorities seem to favour a combination of enhanced supervision, fuller disclosure and the commitment by rating agencies to new governance and ethics rules. Whether that will prove sufficient is an open question.

The unregulated growth of complex derivative products. Derivative products serve either of two ends: they are part and parcel of a risk-mitigating strategy for investors and corporations, or they are a tool for effective speculation.

Some derivative products, such as puts and calls on company shares, are traded on an exchange (the Montreal Exchange, for instance). Then, all transactions may be monitored by securities commissions; the prices of the derivatives and their volume are public information; the sellers and buyers are all known to the exchange, which imposes rules governing risks and exposures. Transactions are settled through a clearing house; sellers and buyers never have direct contact.

But the largest part of the derivative market is made up of over-the-counter (OTC) derivatives, meaning sellers and buyers negotiate directly the terms of each derivative contract. These terms may be standard or tailored to the very specific needs of the parties. These derivatives include interest rate swaps, foreign exchanges, commodities, the infamous credit default swaps and so on. If one wants to speculate on the price of oil or gold, on the value of the euro, on the possible credit default of a country or corporation, OTC derivatives are the tool.

Though formally unregulated, many derivative transactions are governed by the terms of the International Swaps and Derivatives Association (ISDA). Contracts governed by ISDA rules tend to take a standardized form and specify when and what collateral will have to be transferred from one party to the other.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

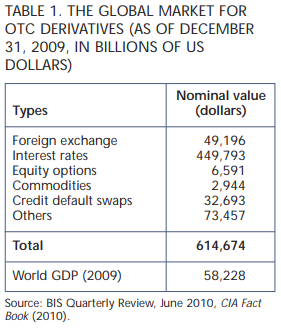

The notional amount of OTC derivatives outstanding on December 31, 2009, amounted to more than $600 trillion (table 1), dwarfing the $53 trillion in exchange-listed derivatives. This derivative market is global in scale and involves all sorts of buyers and sellers with all kinds of motivations.

A good indicator of the speculative nature of these OTC derivatives is their volume of growth over the last 10 years, during which time they went from less than $100 trillion to over $600 trillion.

What is needed is real-time transparency on which parties are doing what in this market. The key proposal, in the United States, Canada and Europe, is to standardize most OTC derivatives and move their trading to exchanges; have them settled through central counterparties and reported to trade repositories; limit or forbid some OTC transactions; and raise capital requirements for nonstandard derivatives.

Implementing these measures will give regulators better and timelier information on this market. To have access to exchanges or centralized counterparties, these derivatives will need to be standardized as to their terms and conditions.

The clearing houses, having become counterparties, will want to assess the risk worthiness of the parties to derivative transactions. But the tasks assigned to the regulatory agencies and those future clearing houses are gigantic.

Not all OTC derivatives that are currently traded will conform to the conditions imposed by a typical clearing house. Centralized counterparties may refuse to handle certain types of derivative transactions that are currently negotiated on the OTC market. What will happen if that occurs? Would these transactions be banned or, as seems to be proposed, subjected to increased capital requirement? How would this requirement be determined? If a large volume of OTC derivatives continues to be traded, does that not defeat the whole purpose of the regulation?

The Dodd-Frank Act gives the agencies concerned (the Securities and Exchange Commission and the Commodity Futures Trading Commission) the authority to exempt certain types of derivative products from the obligation to be traded with a centralized counterparty (the transaction must, however, be registered with a centralized trade repository). These agencies are also authorized to forbid OTC trading of specific derivative products. However, this part of the US law is convoluted enough to create new business opportunities. It calls again for several studies and leaves a number of issues unsettled.

The European approach and the Canadian one are based on displacing most OTC derivatives to centralized counterparties. Nonstandard derivatives that cannot be cleared through centralized counterparties would nevertheless be recorded in a central registry so that the authorities are informed of the amounts outstanding and the identity of the counterparties. Derivatives not traded through a centralized counterparty would be subject to ”more stringent safeguards and capital requirements.”

These are not easy matters. In fact, a variety of consultations are being held to come up with solutions to the problems related to regulation in this area. Given the global nature of this market and the fact that the US and the UK represent the lion’s share of derivative trading, where would these centralized platforms be installed? Do small overall players in these markets, countries such as Canada, merely let their financial institutions trade on some international exchange located elsewhere? Should there be a series of national platforms linked to large global platforms in the US and UK?

According to the Bank of Canada’s December 2010 Financial System Review, three Canadian options are currently being discussed under the bank’s leadership:

- expanding global centralized counterparty (CCP) offerings to include a broader range of Canadian dollar products;

- establishing a stand-alone Canadian CCP with links to regional or global CCP(s); and

- establishing a Canadian CCP that would be an affiliate of an established global CCP.

The stakes are considerable for Canada’s place as a major financial centre.

Curiously, despite the credit default swaps were OTC derivatives directly implicated in the 2008 financial catastrophe, provoking the discomfiture of American International Group (AIG) among other havoc, the regulators are intent on bringing all OTC derivatives under new scrutiny and regulations.

Ironically, the Dodd-Frank Act even stipulates that credit default swaps may not be regarded as insurance, and thus should not be subject to regulation as insurance products. (In the US, states regulate insurance contracts.)

The consequences of ”mark-to-market” (or fair value) accounting for the balance sheets of financial institutions in a time of stress. This issue is the subject of heated debate within and around the accounting profession. Accountants are fairly enamoured of the fair value accounting principles and usually resist the notion that accounting of this sort may have contributed to the financial crisis.

Academic studies often have been less positive and sometimes have been downright harsh in their conclusions about this accounting principle. For instance, as Richard A. Epstein and M. Todd Henderson write:

[Mark-to-market accounting] creates asset bubbles and exacerbates their negative collateral consequences once they burst. It does the former by allowing banks to adopt generous valuations in upmarkets that increase their lending capacity. It does the latter by forcing the hand of counterparties to demand collateral even when watchful waiting and inaction is the more efficient course of action when the downward cascades generated by mark-to-market accounting may trigger massive sell-offs at prices below true asset value.

On the other hand, the American Securities and Exchange Commission (SEC) reported in December 2008 that fair value accounting did not appear to play a meaningful role in the bank failures that occurred in 2008.

Much work is being carried out to harmonize the International Financial Reporting Standards (IFRS) developed by the International Accounting Standards Board (IASB) with the US Generally Accepted Accounting Principles (US GAAP) developed by the Financial Accounting Standards Board (FASB). The IFRS is scheduled for implementation during 2011 and it is hoped that the US GAAP will be highly convergent with the IFRS.

Since the latest financial storm started in the US and raged there with particular force, the FASB has shown some flexibility in the application of the ”mark-to-market” principle. The IFRS was also adjusted to maintain convergence with the American accounting principles.

Both IFRS and US GAAP now include the possibility of classifying financial instruments as ”held to maturity”; these financial instruments are then excluded from strict mark-tomarket rules of evaluation. Financial institutions may thus avoid the full negative impact on their balance sheets of a disrupted ”inactive” market.

The unregulated actions of hedge funds and other speculators as well as large investment banks behaving as traders and speculators. Hedge funds (or more precisely speculative funds) played an important role before and during the financial crisis, certainly in the US market where, in contrast to the UK, hedge funds do not have to register and report to the regulatory agencies. The key problem was that no one knew exactly what these funds were doing and what risks they loaded onto the financial system.

Hank Paulson, ex-CEO of Goldman Sachs, and US secretary of the treasury during the crisis, writes in his memoirs, ”I called [SEC chairman] Chris Cox to discuss market manipulation. The investment bank’s falling stock price and widening CDS appeared to be driven by hedge funds and speculators. I wanted the SEC to investigate what looked to me to be predatory, collusive behavior as our banks were being attacked one by one.”

The Dodd-Frank Act mandates, at last, registration of these funds with the SEC. Regulatory agencies will conduct periodic examinations of their books and operations. The Act applies to all alternative investment funds so that no one may escape these provisions by a change of name and designation. Of course, as pointed out earlier, the FSOC now has the authority to declare that an alternative investment fund may threaten the stability of the American financial system and to take whatever measures it deems necessary to bring order and stability to the system.

As for investment banks (Goldman Sachs, Morgan Stanley, JP MorganChase, etc.) behaving as traders and speculators, Paul Volcker, a past chairman of the US Federal Reserve, proposed that investment banks and commercial banks be prohibited from trading for their own accounts and not be allowed to own hedge funds or private equity funds.

The Dodd-Frank Act does incorporate what became known as the ”Volcker Rule,” but it nevertheless permits investments that were qualified as de minimis in these types of funds. Banking establishments are barred from holding more than 3 percent of a hedge fund or private equity fund. In addition, their total holdings in such funds should not exceed 3 percent of the bank’s tier one capital.

Consultations are currently under way on the implementation of these rules. Opposition to parts of these new rules is vocal, well organized and well financed. A considerable watering down of these provisions may well occur during the regulation-writing phase.

Grossly inadequate risk measurement models. Most risk assessment models are based on the volatility or variance observed over a preceding period of time, rarely exceeding five or ten years. Thus, the very low volatility observed between 2003 and 2006 fed into typical risk models, resulted in low capital requirements and low levels of calculated risk in investment portfolios, made a high level of financial leverage seem riskless, pushed down the price of derivatives and so on. After a prolonged period of low volatility, risk-assessment models will be very permissive of leverage and risk taking of all sorts.

No specific regulations are proposed here, but there is a strong recommendation to submit the results of risk models to stringent ”stress testing”; that is, to subject the results to alternative hypotheses about the future covering a wide range of possibilities. The emphasis and the burden have been placed on boards of directors and risk management committees of the board.

The form and level of compensation in the financial sector. Avarice and warped incentives have fuelled bubbles and financial fiascos throughout history. As Machiavelli wrote centuries ago, the insatiable quest for profit is indeed a constant of history, but over the past 20 years, it has taken on the dimension of a moral crisis.

All stakeholders (commercial banks, investment banks, pension and mutual fund managers, hedge funds, etc.), even guardians and sentinels (i.e., credit rating agencies, financial analysts), were motivated by financial incentives that were closely aligned and driving behave in the same direction.

A compensation system is dangerously flawed if it doles out large incentive payments in cash for short-term performance, without any clawback provision or refund should subsequent performance undo this short-term performance.

So called pay-for-performance compensation systems rarely take into account the risks involved in achieving some level of performance. These compensation systems, which were pushed hard by institutional investors and compensation consultants, actually motivated management to take lots of undisclosed, hidden risks on their way to their performance bonus.

The US Congress and the Obama administration are moving carefully on regulating executive compensation. The population’s ire is palpable and politically charged, but the financial industry donates a massive amount of money to political campaigns and employs a large and effective contingent of lobbyists in Washington.

So the Dodd-Frank Act includes several fairly mild stipulations on matters of compensation including these:

- Financial firms must submit the compensation of their executives to a nonbinding vote by shareholders. This so-called ”say on pay” measure has become a favourite rallying cry for champions of a certain type of corporate governance; it is believed, though many are skeptical, that the fear of embarrassment by a negative vote will motivate boards of directors to adopt more prudent, less extravagant programs of executive compensation.

- The ratio of the chief executive officer’s compensation relative to that of the median compensation of all other employees (excluding the chief executive officer) must be disclosed. This rather novel requirement demonstrates some concern with the equity of compensation structures within companies.

- Compensation plans must include a clawback provision for variable compensation if the company has to restate past earnings due to some breach of accounting rules.

- The company must disclose whether executives, directors and employees may resort to derivatives to minimize their downside risk on their shares and stock options of the company. The EU Commission is proposing to prohibit the use of derivatives to this end.

- Finally, the Dodd-Frank Act contains a broad stipulation that could change the rules of the game: Not later than nine months after the date of enactment of the Act, the appropriate federal regulators jointly shall prescribe regulations or guidelines to require each covered financial institution to disclose to the appropriate federal regulator the structures of all incentive-based compensation arrangements offered by such covered financial institutions sufficient to determine whether the compensation structure: (1) provides an executive officer, employee, director, or principal shareholder of the covered financial institution with excessive compensation, fees, or benefits; or (2) could lead to material financial loss to the covered financial institution.

No doubt, the US regulatory agencies will be subjected to enormous pressures by financial institutions between now and April 2011 to frame this article in appropriate ways for them, certainly to steer the regulators toward ”guidelines” rather than ”regulations.”

In a document entitled ”Principles for Sound Compensation Practices,” the FSB proposed nine principles and 19 standards that should guide compensation policies.

On July 7, 2010, the European Parliament adopted a directive (CRD III) that broadly reflected the principles outlined by the FSB. The proposed principles, which were transformed into European Union directives, apply to hedge funds and private equity funds.

These principles focus more than the Dodd-Frank Act does on (1) the rules and guidelines on compensation apply not only to executives, but also to any employee with risk taking responsibility; and (2) rules are set for the portion of variable compensation, which must be held back and paid over future years.

Canada, a G20 member and an important participant on the FSB, has to implement the compensation principles. However, those principles may be put in place either through regulations or through supervision (or a combination of both, as in the United States).

Canada, with China, Spain, Japan and Hong Kong, chose an approach that is exclusively and entirely based on the supervision and oversight of compensation practices of Canadian financial institutions.

In short, excessive, misaligned compensation, which caused or at least amplified the financial crisis, has led governments to intervene in an area that hitherto had been the responsibility of boards of directors, signalling a lack of confidence in boards’ competence and vigilance in matters of compensation.

The Dodd-Frank Act, the FSB principles and the EU directives all insist that variable compensation should be linked directly, linearly and mathematically, if possible, to financial performance. This is unhealthy and may lead to problems in years to come. It speaks of a vision of the company as entirely dedicated to creating value for shareholders; it wrongly assumes that senior management’s performance can be reduced by some quantitative measure. The FSB principles do try to loosen the link between short-term performance and compensation, but the rules or guidelines will be easily deflected and circumvented.

Conclusions. The financial crisis is slowly fading away, leaving in its wake chastised regulators, unrepentant financial actors, vanishing culprits, sobered-up investors and a bewildered citizenry.

Clearly, the effectiveness of the new regulatory framework will depend on the actual rules, yet to be formulated, that will give substance to the stipulations of new laws and regulations; for this reason, what is in front of us is at best a work in progress.

Some of these measures will help ensure that the banking sector serves as a shock absorber, instead of a transmitter, of risk to the financial system and broader economy.

There is little doubt that, taken together and when fully implemented, the measures proposed in the United States, Europe and Canada will lower the probability that the world will experience another financial crisis of the same type and with similar origins as the 2007-08 crisis.

One or another of the various regulatory agencies has tackled, in some fashion or another, the ”immediate” causes of the crisis. Whether by new laws, new regulations or new supervisory guidelines, most participants in the international financial system are now, or will soon be, operating in a very different context.

Yet, one cannot escape a sense of futility about this massive effort, a sense that it does not address the fundamental causes of these recurrent crises, that it is mere preparation to fight the last war.

Nothing in what is proposed really changes the character of financial systems, the motivations that drive them, the greed that infects them. Thence will come the next crisis.