There is the story of the old college graduate in economics who went back to his alma mater to visit his son, who was following in his footsteps. The son was showing his examination paper and the father was astounded to find that it was exactly the same paper he had sat for 30 years before. So he went to the head of the economics department and confronted him with the discovery he had just made. “What kind of a department,” the man asked, “is this that sits the same papers, asks the same questions of students year after year?” “Well,” said the professor, “the questions don’t change but the answers do.”

So if there’s one thing that Couchiching has provided over the past 78 years or so, it’s just that: answers. And in doing so, your 2010 organizers, panellists and presenters, those here to observe, are acting in the best traditions of Couchiching — you are punching above your weight.

Canadians, when they consider our nation’s economic performance, both leading up to the crisis of 2008 and after, have also been punching above our weight as a nation. We just don’t like talking about it. I’ll break with that very Canadian mould today. I will actually say it: by any economic indicator, Canada is punching above its worldwide economic weight class.

It brings me particular pleasure to say this so soon after, to paraphrase the theme of this conference, a watershed event for this country — that is, the economic summits in Canada that brought world leaders together to set a course for strong and sustainable economic growth. Canada played a pivotal role in drawing out this road map to recovery, both in what we did to prepare for a global crisis and the way we responded when it arrived. It only makes sense then for me to recount the extraordinary events of recent years at this forum that was around during the last great global crisis of this magnitude in the 1930s.

Over the past couple of years, we have witnessed and, I believe, made history of our own. Just as this institution has done, our nation has once again answered the call in global efforts to make the world a more stable place for all. And if that isn’t a nation of 33 million punching above its weight, I don’t know what it is.

Now it is important to put the economic crisis that the world has faced in context, and I’ll try to do that fairly briefly. If we go back to August 2007, it was a time when the threatening credit crisis…manifested itself in the form of a subprime mortgage crisis in the United States. By the middle of the next year, certainly by October 2008, the crisis had grown exponentially and reached into the real economies. The world faced potentially the most serious economic crisis since the Great Depression. By later that fall of 2008, the full effects of the crisis were being felt outside of the credit markets as the recession hit the real economies.

Thankfully, in Canada we had prepared. We had run balanced budgets. We had paid off a massive amount of debt — some $40 billion during our government’s time in office since January 2006.

Our nation has once again answered the call in global efforts to make the world a more stable place for all. And if that isn’t a nation of 33 million punching above its weight, I don’t know what it is.

As the crisis intensified, we were on the campaign trail for the federal election that was held on October 14, 2008. The election was ongoing. The economic news was getting worse. Frequent discussions were being held internationally. I was speaking often with my counterparts, particularly in Europe and the United States, with the G7, regarding what should be done about a looming serious recession, one that was not foreseen by the economists.

In Canada, we took some immediate decisions to help alleviate the troubles in credit markets. First, we decided that we would purchase CMHC-insured mortgages to provide more liquidity in the system. Second, we decided we would guarantee the wholesale debt of our banks to enable them to have certainty as they lent to one another again, and to maintain a level playing field because other countries were guaranteeing the indebtedness of their banks.

I made that first announcement on Friday, October 10, 2008, in the morning in Ottawa. By that afternoon, I was in the Cash Room of the Treasury Building in Washington with the other G7 finance ministers and central bank governors. And let me say I’ve been to lots of these meetings over the course of four and a half years now. But this was a different kind of meeting.

The financial markets were teetering with uncertainty. Hank Paulson, who was the secretary of the treasury then, opened the meeting by saying, basically, We’re in a lot of trouble. Some of the European ministers spent some time expressing some pointed opinions about the US financial system and its contribution to the crisis, passing around a graph, a one-page graph, that showed what had happened: the widening of credit spreads dramatically since the failure of Lehman Brothers the month before.

As a group, we realized the reality that some heavily leveraged European banks were carrying toxic assets. Some British banks had failed. Some US banks had failed. Some German regional banks had failed. It was unclear in fact whether the markets would even open on the following Monday. So this was the dire situation on a Friday afternoon in October 2008.

But the story that weekend had a promising ending as it became really quite a glowing example of what can be accomplished with global cooperation. After the recriminations and the stridency, we tore up the communiqué. These communiqués, they’re rather dense documents prepared by public servants in advance of meetings, and they’re rarely read — frequently published. In this meeting, we actually tore it up, and that was one of the most important things we did. Leading up into that, we created a five-point plan. The five-point plan fundamentally was based on our agreement that we would not allow, as governments, any more banks to fail.

The next morning we met with President Bush at 7 a.m. in the Roosevelt Room of the White House. He agreed to the plan on behalf of the United States. He went out to the Rose Garden and gave a press conference endorsing the plan. And on the Saturday we had meetings with the International Monetary Fund. Later in the afternoon, the Council of the Finance Ministers of the Americas — South America, Central America and North America — we met and we all endorsed the plan. And then that evening, on the Saturday evening in Washington, the G20. And President Bush attended for part of that meeting as well, and the G20 ministers endorsed the plan as well. So that by Saturday evening we had global economic agreement on the five-point plan.

We then started the sequence of G20 summit meetings in Washington in November 2008, then in London in April 2009, in Pittsburgh in September of last year and, as you know, in Toronto in June and in Seoul, Korea, later this year in November.

In Pittsburgh, the leaders agreed that the G20 would serve as the premier forum for international economic cooperation, with a clear mandate to continue its prominent role well beyond the economic crisis.

In Toronto, we set our sights equally high: on ensuring the world’s economy would never come so close to crisis again. Prime Minister Harper summarized the Toronto accomplishments after the summit. First of all — and this was not easy to obtain — firm targets for advanced economies on deficit reduction and reduced debt burdens. We agreed on specific targets: that is, countries would cut deficits in half by 2013 and stabilize or reduce debt-to-GDP ratios by 2016. We reached an agreement to move forward on the second stage of mutual assessments each country will undertake to achieve strong, sustainable and balanced growth. We agreed on higher and better-quality capital standards throughout the global financial system and an extension of our shared pledge not to introduce new barriers to trade over the course of the next three years.

This continued collaborative, long-term approach coming out of the Toronto summit makes for a future far more hopeful than the treacherous past we have just lived through.

Now of all the G20 countries, Canada has a particular reason for post-summit optimism in my view. Our country has weathered the deepest, most synchronized global downturn since the 1930s in far better shape than other major industrialized countries. The decline in our economic output was the smallest of our G7 counterparts. Now, in August 2010, Canada has virtually recouped a recession’s worth of economic decline. With more than 400,000 jobs created since July 2009, we have also recouped all of the jobs lost during the downturn. The IMF expects that Canada will be the fastest-growing economy among the G7 economies during 2010. At a time when other countries, including the United States, still struggle to get their economies back on track, this success cannot be put down to mere luck.

It is the so-called ordinary Canadians who deserve the most credit. Consumer confidence in Canada has remained relatively strong and picked up quickly as we came out of the three quarters of recession. One of my heroes, Robert Kennedy, once said, “Most of our fellow citizens do their best and do it the modest, unspectacular, decent, natural way which is the highest form of public service.”

We also owe our enviable position to how we prepared for the unexpected and how we coped for it when it arrived. Canada had the lowest total government net burden in the G7 at the outset of the crisis. In 2007, before the crisis, Canada’s net debt stood at 23 percent of GDP, which was less than half the G7 average at that point. This prudence means the G20 commitment to cut our deficit in half and reduce our debt-to-GDP ratio by 2016 is not only possible; we’ve already set the course to achieve it in our most recent budget.

Canada took other steps before the global downturn that continue to serve us well. Long before world leaders met to confront the global emergency, our government put in place permanent, broad-based tax reductions that helped position Canada to withstand a global downturn. Actions taken by the government since 2006, including those in the Economic Action Plan, provided $220 billion in tax relief over 2008-09 when the crisis was at its worst, and the following five fiscal years.

That means that as other nations — and this was the competitive aspect of this — that as other nations faced the prospect of tax increases due to unsustainable budget deficits, Canadians can benefit from tax relief that is both permanent and affordable.

We also made innovation a government priority virtually from the day we took office. This year in my budget we provided $1.4 billion in new science and technology funding, and when you go with the previous budgets, which are another $2.2 billion, we have another $4.9 billion in additional funding overall provided in Canada’s Economic Action Plan for innovation. This helps explain why Canada’s investments in higher education, research and development as a proportion of the economy are now the highest in the G7.

This preparation put us in a good position but the magnitude of the crisis required an extraordinary response. As the economy began to slow in December 2008 — and you’ll recall we had just had an election in Canada in the middle of October — we were reelected once again as a minority government and back to Ottawa and back at it. We decided to schedule the earliest budget date in Canadian history — January 27, 2009. We did the prebudget consultations on an urgent basis. It became quite apparent to me quite quickly, listening to small-business people, medium-sized business, larger-business people, people in the financial sector, people all across the country — certainly by the middle of December 2008, that we were in a deep recession. One can look back now at the statistics and see that the Canadian economy basically fell off a cliff in the last quarter of 2008, and worsened in the first quarter of 2009, which was the worst part of the recession.

So what of all of that and what does government do when faced with that reality? Well, we could have tried to muddle through, I suppose. We didn’t. We chose to act boldly and to act quickly and to develop the Economic Action Plan. We also took a lot of advice. I appointed an Economic Advisory Council, chaired by former BC Finance Minister Carole Taylor, to give us urgent advice on steps we ought to take, and I can tell you that when I met with them for the first time in December 2008, they encouraged me to act boldly and quickly because of what they were seeing in the Canadian economy and the global economy as well.

We also had the auto issue at that time in December 2008 — very important to people here in Ontario and for the Ontario economy, of some importance in the riding I represent of Whitby-Oshawa. And we certainly dealt with that. And that was a difficult policy decision for government too. You know, how much does one want to get involved in the private sector? And I’d be happy to talk more about that later on. As you know, General Motors is making a significant comeback. If this continues, it’s going to look like we made the right policy decision. So I’m happy to see General Motors and I hope Chrysler is coming back as well. As you know, General Motors has begun to repay the debt to the Canadian people.

We can see the data in retrospect now about the depth of the recession at that time. Our view at the time was that we needed to act boldly and quickly and that if we did not, there were two great risks. One was we would have a longer, deeper recession in Canada. And the other was that we would have very substantial unemployment, double-digit unemployment in our country, which has been seen elsewhere. As it is now, our unemployment rate is about 8 percent. The American unemployment rate is about 9.5 percent. This reflects well on our country, and about our fiscal fundamentals, because that gap has not existed since 1975, which is an important difference reflecting, I think, economic differences, fundamental differences between our government’s fiscal situation and that in the United States.

In any event, we went ahead with the Economic Action Plan. It is a two year plan. It fit well with the G20 context because we had agreed with the G20, all of the leaders had, that we would all seek to have stimulus put into our economies of about 4 percent of GDP over the course of two years. Now in Canada, in the federation of course, we needed the cooperation of the provinces and territories to do that. And during all of this time about which I have been speaking, I was on the phone conferencing regularly with my provincial and territorial colleagues. And I must say the cooperation was very substantial. Almost all the provinces and territories in Canada went ahead and participated in the infrastructure plan so that we did fulfill, Canada fulfilled its G20 commitment of more than 4 percent of GDP over the four years.

And there’s much talk now about exit strategies. We built in an exit strategy in the Economic Action Plan, an end to the stimulus measures at the end of the two-year period, which we said right at the beginning to everybody: that the spending will end on the infrastructure projects at the end of the fiscal year March 2011. We have targeted measures to limit growth in direct program spending and a comprehensive review of our overhead costs in government. So we have a three-point plan that will place our net debt ratio on a clear downward track when the debt burdens of other nations are expected to escalate even higher.

So the competitive advantage to Canada: we can afford to reduce taxation. We’re stimulating our economy. Our competitors are going to have to raise taxes going forward, a clear economic advantage for Canada. Our debt-to-GDP ratio is much better than our competitors in the Western industrialized economies.

So we have a good brand. Canada today is in a position other nations can only envy and I have to say that I’ve observed that first-hand.

I do want to leave you with a sense of how others see us. In recent months, preparing for the G7, G8 and G20 meetings, I travelled a lot to China and India, of course the United States, Korea, South America. And I can tell you that Canada is viewed in a way that can only be described as admiration. When I went to New York a few days before the Canadian summits, the same day we did the most recent update on the Economic Action Plan, I was able to highlight that Canada was not only hosting the world, it was leading it. By several key measures — job creation, economic growth, the stability of our financial sector, relatively low public debt — Canada is performing markedly better than most advanced economies and all G7 nations.

On the fiscal side, the IMF expects Canada will be the only G7 country to return to balance in the next five years. I’ll just give you a couple of numbers here to give some sense of where we are. The IMF projects our net debt ratio in Canada will stand at 31 percent of GDP in 2015. By way of contrast, the US debt-to-GDP ratio is about 67 percent. The United Kingdom’s is about 75 percent. Japan’s is about 115 percent. All of these are likely to worsen — except ours — over the course of the next several years, another important advantage for Canada.

So this made-in-Canada resilience in weathering the global recession is also a testament to the stability of Canada’s financial sector, not to mention the prudence of Canadians themselves. Canada’s banks [and] our other major financial institutions were better capitalized, less leveraged than their international peers going into the global recession, in part reflecting a strong financial regulatory and supervisory framework. And attitudes changed because of data like that and a strong regulatory system and the global crisis.

The first time I went to China as Canada’s minister of finance was in January 2007. And several times in meetings with my counterparts there, they alluded to the fact that the Canadian banks were risk averse, too risk averse, not willing to take on enough challenges. “Boring” was used. “Timid” was another word that I heard, at least in translation.

I was back in China in August of 2009 and then about six weeks or so ago. And now when the same counterparts were talking to me about the Canadian banks and financial institutions, they were using words like “wise,” “prudent,” “stable,” “solid.” And, as you know, there are substantial investments being made by certain Asian countries in our country.

The World Economic Forum has ranked Canada’s banking system as the soundest in the world for two consecutive years. Combined with that stability is a highly competitive business tax system and our commitment to free trade. This is making Canada increasingly attractive to investors and entrepreneurs — the best place to do business in the next five years in fact, according to the Economist Intelligence Unit. And, as I say, Canada’s tax advantage will only grow as our tax rates continue to fall through 2012 — a major competitive advantage.

And it is a federal advantage because we challenged the provinces and territories several years ago to join us in making Canada a more attractive place to invest by reducing the business tax burden, to try to get to 25 percent overall. When we started in 2006, the federal business tax rate was a little bit over 22 percent. It is down to about 18, a little bit more than 18 percent now. It’ll be down to 15 percent by 2012-13. Most of the provinces are moving in the direction of getting their business tax rate at the provincial level to 10 percent — 15 percent federally, 10 percent provincially. A brand for Canada: 25 percent business tax rate overall. And, as I say, there’s been terrific cooperation by the provinces and territories to get to that place.

We also in the budget this year not only promoted free trade, we eliminated tariffs on imported machinery and manufacturing inputs, in the process becoming the first G20 nation to become a tariff-free zone for manufacturers. So [we] don’t just say that we believe in free trade; we take actions that are consistent with the policy perspective.

That is why it is becoming increasingly clear to the international observers that the initiatives put in place since 2006 are making Canada much more competitive internationally.

So it adds up to a future that looks far more promising than what could be talked about only a couple of years ago.

To turn to Robert Kennedy again, who I was privileged to hear a long time ago when I was an undergraduate at Princeton, he reminds us, “History is a relentless master. It has no present, only the past rushing to the future. To try to hold fast is to be swept aside.”

In terms of financial sector reform, Canada will keep working to build on the momentum that occurred in Toronto. That means keeping the global focus on what matters: quality and quantity of capital; the definition of capital; leverage ratios. These are issues that are being discussed intently now and we hope to have a solution, solutions on both issues ready for the leaders when they meet in Seoul in November of this year.

We will continue on our efforts on the quality issue and on the leverage issue with our colleagues. We will do so with the same tenacity that Canada demonstrated in dousing the attempts to introduce what we viewed as a misguided and punitive global tax on the financial sector. And, as you know, we were successful in having the majority of the G20 agree with Canada on that issue.

For Canada and all nations, our work is far from finished. Much more effort and determination is required if we are to make the Canadian summits the economic legacy they deserve to be.

We have a Canadian advantage. We have come too far and achieved too much to fall back into the complacency that allowed the global economy to be thrown into turmoil. Canadians should be proud that our country played such a pivotal role in overcoming a global downturn, yet we cannot let up now when our nation is increasingly being called upon to show global leadership.

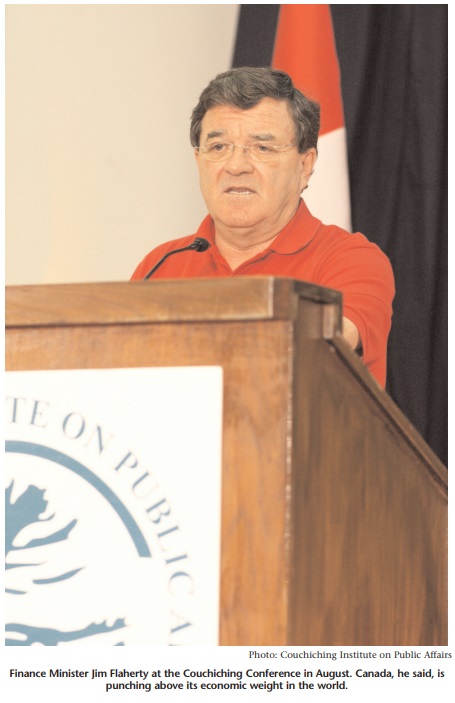

Excerpted from a keynote address to the Couchiching Conference in Orillia, Ontario, August 6, 2010.

Photo: Shutterstock