The federal Liberal party made a big announcement on Monday–a new Canada Child Benefit to replace and build on the existing child benefit framework. I already wrote a lengthy analysis for Maclean’s here, so this Policy Options post just provides a supplemental discussion on one of the nerdy details of the proposed program–the effect on marginal tax rates.

I should note that I provided some technical advice to the Liberals on this proposal–you can read my disclosure here.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

Economist Jack Mintz raised the issue of the impact the new benefit would have on effective tax rates in the National Post today. Income-tested benefits are designed around ‘phase-out rates’. If you earn an extra dollar, not only do you pay income tax on that dollar but you also lose a few cents from your refundable tax credit. This tax credit phase-out stacks on top of the income tax rates to produce what can be very high effective tax rates on income.

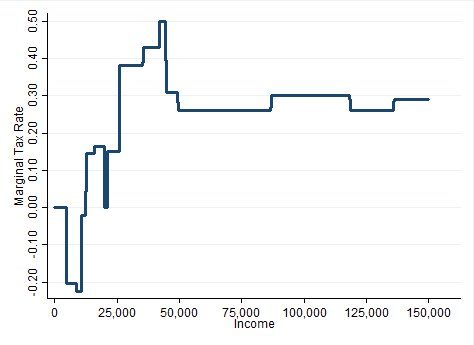

To illustrate, here is a chart of the effective tax rate on a single person with two kids in 2015. At each point of income, the graph shows how much combined income tax and credit phaseout is incurred. The big bubbles at modest income levels are driven not by the income tax brackets, but by the phase-out of all the refundable tax credits, including the GST/HST credit, the Working Income Tax Benefit, the National Child Benefit Supplement (NCBS), and the Canada Child Tax Benefit (CCTB). It is complicated!

The new Liberal proposal aims to ease this complication by combining the CCTB and NCBS with the UCCB to produce the new Canada Child Benefit. What will be the impact of this on the marginal effective tax rate? I modeled the phaseout rates for the existing NCBS/CCTB and the new Canada Child Benefit in a spreadsheet here. Of note, the UCCB was by nature universal and did not have any associated phase-out rate.

The easiest way to see what’s going on is simply to compare the phaseout rates under the existing NCBS/CCTB package to the new Canada Child Benefit. I’ve assumed here that all kids are over age 6.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

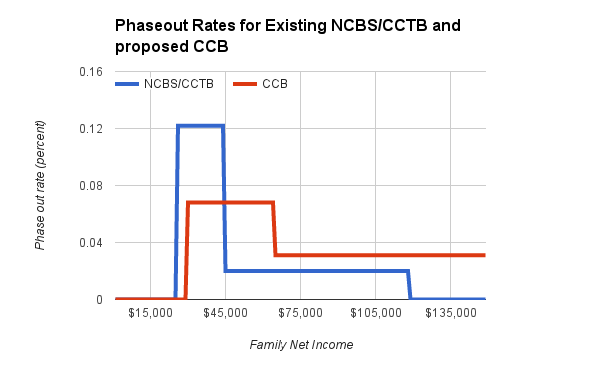

Here is the graph for a one child family. The existing system has a phaseout rate of 12.2% up to $45,000; then 2% after that. The proposed Liberal plan decreases this rate to 6.8% up to $65,000 then 3.1%. The big bump is smoothed out–but at the cost of slightly higher rates farther up the income distribution.

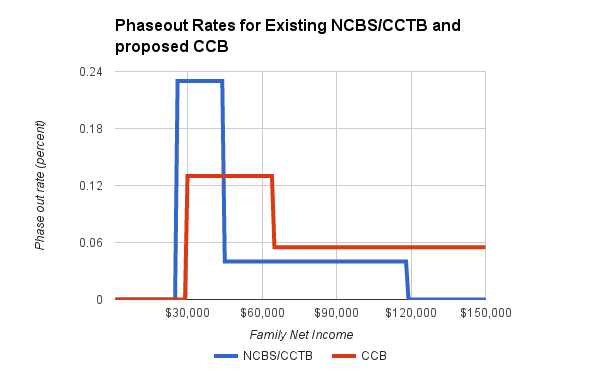

The same pattern can be seen for two-child families. The bubble is smoothed out.

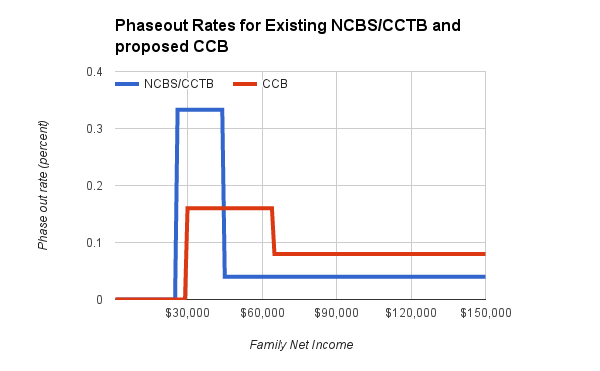

Finally, for three child families, the current NCBS phaseout rate of 33.3% is tamed down to 16%, but higher earners now face 8% instead of 4%.

What does all this mean? Economists have determined that the negative impact of taxes on efficiency increases at the square of the rate of tax–which means that very high tax rates are much more costly than moderate tax rates. If so, then smoothing out the NCBS bubble might be helpful. On the other hand, a higher earner with two kids now faces a 5.5% phase out rate rather than 4%, so there is some downside.