The recent drop in oil prices is a major shock to the Canadian economy. It’s caused the government to delay the federal budget, and it’s a key reason for the Bank of Canada’s surprise interest rate cut.

The Bank’s move is fascinating precisely because central banks generally avoid surprises. (Though, this past week alone has seen three bold and unexpected central bank actions: Canada’s rate cut, India’s, and the Swiss abandoned currency target.) The rationale the Bank of Canada gave was to provide “insurance” against downside risks.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

What are these downside risks for Canada’s economy and how big are they? Recently, economists have been busy putting numbers to these questions and the Bank’s Monetary Policy Report (MPR) provides a glimpse at some of their work.

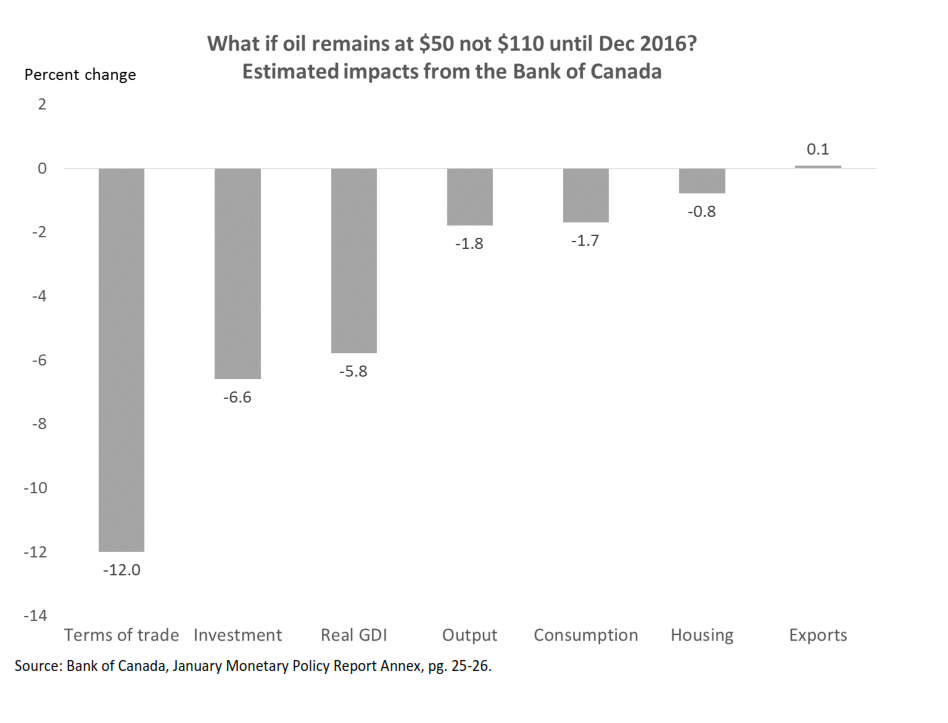

Just over six month ago, oil was trading around US$110 a barrel. It has since fallen below $50. In the Annex of the MPR, the Bank estimates the potential size of this shock. It models a “bad state of the world” for the Canadian economy over the next two years — assuming oil prices stay at $50 and the Bank of Canada leaves rates unchanged, relative to a case where oil continued to trade at the original $110 over the projection. While neither scenario is likely to play out in practice, the economic impacts of the differences are instructive:

In the bad state, Canada would endure a large terms of trade shock (-12%), which would significantly reduce Canadians’ overall incomes, their international purchasing power and domestic demand. (In fact, elsewhere in the MPR, the Bank says that lower oil prices reverse about one-third of income gains associated with our improved its terms of trade since 2002, when commodity prices began their ascent). In the bad state, a decline in energy-related capital spending occurs quickly, making investment the hardest hit GDP component. It falls by roughly 6% as does real gross domestic income (GDI); output is nearly 2% lower.

In the bad state, Canada would endure a large terms of trade shock (-12%), which would significantly reduce Canadians’ overall incomes, their international purchasing power and domestic demand. (In fact, elsewhere in the MPR, the Bank says that lower oil prices reverse about one-third of income gains associated with our improved its terms of trade since 2002, when commodity prices began their ascent). In the bad state, a decline in energy-related capital spending occurs quickly, making investment the hardest hit GDP component. It falls by roughly 6% as does real gross domestic income (GDI); output is nearly 2% lower.

The inner workings of government

Keep track of who’s doing what to get federal policy made. In The Functionary.

The Functionary

Our newsletter about the public service.

Nominated for a Digital Publishing Award.

On the upside during the global energy price boom, the Canadian economy reallocated production to energy-producing sectors and regions and away from the manufacturing sector. On net, I think these impacts benefited Canada, but they entailed significant economic adjustment costs.

Alternatively, on the downside if there were a prolonged energy price bust, the sectoral and regional adjustments would reverse. This too would bring adjustment costs and perhaps one additional wrinkle, as my IRPP colleague Tyler Meridith notes, the new (manufacturing) jobs that would be created are not necessarily the same as the (resource) jobs they effectively replace — they may pay less.

Thus, one could assume that the Bank ran its base-case projection with flat oil prices and they didn’t like what they saw. Deciding to cut rates when few expected it, is a gamble. The thinking seems to be that this calculated risk will offer some monetary stimulus now. And by lowering borrowing costs and depreciating Canada’s currency, it effectively “buys some insurance” to mitigate that bad future state of the world for Canada — of persistent low energy prices and the economic adjustment it would require. Will it work? It’s too early to tell. But one thing is clear: a few bold central bankers have recently lost their traditional fear of surprising people.

Stephen Tapp is a Research Director at the IRPP. Follow him on Twitter @stephen_tapp or e-mail him at: stapp@irpp.org.